Sample Category Title

EUR/GBP Fading

EUR/GBP continues to bounce higher yet not important resistances have been broken (quick test). The pair is back below former resistance at 0.8899 (19/09/2017 low). Hourly support is given at a distance at 0.8746 (27/09/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

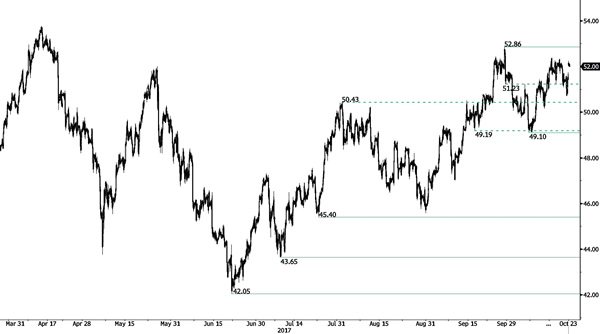

CRUDE OIL Messy Recovery Bounce

Crude oil bounced hard back within range defined by support at 50.43 and the strong resistance lies at 52.86 (28/09/2017). Expected to show continued increase within this range.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Reversal Ahead Of Resistance

Silver is again weakening and is now resting on support at 16.94. Hourly resistance is given at 17.46 (13/10/2017 high). Additional support can be found at 16.13 (06/10/2017 low). Hourly resistance can be found at 17.10 (intraday high).

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Fading Bullish Momentum

Gold remains weak as broken the support at 1284 confirms an underlying bearish trend. Strong support lies at a distance at 11267 then 1204 (10/07/2017 high). Resistance is located at 1288 (20/10/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

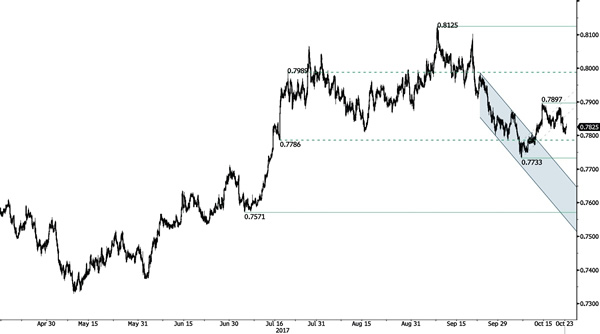

AUD/USD Drifting Lower

AUD/USD broke out of sideways range by moving below support at 0.7821. Fading supply indicated a weak test of support at 0.7786. Hourly resistance is given at 0.7897 (13/10/2017 high). Key support lies at at 0.7733 (06/10/2017 low). Expected to show continued consolidation.

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

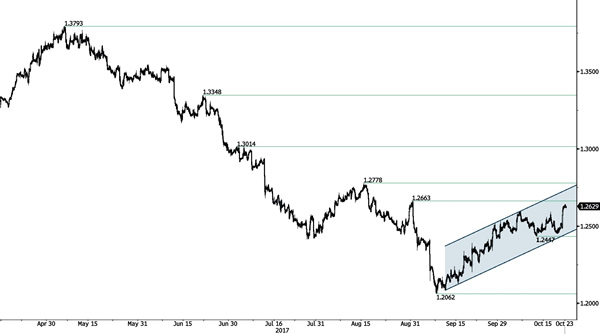

USD/CAD Preparing To Challenge 1.2663

USD/CAD bullish drive suggest a challenge to 1.2663 horizontal resistance. Hourly support lies at 1.2331 (26/09/2017 high). Expected to show continued short-term bullish pressures within uptrend channel.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head further lower.

USD/CHF Pause In Bullish Momentum

USD/CHF has paused after breaking resistance at 0.9838. The technical structure suggests an improving short-term buying interest. Expected to show continued bullish pressures within uptrend channel. Hourly support stands at 0.9712 (12/10/2017 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/JPY Bullish Surge Continues

USD/JPY jumped thru resistance located at 113.44. Next key resistance can be found at 114.49 (11/07/2017 high). Support is located at 111.12 (20/09/2017 low).

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Recovery Bounce Underway

GBP/USD has successfully tested support at 1.3155 bouncing strongly to resistance at (1.3228 reaction high). Hourly resistance stands at 1.3338 (13/10/2017 high). Key support can be found at 1.3122 12/10/2017 low).

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Testing Rising Trendline

EUR/USD is resting on key support at 1.1758. Break will trigger bearish extension to strong support is given at a distance at 1.1662 (17/08/2017 low). Key resistance is located at 1.1878 (12/10/2017 high). Expected to show some short-term consolidation.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).