Sample Category Title

Barnier Comments Push Sterling of a Cliff

- European equities trade narrowly mixed, with the exception of the FX-sensitive FTSE that reached a 5-month high. US equities open with slight losses. JPM and Citi go modestly higher after earnings results.

- The EU's chief Brexit negotiator has said talks with the UK over its exit bill have hit a "deadlock" and he will not tell EU leaders that "sufficient progress" has been made to accelerate talks from divorce to trade negotiations next week. EUR/GBP surged back north of 0.90 for the first time since mid-September.

- EMU industrial output rose by far more than expected and at its highest rate in nine months in August as production of capital goods, such as machinery, rose sharply, boding well for economic growth in the second half of the year. Overall output rose 1.4% M/M and 3.8% Y/Y in August.

- The number of Americans filing for unemployment benefits fell to more than a one-month low last week (243k) as claims in Texas and Florida continued to decline after being boosted by Hurricanes Harvey and Irma. US producer prices rose by the most in six months in September (0.4% M/M & 2.6% Y/Y) as the price of gasoline recorded its biggest increase in more than two years amid production disruptions at oil refineries in Texas caused by Harvey.

- JP Morgan's quarterly profit and revenue easily trumped Wall Street's expectations, but a slump in bond trading clouded gains from loan growth and higher interest rates. Citigroup reported a 7.6% increase in quarterly profit from a gain on an asset sale, lower costs and better-than-expected trading revenue.

- Swedish inflation fell short of estimates, as some suggested price growth may have peaked around the central bank's target. Underlying consumer prices, which adjust for changes in mortgage costs, rose 2.3% Y/Y in September, unchanged from the previous month and less than the 2.5% Y/Y predicted. EUR/SEK rose towards 9.60.

- British lenders are planning the biggest cutback in consumer loans in nearly 10 years, the BoE said, after it warned repeatedly about the strong pace of lending to households.

- The ECB should not keep interest rates low for too long and should tighten policy quickly during an economic upturn, ECB Weidmann said: "the monetary policy taps should be turned off in a quick and consistent manner."

Rates

Core bonds lack direction

Consolidation on core bond markets continued today. Both the German Bund and the US Note future eke out small gains on a daily basis. The US Note future temporarily lost ground on strong PPI data, but the move didn't last long. We might get a stronger reaction if tomorrow's CPI data are higher than forecast.

At the time of writing, US yields decline 1.4 bps to 1.8 bps across the curve with the belly slightly outperforming. German yields decline by 0.9 bps (30-yr) to 2.3 bps (5-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany narrow up to 3 bps (Italy). Italian BTP's outperform following a good auction (see below) and as the lower house approved via 3 confidence votes changes to the electoral law. It allows parties to form coalition ahead of elections and is considered to be negative for the anti-euro 5SM party of Beppe Grillo. It now goes to the Senate.

The Italian debt agency issued a new 3-yr BTP (€4B 0.2% Oct2020) and tapped the on the run 7-yr BTP (€2B 1.45% Nov2024) and 30-yr BTP (€1.5B 3.45% Mar2048). The combined amount sold was the maximum of the targeted €6-7.5B with an auction bid cover of 1.59 which is strong for Italian standards. The US Treasury ends its refinancing operation with a $12B 30-yr Bond auction. The WI currently trades around 2.88%.

Currencies

Dollar decline halts, awaiting tomorrow's data.

Today, the USD bottomed after a decline in past days. The swings in EUR/USD and USD/JPY were again modest. A further decline in US jobless claims and rise in the core US PPI were also slightly supportive for the dollar. EUR/USD trades in the 1.1845/50 area. USD/JPY hovers around 112.40. Tomorrow's US retail sales and CPI might decide whether there is room for sustained USD gains.

New record closing levels on WS supported equity gains in Asia overnight. However, the dollar didn't receive additional interest rate support. USD/JPY traded marginally lower despite strong equities. EUR/USD regained the previous 1.1823 range bottom and traded around 1.1875 ahead of European trading. The Spanish/Catalan crisis entered a period of 'distress' as the Catalan leaders have five days to clarify whether they declared independence. The euro still felt no negative fall-out from the Catalan crisis.

There was no obvious story to guide (FX) trading in Europe. EUR/USD declined slightly off the overnight top in Asia, but the moves in EUR/USD and USD/JPY remained modest. EMU production data were very strong. However, the report is outdated and had no lasting impact on the euro. We also didn't see any 'new news' on Catalonia.

In the US, the focus turned to the eco data. The US jobless claims declined more than expected. The headline PPI was in line with the consensus (0.4% M/M and 2.6% Y/Y), but PPI core inflation rose more expected from 2.0% to 2.2% Y/Y (a stabilisation was expected). The dollar gained a few ticks after the release but the move stalled soon. EUR/USD trades in the 1.1840/50 area. USD/JPY is changing hands in the 112.40 area. Tomorrow's US retail sales and CPI might decide whether there is room for an more protracted USD up-leg.

Barnier comments push sterling of a cliff

There were few eco data in the UK. However, Brexit again came to haunt sterling. At the end of the fifth round of negotiations between the EU and the UK, EU Brexit negotiator Barnier said there weren't any great steps forward. The state of the negotiations doesn't allow him to recommend the start of talks on post-Brexit UK/EU trade relationships at next week's EU summit. It was no secret that the Brexit talks hadn't yield much progress yet. However, Barnier spoke very harsh on the financial separation bill as he said the negotiations on this topic were in a deadlock. So, any talks on trade are likely delayed till after the next EU summit on December 14. The comments pushed sterling off a cliff. EUR/GBP jumped north of the psychological barrier of 0.90. The pair trades around 0.9010/20. Cable also reversed part of this week's rebound. The pair trades again in the 1.3140/50 area.

US: Producer Prices Point to Firming Inflation

Higher energy prices and the volatile trade services component drove the PPI up 0.4 percent in September. Core goods and services prices rose more modestly, but are within the realm of the Fed's inflation target.

Energy and Trade Services Lead September Gain

Producer prices climbed 0.4 percent in September on another sizable lift in the cost of energy goods (up 3.4 percent). Food prices were flat, while core goods rose 0.3 percent.

The 0.4 percent rise in services last month was largely traced to a 0.8 percent rise in the trade component, which is measured in margins. Transportation services, which can be susceptible to fluctuations in energy costs, rose 1.0 percent.

PPI Consistent with Moderate Inflation

Construction costs were little changed in September (up 0.1 percent), but will likely see the upward trend of recent months continue as rebuilding efforts in the Gulf region get underway.

While not the Fed's primary measure, the PPI has firmed over the past year and is in the realm of the FOMC's 2 percent goal. PPI is up 2.6 percent year-over-year while our preferred measure of the core (ex-food, energy, and trade services) is up 2.1 percent.

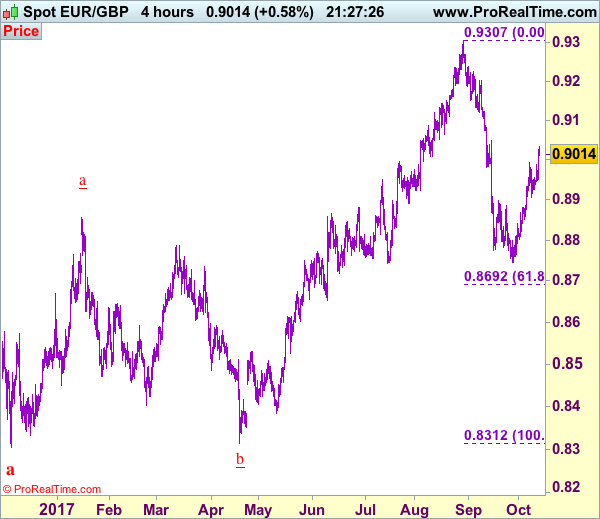

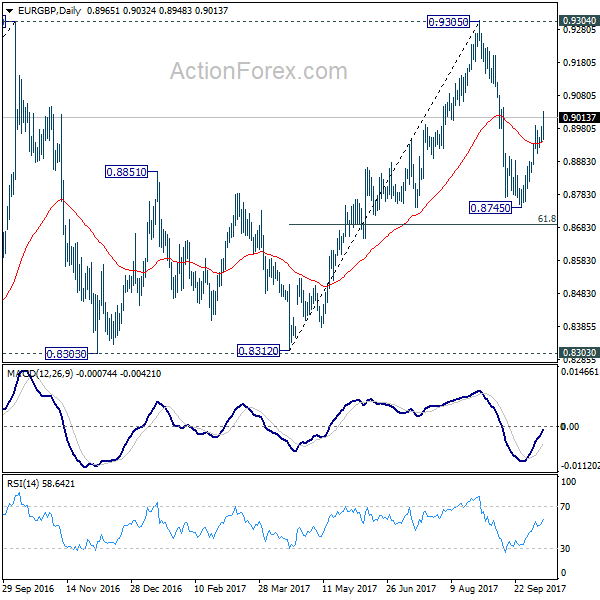

Trade Idea: EUR/GBP – Buy at 0.8985

EUR/GBP - 0.9012

New strategy :

Buy at 0.8985, Target: 0.9085, Stop: 0.8945

Position : -

Target : -

Stop : -

As the single currency has surged again after brief pullback and broke above previous resistance at 0.8993, suggesting the rise from 0.8746 low is still in progress, hence mild upside bias is seen for this move to extend further gain to previous resistance at 0.9048, break there would encourage for at least a strong retracement of the fall from 0.9307 to 0.9075-80 but near term overbought condition should limit upside to 0.9100, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback as 0.8985-90 should limit downside and bring another rise. Below minor support at 0.8949 would suggest top is possibly formed, risk test of 0.8925 but only break support at 0.8906 would confirm top is formed, bring further fall towards 0.8875, having said that, support at 0.8850 should remain intact. Only a break there would provide confirmation that the rise from 0.8746 has ended and extend weakness to 0.8820-25 first.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

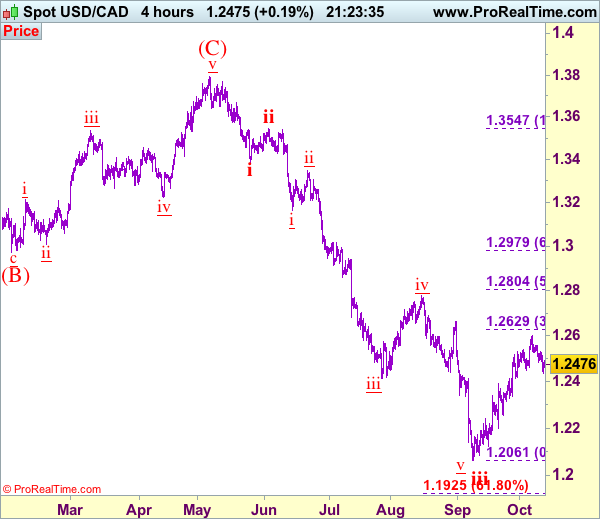

Trade Idea: USD/CAD – Buy at 1.2395

USD/CAD - 1.2478

Trend: Down

Original strategy :

Buy at 1.2415, Target: 1.2600, Stop: 1.2355

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.2395, Target: 1.2595, Stop: 1.2335

Position: -

Target: -

Stop:-

Although the greenback recovered after finding support at 1.2433, reckon upside would be limited to 1.2531 and near term downside risk remains for the corrective decline from 1.2599 top to bring retracement of recent upmove to 1.2415 but reckon 1.2390-95 would limit downside and bring another rebound later, above 1.2531 resistance would suggest low is formed, bring further gain to 1.2555-60, break there would signal the pullback from 1.2599 has ended, bring retest of this level, above there would extend the rise from 1.2061 low (wave iii trough) towards previous resistance at 1.2663 but upside should be limited to 1.2700 and price should falter well below another previous resistance at 1.2778.

In view of this, would not chase this rise here and would be prudent to buy again on pullback as 1.2395-00 should limit downside. Below 1.2395-00 would bring correction back to 1.2350-55 but reckon indicated support at 1.2313 would hold. Only a drop below 1.2313 would abort and signal the aforesaid rise from 1.2061 has ended, bring further fall to 1.2254 support, however, reckon downside would be limited to another previous support at 1.2197, bring rebound later. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction ended at 1.2778, wave v has reached our indicated downside target at 1.2100 and may extend to 1.2000.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.11; (P) 148.48; (R1) 149.12; More

GBP/JPY's recovery was limited at 149.04 and drops sharply after failing to sustain above 4 hour 55 EMA. But it's staying above 146.92 temporary low. Intraday bias remains neutral first. Another decline is expected with 149.73 intact. Below 146.92 will target 61.8% retracement of 139.29 to 152.82 at 144.45. Such decline is seen as a correction and we'd look for strong support from 144.45 to bring rebound. On the upside, break of 149.73 support turned resistance will argue that the pull back is completed and turn bias back to the upside for retesting 152.82 high. However, sustained break of 144.45 will put 139.29 key support in focus.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

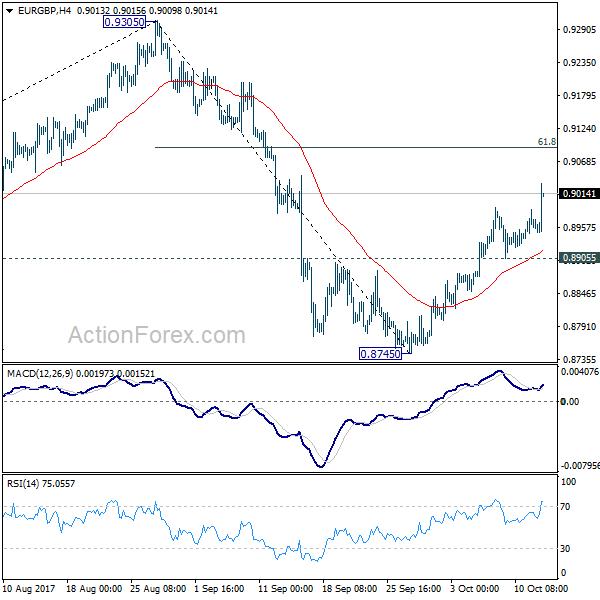

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8927; (P) 0.8941; (R1) 0.8956; More...

EUR/GBP's rise from 0.8475 resumes today and reaches as high as 0.9015 so far. Intraday bias is back on the upside for 61.8% retracement of 0.9305 to 0.8745 at 0.9091. Decisive break there will bring retest of 0.9305 high. On the downside, break of 0.8905 minor support is needed to indicate completion of the rebound. Otherwise, further rise will remain in favor in case of retreat.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of another fall. And in that case, EUR/GBP could have a retest on 0.9303 low. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

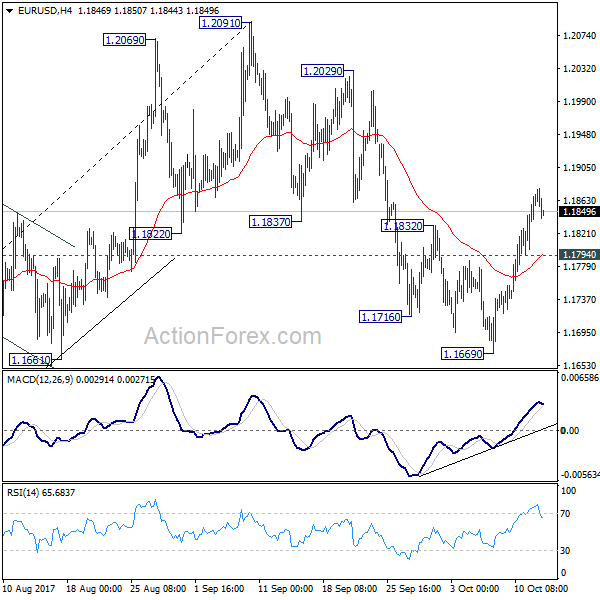

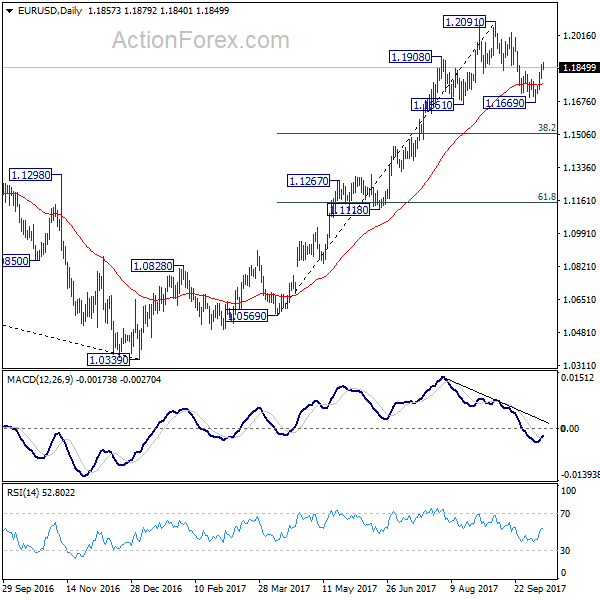

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1813; (P) 1.1841 (R1) 1.1888; More...

EUR/USD dips mildly after hitting 1.1879. But still, with 1.1794 minor support intact, intraday bias stays on the upside for further rally. As noted before, pull back from 1.2091 should have completed at 1.1669, ahead of 1.1661 support. Further rise should be seen to retest 1.2091 high. We'll be cautious on strong resistance from there to bring another fall to extend the consolidation. On the downside, below 1.1794 minor support will turn bias back to the downside and could extend the correction from 1.2091 through 1.1669.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

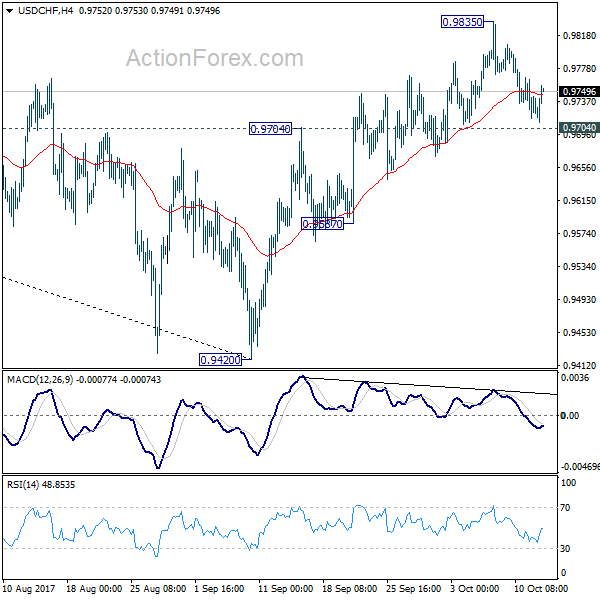

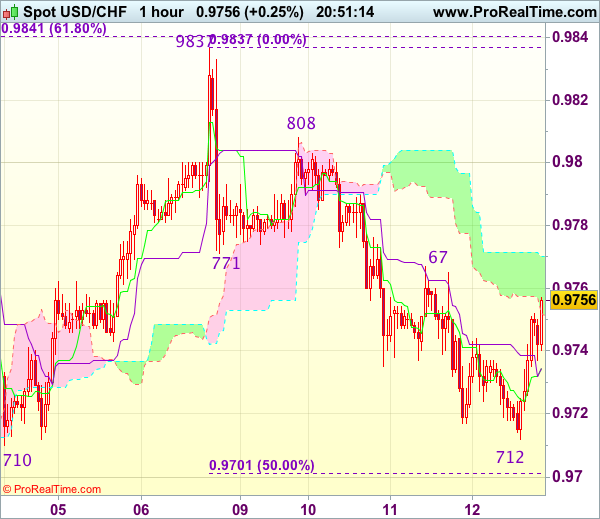

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9709; (P) 0.9737; (R1) 0.9759; More....

USD/CHF recovers ahead of 0.9704 support and intraday bias stays neutral first. Considering bearish divergence condition in 4 hour MACD, break of 0.9704 resistance turned support will argue that rebound from 0.9420 has completed. This will also mixed up the near term outlook and turn bias back to the downside for 0.9587 support. Meanwhile, break of 0.9835 temporary top will extend the rebound to 61.8% retracement of 1.0342 to 0.9420 at 0.9990.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

Trade Idea Update: USD/CHF – Hold short entered at 0.9755

USD/CHF - 0.9750

Original strategy :

Sold at 0.9755, Target: 0.9655, Stop: 0.9790

Position : - Short at 0.9755

Target : - 0.9655

Stop : - 0.9790

New strategy :

Hold short entered at 0.9755, Target: 0.9655, Stop: 0.9790

Position : - Short at 0.9755

Target : - 0.9655

Stop : - 0.9790

Although the greenback has rebounded after holding above previous support at 0.9710 and consolidation with initial upside bias is seen, reckon resistance at 0.9767-71 would limit upside and bearishness remains for the decline from 0.9837 top to resume after consolidation, below said support at 0.9710-12 would confirm and extend weakness to 0.9669-70 (61.8% Fibonacci retracement of 0.9565-0.9837 and previous support) but previous support at 0.9642 should remain intact due to oversold condition.

In view of this, we are holding on to our short position entered at 0.9755. Only break of resistance at 0.9808 would signal an intra-day low is formed and indicate the pullback from 0.9837 has ended, bring retest of this level later.

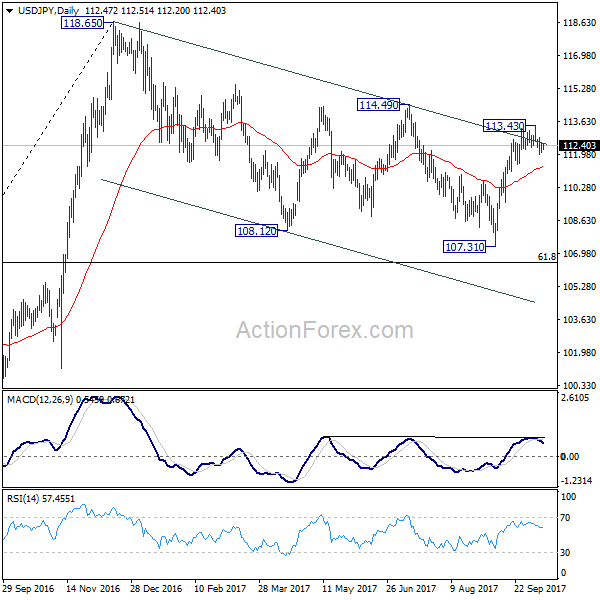

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.18; (P) 112.38; (R1) 112.69; More...

No change in USD/JPY's outlook. The fall from 113.43 short term top is expected to extend lower. Intraday bias stays on the downside for 55 day EMA (now at 111.35) first. Sustained break there will bring retest of 107.31. For now, risk will stays on the downside as long as 113.43 resistance holds.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.