Sample Category Title

Euro-Zone’s Sentix Investor Sentiment Hit A Decade High Level In October

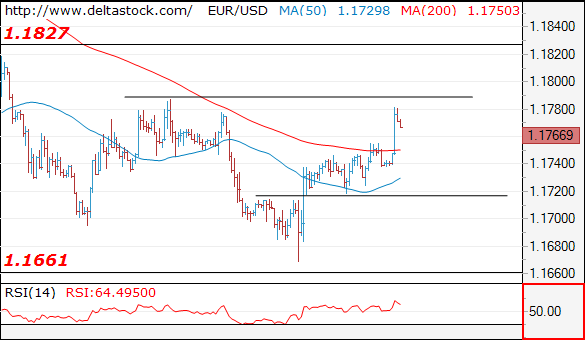

For the 24 hours to 23:00 GMT, the EUR marginally rose against the USD and closed at 1.1740.

In economic news, data showed that the Euro-zone's Sentix investor confidence index advanced more-than-expected to a level of 29.7 in October, notching a ten-year high level, suggesting that investors shrugged off worries of political instability across the common currency region. The index had recorded a level of 28.2 in the prior month, while markets had anticipated for an increase to a level of 28.5.

Separately, Germany's seasonally adjusted industrial production rebounded 2.6% MoM in August, growing at its quickest pace since July 2011 and hinting that industrial sector will remain one of the bright spots for the Euro-bloc's largest economy. Markets had expected industrial production to gain 0.9%, compared to a revised drop of 0.1% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.1770, with the EUR trading 0.24% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1733, and a fall through could take it to the next support level of 1.1695. The pair is expected to find its first resistance at 1.1795, and a rise through could take it to the next resistance level of 1.1819.

Moving ahead, investors will keep a close watch on Germany's trade balance figures for August, slated to release in a few hours. Moreover, the US NFIB small business optimism index for September, due to release later in the day, would be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

The Ball Is In The EU’s Court: Theresa May

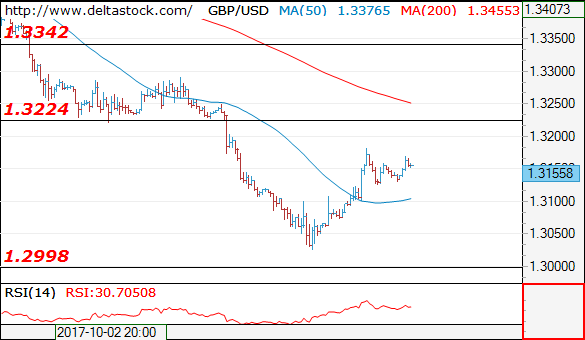

For the 24 hours to 23:00 GMT, the GBP rose 0.44% against the USD and closed at 1.3137, amid news emerged that the British Prime Minister, Theresa May, could reshuffle her cabinet and leave out Foreign Secretary, Boris Johnson.

Meanwhile, the UK Prime Minister, Theresa May, warned the British public to prepare for crashing out of the European Union (EU) with no deal, outlining contingency plans to avoid border meltdown for businesses and travellers. Further, May noted that UK would publish two white papers on trade and customs after Brexit.

In the Asian session, at GMT0300, the pair is trading at 1.3155, with the GBP trading 0.14% higher against the USD from yesterday's close.

Overnight data indicated that UK's BRC retail sales across all sectors recorded a rise of 1.9% on an annual basis in September, rising by the most this year and following a gain of 1.3% in the prior month.

The pair is expected to find support at 1.3095, and a fall through could take it to the next support level of 1.3036. The pair is expected to find its first resistance at 1.3199, and a rise through could take it to the next resistance level of 1.3244.

Trading trend in the Pound today is expected to be determined by the release of UK's industrial and manufacturing production data along with construction output and total trade balance data, all for August, slated to release in a few hours. Also, traders would eye UK's NIESR GDP estimate for the three months to September, due to release later in the day.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japan’s Trade Surplus Shrunk In August

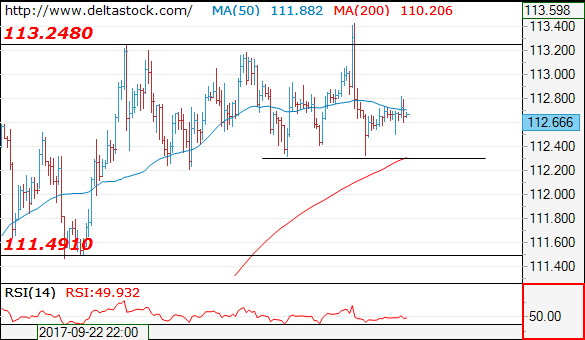

For the 24 hours to 23:00 GMT, the USD slightly rose against the JPY and closed at 112.66.

In the Asian session, at GMT0300, the pair is trading at 112.67, with the USD trading marginally higher against the JPY from yesterday's close.

Overnight data revealed that Japan's trade surplus (BOP basis) narrowed less-than-expected to ¥318.7 billion in August, compared to a revised surplus of ¥566.6 billion in the prior month. Market participants had anticipated the nation's trade surplus to narrow to ¥264.9 billion.

The pair is expected to find support at 112.51, and a fall through could take it to the next support level of 112.35. The pair is expected to find its first resistance at 112.83, and a rise through could take it to the next resistance level of 112.99.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average..

Swiss Franc Trading Higher, Ahead Of Swiss Unemployment Rate Data

For the 24 hours to 23:00 GMT, the USD rose 0.18% against the CHF and closed at 0.9798.

In economic news, Switzerland’s total sight deposits fell to a level of CHF578.5 billion in the week ended 06 October, compared to a level of CHF579.0 billion reported in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9782, with the USD trading 0.16% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9767, and a fall through could take it to the next support level of 0.9753. The pair is expected to find its first resistance at 0.9802, and a rise through could take it to the next resistance level of 0.9823.

Moving ahead, investors will closely monitor Switzerland’s unemployment rate for September, due to release in a while.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading On A Stronger Footing In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.19% against the CAD and closed at 1.2555.

In the Asian session, at GMT0300, the pair is trading at 1.2528, with the USD trading 0.22% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2510, and a fall through could take it to the next support level of 1.2493. The pair is expected to find its first resistance at 1.2552, and a rise through could take it to the next resistance level of 1.2577.

Ahead in the day, the release of Canada's housing starts for September and building permits for August, will garner significant market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

U.K. PM May Assured Businesses Of Two-Year Transition Period, Oil Gains On Possible Production Cuts

Dollar Steadies After Edging Back from 10-Week Peak. The dollar steadied on Tuesday after edging away from a 10-week high overnight, taking support from underlying expectations that improved prospects for the U.S. economy would prompt the Federal Reserve to raise interest rates later this year. The dollar index was a shade higher at 93.720 after dipping about 0.15 percent overnight.

Kiwi Falls Against Other Majors after German Data. Signs of risk aversion were seen in the New York session as equities dipped and bitcoin surged, leaving the higher-yielding Kiwi to suffer the brunt of the losses. Political concerns ebbed in Spain and the UK and figures showed stronger-than-expected German production pushed the New Zealand dollar to a low of US$0.7055, to 1.6640 against the euro and to 1.8600 against the pound.

Sterling Maintains Lead as Worries of UK Political Turmoil Subside. U.K. Prime Minister May had a brief meeting with business leaders and assured them that they can count on a two-year transition period, and that the U.K. will retain access to the single market on current terms. Sterling had a stellar performance in the earlier session and was able to squeeze out a few more gains before pausing from its climb as profits were locked in. Pound rallied to a high of 1.3188 before retreating to 1.3129.

Gold Rises on Geopolitical Risks. Investors moved towards safer investments as the US dollar saw a mixed performance after Russian media reported that North Korea is planning in the upcoming period to test long-range missile attacks that can reach the west cost of the US. Gold prices rose for three consecutive days and last closed at $1,284.9 per ounce.

Oil Prices Climb After OPEC Signals Possible Deal Extension. Oil prices rose slightly on comments by OPEC’s secretary general that indicated further possible extension of a production agreement beyond March 2018 and possible cuts in crude production. Crude settled at $49.58, up 29 cents on the day, while Brent rose 17 cents to settle at $55.79 per barrel. Oil production platforms in the Gulf of Mexico also started returning to service after Hurricane Nate forced the shutdown of more than 90 percent of crude output in the area. The prospective restarts kept price gains in check.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1766

The intraday bias here is positive, for a break through 1.1785 hurdle, for a tight test of 1.1830 major resistance. Crucial on the downside is 1.1720.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1785 | 1.1830 | 1.1720 | 1.1660 |

| 1.1830 | 1.2070 | 1.1660 | 1.1480 |

USD/JPY

Current level - 112.66

The bias remains bearish below 112.90, for a violation of 112.30, towards 111.50 major support.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.90 | 113.80 | 112.30 | 111.50 |

| 113.80 | 114.50 | 111.50 | 107.30 |

GBP/USD

Current level - 1.3155

My outlook remains positive above 1.3100 area, for a rise towards 1.3220 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3150 | 1.3340 | 1.3000 | 1.2910 |

| 1.3220 | 1.3650 | 1.2910 | 1.2760 |

Market Morning Briefing: Aussie Could Test 0.7700

STOCKS

Dow (22761.07, -0.06%) could trade below immediate resistance near 22800-22850 region and may have been exhausted after the recent rally in the last few weeks. A pause could be expected now where the index may trade sideways in the 22500-22800 region. A test of 22500 is on the cards for the coming sessions. Only on a sustained break above 22850, we may look at higher levels of 23000.

Dax (12976.40, +0.16%) made a fresh high of 12996 reaching almost our initial target of 13000. We will have to see if the index pauses here or heads higher to break above 13000. Some sessions of sideways consolidation would be preferred just now before an attempt to move further up. Note important resistance zone of 13000-13050.

Nikkei (20770.99, +0.39%) has broken above medium term resistance at 20750 and while the index trades above this level, there could be chances of testing crucial resistance near 20900-21000 levels on the upside in the near to medium term. Near term looks bullish contrary to our expectation of a pause below 20750.

Shanghai (3359.87, -0.43%) fell sharply in the last 2-sessions from 3410. The current fall may extend towards 3330-3325 before again bouncing back towards 3375 and higher.

Nifty (9988.75, +0.09%) was almost stable yesterday. A sustained rise above 10000 is necessary to take the index towards 10050-10100 in the next few sessions; else the index could continue to trade in the 10000-9900 region this week.

COMMODITIES

Gold (1286.62) has bounced well from 1260 levels last week and while that holds, we could see a rise towards 1293-1295 levels over today and tomorrow. Near term looks bullish.

Silver (17.028) has also broken above 16.75 and if the price manages to remain above 17 just now, we could see an extension of the current up move towards 17.50 where the price could take a pause or trade sideways for some time.

Brent (55.83) tested 55 on the downside yesterday and has bounced back from there. While above 55, a rise to 56.30-56.50 is possible. Trade within 56.65-55.00 could be expected in the coming sessions.

WTI (49.65) has interim support at 49 and while that holds, the price could move up towards 50.00-50.50 in the 2-sessions.

Copper (3.0435) has been coming off from 3.05, in line with our expectation but may bounce back from 3.00 to move up to 3.10 in the near term. The corrective dip is short lived and we could soon see a bounce by the end of the week.

FOREX

Dollar Index (93.548) has faced decent rejection from 94 and while that holds, the index could come off towards 93.26-93.00 levels in the near term. Euro (1.1771) on the other hand has moved above 1.1750. the low of 1.1668 tested on Friday could possibly be the near term low for the coming sessions and if prices remain above 1.1700, the Euro could head higher towards 1.1850 given that the resistance at 94 holds on the Dollar Index.

Dollar Yen (112.677) has been trading in the 113.30-112.30 region for the last 8-9 sessions unable to decide which direction to take. The currency pair is likely to continue to trade within the mentioned region for a few more session trying to move up towards 113.00 or higher. A break on either side is needed to get some clarity on further movement. Looking at Nikkei, it could be headed towards crucial resistance and the upside could be limited for the near term.

Pound (1.3158) has bounced from 1.30 and while that holds, a rise to 1.3275 is a possibility. Near term looks bullish.

Aussie (0.7786) could test 0.7700 on the downside before starting to move up again. Trade within 0.78-0.77 looks likely in the near term.

Dollar Rupee could spend some time in the 65.20-65.50 region before trying to move down to 65.00. Some time and price correction is preferred now especially after the sharp rally in the last 2-3 weeks from levels near 64.00 to almost levels near 65.80.

INTEREST RATES

The US yields have paused and could come down a bit before resuming a rise again by next week. A slight dip could be expected in the coming sessions. Note important resistances on the 30YR (2.91%) and 10Yr (2.36%) near 3.00% and 2.50% respectively.

The German-US 2YR (-2.21%) and the German-US 10YR (-1.91%) are trading just above medium term support levels and if that holds the yield spreads could bounce back sharply indicating a rise in Euro for the coming sessions.

Composition Of Market Risks Remains Unchanged

Composition of market risks remains unchanged

With US market on holiday, price action went as expected.But the one exception is TRY which continues to labour on the escalation of tension between US and Turkey and has precipitated a sell-off across most EM carry trade.Speculators are in no mood for unpleasant news more so with the Catalonian consternations heading for more moments of middlement.

Outside of the Turkey tantrum, the composition of forex market risks remains unchanged as the dollar, for the most part, anchors at current levels.

Trader's remain on geopolitical watch as North Korea celebrates the founding of the North Korean communist party on today.

Australian Dollar

With holidays in Japan and the US, it's been a slow start to the week for the Australian dollar which remains mired in tight ranges. However, dealers continue to view the weak domestic retail sales as a huge negative. Given the record debt levels, how much more spending power can the average consumer add to the economy?. And with the markets still likely underpriced the inflationary fall out from US tax reform, the Aussie will likely remain a go-to short over the near term.

Factor in the slide and Iron ore prices as China state mandates reducing steel production; iron ore demand could contiue to wilt.

The Australian economy looks little more than an asset bubble sitting on top of an iron ore mine. Both of which are the critical negatives in this weak Aussie dollar view.

Chinese Yuan

China returned from the Golden week with a bang as mainland equities soared to multi-year highs driven by last week RRR cuts. ON the FX market there was an aggressive culling of long USD. The liquidation appears guided to provide currency stability heading into the NPC on October 19.

Japanese Yen

Dollar-yen lacks in any momentum wedged between tracking US fixed income and a possible geopolitical flare up. However, the USDJPY continues to exhibit a higher acuteness to softening US rates so top side momentum should cap at 113.20 until this week's critical US CPI reading.

The Euro

Despite the heightened political risk, robust EU economic data continues to attract EURUSD buyers ahead of the critical 1.1700.

ECB's Sabine Lautenschlaeger was on the wires overnight; her hawkish comments also appear supportive for the EUR But with the Euro unchanged this week, the political overhang has taken the air out of the EUR ballon, and this ongoing political uncertainty will most certainly cap any near-term rallies.

The British Pound

The pound was undoubtedly the most energetic performer overnight After an error on Friday, the Office of National Statistics has confirmed that the UK unit labour costs have been revised up from 1.6% to 2.4% YoY. Predictably the inflation revision led to further pricing-in of a November BoE rate hike. But the sterling trade remains fraught with chaos with lots of head scratching on both the political and monetary policy fronts

New Zealand Dollar

NZ$ stays on the back foot after the weekend shift in election results. But the markets continue to bid on dip mode expecting the election tumult and the broader uncertainties to dissipate which could provide a lift to the Kiwi near-term expectations

Asia EMfx

The volatility in both US rates and commodities has muddied the landscape as the market continues to drift in no man's land. Geopolitical risks remain elevated which is not helping matters, but selective opportunities should stay in fashion. While the exclusive carry trades remains a tough grind the economic fundamentals continue to look favourable on the THB, MYR despite the overnight purge in EM positions overnight

Positioning on the MYR remains very light and on the first sign from the sell-off in global fixed income abates ,I expect regional inflows to pick up again.

Turkish Lira

Where do we go from here.? The Carry trade should remain alive and well however over the near term there will likely remain a lack of confidence in the TRY institutional markets after fairweather liquidity providers baulked at providing streamable quotes and the one or two that did support electronic venues felt 2-4 % spread was appropriate for market conditions. If there's any doubt what adds more unwarranted fuel to market unwinds, look no further than the risk-averse mindset that dominates today's Top Tier bank trading rooms. what investor appreciates his stop-loss triggered on a disproportionately wide 4% spread

Gold Rally Continues On Holiday Monday

After an uneventful week, gold has started the week with gains. In Monday’s North American trade, the spot price for an ounce of gold is $1280.61, up 0.37% on the day. There are no US releases today, and banks are closed for Columbus Day.

Gold prices moved higher on Friday, as Nonfarm Employment Change shocked the markets by wiping out 33 thousand jobs in September, much weaker than the estimate of a gain of 85 thousand. The dismal release was a result of the severe impact of hurricanes Harvey and Irma, which hit the US in late August and early September. The two storms caused $150-200 billion in damage and also took a toll on the employment market, although the labor market is expected to rebound as the recovery effort intensifies. There was better news from wage growth, which accelerated to 0.5%, above the estimate of 0.3%. This reading is pointing to stronger inflationary pressure, although we’ll have to wait for additional inflation indicators, such as CPI, to gauge inflation is moving higher. As well, the unemployment rate fell from to 4.2% in September, down from 4.4% a month earlier.

Early in the year, the Federal Reserve broadly hinted that it would raise rates three or four times in 2017, and a third hike in December now appears very likely. Fed futures are currently priced in at 91%, which is remarkable, considering that only a month ago, the odds of a December increase were just 31 percent. A strong US economy has helped raise the odds, but the primary reason for the huge shift in market sentiment can be attributed to the Fed policymakers that have come out in support of a rate hike, notably Fed Chair Janet Yellen. The lack of inflation remains the most significant impediment to raising rates, but Yellen and other FOMC members have insisted that strong economic conditions will lead to higher inflation levels.