Sample Category Title

Elliott Wave View: NZDUSD Short-Term

NZDUSD Short term Elliott Wave view suggests the decline from 9/20 peak remains in progress a zigzag Elliott Wave structure. Down from 9/20 high (0.7434), pair ended Minor wave A at 0.7165. Subdivision of Minor wave A unfolded as 5 waves impulse where Minute wave ((i)) of A ended at 0.7276 and bounce to 0.7362 ended Minute wave ((ii)) of A. Afterwards, decline to 0.7166 ended Minute wave ((iii)) of A and Minute wave ((iv)) of A ended at 0.7239. Minute wave ((v)) of A completed at 0.7165. Pair then bounced in Minor wave B in 3 waves and ended at 0.7243. Minor wave C is currently in progress and unfolding also as 5 waves impulse. Minute wave ((i)) ended at 0.7145, Minor wave ((ii)) ended at 0.7206, and Minute wave ((iii)) at 0.7049. While Minute wave ((iv)) bounce stays below 9/29 peak (0.7243), expect pair to extend lower towards 0.6919 – 0.6983 before ending cycle from 9/20 peak.

NZDUSD 1 Hour Elliott Wave Chart

Daily Wave Analysis: GBP/USD Builds Wave 4 Correction In Downtrend Channel

Currency pair GBP/USD

The GBP/USD is building a bullish retracement in the downtrend channel (red line) which could be part of a larger wave C or 3 (green).

The GBP/USD is probably building a deeper bullish retracement via a wave 4 (orange). This wave 4 (orange) becomes less likely if price breaks above the downtrend channel and 50% Fib. A bearish break below the bullish channel (blue) could indicate the continuation of the downtrend.

Currency pair EUR/USD

The EUR/USD broke above the falling wedge chart pattern (dotted orange), which indicates a bullish bounce at the 23.6% Fibonacci level of wave 4 (purple). The wave 4 does not have to be completed. This depends on whether price makes a bullish ABC or 12345 pattern when challenging the next resistance trend lines.

The EUR/USD wave structure has multiple options at this moment but a wave 3 (pink) is more likely if price manages to break above the resistance trend line (red).

Currency pair USD/JPY

The USD/JPY is in a sideways range, which is indicated by the support (blue) and resistance (red) trend lines. A bearish breakout could indicate a retracement towards the Fibonacci levels of wave 2 or B (purple).

The USD/JPY could be building a potential ABC (pink) correction.

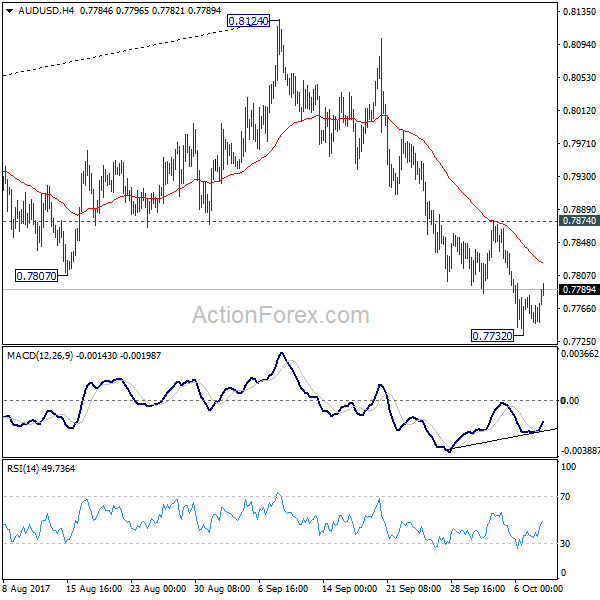

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7739; (P) 0.7760; (R1) 0.7774; More...

A temporary low is in place at 0.7732 and intraday bias is turned neutral first. Another fall is expected as long as 0.7874 resistance holds. As noted before, rise from 0.7382 is possibly completed at 0.8124 already. Below 0.7732 will target medium term fibonacci level at 0.7628 first. Decisive break there will target 0.7328 key cluster support. On the upside, break of 0.7874 will argue that the decline is completed and turn bias back to the upside.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. Current development suggests that it might be completed with three waves up to 0.8124 already. Break of 38.2% retracement of 0.6826 to 0.8124 at 0.7628 will firm this bearish case. And, decisive break of 0.7328 key cluster support (61.8% retracement at 0.7322) will confirm and bring retest of 0.6826 low. In case rise from 0.6826 resumes and extends, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside.

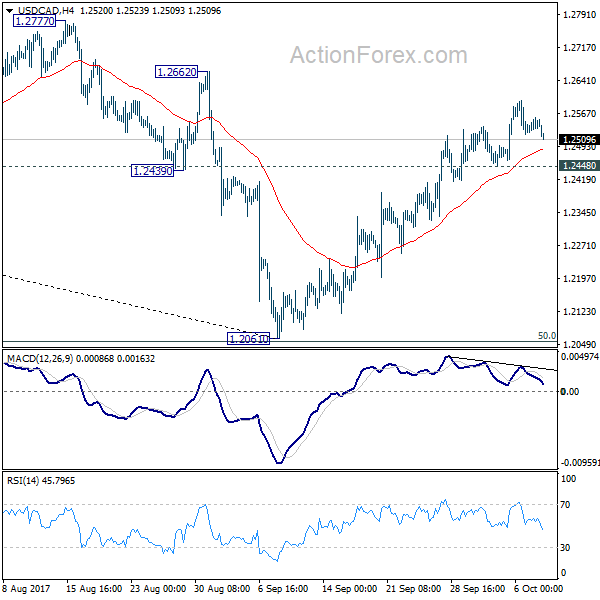

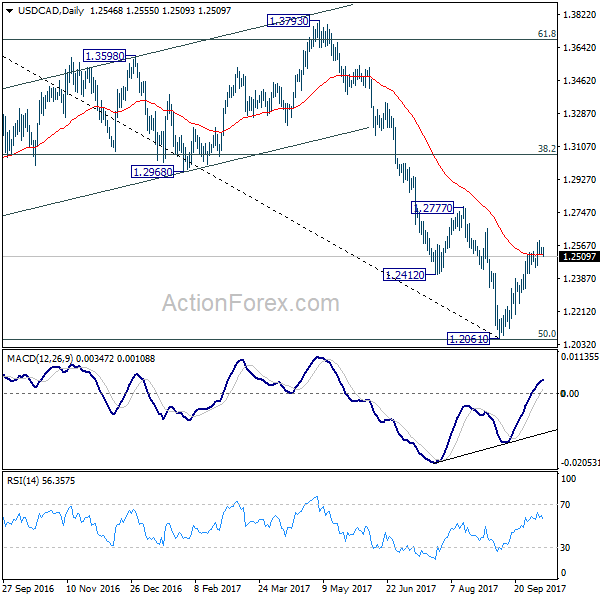

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2531; (P) 1.2544; (R1) 1.2564; More....

USD/CAD continues to lose upside momentum as seen in 4 hour MACD. But with 1.2448 minor support intact, further rise is in favor. Rally from 1.2061 would target 1.2777 resistance first. Decisive break there will target key medium term fibonacci level at target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. On the downside, break of 1.2448 will indicate short term topping and turn bias back to the downside for retesting 1.2061 low.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

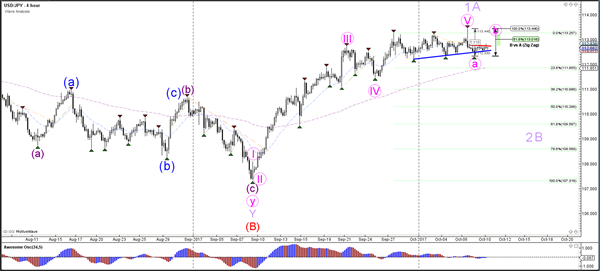

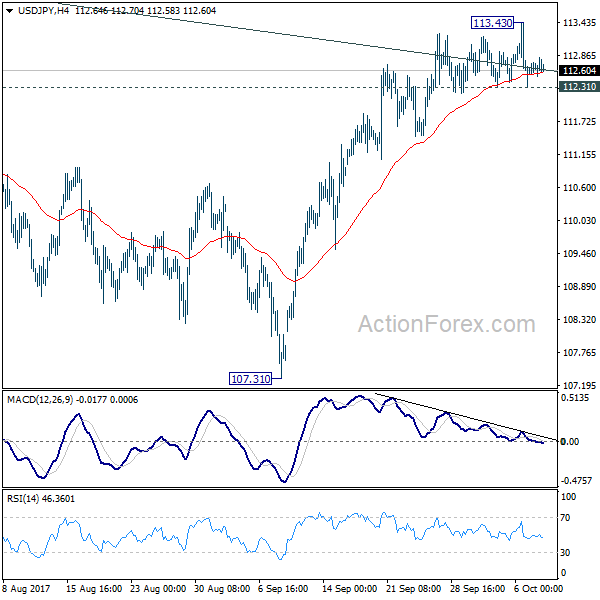

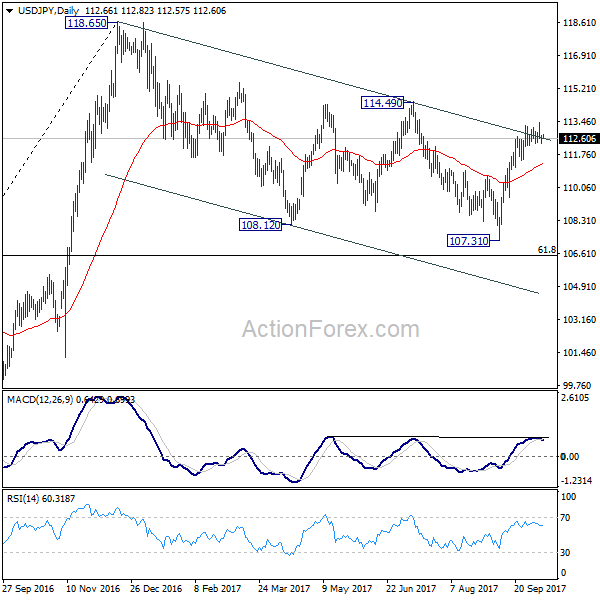

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.34; (P) 112.88; (R1) 113.17; More....

Intraday bias in USD/JPY remains neutral at this point. On the upside, break of 113.43 and sustained trading above the channel resistance will argue that correction from 118.65 is already completed with three waves down to 107.31. Break of 114.49 will confirm this bullish case and target a test on 118.65 next. On the downside, considering bearish divergence condition in 4 hour MACD, break of 112.31 will suggest rejection from the channel resistance and turn bias back to the downside.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

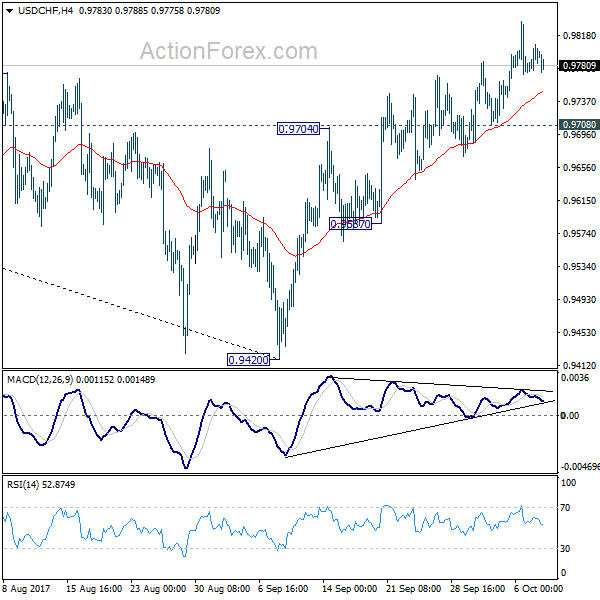

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9775; (P) 0.9791; (R1) 0.9812; More....

USD/CHF continues to lose upside momentum as seen in 4 hour MACD. But with 0.9708 minor support intact, further rise is expected. We're favoring the whole down trend form 1.0342 has completed after defending 0.9443 key support again. Further rise would be seen to 61.8% retracement of 1.0342 to 0.9420 at 0.9990. However, break of 0.9708 will mix up this bullish outlook and turn bias back to the downside for 0.9587 support instead.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

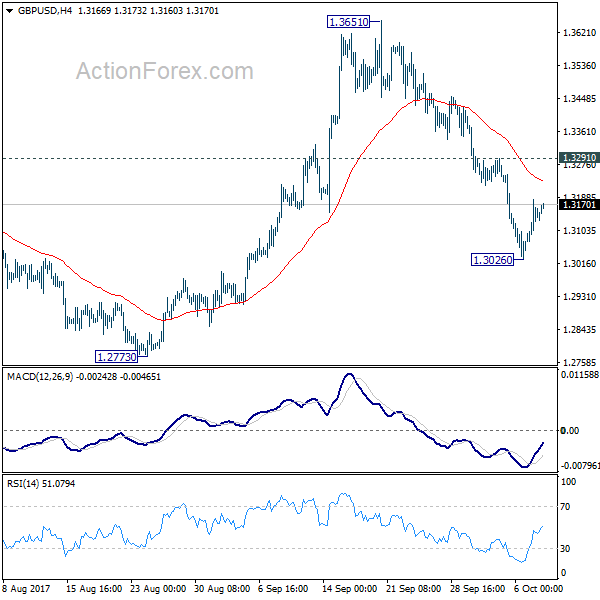

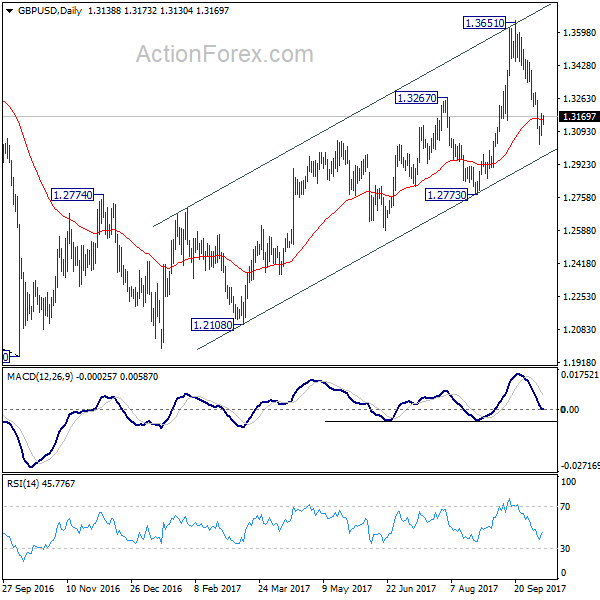

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3083; (P) 1.3134; (R1) 1.3192; More....

A temporary low is in place at 1.3026 in GBP/USD and intraday bias is turned neutral first. At this point, deeper fall is mildly in favor as long as 1.3291 minor resistance holds. Below 1.3026 will target 1.2773 key support level. Decisive break there will affirm the bearish case of medium term reversal. Nonetheless, break of 1.3291 will suggest that the pull back from 1.3651 is completed and turn bias back to the upside.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll turn neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

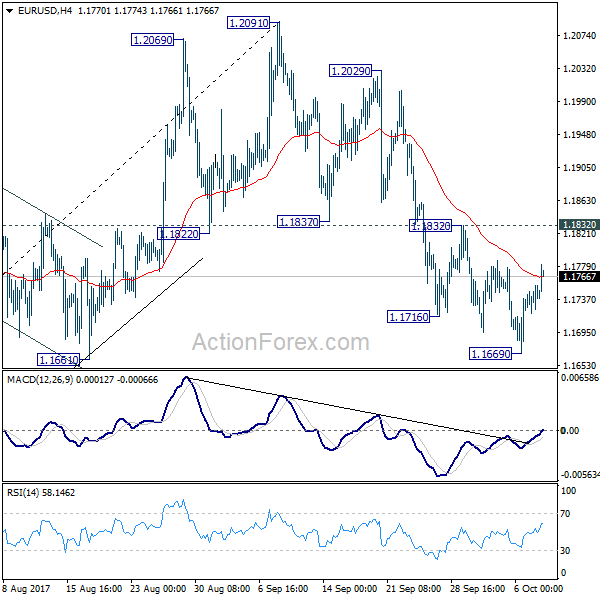

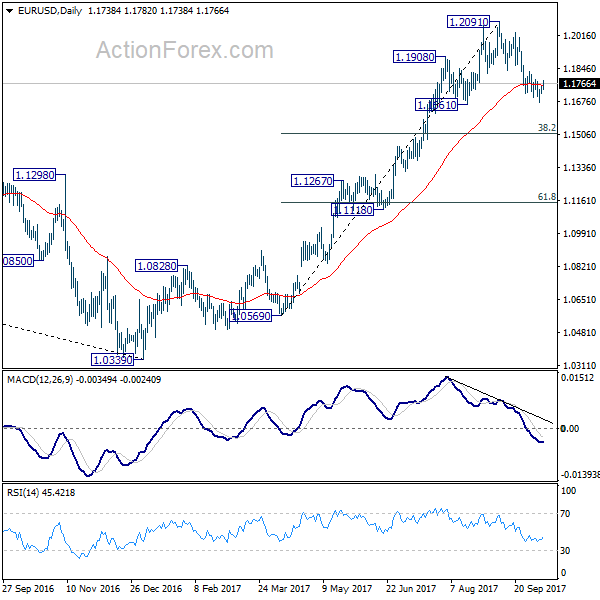

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1721; (P) 1.1738 (R1) 1.1758; More...

EUR/USD's recovery from 1.1669 continues today. But for the moment, it's staying below 1.1832 resistance and intraday bias stays neutral. Another fall is still in favor as long as 1.1832 resistance holds. . Break of 1.1669 temporary low will extend the fall from 1.2091 to 38.2% retracement of 1.0569 to 1.2091 at 1.1510. As such decline is viewed as a correction to rise from 1.5069, we'd expect strong support from 1.1510 to bring rebound. Meanwhile, break of 1.1832 resistance will argue that the correction is already completed and turn bias back to the upside for retesting 1.2091 high.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

Euro Broadly High as ECB is Preparing to Scale Back Asset Purchases

Euro trades broadly higher as lifted by comments from ECB officials that affirm the expectation of some sort of tapering in asset purchases next year. Catalonia remains a risk to the common currency but the case for independence seem to be fading. The risk is taking a back seat for the moment. Meanwhile, Sterling also recovers together with Euro as Prime Minister Theresa May seems to be safe from being ousted for now. Dollar, on the other hand, is trading generally lower together with the Japanese Yen.

ECB Lautenschlaeger: We should begin reducing bond purchases

ECB Executive Board Member Sabine Lautenschlaeger, a known hawk, urged that "we should begin reducing our bond purchases next year". And, "this should be done gradually, until we are no longer purchasing additional bonds". She emphasized that "it is important that we really move towards the exit - step by step, but steadily and in a clear direction". Meanwhile, she also noted that "it is clear which sequence the exit will follow". That is, "bond purchases will come to an end, while interest rates will remain low, well past the horizon of net asset purchases".

ECB Knot: The time has come to phase out stimulus

ECB Governing Council member Klaas Knot warned that the financial markets could be underpricing global risks. He noted that "markets seem resilient at the moment, but the low level of volatility and the overvaluation in a range of investments make me feel uneasy." And, to prevent further build-up of risks, the time has come to phase out monetary stimulus. And, "economic growth has been above potential for months and the threat of deflation is gone." He also echoed Lautenschlaeger's view that "interest rates will stay very low for a very long time, even if we decide to phase out our bond buying program at our next meeting. Nobody at the ECB is talking about raising interest rates yet."

51 banks needs intense discussions on interest rate risks

In a report released yesterday, ECB noted that "interest rate risk is well managed by most European banks." But 51 of them may need "intense discussions" to make sure they have enough capital if things go wrong. A hypothetical interest rate shock with 2% hike is put in a stress test. That would like to a rise in net interest income of 4.1% in 2017 and 10.5% by 2019 for the banks tested. Net value of assets and liabilities of banks will change with interest rate movements. ECB found that bank's equity would decrease on aggregate by 2.7%.

Catalan leader Puigdemont to address regional parliament

Catalan President Carles Puigdemont will address the regional Parliament today. It's unknown whether Puigdemont will declare independence considering that there was a mass pro-unity rally in Barcelona on Sunday. And Puigdemont clearly didn't get much support from European leaders. German Chancellor Angela Merkel talked to Spanish Prime Minister Mariano Rajoy over the weekend, and "affirmed her support for the unity of Spain", according to a German government spokesman. French European Affairs Minister Nathalie Loiseau said "if there was a declaration of independence, it would not be recognized." And Loiseau warned that "the first consequence would be its exit from the European Union."

UK May laid out steps to minimise disruption on Brexit day

In UK, Prime Minister Theresa May told the parliament that "real and tangible progress " had been made in Brexit negotiations with EU. However, she emphasized the need to prepare for "every eventuality". And May set out detailed "steps to minimise disruption" on Brexit day in 2019. May has been calling for a so called "implementation period" as transition. And she said that a transition deal "may mean we will start off with European court of justice still governing rules we're part of for that period". That drew heavy criticism from Tories MPs. Conservative Jacob Rees-Mogg argued that "if the ECJ still has jurisdiction, we will not have left the EU. It is perhaps the most important red line in ensuring the leave vote is honoured."

BoJ governor Kuroda repeated economy expanding moderately

BoJ Governor Haruhiko Kuroda reiterated that "Japan's economy is expected to continue expanding moderately in the future." And, after three years of massive quantitative easing, inflation is still struggling to come up. Kuroda noted that the central bank will maintain the stimulus program and he's optimistic that inflation will gradually pick up towards the 2% target, thanks to closure of output gap and improvements in inflation expectations.

Japanese Prime Minister Shinzo Abe begins his election campaign by attacking the opposition for creating new parties. He said that "what creates our future is not a boom or slogan. It is policy that creates our future." Based on recent polls, Abe's Liberal Democratic Party-led coalition is predicted to repeat the past landslide victories in this snap election on October 22.

Released from Japan, current account surplus widened to JPY 2.27T in August. Eco Watchers sentiment rose to 51.3 in September.

Business sector in Australia is doing very well

Australia NAB business confidence rose to 7 in September, up from 5. Business conditions remained at 14, close to triple of the historical average. NAB Chief Economist Alan Oster noted that "business conditions at these levels tell us that the business sector in Australia is doing very well." However, he pointed out that "the sustained weakness in retail conditions should justifiably be raising doubts around expectations for any imminent, and sustained rebound in consumer spending, although tough competition and other margin pressures are likely behind the result as well." Also, "elevated underemployment, an elevated Australian dollar, household debt and peaks in LNG exports and housing construction are all potential hurdles that will ensure that the Reserve Bank of Australia proceeds with caution."

On the data front

UK productions will be the main focus in European session, and trade balance will also be released. Germany will also release trade balance while Swiss will release unemployment rate. Later in the day, Canadian housing data will be featured.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1721; (P) 1.1738 (R1) 1.1758; More...

EUR/USD's recovery from 1.1669 continues today. But for the moment, it's staying below 1.1832 resistance and intraday bias stays neutral. Another fall is still in favor as long as 1.1832 resistance holds. . Break of 1.1669 temporary low will extend the fall from 1.2091 to 38.2% retracement of 1.0569 to 1.2091 at 1.1510. As such decline is viewed as a correction to rise from 1.5069, we'd expect strong support from 1.1510 to bring rebound. Meanwhile, break of 1.1832 resistance will argue that the correction is already completed and turn bias back to the upside for retesting 1.2091 high.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Sep | 1.90% | 1.30% | ||

| 23:50 | JPY | Current Account (JPY) Aug | 2.27T | 1.98T | 2.03T | |

| 0:30 | AUD | NAB Business Confidence Sep | 7 | 5 | ||

| 5:00 | JPY | Eco Watchers Survey Current Sep | 51.3 | 49.9 | 49.7 | |

| 5:45 | CHF | Unemployment Rate Sep | 3.20% | 3.20% | ||

| 6:00 | EUR | German Trade Balance (EUR) Aug | 20.1B | 19.5B | ||

| 8:30 | GBP | Industrial Production M/M Aug | 0.20% | 0.20% | ||

| 8:30 | GBP | Industrial Production Y/Y Aug | 0.90% | 0.40% | ||

| 8:30 | GBP | Manufacturing Production M/M Aug | 0.20% | 0.50% | ||

| 8:30 | GBP | Manufacturing Production Y/Y Aug | 1.90% | 1.90% | ||

| 8:30 | GBP | Construction Output M/M Aug | 0.00% | -0.90% | ||

| 8:30 | GBP | Visible Trade Balance (GBP) Aug | -11.2B | -11.6B | ||

| 12:00 | GBP | NIESR GDP Estimate Sep | 0.40% | |||

| 12:15 | CAD | Housing Starts Sep | 223.2K | |||

| 12:30 | CAD | Building Permits M/M Aug | -3.50% |

Australia’s NAB Business Confidence Improved In September

For the 24 hours to 23:00 GMT, the AUD declined 0.26% against the USD and closed at 0.7754.

LME Copper prices declined 0.5% or $32.0/MT to $6607.0/MT. Aluminium prices rose 0.6% or $13.5/MT to $2135.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7779, with the AUD trading 0.32% higher against the USD from yesterday's close.

Earlier in the session, data indicated that Australia's NAB business confidence index advanced to a level of 7.0 in September, compared to a reading of 5.0 in the previous month. Moreover, the nation's NAB business conditions index remained unchanged at a level of 14.0 in September.

The pair is expected to find support at 0.7755, and a fall through could take it to the next support level of 0.7730. The pair is expected to find its first resistance at 0.7797, and a rise through could take it to the next resistance level of 0.7814.

Going ahead, traders will keep a close watch on Australia's Westpac consumer confidence index for October, due to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.