Sample Category Title

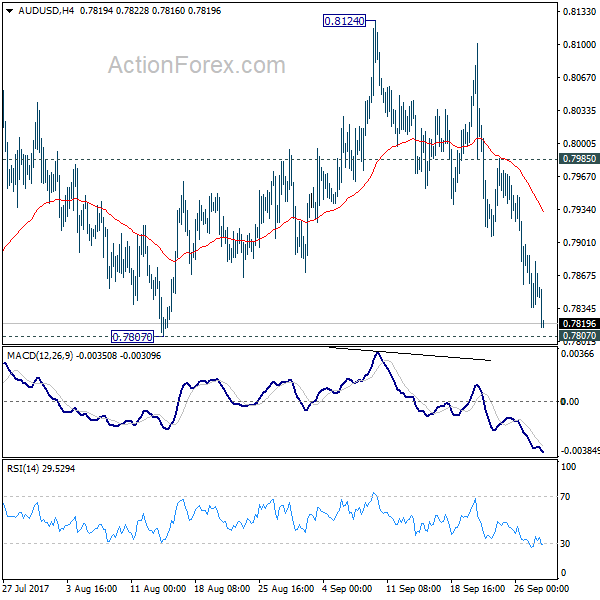

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7826; (P) 0.7857; (R1) 0.7879; More...

AUD/USD's fall from 0.8124 extended lower today and focus is now on 0.7807 key support level. Considering bearish divergence condition in daily MACD, firm break of 0.7807 will indicate near term reversal. Outlook will then be turned bearish for 55 week EMA (now at 0.7670) first. Meanwhile, rebound from 0.7807 will retain bullishness for another rise through 0.8124 high.

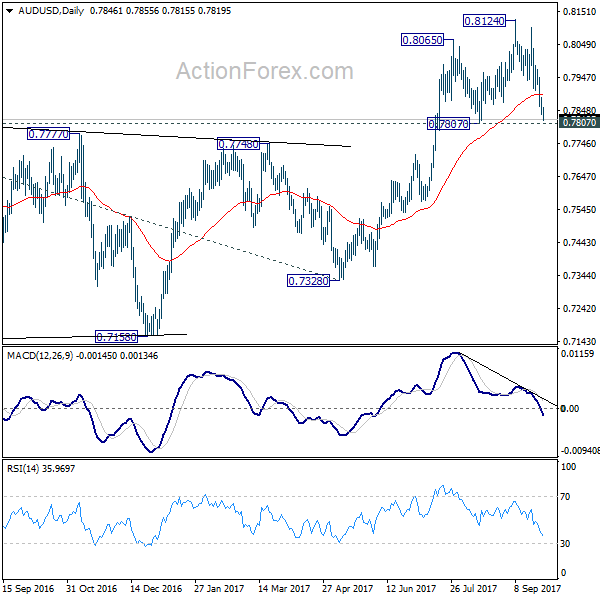

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8090) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7807 support is needed to to be the first sign of completion of the rebound. Otherwise, further rise is now in favor.

European Open Briefing: Asian Equities Were Mixed Early On Thursday

Global Markets:

- Asian stock markets: Nikkei rose 0.48 %, Shanghai Composite down 0.09 %, Hang Seng lost 0.39 %, ASX 200 rose 0.21 %

- Commodities: Gold at $1284.00 (-0.29 %), Silver at $16.77 (-0.32 %), WTI Oil at $51.98 (-0.31 %), Brent Oil at $57.34 (-0.40 %)

- Rates: US 10-year yield at 2.34, UK 10-year yield at 1.37, German 10-year yield at 0.46

News & Data:

- (NZD) Official Cash Rate 1.75 % vs 1.75 % expected

- (EUR) M3 Money Supply y/y 5.0 vs 4.6 % expected

- (USD) Core Durable Goods Orders m/m 0.2 % vs 0.2 % expected

- (USD) Durable Goods Orders m/m 1.7 % vs 1.0 % expected

- (USD) Pending Home Sales m/m -2.6 % vs -0.5 % expected

- (USD) Crude Oil Inventories -1.8 M vs 2.9 M expected

- Trump proposes U.S. tax overhaul, stirs concerns on deficit- RTRS

Markets Update:

Asian equities were mixed early on Thursday as investors began to assess the implications of the much-anticipated tax proposal. The dollar and U.S. bond yields rose after President Donald Trump proposed the biggest U.S. tax overhaul in three decades and as strong U.S. economic data added to the case for a rate hike by the Federal Reserve later this year.

USDJPY is currently seen trading around 113.07, the pair was seen ranging within a 20 pip range for most of the session earlier today with little to drive it. Japanese parliament was officially dissolved today to bring on the October 22 election. Overall the Yen continues to drop against the USD, down 0.2 percent on Thursday, continuing its 0.5 percent fall on Wednesday.

EURUSD continued to decline for the third straight day after hitting a six-week low of $1.1717 on Wednesday and is currently seen trading around 1.1733 as there were some signs of further USD strength. The dollar index, which tracks the dollar against a basket of currencies rose 0.2 percent and is currently valued at 93.57 touching the highest in a month.

AUDUSD is currently seen trading at 0.7818, as the Aussie further declined 0.4 percent against the US Dollar. Likewise, the NZDUSD is seen trading at 0.7192 as the Kiwi lost 0.2 percent against the US Dollar. The kiwi fluctuated as the Reserve Bank of New Zealand signaled it will keep rates on hold for some time on a weaker economic growth outlook and slowing inflation.

Upcoming Events:

- All Day – (EUR) German Prelim CPI m/m

- 06:35 GMT – (JPY) BOJ Gov Kuroda Speaks

- 07:00 GMT – (EUR) Spanish Flash CPI y/y

- 08:15 GMT – (GBP) BOE Gov Carney Speaks

- 09:00 GMT – (AUD) RBA Assist Gov Debelle Speaks

- 12:30 GMT – (USD) Final GDP q/q

- 12:30 GMT – (USD) Unemployment Claims

- 14:15 GMT – (USD) FOMC Member Fischer Speaks

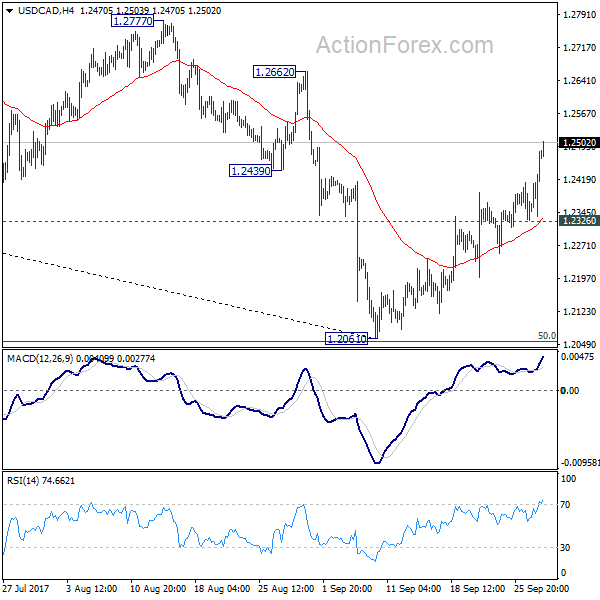

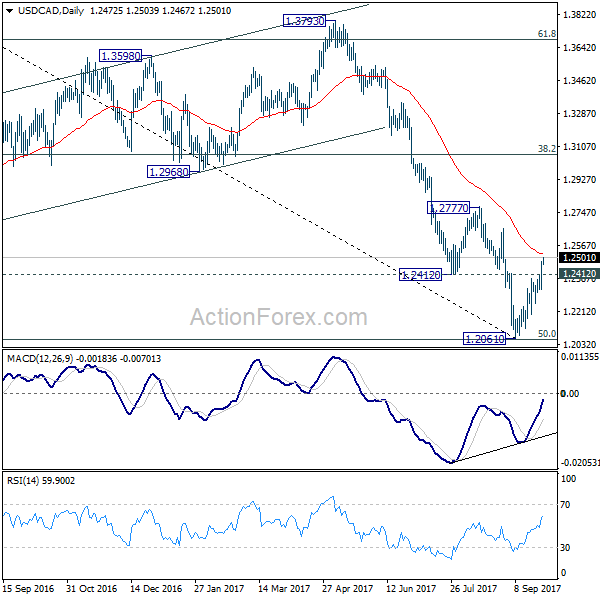

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2380; (P) 1.2431; (R1) 1.2528; More....

USD/CAD's rebound from 1.2061 extended to as high as 1.2503 so far. The strong break of 1.2412 support turned resistance and upside acceleration carries bullish implications. The pair should have now successfully defended key long term fibonacci level at 2.1048. Near term outlook is turned bullish for 1.2777 resistance first. Decisive break there will target 38.2% retracement of 1.4689 to 1.2061 at 1.3065 next. And, this will be the preferred case as long as 1.2326 support holds.

In the bigger picture, focus remains on 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. As long as this level holds, we'd still favor that case that fall from 1.4689 is a correction. Rebound from 1.2048 could extend the larger up trend from 0.9406. However, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Yields Surge and Dollar Firm as Markets Responded Positively to Trump’s Tax Plan

The financial markets responded quite positively to US President Donald Trump's tax plan in spite of some criticisms. Most notable movements are seen in treasury yields. 10 year yield closed up 0.080 at 2.309, resuming recent rise from 2.034 and is on course to 2.396 resistance. 30 year yield also resumed recent rally and ended up 0.093 at 2.863. Stocks also strengthened with S&P 500 hitting new intraday high at 2511.75 before closing at 2507.04, up 0.41%. DOW gained 0.25% to close at 22340.71. Fed fund futures are pricing in 83% chance of December hike, up from 73% a week ago. Dollar extended this week's advance, in particular, it's picking up momentum against commodity currencies.

In the framework proposed by Trump and Republicans released yesterday, tax rates on corporations would be set at 20%, down from the current 35%. Businesses would also be allowed to immediately write off their capital spending for five years at least. Pass through business tax rate would be capped at 25%. For individuals, the number of tax brackets are reduced from seven to three. The new tax brackets would be 12%, 25% and 35%, with top rate down from current 39.6%. The Congress would be given the flexibility to add a fourth rate for higher earners.

The question now is on how the Republicans are going to push the plan through Congress, and complete by year end as Trump is asking for. The plan was hailed by some Republicans which we're not going to repeat here. On the other hand, the Committee for a Responsible Federal Budget estimated that the plan would equate to a USD 2.2T tax cut with USD 5.8% lost to lower rates and USD 3.6T recouped by eliminating deductions. There is no estimate on the impact to growth, and thus tax revenue yet. And there is no details on how to fill up the gaps left by the lost in revenue. At the same time, the criticism that the plan only benefits the wealthy, with modest help to the middle class, remained.

The jump in TNX (10 year yield) further affirm the case that correction from 2.621 is completed at 2.034 already. Near term outlook will remain bullish as long as 2.215 support holds. Further rise is expected to 2.396 resistance next. Break will pave the way to retest 2.621 high. Such a development could likely help push dollar index (current at 93.36) through 94.14 near term resistance to confirm trend reversal. And that will be accompanied by deeper fall in EUR/USD through 1.1661 support and USD/JPY through 114.49 resistance.

BoC Poloz talked cautious to tame rate speculations

Canadian Dollar tumbled overnight after comments from BoC Governor Stephen Poloz. Poloz sounded like he wanted to tame down speculations for further rate hike by the central bank. He emphasized that there is no "predetermined path" for interest rates, decisions will be "data-dependent" and policy makers could "still be surprised in either direction". And he spelled out some risks ahead too as the reactions to the recent two rate hikes are uncertain, especially given high household debt. And there uncertainties from the "moving target" nature of full capacity, impacts of technology on inflation and sluggish wage growth. Poloz also mentioned geopolitical concerns and trade protectionism. But at least, for now, Poloz believed that "at a minimum, that additional stimulus is no longer needed", referring to the impact of oil price collapse back in 2014/15.

Kiwi stays weak after RBNZ stands pat

New Zealand Dollar remains the weakest one for the week after RBNZ rate decision. As widely anticipated, RBNZ left the OCR unchanged at 1.75% in September Policymakers downgraded the domestic growth outlook and suggested that the accommodative monetary policy would stay for a 'considerable period'. Thanks to the recent decline in New Zealand, driven by heightened political uncertainty, RBNZ tweaked its warning over currency strength. It noted that a lower exchange rate would "would help" raise tradables inflation. We expect RBNZ to keep the policy rate unchanged for the rest of the year, and likely through 2018. More in RBNZ Downgrades Growth Outlook While Keeping OCR At 1.75%

On the data front

German Gfk consumer sentiment and September CPI will be released in European session. Eurozone will also release confidence indicators. Later in the day, US will release Q2 GDP final, trade balance, jobless claims and wholesale inventories.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2380; (P) 1.2431; (R1) 1.2528; More....

USD/CAD's rebound from 1.2061 extended to as high as 1.2503 so far. The strong break of 1.2412 support turned resistance and upside acceleration carries bullish implications. The pair should have now successfully defended key long term fibonacci level at 2.1048. Near term outlook is turned bullish for 1.2777 resistance first. Decisive break there will target 38.2% retracement of 1.4689 to 1.2061 at 1.3065 next. And, this will be the preferred case as long as 1.2326 support holds.

In the bigger picture, focus remains on 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. As long as this level holds, we'd still favor that case that fall from 1.4689 is a correction. Rebound from 1.2048 could extend the larger up trend from 0.9406. However, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 6:00 | EUR | German GfK Consumer Confidence Oct | 11 | 10.9 | ||

| 9:00 | EUR | Eurozone Business Climate Indicator Sep | 1.12 | 1.09 | ||

| 9:00 | EUR | Eurozone Economic Confidence Sep | 112 | 111.9 | ||

| 9:00 | EUR | Eurozone Industrial Confidence Sep | 5.1 | 5.1 | ||

| 9:00 | EUR | Eurozone Services Confidence Sep | 15 | 14.9 | ||

| 9:00 | EUR | Eurozone Consumer Confidence Sep F | -1.2 | -1.2 | ||

| 12:00 | EUR | German CPI M/M Sep P | 0.10% | 0.10% | ||

| 12:00 | EUR | German CPI Y/Y Sep P | 1.80% | 1.80% | ||

| 12:30 | USD | GDP (Annualized) Q2 T | 3.10% | 3.00% | ||

| 12:30 | USD | GDP Price Index Q2 T | 1.00% | 1.00% | ||

| 12:30 | USD | Initial Jobless Claims (SEP 23) | 269K | 259K | ||

| 12:30 | USD | Advance Goods Trade Balance (USD) Aug | -65.0B | -65.1B | ||

| 12:30 | USD | Wholesale Inventories Aug P | 0.40% | 0.60% | ||

| 14:30 | USD | Natural Gas Storage | 97B |

Market Morning Briefing: Expect A Range Of 1.1700-70 On The Euro Today

STOCKS

Some corrective dip is expected in most of the indices except Dax, which has some more room on the upside before pausing.

Dow (22340.71,+0.25%) could remain stable near current levels or move down towards 22200-22100 in the near term. While the index remains below 22600, bearishness may remain intact with a maximum downside of 22000.

Dax (12657.41, +0.41%) could be headed towards 12800 eventually from where a sharp rejection is possible back towards 12600-12500 levels.

Nikkei (20323.81, +0.28%) looks weak on the weekly candles and could possibly come off towards 20100-20000 in the upcoming sessions. Near to medium term looks bearish. But at the same time if Dollar Yen continues to rise, the fall in Nikkei could be limited and the index could trade sideways for sometime.

Shanghai (3338.20, -0.21%) is trading quiet. No major movement expected just now but there is scope of falling towards 3320 in the near term before again bouncing back towards 3350 and higher.

Initial downside target for Nifty (9735.75, -1.38%) would be 9680/85 levels which could give a pause for some sessions, but in case the index breaks below 9680, it could head towards 9600-9500 in a few sessions. Bears look strong just now and could be dominant in the near term.

COMMODITIES

Gold (1282.95) is trading just above important support levels of 1280/90. On a break below 1280, the index could be pushed to 1275-1260 levels in a few sessions. Else if 1280 holds, the price can move back to 1300 and higher. Dollar Index (93.52) has started to rise and could test 94.00-94.50 in the next 2-3 sessions. If that happens, Gold could be headed towards 1260 soon.

Silver (16.76) could be following the footsteps of Gold. While Gold falls, Silver too can weaken towards 16.50 or even lower in the enar term.

Brent (57.65) and WTI (51.98) are trading at lower levels. WTI looks bearish in the longer term charts while Brent could test support just below current levels and indicates a rise in the coming sessions if that holds. Else both the crude prices can come down in the near term.

Copper (2.9255) is stable between 2.95-2.90 levels for the last few sessions and the price seems to be consolidating sideways. Some more movement in this region is possible in the coming days before a sharp move comes in. Range trade could be expected for now between the narrow 2.95-2.90 region.

FOREX

As expected, the Euro (1.1739) did indeed come down to our target region of 1.1750-10 (low being 1.1716) and the Dollar Index (93.51) trades higher coming into our target zone of 93.50-94.00.

Expect a range of 1.1700-70 on the Euro today, while the Dollar Index could rise a bit more towards 94.00.

Dollar-Yen (112.89) saw a high of 113.26 yesterday and see 113.15 again. Need to see if it closes above 112.95 or not, for there is an important trendline Resistance at that level. A Close above 112.94 could take the market up to 115.00 as well. Let us see.

The Euro-Yen (132.43) is consolidating between 132-133 for now, but has chances of a falling towards 131. If that happens, it could pull Dollar-Yen down with it.

The Pound (1.3385) has broken below the mentioned support at 1.3430-00 and may thus have chances of falling towards 1.3315-3265 next week. Immediate Support available near current levels for the day. Rallies may be sold into.

The Aussie (0.7821) too has lost further ground and may end up testing 0.7750, as suggested yesterday.

Dollar-Yuan (6.6499) has met our target of 6.65 and might take a bit of rest now. Dollar-Rupee (64.71) saw a high of 64.75 yesterday, the outer end of our 64.50-75 Resistance region. Allow for a spike to 64.80-85 today before the market exhausts itself and comes down.

INTEREST RATES

Sharp rise in US yields, with the US 5Yr (1.91%), 10Yr (2.31%) and 30Yr (2.87%) all breaking above near-term resistances. The 30Yr may target 3.00% while the 10Yr may move up towards 2.44% at least. The 5yr may have fresh Resistance near current levels.

The US yield Curve is steepening a bit now, with the 10-5 (0.40%) and 30-10 (0.56%) bouncing well from Supports over the last few days. Further steepening possible in the near term.

Due to the surge in US yields, German-US 10Yr Spread (-1.85%) has come down again from -1.75%, abetting the weakness in the Euro.

RBNZ Downgrades Growth Outlook While Keeping OCR At 1.75%

As widely anticipated, RBNZ left the OCR unchanged at 1.75% in September Policymakers downgraded the domestic growth outlook and suggested that the accommodative monetary policy would stay for a 'considerable period'. Thanks to the recent decline in New Zealand, driven by heightened political uncertainty, RBNZ tweaked its warning over currency strength. It noted that a lower exchange rate would "would help" raise tradables inflation. We expect RBNZ to keep the policy rate unchanged for the rest of the year, and likely through 2018.

Policymakers turned less optimistic over the economic developments. As mentioned in accompanying statement, 'construction was weaker than expected' and 'growth is projected to maintain its current pace going forward, supported by accommodative monetary policy, population growth, elevated terms of trade, and fiscal stimulus'. This is contrasted with October’s statement that 'growth is expected to improve going forward, supported by accommodative monetary policy, strong population growth, an elevated terms of trade, and the fiscal stimulus outlined in Budget 2017'. On inflation, RBNZ attributed the ongoing decline in headline inflation to the 'volatility in tradable inflation'. In August, it suggested that it was due to the dissipation of' higher fuel and food prices'. The view on the housing market stayed largely unchanged, despite the weaker housing price since the last forecast.

New Zealand dollar dropped modestly since the last meeting on August 10. NZD fell -0.74% against USD and -0.27% against AUD. Yet, the central bank appeared less concerned about the currency strength. As noted in the statement, the 'trade-weighted exchange rate has eased slightly' during the inter-meeting period. It, however, affirmed that 'a lower New Zealand dollar would help to increase tradables inflation and deliver more balanced growth'. This marks a more relaxed language when compared to the August one, when the central bank warned that 'the trade-weighted exchange rate has increased since the May Statement, partly in response to a weaker US dollar. A lower New Zealand dollar is needed to increase tradables inflation and help deliver more balanced growth'.

On the monetary policy outlook, RBNZ noted that it would 'remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly'. One of the key uncertainties is the new government. The general election held last week resulted in a hung parliament. Although the National Party got most seats in the parliament, it fails to secure over 61 seats form a majority government by itself. A minority government appears less likely than in the previous term as the number of small parties entering the parliament has reduced this time. It appears quite possible for a coalition government of Nationals and NZ First. It is a real risk that the reforms proposed by the populist NZ First would drag the economic growth outlook, prolonging the accommodative monetary policy. We expect RBNZ to keep the policy rate unchanged for the rest of the year, and likely through 2018.

(RBNZ) Official Cash Rate Unchanged at 1.75 percent

The Reserve Bank today left the Official Cash Rate (OCR) unchanged at 1.75 percent.

Global economic growth has continued to improve in recent quarters. However, inflation and wage outcomes remain subdued across the advanced economies and challenges remain with on-going surplus capacity. Bond yields are low, credit spreads have narrowed and equity prices are near record levels. Monetary policy is expected to remain stimulatory in the advanced economies, but less so going forward.

The trade-weighted exchange rate has eased slightly since the August Statement. A lower New Zealand dollar would help to increase tradables inflation and deliver more balanced growth.

GDP in the June quarter grew in line with expectations, following relative weakness in the previous two quarters. While exports recovered, construction was weaker than expected. Growth is projected to maintain its current pace going forward, supported by accommodative monetary policy, population growth, elevated terms of trade, and fiscal stimulus.

House price inflation continues to moderate due to loan-to-value ratio restrictions, affordability constraints, and a tightening in credit conditions. This moderation is expected to continue, although there remains a risk of resurgence in prices given population growth and resource constraints in the construction sector.

Annual CPI inflation eased in the June quarter, but remains within the target range. Headline inflation is likely to decline in coming quarters, reflecting volatility in tradables inflation. Non-tradables inflation remains moderate but is expected to increase gradually as capacity pressure increases, bringing headline inflation to the midpoint of the target range over the medium term. Longer-term inflation expectations remain well anchored at around two percent.

Monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly.

Note: Following the departure of Graeme Wheeler, the Reserve Bank's policy making Governing Committee now comprises: Acting Governor Grant Spencer, Deputy Governor Geoff Bascand, and Assistant Governor John McDermott.

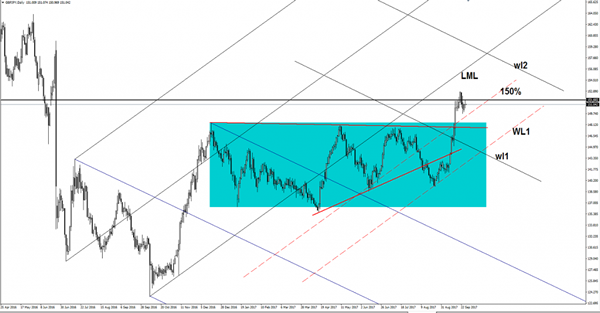

GBP/JPY Another Breakout Attempt?

GBP/JPY tries hard to stay higher and to take out the major horizontal resistance from the 151.66 level. Price failed to reach and retest the 150% Fibonacci line (ascending dotted line), signaling that the bulls are still in the game and could take control again. The perspective remains bullish as long as the price is located above this dynamic support. GBP/JPY could jump much higher if the Nikkei stock index will resume the upside movement.

NZD/USD Uninspired By RBNZ

The currency pair has managed to stay above the 50% retracement level after the last two breakdown attempts. It could move sideways in the upcoming days and could even increase a little if the dollar index will slip lower after the impressive rally. However, technically is expected to drop further after the breakdown below the sliding line (sl), but maybe after a retest of the broken line.

USD/CAD At New Highs

The currency pair rallied aggressively in the afternoon and reached fresh new highs after the BOC Poloz's speech. Price has managed to erase the Tuesday's losses and to resume the upside momentum. USD/CAD has jumped above some important resistance levels, but the breakout needs confirmation.

Technically, we may have a minor consolidation here, it could come to retest the broken levels if the USDX will slip lower in the upcoming days.

The USDX climbed as much as 93.61 level, where has found temporary resistance again. The index is bullish on the short term, but remains to see how long this rebound will be because personally, I'm expecting to see a minor decrease after the current rally.

You should know that we may have a high volatility in the afternoon after the United States data will be released.

Price has jumped much above the median line (ml) of the blue ascending pitchfork and now stand above the 1.2460 static resistance as well. Has changed little in the first 30 minutes of the Asian session, but most likely will have a significant move later in the afternoon when the fundamental factors will take the lead again.

Is still under some pressure despite the minor increase because is trapped within the descending pitchfork's body, only a valid breakout from it will confirm a larger rebound in the upcoming period. Personally, I believe that will take out the dynamic resistance from the upper median line (uml) if will touch it in the upcoming days.