Sample Category Title

Aussie Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.29% against the USD and closed at 0.8030.

LME Copper prices rose 0.4% or $28.0/MT to $6520.0/MT. Aluminium prices rose 2.7% or $56.5/MT to $2164.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.8003, with the AUD trading 0.34% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7959, and a fall through could take it to the next support level of 0.7914. The pair is expected to find its first resistance at 0.8075, and a rise through could take it to the next resistance level of 0.8146.

Moving ahead, a speech by the Reserve Bank of Australia’s (RBA) Governor, Philip Lowe, due in a while, will be eyed by investors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro Trading On A Weaker Footing, Ahead Of ECB President’s Speech

For the 24 hours to 23:00 GMT, the EUR declined 0.87% against the USD and closed at 1.1891.

On the macro front, Germany's producer price index climbed more-than-expected by 2.6% on an annual basis in August, compared to a rise of 2.3% in the previous month, while markets were anticipating the index to gain 2.5%.

The greenback gained ground against a basket of major currencies, after the US Federal Reserve (Fed), in a surprise move, indicated that it expects one more interest rate hike before the year-end.

The Fed, at its latest monetary policy meeting, left its key interest rate unchanged between 1.00% and 1.25% and announced a plan to start unwinding its $4.5 trillion balance sheet next month. In a statement accompanying the decision, the central bank offered a broadly optimistic view on the current economic conditions and signalled that it was still eyeing a possible third rate hike this year. However, the Fed Chairwoman, Janet Yellen, stated that a fall in inflation this year remained a mystery and added that the US central bank stands ready to change the interest rate outlook if needed.

Meanwhile, in its latest Summary of Economic Projections, the Fed forecasted the US economy to grow 2.4% this year, faster than a projection of 2.2% made in June. However, the central bank also lowered its inflation projection to be 1.9% by the end of 2018, slightly below its earlier forecast of 2.0%.

On the data front, existing home sales in the US unexpectedly fell 1.7% on monthly basis to a level of 5.35 million units in August, declining to its lowest level in a year, amid a shortage of properties and a sharp drop in Houston home purchases due to Hurricane Harvey. In the previous month, existing home sales recorded a level of 5.44 million, while markets had envisaged for an advance to a level of 5.45 million.

In the Asian session, at GMT0300, the pair is trading at 1.1883, with the EUR trading 0.07% lower against the USD from yesterday's close.

The pair is expected to find support at 1.1819, and a fall through could take it to the next support level of 1.1755. The pair is expected to find its first resistance at 1.1990, and a rise through could take it to the next resistance level of 1.2097.

Going ahead, market participants will closely monitor a speech by the ECB President, Mario Draghi as well as the release of the Euro-zone's flash consumer confidence index for September, both due later in the day. Also, the ECB's economic bulletin report, slated to release in a few hours, will be on investors' radar. Moreover, the US initial jobless claims and leading indicators data for August, scheduled to release later today, will attract a lot of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

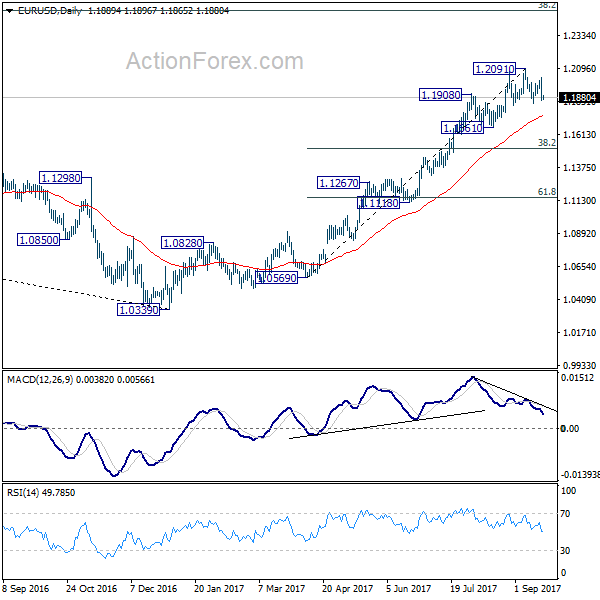

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1826; (P) 1.1929 (R1) 1.1998; More...

EUR/USD dropped sharply overnight but it's staying in range of 1.1822/2091 so far. Intraday bias remains neutral first. The development is raising chance of a head and should top reversal pattern (ls: 1.2069, h: 1.2091, rs: 1.2029). Break of 1.1822/1837 support zone should confirm near term reversal. In the case, intraday bias will be turned back to the downside through 1.1661 support. EUR/USD should then correct whole rise from 1.0569 and target 38.2% retracement of 1.0569 to 1.2091 at 1.1510. However, rebound from 1.1822/1837 and break of 1.2029 will resume the larger up trend to next key fibonacci level at 1.2516.

In the bigger picture, rise from medium term bottom at 1.0339 is still in progress for 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall fro 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside. But after all, break of 1.1661 is needed to indicate medium term topping. Otherwise, outlook will remain bullish in case of pull back.

Britain’s Retail Sales Accelerated To A 4-Month High Level In August

For the 24 hours to 23:00 GMT, the GBP slightly declined against the USD and closed at 1.3506.

On the economic front, data showed that UK's retail sales jumped 1.0% MoM and surged to a 4-month high in August, suggesting a solid consumer spending and brightening chances of the Bank of England hiking interest rates in the near future. In the prior month, retail sales had risen by a revised 0.6%, while markets had anticipated for a gain of 0.2%.

In the Asian session, at GMT0300, the pair is trading at 1.3495, with the GBP trading 0.08% lower from yesterday's close.

The pair is expected to find support at 1.3413, and a fall through could take it to the next support level of 1.3331. The pair is expected to find its first resistance at 1.3617, and a rise through could take it to the next resistance level of 1.3739.

Moving ahead, UK's BBA mortgage approvals and public sector net borrowing data, both for August, slated to release in a few hours, will keep investors on their toes.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

BoJ Stood Pat On Monetary Policy

For the 24 hours to 23:00 GMT, the USD rose 0.75% against the JPY and closed at 112.36, after the US Fed hinted that it would consider a further tightening of monetary policy this year.

In the Asian session, at GMT0300, the pair is trading at 112.47, with the USD trading 0.1% higher against the JPY from yesterday's close.

Earlier today, the Bank of Japan (BoJ), as widely expected, left its key interest rate steady at -0.1% and pledged to continue its asset-buying programme. Further, the central bank maintained its optimistic view of the economy, signalling its confidence that a solid recovery will eventually push inflation towards its 2.0% target without additional stimulus.

On the macro front, Japan's all industry activity index dropped 0.1% on a monthly basis in July, meeting market expectations. In the prior month, the index had recorded a revised rise of 0.2%.

The pair is expected to find support at 111.51, and a fall through could take it to the next support level of 110.55. The pair is expected to find its first resistance at 113.04, and a rise through could take it to the next resistance level of 113.61.

Looking ahead, investors anxiously await for comments from the BoJ Governor, Haruhiko Kuroda, to get cues on the central bank's monetary policy outlook.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Lower, Ahead Of Swiss Trade Balance Data

For the 24 hours to 23:00 GMT, the USD rose 0.81% against the CHF and closed at 0.9700.

In the Asian session, at GMT0300, the pair is trading at 0.9708, with the USD trading 0.08% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9626, and a fall through could take it to the next support level of 0.9544. The pair is expected to find its first resistance at 0.9754, and a rise through could take it to the next resistance level of 0.9800.

Ahead in the day, market participants will focus on Switzerland’s SECO economic forecast report and trade balance data for August.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Loonie Extends Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.32% against the CAD and closed at 1.2330.

In the Asian session, at GMT0300, the pair is trading at 1.2337, with the USD trading 0.06% higher against the CAD from yesterday’s close.

The pair is expected to find support at 1.2228, and a fall through could take it to the next support level of 1.2119. The pair is expected to find its first resistance at 1.2418, and a rise through could take it to the next resistance level of 1.2499.

In absence of major macroeconomic releases in Canada today, investors will look forward to global macroeconomic events for further direction.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

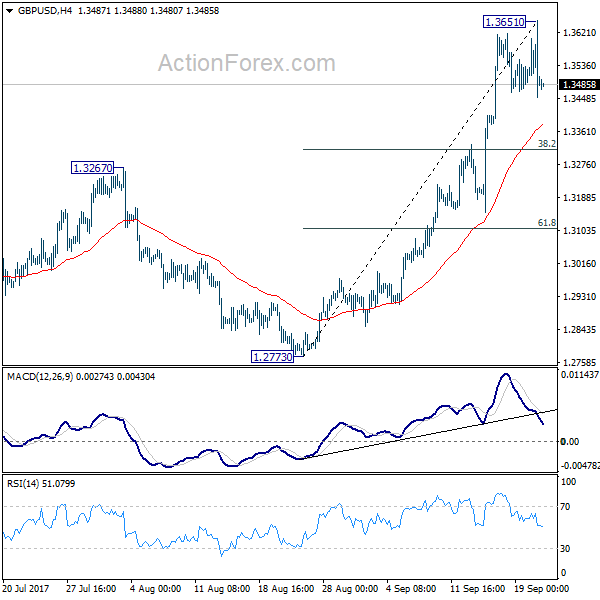

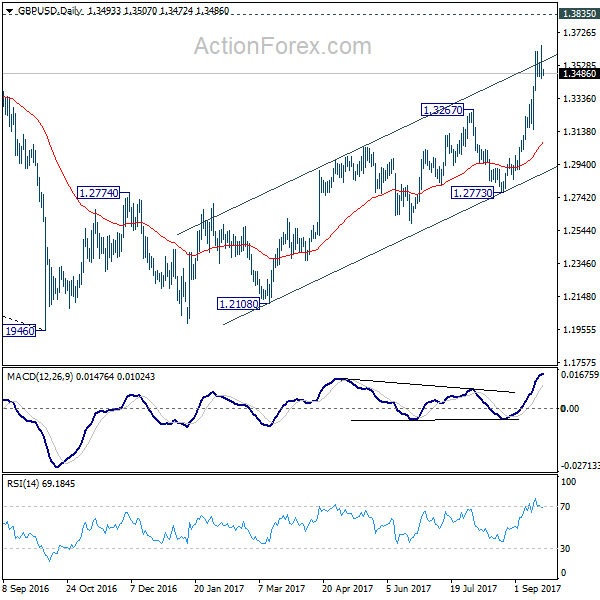

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3412; (P) 1.3533; (R1) 1.3616; More....

GBP/USD edged higher to 1.3651 but quickly retreated back into established range. Intraday bias stays neutral for more consolidations. In case of deeper fall, downside should be contained by 38.2% retracement of 1.2773 to 1.3651 at 1.3316 and bring rise resumption. Above 1.3651 will turn bias back to the upside for 1.3835 support turned resistance next. Break there will target 55 month EMA (now at 1.4405).

In the bigger picture, the strong break of 1.3444 key resistance now argues that the long term trend in GBP/USD has reversed. That is a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bullish as long as 1.2773 support holds.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9617; (P) 0.9667; (R1) 0.9747; More....

USD/CHF's rebound from 0.9420 resumed by taking out 0.9704 resistance. Intraday bias is now back on the upside for 0.9772 key resistance next. Decisive break there will suggest that whole down trend form 1.0342 has completed. In that case, near term outlook will be turned bullish for 0.9860/1.0099 resistance zone. Nonetheless, with 0.9772 resistance intact, outlook remains bearish. Below 0.9587 minor support will turn bias back to the downside for 0.9420 low.

In the bigger picture, current development suggests that 0.9443 key support (2016 low) could be taken out firmly as down trend form 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090. However, break of 0.9772 will indicate that USD/CHF has successfully defended 0.9443 again and turn outlook bullish for 1.0099 resistance.

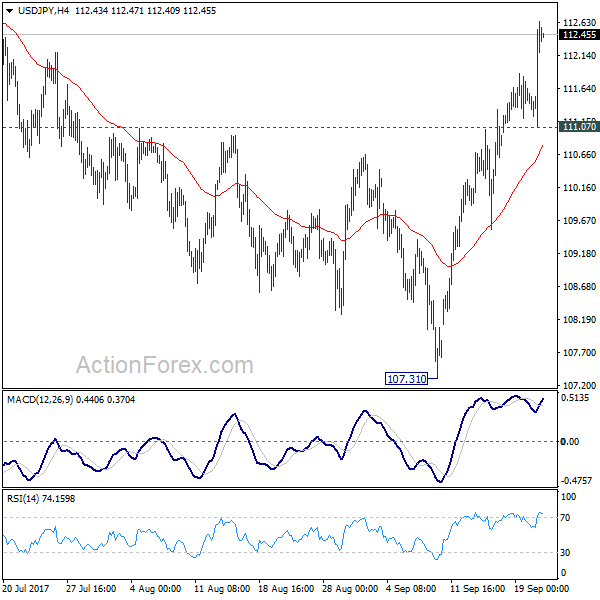

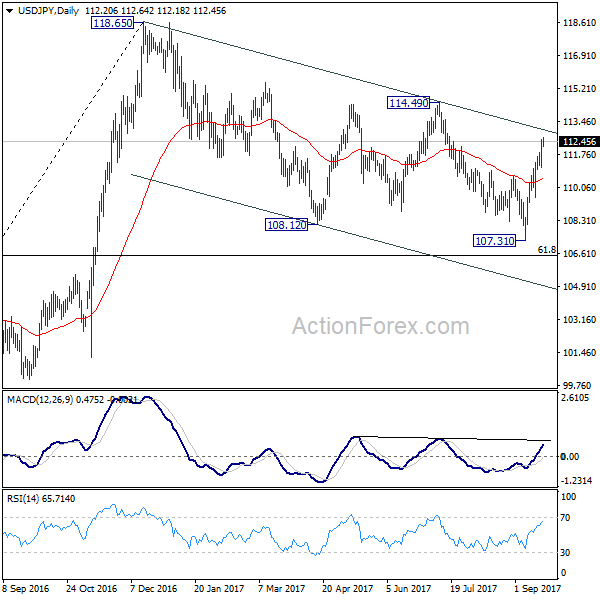

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.23; (P) 111.55; (R1) 111.92; More...

USD/JPY's rally from 107.31 extends to as high as 112.62 so far. Intraday bias is back on the upside for medium term channel resistance (now at 113.03). Sustained break there will argue that whole correction from 118.65 has completed too. In that case, further rise should be seen to 114.49 resistance for confirmation. On the downside, below 111.07 minor resistance will raise the risk of rejection from channel resistance and turn bias back to the downside for 55 day EMA (now at 110.53).

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.