Sample Category Title

Trade Idea Update: GBP/USD – Buy at 1.3125

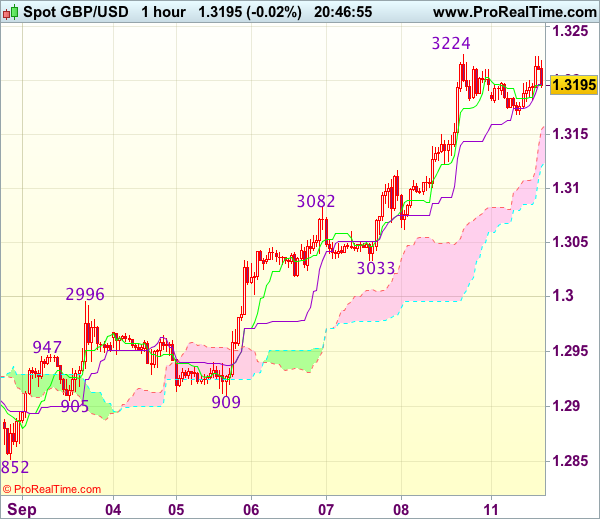

GBP/USD - 1.3196

Original strategy :

Buy at 1.3125, Target: 1.3225, Stop: 1.3090

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3125, Target: 1.3225, Stop: 1.3090

Position : -

Target : -

Stop : -

Last week’s rally to 1.3224 adds credence to our bullish view that recent upmove from 1.2774 is still in progress and upside bias remains for further gain to 1.3225-30, then towards 1.3250, however, loss of near term upward momentum should prevent sharp move beyond latter level and price should falter below recent high at 1.3269, bring retreat later.

In view of this, would not chase this rise at current level and would be prudent to buy cable on subsequent pullback as 1.3120-25 should limit downside. Only below 1.3082 (previous resistance turned support) would abort ad suggest top is possibly formed, risk test of 1.3062 but reckon support at 1.3033 would hold.

USD/CHF Throwback

USD/CHF has opened with a gap up and continues to increase on the daily chart. Looks like we had a false breakdown below the 0.9440 static support and under the lower median line (lml) of the minor descending pitchfork. A retest of the lower median line (lml) will confirm a further increase in the upcoming period, the next important upside target will be at the median line (ml) of the minor descending pitchfork.

Trade Idea Update: EUR/USD – Hold long entered at 1.1985

EUR/USD - 1.1984

Original strategy :

Bought at 1.1985, Target: 1.2090, Stop: 1.1950

Position : - Long at 1.1985

Target : - 1.2090

Stop : - 1.1950

New strategy :

Hold long entered at 1.1985, Target: 1.2090, Stop: 1.1950

Position : - Long at 1.1985

Target : - 1.2090

Stop : - 1.1950

Euro’s retreat after rising to 1.2093 late last week suggests consolidation below this level would be seen and marginal weakness from here cannot be ruled out, however, reckon downside would be limited and bring another rise later, above 1.2030 would suggest an intra-day low is formed, bring test of 1.2070-75, break there would signal the pullback from 1.2093 has ended, then retest of this resistance would follow but break there is needed to extend recent upmove towards 1.2150-55 (61.8% projection of 1.1119-1.1910 measuring from 1.1662).

In view of this, we are holding on to our long position entered at 1.1985. Below 1.1950 (previous resistance turned support) would signal a temporary top is formed instead bring weakness to 1.1925-30 first.

USDJPY: Triggers Corrective Recovery, Eyes 109.00 Zone

USDJPY: The pair saw a saw recovery during early trading today opening the door for correction in the days ahead. On the downside, support comes in at the 108.00 level where a break if seen will aim at the 107.50 level. A cut through here will turn focus to the 107.00 level and possibly lower towards the 106.50 level. On the upside, resistance resides at the 109.00 level. Further out, we envisage a possible move towards the 109.50 level. Further out, resistance resides at the 110.00 level with a turn above here aiming at the 110.50 level. On the whole, USDJPY now faces a recovery higher threats.

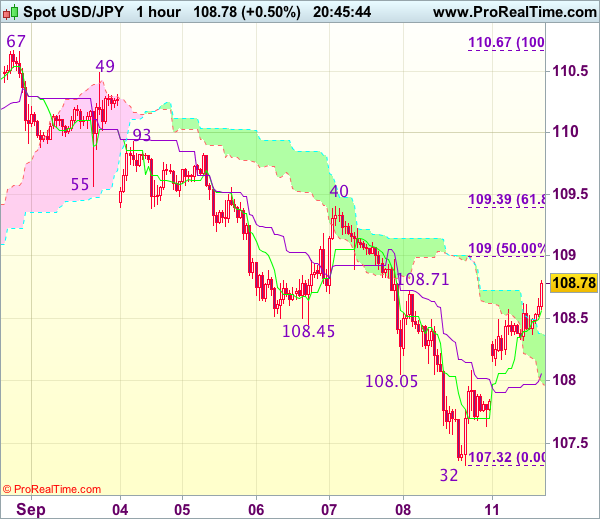

Trade Idea Update: USD/JPY – Sell at 109.35

USD/JPY - 108.79

Original strategy :

Sell at 108.90, Target: 107.70, Stop: 109.25

Position : -

Target : -

Stop : -

New strategy :

Sell at 109.35, Target: 108.35, Stop: 109.70

Position : -

Target : -

Stop : -

As the greenback opened higher today and has edged higher, suggesting near term upside risk remains for the rebound from last week’s low of 107.32 to extend gain to 109.00 (50% Fibonacci retracement of 110.67-107.32), however, still reckon upside would be limited to 109.39-40 (61.8% Fibonacci retracement and previous resistance) and bring retreat later, below the Kijun-Sen (now at 108.07) would suggest the rebound from 107.32 has possibly ended but break of 107.60-65 is needed to confirm and bring retest of 107.32.

In view of this, we are still looking to sell dollar on further recovery as 109.35-40 should limit upside, bring retreat later. Above 109.55 would defer and signal low has been formed, bring a stronger rebound towards resistance at 108.93 which is likely to hold from here due to near term overbought condition.

EURUSD Testse Key 1.2030 Level

The EURUSD pair continues to hold above the 1.2000 level, with price-action moving to test the key 1.2030 level, despite a minor relief rally in the U.S dollar index, and a lack of macroeconomic data from Europe and the United States.

The euro is currently confined to a tight trading range between the 1.1980 and 1.2040 region, with a higher time frame close above or below these levels needed to set a stronger intraday directional trend.

This week's EURUSD directional bias is likely to be set by U.S economic data, as we see a number of high impact inflation and consumer spending data points from the United States economy.

Key intraday resistance for the EURUSD pair is located at 1.2048, 1.2069 and 1.2092. Once above the 1.2092 level, traders should look for further bullish advancement towards the 1.2130, 1.2160 and 1.2230 levels.

Intraday corrections lower for the EURUSD pair should find initial support from the September 1st Nonfarm payrolls spike high, at 1.1979.

The euro's 100-hour moving average offer further support, at 1.1968, as does the 200-hour moving average, at 1.1935.

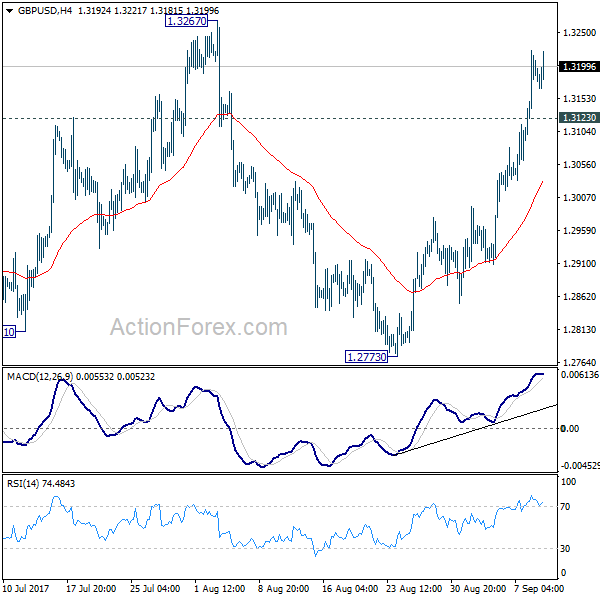

GBPUSD Back Above 1.3200

The GBPUSD pair has moved back above the 1.3200 level, after a minor correction to the 1.3168 support level, during the early European trading session.

Price-action continues to remain extremely bullish, with the pair increasingly likely to target the current monthly and yearly price highs, at 1.3224 and 1.3268

The GBPUSD pair is now starting to test the 1.3220 level, which is a key Fibonacci level, and represents the 50 percent retracement of the Brexit spike high at 1.5017, to the 2016 trading low, located at 1.1434.

Above the 1.3268 level, GBPUSD upside objectives remain 1.3300 and 1.3348.

The 100-week moving average and upside channel top also converge, at 1.3396.

To the downside, GBPUSD support is located at the daily pivot at 1.3180, and the current weekly low, at 1.3168.

Further support is located at the weekly pivot, at 1.3109, and the former monthly pivot, at 1.3080.

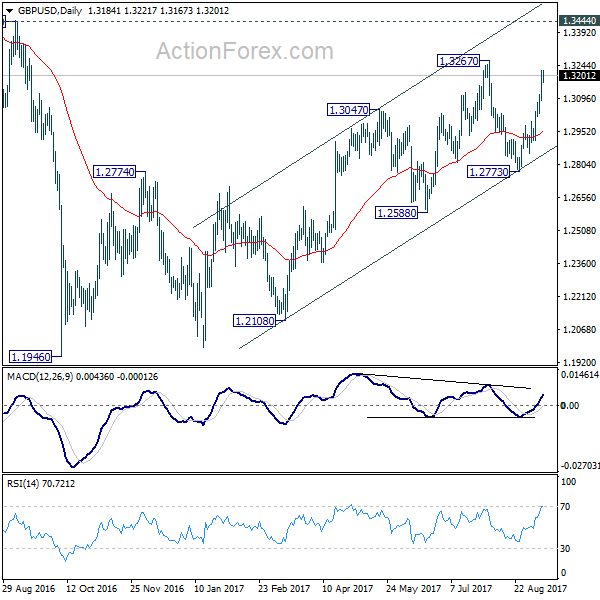

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3113; (P) 1.3168; (R1) 1.3245; More...

Intraday bias in GBP/USD remains on the upside and rise from 1.2773 should target 1.3267 resistance first. Break there will resume whole rise from 1.1946 and target 1.3444 key resistance next. But again, price actions from 1.1946 are still seen as a corrective pattern. Hence, we'd expect strong resistance from 1.3444 to limit upside to bring larger down trend reversal eventually. On the downside, below 1.3123 minor support will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2773 support will be the first sign that such down trend is resuming.

US Backs Down on Tough North Korea Sanctions, Sterling Jumps on BoE Talk

Dollar recovers mildly today as risk aversion eased slightly. Hurricane Irma is weakening as it moved past Tampa, Florida. Some analysts pointed out that damage of Irma is not as catastrophic as feared, even though it's still devastating. Meanwhile, North Korea risk is temporarily eased after the weekend. The US has backed down on pushing toughest sanctions on North Korea. A watered down version will be tabled for vote in UNSC today. While the greenback trades mildly higher, it's clearly outshone by Canadian Dollar and Sterling. Meanwhile, Yen and Swiss Franc are trading as the weakest ones. Gold is also notably weaker, hitting as low as 1335.2, comparing to Friday's high at 1362.4. WTI crude oil is hovering tight range below 48 handle.

US watered down its proposal on North Korea sanction, UNSC to vote

A major focus today will be on United Nation Security Councils' vote on fresh sanctions on North Korea. The US originally wanted to propose tougher measures that include bans on oil imports, textile exports and employment of works from North Korea. However, it's reported that the US has backed down and scaled back the proposal before the vote. Now, the revised draft dropped the proposed complete oil ban. It's changed to a cap on shipments of refined petroleum products at 2m barrels a year. Crude oil exports to North Korea would be maintained at current level. Workers ban was also diluted while freeze of leader Kim Jong-Un's assets and national airline Koryo is dropped too. But even after that, it's uncertain whether the proposal would be passed in UNSC. Two veto-holding members, Russia and China, are known to be against fresh sanctions on North Korea.

Meanwhile, geopolitical tension between the US and North Korea seemed to have eased moderately. North Korea did nothing provocative on the foundation day during the week end. However, North Korea did warned that "in case the U.S. eventually does rig up the illegal and unlawful 'resolution' on harsher sanctions, the DPRK shall make absolutely sure that the U.S. pays a due price.." And, "the forthcoming measures to be taken by the DPRK will cause the U.S. the greatest pain and suffering it had ever gone through in its entire history."

Sterling jumps on BoE talks, but it will face CPI test first

Sterling jumps broadly today on talk that BoE would step up its warning on interest rate later in the week. The central bank is widely expected to keep bank rate and asset purchase target unchanged. Based on current inflation outlook, there is also no imminent need for a hike. But BoE may reiterate that markets are under-estimating the scale of interest rate hikes in the coming years. And it may want households, business and investors to be well prepared. However, it should be noted that policy makers will have to look into inflation data to be released tomorrow. In particular, CPI is expected to climb back to 2.8% yoy in August. Any downside surprise there would intensify expectation that inflation won't hit 3% handle as BoE projected. And that would knock Sterling back down. Of course, focus will also be on whether hawks Michael Saunders and Ian McCafferty would change their mind on voting for rate hike too.

Before that, eyes will be on a parliamentary vote of the so called Brexit "Repeal Bill" today. In short, the bill seeks to copy and paste EU laws into UK legislation so that UK will have the same functioning laws and regulatory framework at the time of Brexit. Brexit Secretary David Davis warned that a vote against the bill is "a vote for chaotic exit from the European Union". And he emphasized that "businesses and individuals need reassurance that there will be no unexpected changes to our laws after exit day and that is exactly what the repeal bill provides. Without it, we would be approaching a cliff edge of uncertainty which is not in the interest of anyone." The government will need to secure the votes today to move on to the next phase of the legislation process. Opposition Labour Party has already indicated that they will vote against unless there are concessions.

ECB Coeure warned of exogenous shocks to the exchange rate

ECB Executive Board member Benoit Coeure said today "compared with past demand shocks, policy will remain more accommodative for longer, thereby likely muting further the pass-through of any growth-driven exchange rate appreciation." He noted that current recovery in Eurozone is "driven by domestic demand". Therefore, Euro strength might "have less of an impact on growth than, for example, after the Great Financial Crisis." Stronger than expected growth this is has prompted ECB policy makers to consider scaling back the quantitative easing program. Coeur noted that "at the current juncture, however, the policy-relevant horizon – the 'medium term' concept in our monetary policy strategy – is likely to be longer given the persistence of subdued inflationary pressures." And he warned that "exogenous shocks to the exchange rate, if persistent, can lead to an unwarranted tightening of financial conditions with undesirable consequences for the inflation outlook."

BoJ's ultra loose policy will destabilize the banking sector

A Japan Financial Services Agency adviser Naoki Ohgo warned that BoJ's stimulus program is severely cutting into bank profits. "Only a handful of regional banks successfully making money in niche areas." Others are struggling to find new business models. And, unless regional banks boost profitability it "might not take long" for BoJ's policies to finally destabilize the banking sector. Ohgo warned that "consolidation is inevitable". Meanwhile, Ohgo also pointed out that "despite abundant supply of cash in the economy, inflation did not reach 2 percent." Hence, "it's clear that monetary easing wasn't enough to generate inflation."

Released from Japan, machine orders rose 8.0% mom in July, M2 rose 4.0% yoy, tertiary industry index rose 0.1% mom in July. Machine tool orders rose 36.3% yoy in August.

China cut forex reserve requirement from 20% to 0%.

In China, the PBoC will unwind the rules on forex exchange forward reserve requirements that were implemented back in 2015. Back then the Renminbi exchange rate suffered prolonged depreciation after the devaluation in August 2015. The implementation of 20% reserve requirement was a move to halt the unwanted speculation in the exchanged rate. Effective today, the requirement is cut down to 0%. The move is seen by the markets as the government is adopting a more liberalized approach to Yuan trading. And it's also an act to soften restriction on capital outflow. Released over the weekend, China CPI accelerated to 1.6% yoy in August, up from 1.4% yoy. PPI slowed to 5.4% yoy, below 5.5% yoy.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3113; (P) 1.3168; (R1) 1.3245; More...

Intraday bias in GBP/USD remains on the upside and rise from 1.2773 should target 1.3267 resistance first. Break there will resume whole rise from 1.1946 and target 1.3444 key resistance next. But again, price actions from 1.1946 are still seen as a corrective pattern. Hence, we'd expect strong resistance from 1.3444 to limit upside to bring larger down trend reversal eventually. On the downside, below 1.3123 minor support will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2773 support will be the first sign that such down trend is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machine Orders M/M Jul | 8.00% | 4.10% | -1.90% | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Aug | 4.00% | 4.10% | 4.00% | |

| 4:30 | JPY | Tertiary Industry Index M/M Jul | 0.10% | 0.10% | 0.00% | |

| 6:00 | JPY | Machine Tool Orders Y/Y Aug P | 36.30% | 28.00% | ||

| 12:15 | CAD | Housing Starts Aug | 223K | 220.0K | 222.3K |

Gold Retreats As Risk Appetite Returns

Gold gapped down on Monday, but with the Dollar vulnerable to further losses, the yellow metal will likely remain supported in the long-term.

Gold lost some of its sparkle on Monday, having hit its highest level in over a year in the previous session, as risk appetite flickered back to life.

The market players who were bracing for North Korea to conduct another missile launch over the weekend to mark their foundation day, were relieved when Pyongyang decided to host a celebration instead. This reprieve has rekindled appetite for riskier assets, and supported the Greenback while punishing safehavens such as Gold. While the yellow metal may continue to edge lower amid the risk-on trading environment, the lingering air of caution is likely to limit downside losses.

The Dollar is still vulnerable to further losses, as expectations rapidly fade over the Federal Reserve raising US interest rates in December, so Gold is likely to remain supported moving forward. Further upside is still on the cards, especially when considering how heightened political uncertainty in Washington, geopolitical tensions and Brexit concerns continue to stimulate the flight to safety.

From a technical standpoint, Gold bulls are still in the game, despite the nasty drop from over the weekend. A breakout above $1340 should encourage a further appreciation higher towards $1350. In an alternative scenario, a breakdown and repeated weakness under $1325 is likely to encourage a decline towards $1315 and $1300, respectively.