Sample Category Title

UK’s Manufacturing Sector Activity Rose To A 4-Month High In August

For the 24 hours to 23:00 GMT, the GBP declined 0.12% against the USD and closed at 1.2926 on Friday.

On the macro front, the Markit manufacturing PMI unexpectedly climbed to a level of 56.9 in August, notching a four-month high level and defying market consensus for a fall to a level of 55.0. The PMI had recorded a revised level of 55.3 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.2955, with the GBP trading 0.22% higher against the USD from Friday's close.

The pair is expected to find support at 1.2919, and a fall through could take it to the next support level of 1.2884. The pair is expected to find its first resistance at 1.2977, and a rise through could take it to the next resistance level of 1.3000.

Moving ahead, market participants will keep a close watch on Britain's Markit construction PMI for August, due to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Reverses Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.19% against the JPY and closed at 110.27 on Friday.

In the Asian session, at GMT0300, the pair is trading at 109.8, with the USD trading 0.43% lower against the JPY from Friday's close.

Overnight data showed that Japan's monetary base rose 16.3% on an annual basis in August, higher than market expectations for an advance of 15.6%. The monetary base had recorded a revised gain of 15.7% in the prior month.

The pair is expected to find support at 109.42, and a fall through could take it to the next support level of 109.03. The pair is expected to find its first resistance at 110.33, and a rise through could take it to the next resistance level of 110.85.

Looking ahead, investors will closely monitor Japan's Nikkei services PMI for August, due to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

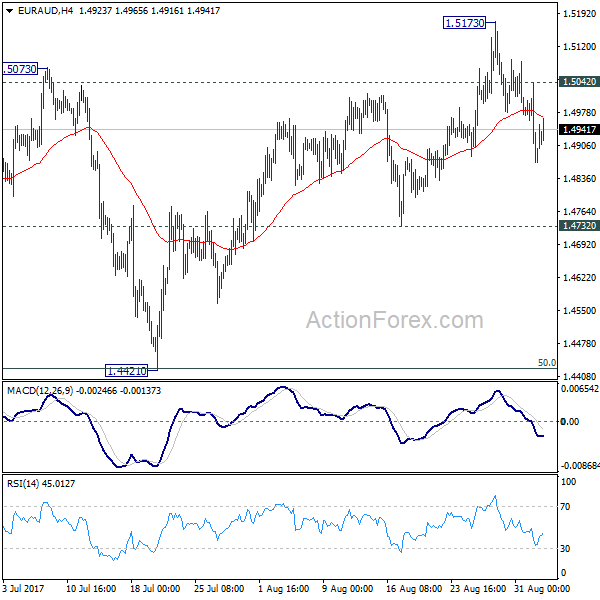

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4941; (P) 1.5014; (R1) 1.5057; More....

Intraday bias in EUR/AUD remains mildly on the downside for 1.4732 support. The cross could have failed 1.5226 resistance and rebound from 1.4421 is likely finished. Fall from 1.5173 is viewed as the third leg of the consolidation pattern from 1.5226. Break of 1.4372 will target 1.4421 again. But we'd expect strong support from there to contain downside and bring rebound. On the upside, above 1.5042 minor resistance will turn bias back to the upside for 1.5173 resistance instead.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

Switzerland’s Real Retail Sales Dipped In July

For the 24 hours to 23:00 GMT, the USD rose 0.55% against the CHF and closed at 0.9649 on Friday.

Macroeconomic data revealed that in Switzerland's real retail sales registered a drop of 0.7% on an annual basis in July, following a revised gain of 1.7% in the prior month.

On the other hand, the nation's SVME–manufacturing PMI unexpectedly rose to a level of 61.2 in August, confounding market consensus for a decline to a level of 60.2. The PMI had recorded a reading of 60.9 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 0.9608, with the USD trading 0.42% lower against the CHF from Friday's close.

The pair is expected to find support at 0.9552, and a fall through could take it to the next support level of 0.9497. The pair is expected to find its first resistance at 0.9658, and a rise through could take it to the next resistance level of 0.9709.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canadian Manufacturing Sector Growth Cooled In August

For the 24 hours to 23:00 GMT, the USD declined 0.75% against the CAD and closed at 1.2386 on Friday.

In economic news, data indicated that Canada’s Markit manufacturing PMI fell to a level of 54.6 in August, after recording a level of 55.5 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.2386, with the USD trading flat against the CAD from Friday’s close.

The pair is expected to find support at 1.2321, and a fall through could take it to the next support level of 1.2255. The pair is expected to find its first resistance at 1.2472, and a rise through could take it to the next resistance level of 1.2557.

Amid a holiday observed in Canada today, investor sentiment will be governed by global macroeconomic factors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

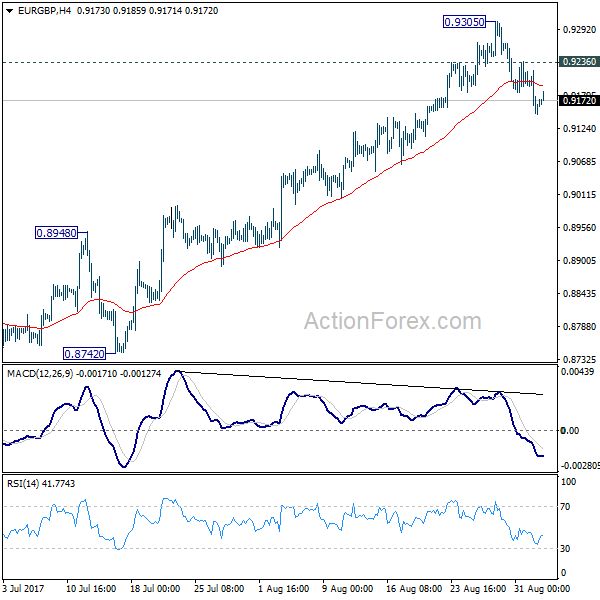

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.9128; (P) 0.9175; (R1) 0.9201; More

With 0.9236 minor resistance intact, decline from 0.9305 short term top is expected to extend to 55 day EMA (now at 0.8998). Sustained trading below there will likely start the third leg of the consolidation from 0.9304 and target 0.8303 key support again. On the upside, above 0.9236 minor resistance will turn bias back to the upside for 0.9305 instead.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes. Firm break of 0.9799 high will target 61.8% projection of 0.5680 to 0.9799 from 0.6935 at 1.1054.

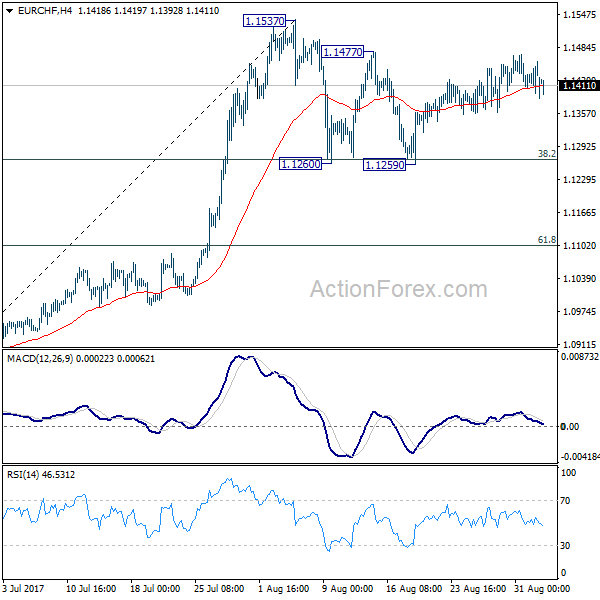

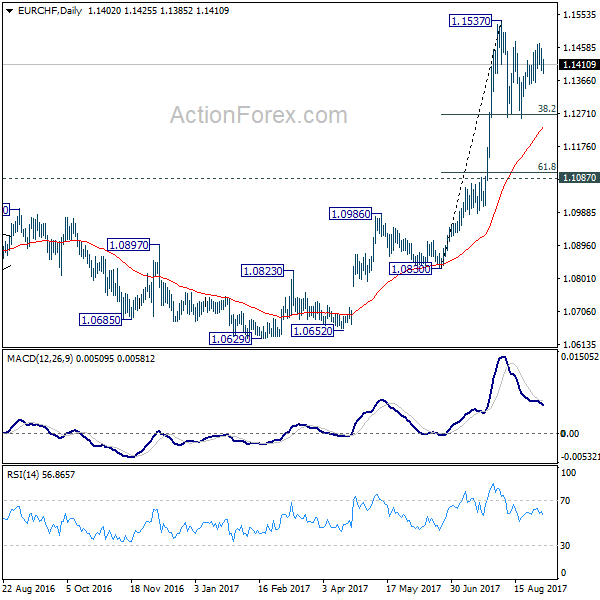

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1403; (P) 1.1430; (R1) 1.1465; More...

Intraday bias in EUR/CHF remains neutral as it's staying in consolidation from 1.1537. On the upside, break of 1.1537 resistance will confirm resumption of larger rally from 1.0629. In that case, EUR/CHF should target 1.2 key resistance level next. On the downside, firm break of 38.2% retracement of 1.0830 to 1.1537 at 1.1267 will extend the correction to 61.8% retracement at 1.1100 before completion.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

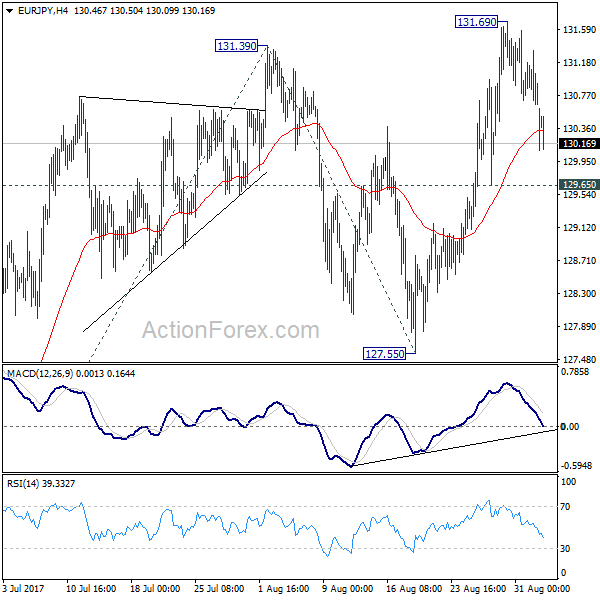

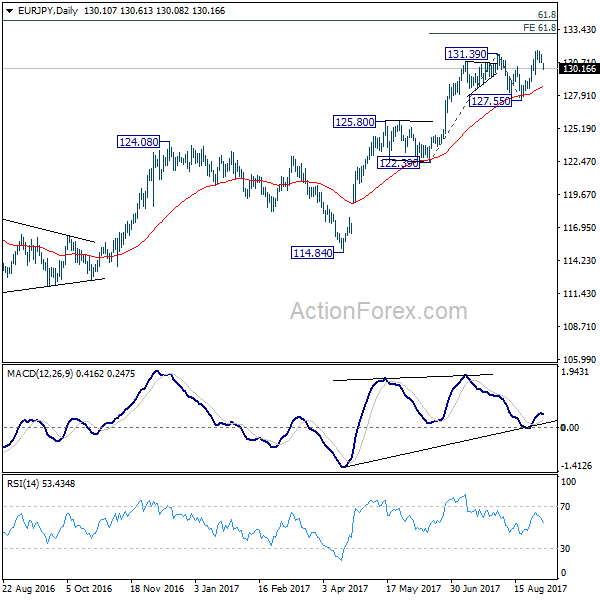

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.49; (P) 130.92; (R1) 131.17; More...

EUR/JPY drops sharply today but it's staying above 129.65 minor support for the moment. Intraday bias remains neutral and another rise is still mildly in favor. Break of 131.69 will extend the larger up trend to 61.8% projection of 122.39 to 131.39 from 127.55 at 133.11 next. However, break of 129.65 will dampen the bullish case and turn bias back to the downside for 127.55 support instead.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 124.08 resistance turned support holds. However, firm break of 124.08 will argue that rise from 109.03 is completed and turn outlook bearish.

Daily Technical Analysis: EUR/USD Waiting To Break Triangle Chart Pattern

Currency pair EUR/USD

The EUR/USD could be building an ABC (red) correction within a larger wave 4 (blue) pattern. A break below the support trend line (blue) would increase the likelihood of such an ABC. The ABC correction (red) is invalidated if price breaks above the 138.2% Fib at 1.2165. A break above the resistance trend line (red) could indicate that there is bullish pressure to test the Fib levels of wave B vs A.

The EUR/USD is building a triangle chart pattern which is indicated by the trend lines (red/blue).

Currency pair USD/JPY

The USD/JPY continues with its sideways correction between the support zone and the resistance levels (red line and red box). For the moment a larger bullish wave C (orange) still seems more likely.

The USD/JPY has completed a bearish ABC (green) correction which could indicate a potential bullish bounce. But the overall market structure remains choopy.

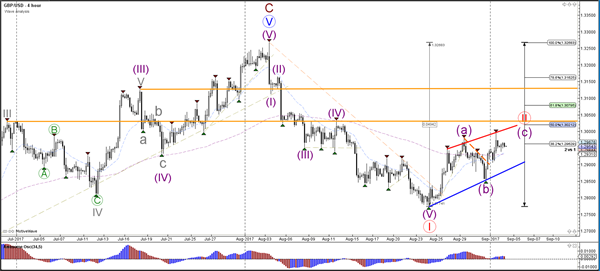

Currency pair GBP/USD

The GBP/USD is building a corrective bullish channel (red/blue). The bullish price action is probably part of a wave 2 (red).

The GBP/USD seems to have completed an ABC (green) correction within wave B (grey), which could indicate that a new bearish correction could take place within an expanded wave B (purple).

European Open Briefing: Asian Equities Fell Early On Monday

Global Markets:

- Asian stock markets: Nikkei down 0.97 %, Shanghai Composite rose 0.18 %, Hang Seng lost 0.39 %, ASX 200 fell 0.28 %

- Commodities: Gold at $1339.26 (+0.67 %), Silver at $17.92 (+0.59 %), WTI Oil at $47.44 +(0.32 %), Brent Oil at $52.52 (-0.44 %)

- Rates: US 10-year yield at 2.16, UK 10-year yield at 1.06, German 10-year yield at 0.38

News & Data:

- AUD Company Operating Profits q/q -4.5 % vs -3.9 % expected

- CNY Caixin Manufacturing PMI 51.6 vs 50.9 expected

- EUR Spanish Manufacturing PMI 52.4 vs 54.4 expected

- GBP Manufacturing PMI 56.9 vs 55.0 expected

- USD Average Hourly Earnings m/m 0.1 % vs 0.2 % expected

- USD Non-Farm Employment Change 156 K vs 180 K expected

- USD Unemployment Rate 4.4 % vs 4.3 % expected

- USD ISM Manufacturing PMI 58.8 vs 56.5 expected

- USD Revised UoM Consumer Sentiment 96.8 vs 97.4 expected

- Japan PM Abe Says Aim to Increase Missile Defence Capabilities – RTRS

- Oil markets volatile in wake of Hurricane Harvey, North Korea nuclear test – RTRS

CFTC Positioning Data:

- EUR long 87K vs 88K long last week. Longs decreased by 1K

- GBP short 52K vs 46K short last week. Shorts increased 6K

- JPY short 69K vs 74K short last week. Shorts trimmed by 5K

- CHF short 2K vs 2K short last week. Unchanged from prior week.

- CAD long 53K vs 51K long. Longs increased by 2K.

- AUD long 67k vs 60k last week. Longs increased by 7K

- NZD long 19K vs 22K long last week. Longs trimmed by 3K

Markets Update:

Asian equities fell early on Monday as market participants turned to haven assets after North Korea's latest nuclear test on Sunday sending the yen, gold and Sovereign bonds higher. Following this, U.S. President Trump threatened to increase economic sanctions and halt trade with any nation doing business with Kim Jong Un's regime

USD/JPY dropped around a big figure from late Friday levels falling as deep as 109.22 early on Monday, currently the pair is seen trading around 109.80 as there were no follow through selling after the inirial drop. Overall the yen has climbed 0.4 percent against the US dollar. Japan is the world's largest creditor nation and traders tend to assume Japanese investors would repatriate funds at times of crisis, thus pushing up the yen

EURUSD opened a few points net higher for the session and is currently seen trading at 1.8820, overall the Euro has climbed 0.2 percent against the US Dollar. The investors are wary ahead of a European Central Bank meeting on Thursday as there have been reports some at the ECB are unhappy with the euro's strength. The Dollar Index slipped 0.1 percent and currently trading at 92.68.

AUDUSD has recovered from its early losses and is currently seen trading back around 0.7962. Earlier on Monday, the Australian dollar had lost 0.2 percent against the US Dollar dropping to lows of 0.7946. On the other side, the kiwi has strengthened against the US Dollar following a minor drop earlier in the session, Currently the NZDUSD is seen trading at 0.7175 gaining 30+ pips from today's opening.

Upcoming Events:

- USD Bank Holiday

- CAD Bank Holiday

- 07:00 GMT – (EUR) Spanish Unemployment Change

- 08:30 GMT – (GBP) Construction PMI

- 11:30 GMT – (GBP) BRC Retail Sales Monitor y/y

The Week Ahead:

Tuesday, September 5th

- 01:30 GMT – (AUD) Current Account

- 04:30 GMT – (AUD) Cash Rate

- 04:30 GMT – (AUD) RBA Rate Statement

- 07:15 GMT – (CHF) CPI m/m

- 08:30 GMT – (GBP) Services PMI

- 09:10 GMT – (AUD) RBA Gov Lowe Speaks

- 12:00 GMT – (USD) FOMC Member Brainard Speaks

- 14:00 GMT – (USD) Factory Orders m/m

- 17:10 GMT – (USD) FOMC Member Kashkari Speaks

- 22:05 GMT – (USD) FOMC Member Kaplan Speaks

Wednesday, September 5th

- 01:30 GMT – (AUD) GDF q/q

- 12:30 GMT – (CAD) Trade Balance

- 12:30 GMT – (CAD) Labor Productivity q/q

- 12:30 GMT – (USD) Trade Balance

- 14:00 GMT – (CAD) BOC Rate Statement

- 14:00 GMT – (CAD) Overnight Rate

- 14:00 GMT – (USD) ISM Non-Manufacturing PMI

Thursday, September 6th

- 01:30 GMT – (AUD) Retail Sales m/m

- 01:30 GMT – (AUD) Trade Balance

- 07:30 GMT – (GBP) Halifax HPI m/m

- 11:45 GMT – (EUR) Minimum Bid Rate

- 12:30 GMT – (CAD) Building Permits m/m

- 12:30 GMT – (EUR) ECB Press Conference

- 12:30 GMT – (USD) Unemployment Claims

- 14:00 GMT – (CAD) Ivey PMI

- 15:00 GMT – (USD) Crude Oil Inventories

- 23:00 GMT – (USD) FOMC Member Dudley Speaks

- 23:50 GMT – (JPY) Final GDP q/q

Friday, September 7th

- Tentative– (CNY) Trade Balance

- 03:00 GMT – (AUD) RBA Assist Gov Debelle Speaks

- 08:30 GMT – (AUD) RBA Gov Lowe Speaks

- 08:30 GMT – (GBP) Manufacturing Production m/m

- 08:30 GMT – (GBP) Goods Trade Balance

- 12:30 GMT – (CAD) Employment Change

- 12:30 GMT – (CAD) Unemployment Rate

- 12:45 GMT – (USD) FOMC Member Harker Speaks