Sample Category Title

USD/CAD Weekly Outlook

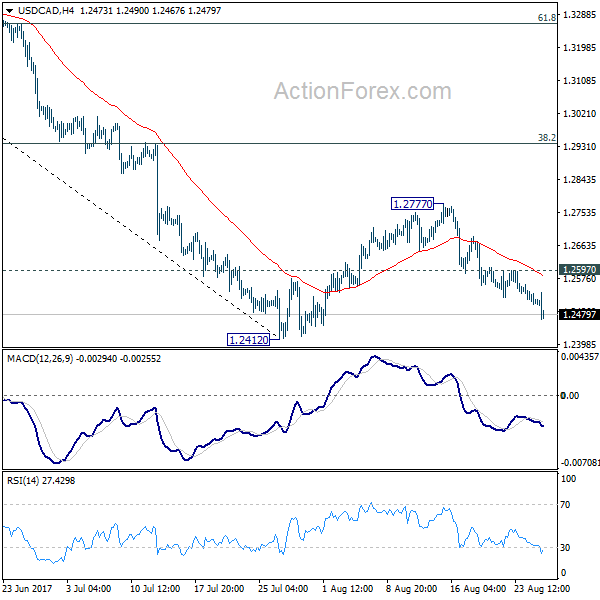

USD/CAD's decline from 1.2777 extended lower last week. The development affirmed the case that correction from 1.2412 has already completed and larger fall is resuming. Initial bias stays on the downside this week for 1.2412 first. Decisive break there will target next long term fibonacci level at 1.2048. On the upside, above 1.2597 minor resistance will extend the correction from 1.2412 with another rise. But we'd expect upside to be limited by 38.2% retracement of 1.3793 to 1.2412 at 1.2940 to bring fall resumption eventually.

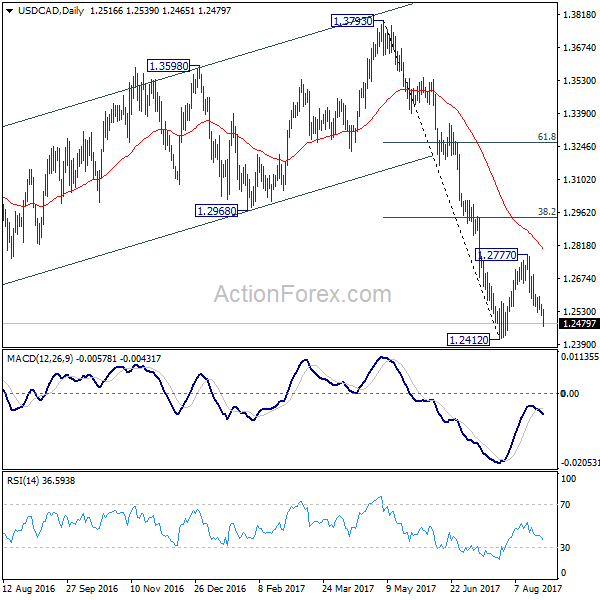

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is still expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Nonetheless, on the upside, sustained break of 1.2968, 38.2% retracement of 1.3793 to 1.2412 at 1.2940 will be the first sign of completion of the correction and will turn focus back to 1.3793 key resistance.

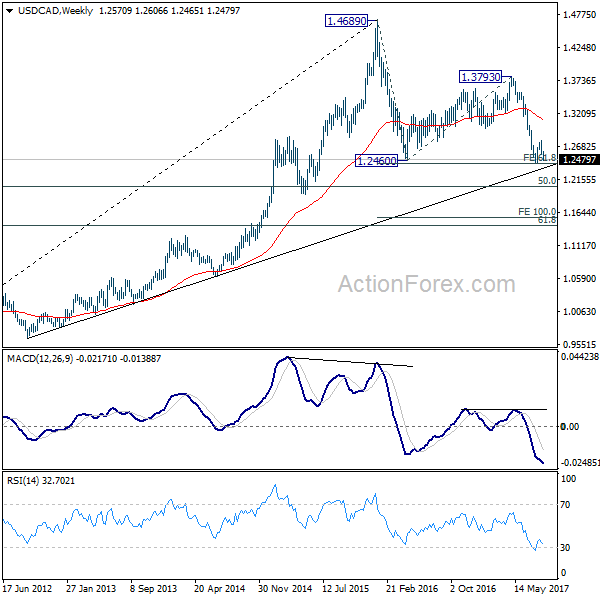

In the longer term picture, rise from 0.9056 (2007 low) is viewed as a long term up trend. It's taking a breath after hitting 1.4689. But such rise is expected to resume later to test 1.6196 down the road. But firm break of 50% retracement of 0.9406 to 1.4869 at 1.2048 will raise doubt over this view. In that case, the long term trend could have reversed.

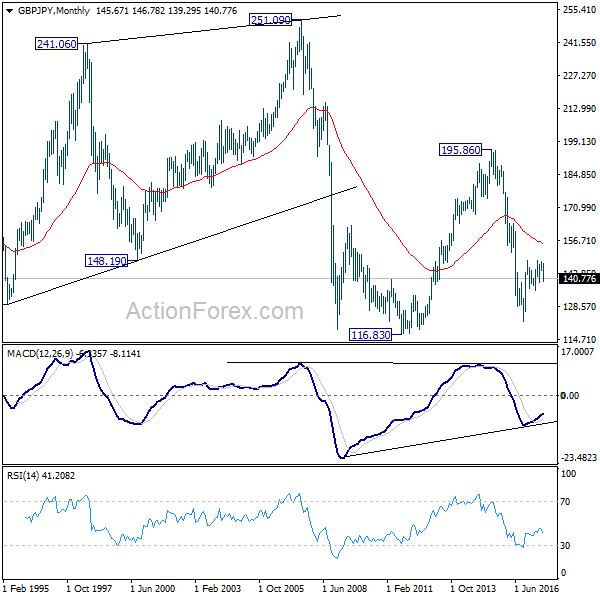

GBP/JPY Weekly Outlook

GBP/JPY edged lower to 139.29 last week but formed a temporary low there and recovered. Initial bias is neutral this week first. Near term outlook remains bearish as long as 143.18 resistance holds and deeper decline is in favor. Below 139.29 will target 135.58 key support level. At this point, price actions from 148.42 are seen as a sideway consolidation pattern. Hence, we'll expect strong support from 135.58 to contain downside and bring rebound. Meanwhile, break of 143.18 will indicate short term reversal and turn bias back to the upside.

In the bigger picture, the sideway pattern from 148.42 is extending with another leg. We'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise from 122.36 is still expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

In the longer term picture, it remains to be confirmed if whole down trend from 195.86 has completed at 122.36 already and there is no confirmation yet. But in any case, firm break of 38.2% retracement of 195.86 to 122.36 at 150.43 would pave the way to 61.8% retracement at 167.78. And with that, the 55 month EMA will be firmly taken out which suggests that price actions from 116.83 is indeed a sideway pattern that could last more than a decade.

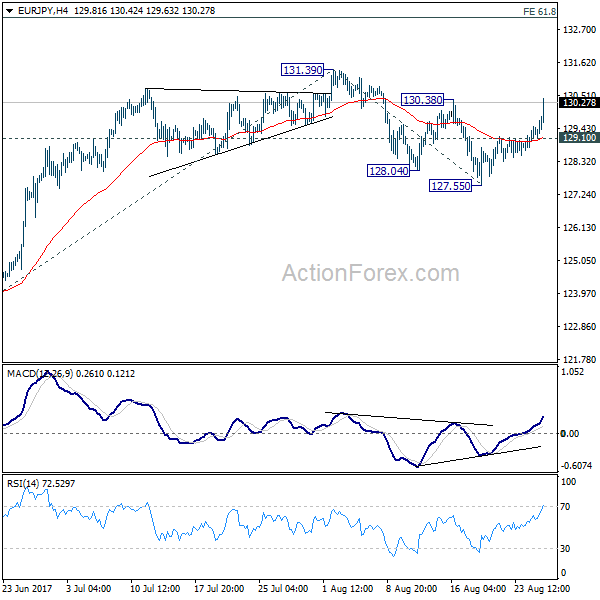

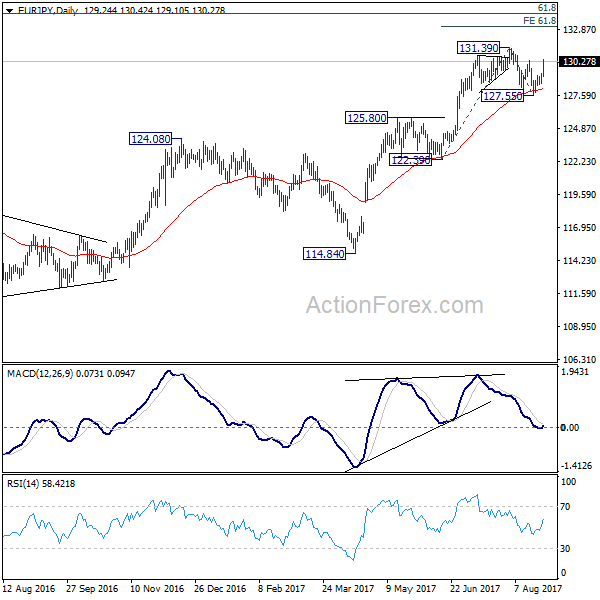

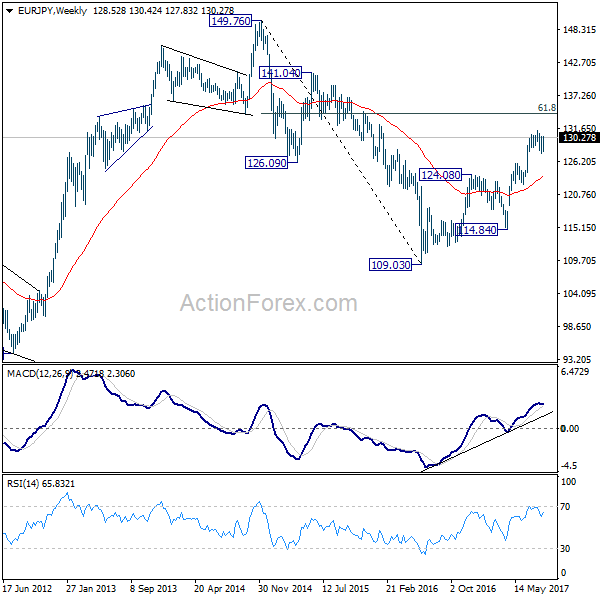

EUR/JPY Weekly Outlook

EUR/JPY's strong rebound last week and breached of 130.38 resistance suggests that correction from 131.39 has completed at 127.55 already, after hitting 55 day EMA. Initial bias is back on the upside this week for 131.39 high first. Break there will extend larger rally to 61.8% projection of 122.39 to 131.39 from 127.55 at 133.11 next. On the downside, below 129.10 minor support will dampen this bullish view and turn focus back to 127.55 support instead.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 124.08 resistance turned support holds. However, firm break of 124.08 will argue that rise from 109.03 is completed and turn outlook bearish.

In the long term picture, at this point, there is no clear indication that rise from 109.03 is resuming that from 94.11. Hence, we'd be cautious on topping below 149.76 to extend range trading. Nonetheless, firm break of 149.76 will indicates strong underlying buying. In such case, EUR/JPY will target 100% projection of 94.11 to 149.76 from 109.03 at 164.68.

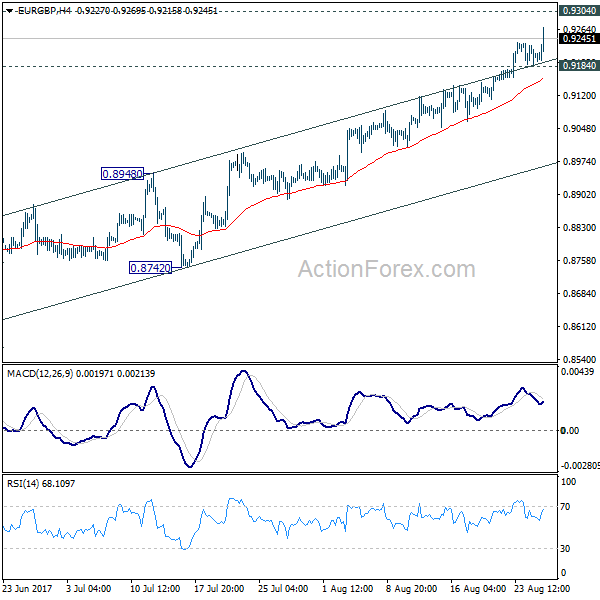

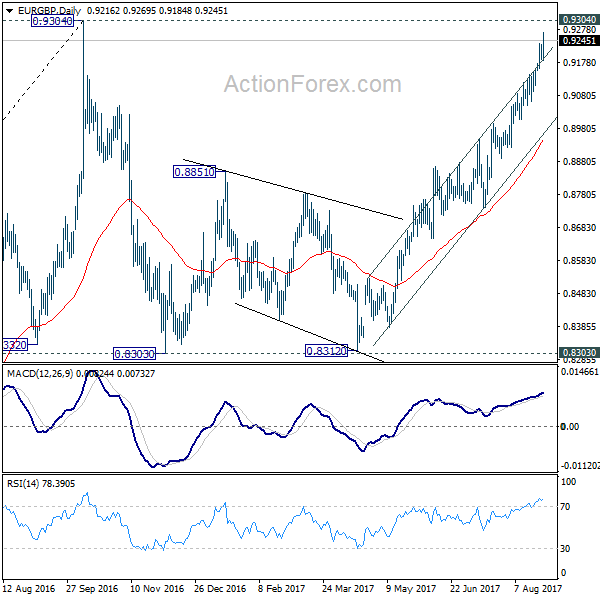

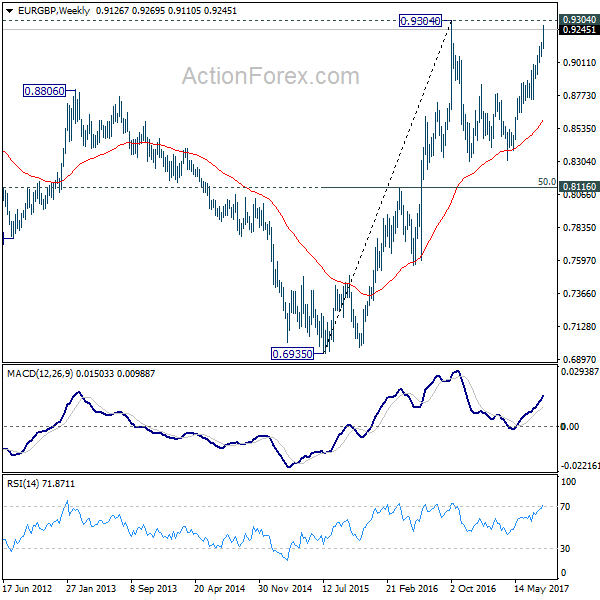

EUR/GBP Weekly Outlook

EUR/GBP's rally from 0.8312 continued last week and reached as high as 0.9269. Initial bias stays on the upside for 0.9304 high next. We'd remain cautious on rejection fro 0.9304 to extend the medium term consolidation pattern. Break of 0.9184 will turn bias back to the downside for pull back to 55 day EMA (now at 0.8948). However, sustained break of 0.9304 will confirm up trend resumption and pave the way to 0.9799.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes. Firm break of 0.9799 high will target 61.8% projection of 0.5680 to 0.9799 from 0.6935 at 1.1054.

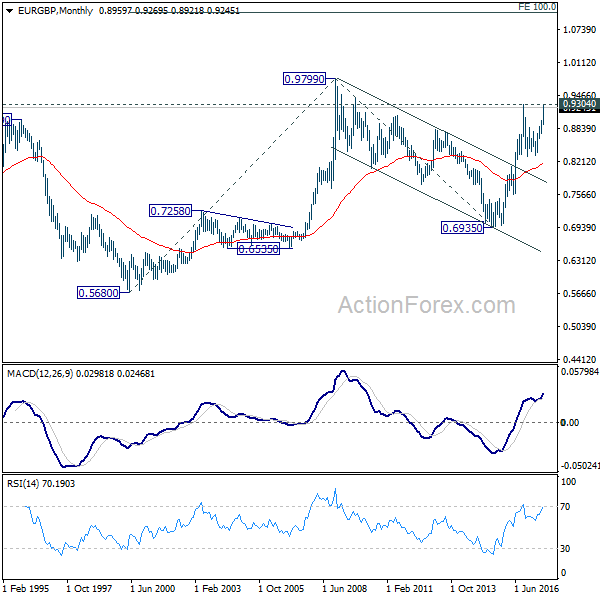

In the long term picture, firstly, price action from 0.9799 (2008 high) is seen as a long term corrective pattern and should have completed at 0.6935 (2015 low). Secondly, rise from 0.6935 is likely resuming up trend from 0.5680 (2000 low). Thirdly, this is supported by the impulsive structure of the rise from 0.6935 to 0.9304. Hence, after the correction from 0.9304 completes, we'd expect another medium term up trend through 0.9799 to 61.8% projection of 0.5680 to 0.9799 from 0.6935 at 1.1054.

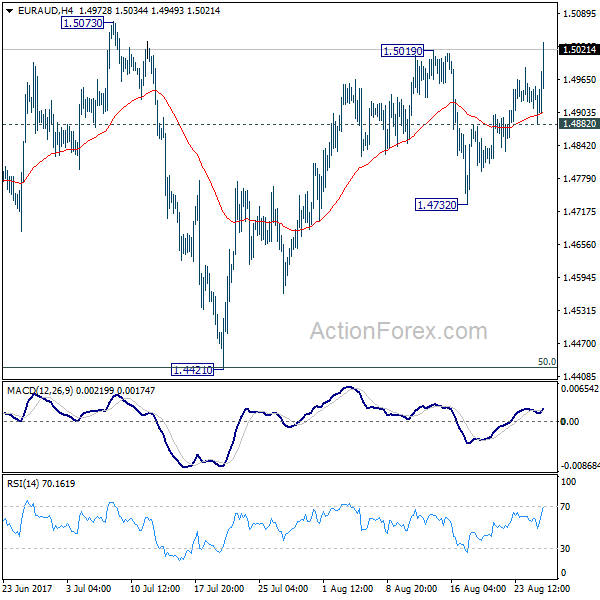

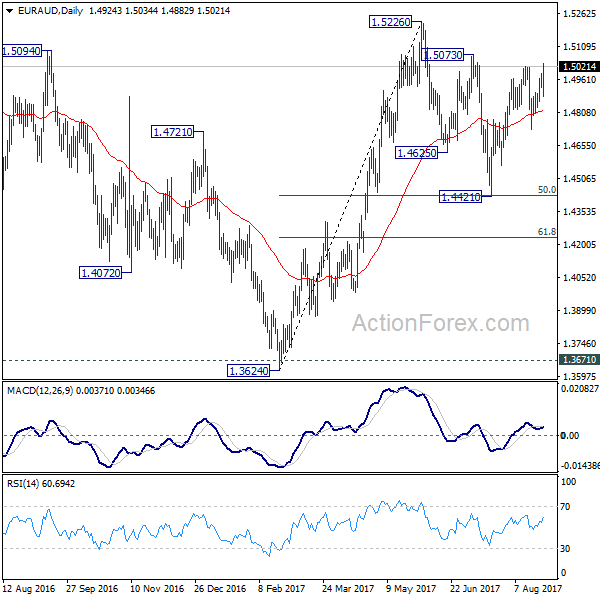

EUR/AUD Weekly Outlook

EUR/AUD's rally and break of 1.5019 last week suggests that rebound from 1.4421 has resumed. More importantly, it revived the case that correction from 1.5226 has completed with three waves down to 1.4421. Initial bias is back on the upside this week for 1.5073 resistance first. Break there will affirm the case that whole rebound from 1.3624 is resuming and target 1.5226 high. On the downside, below 1.4882 minor support will turn intraday bias neutral first. But outlook will remain cautiously bullish as long as 1.4732 support holds.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the fall from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

In the longer term picture, the rise from 1.1602 long term bottom isn't over yet. We'll keep monitoring the development but there is prospect of extending the rise to 61.8% retracement of 2.1127 to 1.1602 at 1.7488 and above. However, sustained trading below 1.3671 should confirm trend reversal and target 1.1602 long term bottom again.

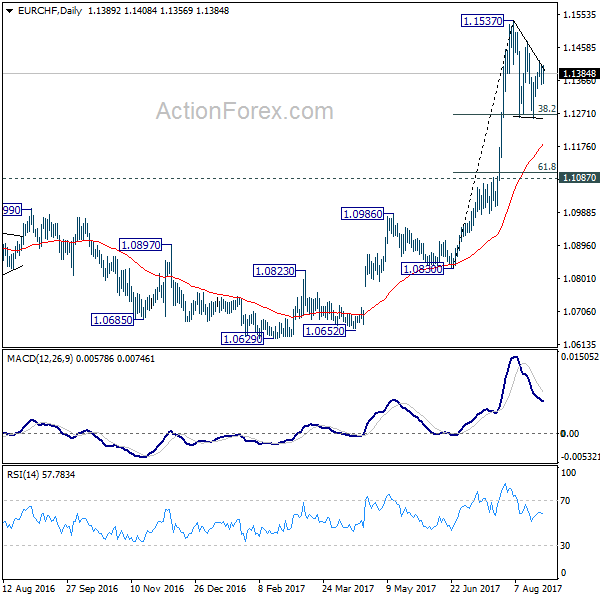

EUR/CHF Weekly Outlook

EUR/CHF stayed in the consolidation pattern from 1.1537 last week and outlook is unchanged. Initial bias stays neutral this week first. On the upside, break of break of 1.1477 resistance will argue that the consolidation from 1.1537 has completed and larger rise is resuming. Further break of 1.1537 will confirm and target 1.2 key resistance level next. On the downside, however, firm break of 38.2% retracement of 1.0830 to 1.1537 at 1.1267 will extend the correction to 61.8% retracement at 1.1100 before completion.

In the bigger picture, firm break of 1.1198 key resistance confirms resumption of the long term rise from SNB spike low back in 2015. In this case, EUR/CHF would eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

Business Back to Usual after Jackson Hole, EUR/USD Surged to New High

Dollar ended the week as a big loser after the highly anticipated Jackson Hole Symposium. It was pointed out before that there were little expectations for comments on monetary policies from Fed Chair Janet Yellen and ECB President Mario Draghi. And the reactions indeed showed that traders were relieved by the lack on cover on monetary policies. And business returned to usual with EUR/USD resuming recent up trend while Dollar was back under pressure. While Dollar still managed to end higher against Yen, near term outlook remained bearish in USD/JPY and it's just a matter of time to see downside breakout in the pair. Focus will now turn to key economic data including non-farm payroll from US but it's unlikely to safe the Dollar. Another focus to watch this week is another round of Brexit negotiation.

Fed Yellen defended post crisis regulations

Yellen didn't touch on Fed's monetary policy in her speech Financial Stability a Decade after the Onset of the Crisis. Instead, she made use of this high profile occasion to openly defend the post financial crisis regulations. And that is seen as a statement that she will not turn her back on the reforms even if she's re-appointed as Fed chair after the current term expires in February. Yellen emphasized that "the events of crisis demanded action, needed reforms were implemented and these reforms have made the system safer". And she warned that "already, for some memories of this experience may be fading - memories of just how costly the financial crisis was and why certain steps were taken in response". And she pointed out that "the balance of research suggests that the core reforms we have put in place have substantially boosted resilience without unduly limiting credit availability or economic growth."

... that's effectively sending resignation to Trump

Yellen also pledged that "the Federal Reserve is committed to evaluating where reforms are working and where improvements are needed to most efficiently maintain a resilient financial system." And, "any adjustments to the regulatory framework should be modest and preserve the increase in resilience at large dealers and banks associated with the reforms put in place in recent years." Some analysts saw Yellen's speech as equivalent to submission of resignation to US President Donald Trump for the job of Fed chair. Trump has been openly attacking the regulations since the 2010 Dodd-Frank act and criticized that they hurt lending and the economy. Yellen's message is clear that if she's taken as Fed chair again, she's going to defend the regulations to the end.

...but front-runner Cohn also ruled himself out

According to a recent survey by the National Association for Business Economics, only 17% expected Fed Chair Janet Yellen would be offered a second term. Among the contenders, 49% expect White House economic adviser Gary Cohn would be picked for the top Fed job. Cohn said earlier in February that "we're going to attack all aspects of Dodd-Frank". But at the same time, it's reported by the New York Times yesterday that Cohn has indeed drafted a resignation letter to Trump after the latter blamed "both sides" for the violence at a rally by white supremacists and neo-Nazis in Charlottesville. Cohn also said in an interview by the Financial Times yesterday that he was "compelled to voice his distress over the events of the last two weeks" even though he didn't want to leave the job. And, Roger Stone, a long time adviser to Trump, tweeted that Cohn should be "fired immediately for his public attack on the president".

Uncertainties to continue to weigh on Dollar

So now, the one thing that is pretty sure is that Fed will announce unwinding of the balance sheet in September. It's a big question if Fed will hike again in December, and fed fund futures are pricing in around 40% chance of that. It's another big question who will lead Fed after February. And it's question what policy bias would Fed adopt after that. It's probably even a bigger question whether the Congress would raise the debt ceiling on time to avoid government shut down or debt default, with or without the border wall. And, not to mention, given the never-ending drama in the White House, it's uncertain when the promised tax reforms and infrastructure spending be done. All these development will be dollar negative in near term.

Draghi touched lightly on monetary policy

Draghi didn't touch much on ECB's monetary policy neither. He just noted that "we haven't seen yet that self-sustained convergence of inflation toward our objective, our medium-term objective." And, "on one hand, we are confident that as the output gap closes, inflation will continue to converge to its objective over the medium term. On the other, we have to be very patient" and "a significant degree of monetary accommodation is still warranted." The key takeaway regarding monetary policy is that Draghi isn't too concerned with the current outlook of inflation, growth nor the exchange rate. And he will wait for the September meeting with other policymakers for discussions on tapering the asset purchases or stimulus exit.

...urged to fight protectionism

Instead, Draghi made use of the podium to talk about global challenges in his speech titled Sustaining Openness in a Dynamic Global Economy. He emphasized that "openness to trade is under threat, and this means that policies aimed at answering this backlash are a vital part of the policy mix for dynamic growth." And he warned that "a turn towards protectionism would pose a serious risk for continued productivity growth and potential growth in the global economy." He pointed out that protectionism is a risk that "is particularly acute in the light of the structural challenges facing advanced economies." Also, "to foster a dynamic global economy we need to resist protectionist urges. But to do so, we also need to identify how best to respond to protectionism."

Dollar index to take on 91.91/3 key cluster

The dollar index finally broke out of recent rate and resumed the medium term decline from 103.82. Initial bias is now on the downside this week for 91.91/3 key cluster support zone (38.2% retracement of 72.69 to 103.82 at 91.93). Outlook is unchanged that such decline is correcting the long term up trend from 2011 low at 72.69 to 2017 high at 103.82. The index is now at a juncture as it's close to key cluster support level at 91.91/3 with oversold condition in weekly RSI. Theocratically, a sustained rebound is due. But we haven't seen any sign of buying yet. Near term outlook will remain bearish as long as 94.14 resistance holds. Sustained break of 91.91/3 will extend whole correction from 103.82 to 50% retracement at 88.25 and below.

Trading strategy: Hold EUR/USD long

Regarding trading strategies, our bearish view on NZD/JPY was correct as the cross resumed the fall from 83.90 last week by taking out 79.07. Nonetheless, our sell NZD/JPY at 80.85 was not filled again. We'll cancel it first. On the other hand, we bought EUR/USD on break at 1.1846. The pair's up trend from 1.0339 resumed by taking out 1.1908 and confirmed our bullish view. We'll hold on to EUR/USD long, with stop raised to 1.1770. Target will be long term fibonacci level at 1.2516.

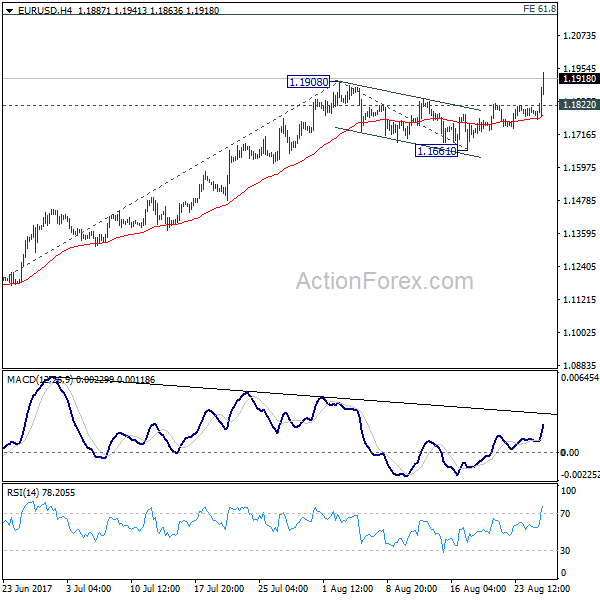

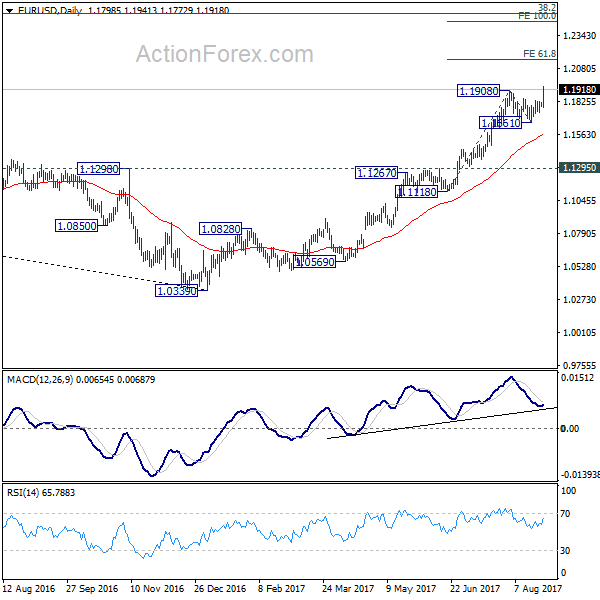

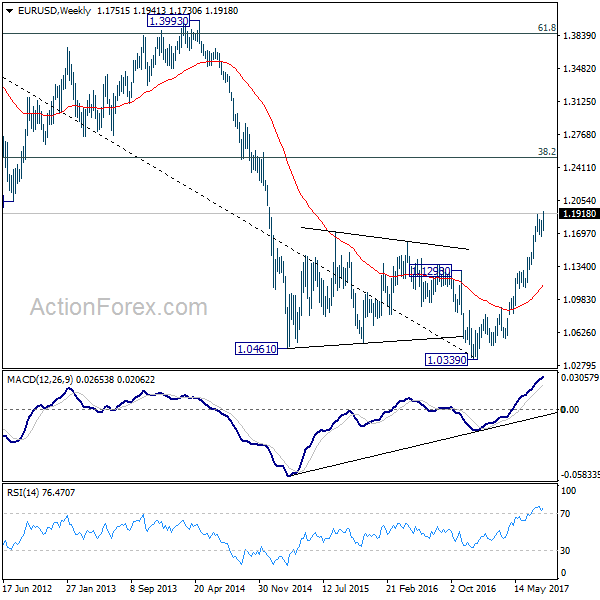

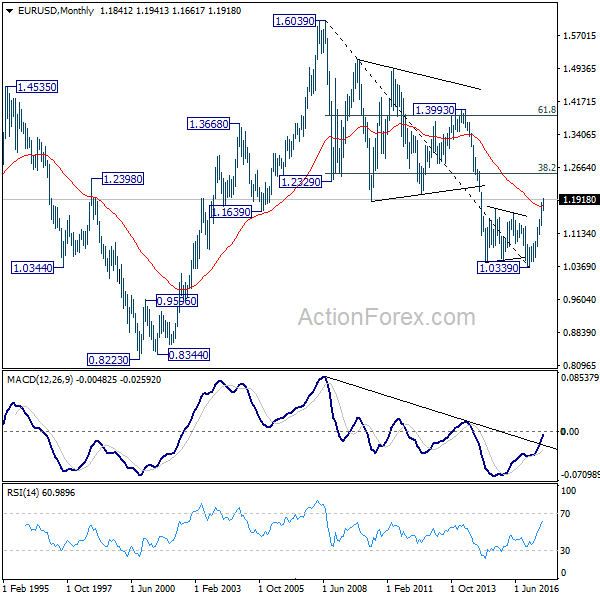

EUR/USD Weekly Outlook

EUR/USD 's up trend resumed last week by breaking 1.1908 resistance and reached as high as 1.1941. Initial bias is back on the upside this week. Current rally should target 61.8% projection of 1.1118 to 1.1908 from 1.1661 at 1.2149 first. Break there will target 100% projection at 1.2451 next. On the downside, below 1.1822 minor support will turn intraday bias neutral first. But retreat should be contained above 1.1661 support and bring rise resumption.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. For now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

In the long term picture, 1.0339 is now seen as an important bottom as the down trend from 1.6039 (2008 high) could have completed. It's still early to decide whether price action form 1.0339 is developing into a corrective or impulsive move. But in either case, further rally would be seen to 38.2% retracement of 1.6039 to 1.0339 at 1.2516

Eco Data 9/1/17

[php_everywhere] [/php_everywhere]

Eco Data 8/31/17

[php_everywhere] [/php_everywhere]

Eco Data 8/30/17

[php_everywhere] [/php_everywhere]