Sample Category Title

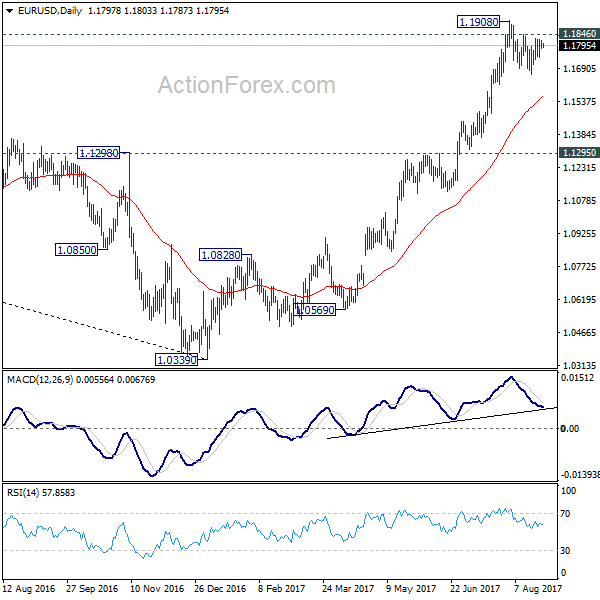

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1782; (P) 1.1800 (R1) 1.1816; More...

Intraday bias in EUR/USD remains neutral as consolidation from 1.1908 is still in progress. In case of another fall, downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring up trend resumption. Break of 1.1846 minor resistance will argue that larger rise from 1.0339 is resuming for 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

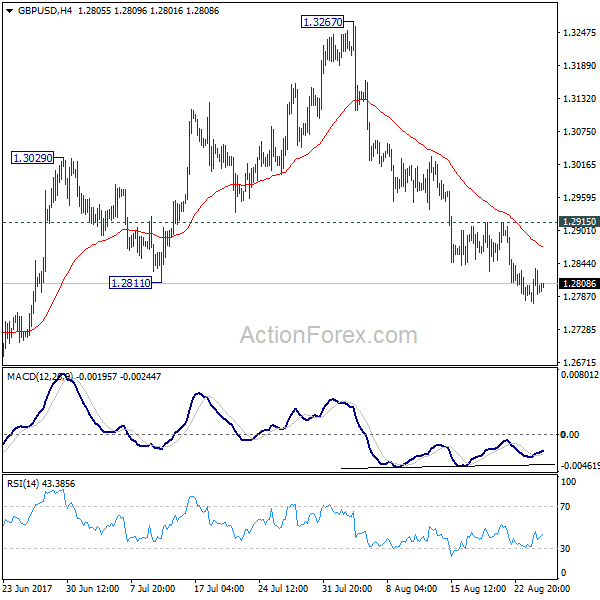

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2769; (P) 1.2803; (R1) 1.2832; More...

With 1.2915 minor resistance intact, deeper fall is expected in GBP/USD. Current fall from 1.3267 should be targeting to 1.2588 key near term support. As noted before, we're favoring the case that correction from 1.1946 is completed at 1.3267. Decisive break of 1.2588 will confirm our view and target a test on 1.1946 low. Though, break of 1.2915 will indicate short term bottoming and bring stronger rebound.

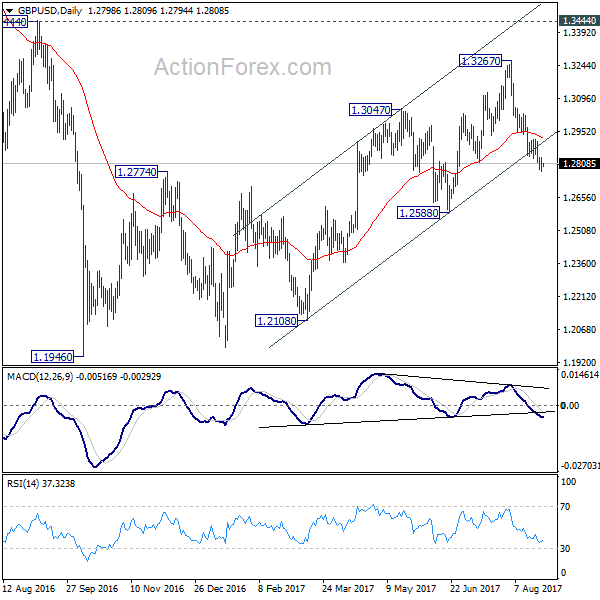

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9626; (P) 0.9647; (R1) 0.9674; More....

No change in USD/CHF's outlook as it's bounded in range of 0.9582/9772. Intraday bias remains neutral at this moment. On the upside, decisive break of 0.9772 resistance will revive the bullish case of reversal. That is, whole decline from 1.0342 has completed at 0.9437 after defending 0.9443 support. USD/CHF should then target channel resistance (now at 0.9849) next. Meanwhile, the pair is bounded inside medium term falling channel and limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783 for the moment. Break of 0.9582 will turn bias back to the downside for 0.9437. This could also extend the fall from 1.0342 through 0.9437/43 key support level.

In the bigger picture, we're slightly favoring the case that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996. However, firm break of 0.9443 will carry larger bearish implication and would target next key support at 0.9072.

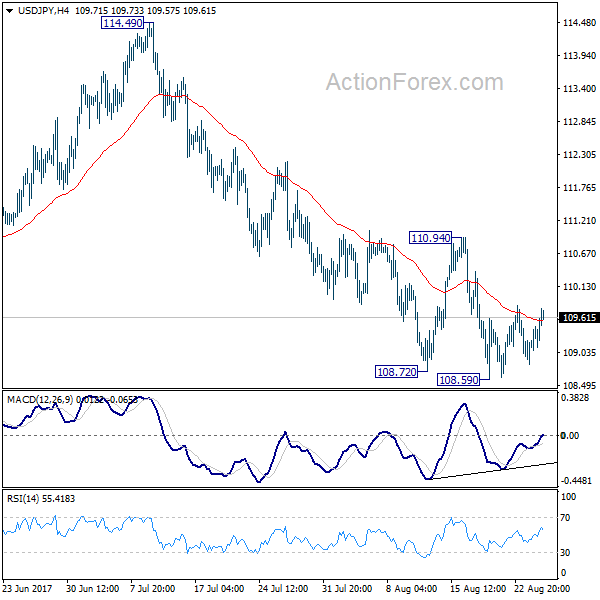

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.05; (P) 109.33; (R1) 109.81; More...

Intraday bias in USD/JPY remains neutral for consolidation above 108.59 temporary low. Near term outlook stays bearish with 110.94 resistance intact and deeper decline is expected. Break of 108.59 will target a test on 108.12 low. Whole corrective decline from 118.65 is possibly resuming and break of 108.12 will target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, firm break of 110.94 will indicate short term bottoming and turn bias back to the upside.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

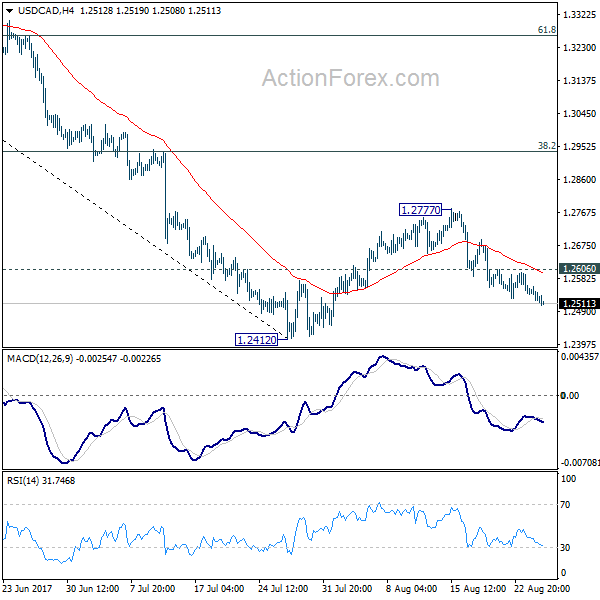

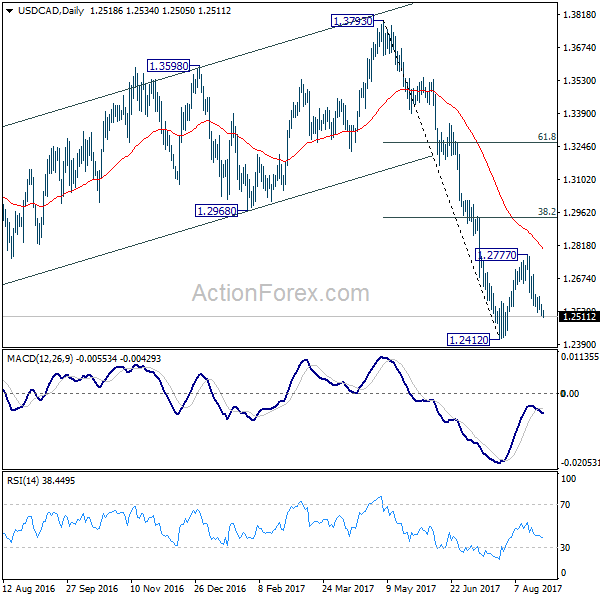

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2501; (P) 1.2531; (R1) 1.2549; More....

Intraday bias in USD/CAD remains mildly on the downside for retesting 1.2412 low first. Break there will resume the larger decline and target next long term fibonacci level at 1.2048. On the upside, above 1.2606 minor resistance will extend the correction from 1.2412 with another rise. But we'd expect upside to be limited by 38.2% retracement of 1.3793 to 1.2412 at 1.2940 to bring fall resumption eventually.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is still expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Nonetheless, on the upside, sustained break of 1.2968, 38.2% retracement of 1.3793 to 1.2412 at 1.2940 will be the first sign of completion of the correction and will turn focus back to 1.3793 key resistance.

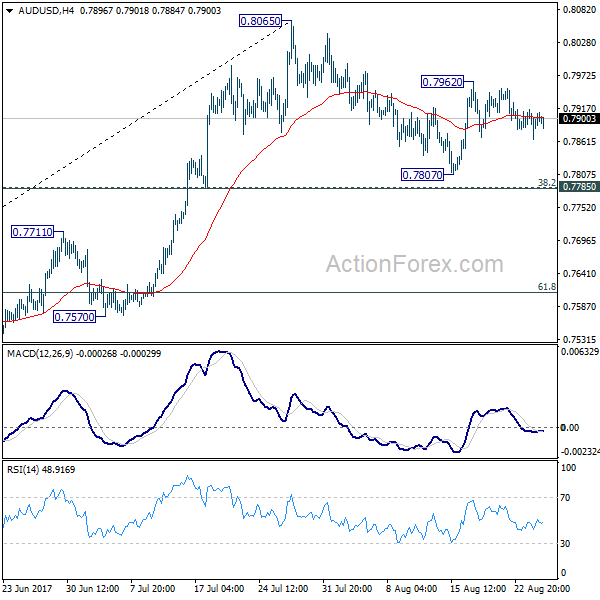

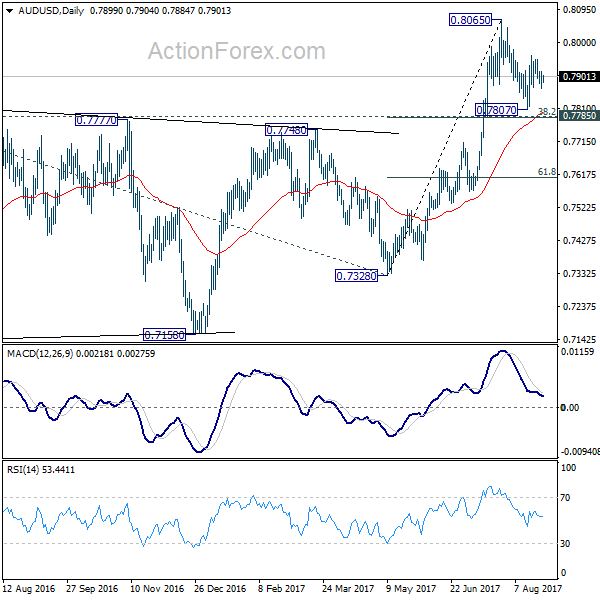

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7872; (P) 0.7894; (R1) 0.7922; More...

AUD/USD is staying in consolidation and intraday bias remains neutral for the moment. Correction from 0.8065 might extend and another fall cannot be ruled out. But downside should be contained by 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) to bring rebound. Above 0.7962 will target a test on 0.8065 resistance first. Firm break of 0.8065 will resume the medium term rise and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8097) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.

Markets Holding Their Breath as Fed Yellen and ECB Draghi Awaited

The financial markets are generally holding their breath as speeches of Fed Chair Janet Yellen and ECB President Mario Draghi at the Jackson Hole Symposiums are awaited. The occasion is seen in recent years as a platform to launch monetary policy shifts. But this time, neither Yellen nor Draghi is expected to deliver anything drastic regarding monetary policy in near term. At the same time, this could also be Yellen's last address at Jackson Hole since it's uncertain whether she will be granted another term by US President Donald Trump, after the current one expires in February. Yellen might make use of the speech on financial stability to lay down from ground work for the future and leave some legacy.

Fed George and Kaplan differ on rate

Esther George, President of Kansas City Fed which holds the symposium, sounded unbothered with the slowdown in inflation and maintained her push for another rate hike later this year. George told reporters that "while we haven't hit 2 percent, I'm reminded that 2 percent is a target over the long term, and in the context of a growing economy, of jobs being added, I don't think it's an issue that we should be particularly concerned about unless we see something change." And based on what she's seeing, "there's still opportunity" for another rate hike this year.

On the other hand, Dallas Fed President Rob Kaplan sounded more cautious. He noted that "I'm not saying we won't act by the end of the year, but we have the ability to be patient." And, according to Kaplan, the peak of interest rate at this tightening cycle is probably lower than the others. He said that "if you ask me today, I would say it's closer to 2 than to 3". Meanwhile, 10 years ago, he could have said in range of 4-5%.

Japan CPI improved but still way below target

Japan national CPI core ticked up to 0.5% yoy in July, up fro 0.4% yoy and met expectation. Tokyo CPI core rose to 0.4% mom in August, up from 0.2% yoy and beat expectation of 0.3% yoy. Corporate service price slowed to 0.6% yoy in July, down from 0.7% yoy and missed expectation of 0.8% yoy. The inflation reading is still nowhere near to BoJ's 2% target even though growth outlook improved. And the central bank just slashed its annual inflation forecast last month. BoJ expects that inflation won't hit target before 2020.

On the data front, German Q2 GDP final and Ifo business climate are the main features in European session. US will release durable goods orders.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7872; (P) 0.7894; (R1) 0.7922; More...

AUD/USD is staying in consolidation and intraday bias remains neutral for the moment. Correction from 0.8065 might extend and another fall cannot be ruled out. But downside should be contained by 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) to bring rebound. Above 0.7962 will target a test on 0.8065 resistance first. Firm break of 0.8065 will resume the medium term rise and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8097) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Jul | 0.50% | 0.50% | 0.40% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Aug | 0.40% | 0.30% | 0.20% | |

| 23:50 | JPY | Corporate Service Price Y/Y Jul | 0.60% | 0.80% | 0.80% | 0.70% |

| 6:00 | EUR | German GDP Q/Q Q2 F | 0.60% | 0.60% | ||

| 8:00 | EUR | German IFO - Business Climate Aug | 115.5 | 116 | ||

| 8:00 | EUR | German IFO - Expectations Aug | 106.8 | 107.3 | ||

| 8:00 | EUR | German IFO - Current Assessment Aug | 125 | 125.4 | ||

| 12:30 | USD | Durable Goods Orders Jul P | -5.80% | 6.40% | ||

| 12:30 | USD | Durables Ex Transportation Jul P | 0.40% | 0.10% | ||

| Jackson Hole Symposium |

Unpredictable Jackson Hole

Low expectations for the annual central banker gathering in Jackson Hole in the days ahead set the stage for a surprise. The Canadian dollar was the top performer on Thursday while the yen lagged. Japanese CPI data is due up next. The video for Premium members, focusing on the existing 5 trades and upcoming ideas is below.

Market moves were minimal on Thursday and EUR/USD was locked into a 35-pip range as the market braces for speeches from Yellen and Draghi at Jackson Hole. Other central bankers will be added to the agenda at the annual symposium.

Most of the commentary this week has been dismissive of the speeches from Yellen and Draghi. The topic of Yellen's 10 am ET Friday speech is financial stability, which is sometimes a code word for regulation. Lately, however, the Fed has started to debate whether it's worth raising rates to curb financial risk, even if inflation isn't forecast. If that's the thrust of Yellen's speech, and especially if she argues that it would be prudent to hike in order to curb some excesses in markets, then she could catch the market by surprise.

A week ago, the stakes for Draghi were higher because he was expected to announce, or at least hint, that an ECB taper was coming soon. That plan was scrapped because the ECB has grown increasingly concerned about euro strength, especially with supposed global coordinated tightening failing before it ever got started. However, in the past few months even the smallest hints of tightening have led to major market moves. He could avoi monetary policy, but at least mention the obvious --the growth upswing in the Eurozone.

If the euro sells off, the dip may be short-lived because many market participants are absolutely convinced that it's only a matter of time until the taper announcement comes. So even if Draghi manages to hold the euro down, it's like holding a ball underwater, it's only a matter of time until it pops. AshrafLaidi.com's last 7 trades in EURUSD have each attained a gain of 130-280 pips. The current trade is also in the green.

The yen is likely to be a passenger as it's whipped around by the risk trade on Friday. But before the meetings begin it will briefly have the spotlight with July CPI data due at 2350 GMT. The consensus is for a modest 0.4% y/y rise in the national CPI and just a 0.1% y/y rise in the CPI ex food and energy.

Sterling Hovers Near New Lows as Britain Makes First Step on Brexit Legislation and Growth Stagnates

Today marks a year how the UK Prime Minister gave a speech about Brexit in a Conservative conference and said that "We are not leaving only to return to the jurisdiction of the European Court of Justice - that's not going to happen". Yesterday, though, while May reiterated her view on Britain's own legal path, a Brexit paper on "enforcement and dispute resolution" submitted by the state's secretary David Davis expressed a different opinion. Following the report, which revealed that contradictions between May and her team remain, and today's disappointing evidence on migration, the pound touched new lows against its major counterparts.

The UK's legal positions were put on paper on Wednesday for the first time since the divorce vote in 2016. A few hours later after May reiterated that only the UK and not the ECJ would have the right to decide on the country's legal matters after Brexit. In contrast to May's remarks, the paper which was characterized as "constructive" stated several ways in which the ECJ's permissions would be needed even after the "direct jurisdiction" transitory period (probably three years after divorce) would end. Papers were also published on security and citizen's rights, as well as on a future customs agreement, which is the most important to businesses. The UK government is proposing a "freest and most frictionless possible trade in goods between the UK and the EU". The paper admitted that if the UK refuses to accept EU legal judgment, it will face difficulties to reach a trade agreement with the block. Although the paper did not mention which trade model the UK is heading towards, countries such as Iceland, Liechtenstein, and Norway which operate under ECJ's independent European Free Trade Association court (EFTA), follow ECJ's rules on the single market. The justice minister, Dominic Raab, also argued that the country has to keep "half an eye" on EU legislations as future trade disputes could emerge.

Meanwhile, second estimates of GDP growth figures for the second quarter, published during early European trading hours, showed that the UK economic environment remains fragile. Despite GDP growth rate remaining unrevised at 0.3% q/q and at 1.7% y/y, consumer spending and business investments did not contribute to the country's economic expansion. Household spending rose by 0.1% y/y, the weakest rate posted since 2014, while business spending recorded a 0% growth. Exports and imports increased by 0.7%, while government spending improved by the same amount.

Another report out of the UK showed that net migration has dropped to the lowest level in three years. The Migration Minister, Brandon Lewis, considered this fall as "encouraging", though the head of employment at the CBI, Mathew Percival, claimed that the increasing number of EU departures might lead to skill shortages in the labor market. Based on the statistics, more than half of the fall in net migration was attributed to a decrease of 51,000 EU citizens, the lowest reduction since December 2013.

With political risks heightening and Brexit talks weighing significantly on domestic economic performance, the odds for a rate hike anytime soon are diminishing.

Looking at the reaction in the forex markets, the pound reached a 2-month low of $1.2777 yesterday, while on Thursday cable was trading higher at 1.2810. Euro/pound jumped to a 10 ½ -month high at 0.9235 on Wednesday and pulled back to 0.9207 today. Pound/yen dropped to more than 2-month low of 139.29. Against a trade-weighted basket of currencies, the pound index tumbled to 74.60, its lowest level since November 2016.

Dollar Firmer as Risk Appetite Improves ahead of Jackson Hole; Pound Perks Up on Euro Weakness

Risk appetite improved notably on Wednesday as investors shrugged off the threat of a government shutdown in the United States to focus on the three-day Jackson Hole gathering of central bankers in Wyoming, which starts today. The US dollar extended its Asian session gains to climb towards 109.50 yen, but the euro floundered ahead of an extended speech by ECB head Mario Draghi tomorrow in Jackson Hole.

GDP data dominated the early European session as growth figures were released in Norway and the United Kingdom. British growth was unrevised at 0.3% quarter-on-quarter for the second quarter as expected, but the component breakdowns painted a bleak picture for the UK economy. Business investment was flat in the three months to June, missing forecasts of a 0.4% quarterly gain, while household spending rose by a meagre 0.1%. Other UK data included the CBI's retail sales survey, with the balance of reported sales falling unexpectedly to -10 from +22. Forecasts were for a reading of +15.

The pound initially spiked down after the data, only to quickly resume its uptrend that began in late Asian trading on euro/pound selling. Sterling touched a session-high of $1.2836 before settling around $1.2810 in late European session. The euro slipped against the pound as traders took profit from the pair's sharp gains yesterday. Euro/pound hit a low of 0.9189 from yesterday's 10-month lows before attempting to reclaim the 0.92 level. The single currency also lost ground versus the dollar, easing to around the $1.18 handle.

The Norwegian krone firmed against both the dollar and the euro after growth in Norway jumped to 1.1% q/q in the second quarter. This is up sharply from the growth of just 0.2% in the prior quarter. The dollar was down by about 0.3% at 7.84 kr, with the euro falling a similar amount to 9.25 kr.

The greenback made a steady advance to 109.45 yen but the uptrend lost some of its shine after the release of worse-than-expected housing data. Existing home sales fell by 1.3% in July to an annual figure of 5.44 million. This compares with expectations of 5.57 million and a downwardly revised 5.51 million in June. The dollar slid to around 109.20 after the data, erasing some of the gains from stronger-than-expected weekly jobless claims. Initial claims for unemployment benefits rose by 2k to 234k last week, though this was better than forecasts of an increase to 238k.

The Australian and New Zealand dollars both bounced off support levels to recoup some of their earlier losses. The aussie was flat on the day at around the $0.79 level, while the kiwi fell marginally to $0.7216. The antipodean currencies have been dogged by political concerns in recent days with elections looming in New Zealand in what is turning out to be a tight race, and controversy surrounding senior Australian politicians over dual citizenship.

In commodities, gold was weaker on the back of risk-on and a stronger dollar. The precious metal was slightly lower at $1287 an ounce. Crude oil was also down, despite yesterday's dip in US inventories and the threat of a hurricane hitting Texas, which could cause disruption to supply. WTI oil was 1.3% weaker at $47.79 a barrel and Brent crude was down by a lesser 0.8% at $52.16.