Sample Category Title

Capitol Hill Update: Fall Legislative Preview

Executive Summary

Congress returns from its August recess Tuesday, September 5 with a long to-do list of legislative deadlines, including lifting the debt ceiling, funding the government beyond the end of September, reauthorizing a number of federal programs and passing a budget resolution to serve as the vehicle for changes to tax law. For the House of Representatives, there are just 12 scheduled legislative days in September to accomplish the to-do list. In this slightly longer edition of the Capitol Hill Update, we outline the legislative calendar and provide our views on how we believe federal fiscal policy will unfold in the month ahead.

Our expectation is that the debt ceiling will be lifted before the projected September 29 deadline. Given the need for a bipartisan vote in the Senate to lift the borrowing limit, we expect the debt ceiling will be suspended for a period of time without being tied to budget cuts or other policy changes. The federal funding bill will also require bipartisan support and thus we expect Congress will enact a continuing resolution that maintains this fiscal year's funding levels through the beginning/middle of December, buying policymakers more time to work toward a solution for the remainder of the fiscal year. While tax reform discussions will be ongoing, we do not expect any major developments until late October or early November due to the numerous other pressing legislative priorities and the need to first pass a budget resolution.

Debt Ceiling: Will There Be Strings Attached?

One of the biggest concerns among market participants is the need to lift the nation's borrowing limit. Back in 2011, a down-to-the-wire vote resulted in volatile financial markets and a credit rating downgrade of U.S. sovereign debt. During this round of the debt ceiling debate, there have been demands by some fiscally conservative members of the House of Representatives to cut nondefense spending in exchange for lifting the debt ceiling. Other members of Congress have balked at this approach, preferring to pass a "clean" debt ceiling bill that does not tie the borrowing limit to other legislative items.

Given the fact that at least eight Democrats will need to join with Republicans in the Senate to advance the bill, it will require a bipartisan effort to raise the debt ceiling. A key question surrounding the debt ceiling debate is whether Democrats will demand concessions from Republicans to gain their votes. If fiscally conservative members begin to abandon ship in droves and Republican leadership must lean heavily on Democratic votes to pass a debt ceiling increase, it may empower the minority party to try to extract a hefty price from the party in power. If this was to occur, it would put Republican leadership in an awkward place; short of the necessary votes, and stuck between two sides both demanding concessions for their critical block of votes. The probability of a major market moving event in this case would likely increase, and we will be watching closely in the weeks ahead for signs that events are unfolding along this path.

Our view is that a "clean" debt ceiling bill with no other policy changes or budget cuts attached will be passed. There are just 12 legislative days scheduled in the House of Representatives before the September 29 deadline, suggesting that both the House and Senate must move quickly toward passage, limiting the ability to have a long, drawn out debate over other policy changes.1 This "clean" debt ceiling bill is likely to suspend the borrowing limit as has been done frequently in the recent past as opposed to increasing the borrowing limit to a specific dollar amount.

Federal Funding: Expect the Can to Be Kicked

The next major issue to tackle is funding the federal government beyond September 30. Should Congress fail to pass a funding bill, the result would be a partial federal government shutdown. In the case of a partial shutdown, the President's Office of Management and Budget would develop a plan to determine which federal employees would be affected through furlough. The most likely outcome given the very short timeline entails passing a continuing resolution (CR) that funds the government through the first or second week in December. Once again, the CR will require at least eight Democrats to join with Republicans to keep the government functioning. This CR will likely carry over funding from the current 2017 fiscal year to keep the bill bipartisan and hopefully noncontroversial. We believe policymakers will likely turn to a shortterm patch because the regular appropriations process has been delayed as policymakers have grappled with other legislative items and difficult questions remained unresolved. Thus far, Republicans have pursued an aggressive expansion of defense spending while keeping nondefense spending more or less flat. Budget agreements over the past few years have often led a more bipartisan approach that provides bumps in funding to both defense and nondefense discretionary spending. If Democrats refuse to play ball in the Senate on a budget that abandons this balanced framework, or if a fight erupts over controversial budget items such as funding for a border wall, the appropriations process would likely continue to face major roadblocks throughout the fall.

Kicking the can to December will buy more time for a longer-term funding bill to be worked out in the remaining months of the year and allow Congress to turn to the other legislative deadlines it is facing in September, including the need to reauthorize the Federal Aviation Administration, the National Flood Insurance Program and the Children's Health Insurance Program. Historically, reauthorizing these programs has at times been controversial and time consuming, requiring several weeks of debate to find solutions. This time around, we would not be surprised if these programs' authorizations are also extended for a short period to buy time for continued negotiations and more comprehensive legislation.

What about Tax Reform?

Given the multiple legislative deadlines facing Congress in September, as well as the fact that Republicans still need to pass a budget resolution before moving on to tax reform, we do not expect much progress on tax legislation until October or November. As we have described in previous pieces, the FY 2018 budget resolution is needed to proceed with the reconciliation process that will allow tax legislation to clear both chambers with a simple majority vote.2 Early signs are that the debate over a budget resolution could take some time. Fiscal conservatives in the House want more nondefense budget cuts, while more moderate members have resisted sharp cuts to nondefense discretionary and/or mandatory spending. Disagreements over balancing the budget/deficit size over the next decade have also plagued the budget resolution. For now, despite the optimistic rhetoric coming from Washington D.C. on taxes, we expect tax legislation will take a backseat in September to other more pressing federal fiscal policy items, such as the debt ceiling and government funding.

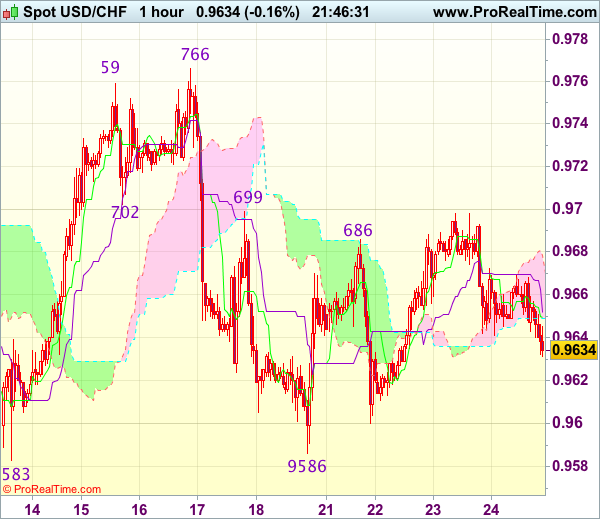

Trade Idea Update: USD/CHF – Hold long entered at 0.9620

USD/CHF - 0.962

Original strategy :

Bought at 0.9620, Target: 0.9720, Stop: 0.9585

Position : - Long at 0.9620

Target : - 0.9720

Stop : - 0.9585

New strategy :

Hold long entered at 0.9620, Target: 0.9720, Stop: 0.9585

Position : - Long at 0.9620

Target : - 0.9720

Stop : - 0.9585

Dollar’s retreat after faltering below resistance at 0.9699 suggests initial downside risk remains for marginal weakness, however, as long as support at 0.9586 holds, prospect of another rebound remains, above indicated resistance at 0.9699 would signal the retreat from 0.9766 has ended at 0.9586 last week and mild upside bias is seen for gain to 0.9720, then 0.9740, having said that, reckon resistance at 0.9766-73 would cap upside and bring further consolidation. Only a break of 0.9773 would retain bullishness and signal early rise from 0.9438 has resumed and extend gain to 0.9800.

In view of this, we are holding on to our long position entered at 0.9620. Below 0.9600 would risk test of strong support at 0.9583-86 but only break there would signal a downside break of recent broad range has occurred, bring subsequent fall to 0.9550.

As Dollar Reaches Bottom of Range Again, Investors Await Direction from Fed and White House

Despite a series of significant uptrends and downtrends since March, the US dollar has largely been bound within a trading range of between 115 and 108 against the Japanese yen for much of the year.

Growing doubts about the Fed's ambitious projections of one more rate increases in 2017 and three hikes in 2018 have weighed on the yield of 10-year Treasury notes, which peaked at 2.629% in March and currently stand around 2.185%. However, another factor in putting an end to the dollar's post-election rally has been the never-ending saga of political upheaval in the White House and in turn, fading hopes of a fiscal stimulus anytime soon. Ongoing troubles in the White House have been capping any advances the dollar has been able to muster from positive economic data.

The dollar's decline has been even steeper against other currencies, particularly against the euro, which is up 12% in the year-to-date. Even the Brexit-battered pound has gained versus the dollar so far this year. Against the safe-haven yen, the greenback is currently down by almost 7% since the start of 2017 as it hovers near the bottom of its range that's been in place since mid-January. It's worth noting though that when the dollar is trading near the top of its present range, those losses are limited to just under 2%.

The troubles in the Trump administration started on January 30 soon after the President took office and he fired the acting Attorney General, Sally Yates, after she refused to defend Trump's ban on immigrants from several Muslim-majority countries. They escalated on February 13 when Michael Flynn, the national security advisor was forced to resign over revelations of potentially illegal contacts with the Russian ambassador to the US. The next major departure came on May 9 when Trump fired the FBI director, James Comey. This was followed by the exit of Trump's first communication director on May 30. But the scale of the turmoil in the West Wing only became apparent in July when Tump's second communications director, Anthony Scaramucci, his press secretary, Sean Spicer, and chief of staff, Reince Priebus, all departed within days of each other.

There was some positive news for the markets in August when the President's chief strategist, Stephen Bannon, a known economic nationalist, was fired by Trump on the advice of his new chief of staff, John Kelly. Bannon was widely credited for driving much of Trump's anti-immigration and anti-trade policies and his departure gave some hope to market participants that Trump would tone down his rhetoric on trade and immigration. It's also a sign that the newly appointed chief of staff and retired general John Kelly is able to get a tighter grip on the White House, bringing discipline to the disorder.

While the series of resignations and sackings in July exasperated the dollar's decline from its July peak of 114.49 yen, the downtrend was triggered by an apparent shift in the Fed's stance to a less hawkish one. Federal Reserve Chair Janet Yellen voiced some concern about the softening in US inflation at her semi-annual testimony before Congress on July 12. Interestingly, the March downtrend was also sparked by the Fed, following the not-as-hawkish-as-expected FOMC projections from the March policy meeting, while the May downtrend came about from disappointing economic indicators.

This suggests Fed policy remains the main driver for the greenback despite the growing volatility and uncertainty being generated by White House developments. The next big move by the Fed is expected to come at the September policy meeting where they will likely initiate their well-telegraphed balance sheet reduction plan. Concerns about a possible government shutdown are unlikely to derail the Fed's plans unless it was to lead to a market panic.

President Trump this week threatened to shut down the government if Congress did not provide funding for his election pledge to build a wall across the Mexican border, adding to the unease in the markets. However, the dollar remains off its four-month low of 108.60 touched last week and could be on the verge of a new uptrend if it bounces off its support level of the bottom of the range, as it has done after the previous downtrends reached this area.

As sentiment for the dollar turns increasingly negative, with a bearish crossover of the 50- and 200-day moving averages in July underlining this view, it might not take much to trigger an upside correction. However, the odds for a breach of the range bottom is as likely, if not greater, given the downside risks. As dollar/yen wavers near this support level, direction could come either way from the Fed and Washington.

While Trump's record in the White House leaves much to be desired, progress on the tax front is not inconceivable as the reforms have broad-based support within the Republican party. Traders are unlikely to push the dollar substantially higher however, unless there was evidence that the tax reform plans were moving significantly forward as there's always going to be the risk of the President creating unnecessary distraction and antagonising his own party. Trump's response to the recent events in Charlottesville, Virginia may have lost him some key support from not just the Republicans but also from the business community.

Meanwhile, as the Fed appears to be taking a more cautious approach to inflation, markets may be underestimating the likelihood of another rate hike this year. Although various measures of inflation have weakened over the past few months, the labour market continues to tighten and consumer spending has rebounded from a soft patch earlier in the year. More importantly for the Fed, market volatility is at a record low, the dollar has depreciated substantially this year and financial conditions remain loose. Therefore, it could only require a minor reassuring uptick in price pressures to prompt Fed policymakers to resume their rate hiking cycle.

Alternatively, signs of further delays in Trump's economic agenda would only increase the bearish bets already placed against the dollar. A deepening turmoil in the White House as well as a possible escalation of tensions with North Korea could overshadow strong economic data. However, an increasing number of analysts are taking the view that low inflation is here to say and are not forecasting interest rates to peak much higher from their current levels. The next FOMC projections due on September 20 will be especially interesting to watch for any change in committee members outlook on inflation, as well as the updated dot plot chart.

Ceilings and Budgets and Shutdowns. Oh My!

Highlights

- Congress has two critical to-dos in September: raise the debt ceiling and pass a resolution to fund the government beyond Sept. 30th. In recent years, these issues often are not settled until the 11th hour, resulting in market volatility.

- With Republicans dominating Washington, agreements on both items should seemingly be reached more easily. However, the need for Democratic cooperation in the Senate raises the probability of a government shutdown in particular. A brief government shutdown would dent, but not derail, economic growth in the fourth quarter.

- The risk is a standoff could damage market confidence in Washington Republicans enacting pro-growth policies they expect. We had a sneak preview of the volatility that could result from this last week. While not our base case, a worst case scenario of a bad standoff and severe market turmoil could lead to the Fed delaying the start of normalizing its balance sheet in September.

When Congress resumes sitting on September 5th it has two pressing matters to address: the debt ceiling and funding the government beyond the end of September. In theory, the stakes are high on both fronts. If the debt ceiling is not raised or suspended, the government can no longer borrow to fund its deficit. This would be equivalent to an individual who has maxed out their credit cards, used all the cash hidden in cookie jars, and whose next paycheck isn't going to cover their expenses – something has to give. This raises the risk the government would either default on its debt payments, or leave other bills unpaid. And, if legislation is not passed to fund government programs beyond September 30th, many government functions and services would shut down, as we saw most recently in 2013.

Both of these items have proved contentious in the past, as various factions in Congress use them as leverage to achieve other policy priorities. With Republicans (GOP) controlling the Senate, the House and the White House, it would seem that a standoff is less likely this time around. Financial markets' are currently making the same bet. On a trend basis, volatility (as measured by the VIX) had been hovering near all-time lows, or reacting to geopolitical events such as North Korea and rumors about turmoil in the White House's economic leadership (Chart 1). Last week's experience shows how sensitive markets are to perceived turmoil in Washington. Markets currently assume the lion waiting for them in September is cowardly, just like in Oz. But, they will likely be spooked if it turns out to be the Wicked Witch.

However, the diversity of views within the GOP, and a narrow majority in the Senate doesn't eliminate the risk of a standoff. If a game of fiscal chicken erupts on either front, as we have seen in the past, market sentiment is likely to sour quickly.

The Debt Ceiling – the more you ignore me, the closer I get

For starters, the debt limit or "ceiling" caps the government's authority to borrow money (issue Treasury securities) to pay for spending already authorized by Congress. The U.S. government hit this ceiling back in mid-March, and the Treasury has since been using "extraordinary" measures to fund the government. The Treasury estimates the money in cookie jar and under mattresses will run out by September 29th, and has formally requested Congress to raise or suspend the debt ceiling, which it did not do before going on its August recess.

So far, the GOP leadership has not conveyed an interest in engaging in a public, confidence-damaging fight on the decision to raise or suspend the debt ceiling. GOP leadership, including Freedom Caucus leader Mark Meadows, recently reassured markets that they will raise or suspend the debt ceiling with no strings attached. No doubt, the 2011 experience of a disastrous debt ceiling standoff remains fresh in the minds of Republicans. Historically, Congress routinely raised the debt ceiling without much fuss. But in 2011, Republicans, having recently taken control of the House, demanded the President negotiate over deficit reduction in exchange for an increase in the debt ceiling. Two days before Treasury's stated deadline, Republicans agreed to raise the ceiling in exchange for future spending cuts embodied in the Budget Control Act of 2011. In reaction to the standoff, S&P downgraded the sovereign credit rating of the U.S. government for the first time ever. This resulted in the worst financial market volatility since the financial crisis, with the S&P 500 dropping about 12% over the course of the 2011 debt ceiling debacle.

There's some comfort today that the 2011 experience was under a Democratic President, and this time around, members are likely more confident that government spending restraint is more achievable with a Republican President. But it's not totally free and clear, as legislation to raise the debt ceiling will need 60 votes to pass the Senate, and Democrats could choose to be obstructive in getting a bill passed in a timely manner. It is unclear at this time what the Congressional leadership's strategy will be.

If an agreement does prove difficult when Congress returns in September, financial market reaction is likely to be more muted than the 2011 experience. At that time, S&P already had the U.S. rating on a negative watch. That is not the case this time around. S&P recently reaffirmed (Aug. 2, 2017) the US AA+ rating as stable. With the U.S. government's fiscal situation markedly improved since then (Chart 2), a downgrade is not in the offing.

Absent the credit rating experience, more recent debt ceiling showdowns in 2013 and 2015 were less damaging to markets. In 2013, the S&P 500 dipped slightly as the clocked ticked down to the deadline, but rebounded quickly afterwards, and in 2015 equity markets rose steadily. These more muted responses may reflect the fact that they expect an 11th hour deal, as was the case in 2011. Moreover, markets have greater confidence that default is not really on the table. According to transcripts (made public in 2016) of a Conference call with then Fed Chair Ben Bernanke in 2011, the Federal Reserve and Treasury had developed procedures that would have insured principal and interest on Treasury securities would continue to be made on time. "Other" payments may be delayed. We don't know specifics, but these payments could include salaries, payments on contracts or even delay Social Security or Medicare payments.

Even if the debt ceiling isn't raised and the U.S. avoids a technical default, there would still be a price to pay for the standoff apart from losses on equity markets. Reduced market confidence in the U.S. government's ability to keep its fiscal house in order has a real cost. The U.S. Government Accountability Office estimated that delays in raising the debt ceiling in 2011 led to an increase in government borrowing costs of $1.3 billion in 2011. 2011 likely represents a worst-case scenario, but the short-term measures Secretary Mnuchin has had to take since the debt limit was reached in March have cost at least $2.5 billion, not including any increased borrowing costs. (Ultimately, this is a drop in the bucket for a $4 trillion budget.)

Government shutdown more likely, but less damaging

The second pressing issue facing the GOP relates to funding government services for the next fiscal year, which starts on October 1st. On this front, consensus is less clear. In the tangled web of U.S. budgeting process, the appropriations process for the 2018 fiscal year is underway without a Budget resolution. The House has passed four of 12 appropriation bills, but these would likely need Democratic support in the Senate. So funding decisions for FY2018 are far from assured, and Congressional leadership has not outlined their plan publically for September.

Congress must either pass a budget resolution or a continuing resolution stop gap to fund the government beyond September 30th. To pass tax reform through reconciliation, Congress ultimately needs to pass a budget resolution with reconciliation instructions. But, in the interim, a continuing resolution to fund government for a given period of time may be more achievable given the House is only sitting for 12 days in September. However, a continuing resolution could be filibustered in the Senate, and therefore would need Democratic support to pass. Add to this the fact that Trump had threatened a government shutdown in the fall earlier this year, and the risks that an agreement will not be reached cannot be ignored.

This is not uncharted territory. The U.S. government has gone through 18 government shutdowns in the modern budgeting era (since 1976), and the economic impact would be small provided the shutdown is not prolonged. The Bureau of Economic Analysis (BEA) estimated that the 16-day shutdown in 2013 lowered real GDP in Q4 2013 by 0.3 percentage points (annualized), but growth was still very strong in that quarter as a whole. If the shutdown were to drag on, for example, for four weeks, it is estimated it would lower real GDP growth by 1.5 percentage points (annualized) in the fourth quarter.

On average, government shutdowns have lasted seven days. However, the two most recent shutdowns were far longer. During the 2013 shutdown, about 40% of government workers were furloughed, equivalent to 850 000 people. However, one of the reasons that the impact isn't greater on economic activity is because essential roles remain in place, like air-traffic controllers, armed forces, and food safety inspectors. The Federal Reserve is not funded by Congress, so it too would remain open for business. But, tax refunds and economic data releases would be delayed, among other things, causing significant disruption in the lives of many Americans.

Worst case scenarios could stay the Fed's hand

Facing midterm elections next year the GOP likely wants to demonstrate their ability to govern, and a damaging game of fiscal chicken is not in their interest. That said, raising the debt ceiling and passing a continuing resolution to fund government beyond Sept. 30th will require cooperation with Democrats in the Senate. That is a wide ideological expanse to bridge with right-wing factions in the GOP. Therefore, a down-to-the wire debate on either matter cannot be ruled out. If market volatility spikes significantly, the Fed could delay normalizing its balance sheet, which is expected to be detailed at the September 20th meeting. Back in May, Fed Governor Brainard had flagged the debt limit as a possible pitfall for her outlook.

This scenario is not our base case, but financial markets have until recently been complacent about domestic risks. There is a tendency for agreements to not be reached until the 11th hour, and it would not take much in this environment to see volatility return in September. This was born out in last week's experience where mere rumors that moderate White House economic advisor Gary Cohn might resign, sent volatility back as nearly as high as it was during heightened worries about North Korea. As such, investors would do well to brace themselves for a potential twister of volatility in September.

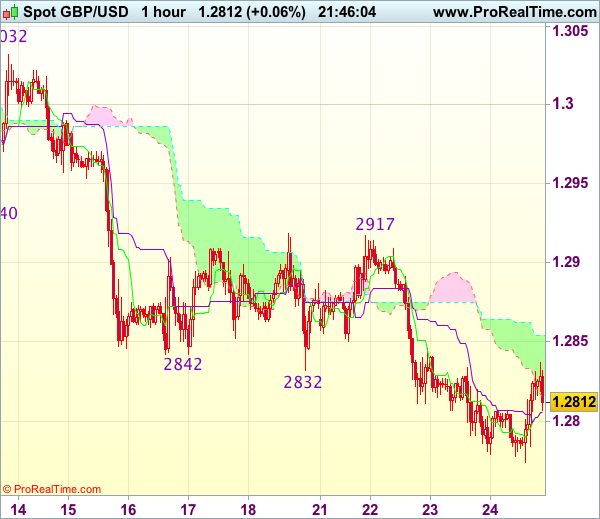

Trade Idea Update: GBP/USD – Buy at 1.2770

GBP/USD - 1.2815

Original strategy :

Buy at 1.2770, Target: 1.2870, Stop: 1.2735

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2770, Target: 1.2870, Stop: 1.2735

Position : -

Target : -

Stop : -

Although cable has remained under pressure and near term downside risk remains for recent selloff to extend one more fall, loss of downward momentum should prevent sharp fall below 1.2750-55, risk from there has increased for a rebound to take place soon, above 1.2845-50 would suggest a temporary low is possibly formed, bring a stronger rebound to 1.2870, break there would add credence to this view, then retracement of recent decline would commence for further gain to 1.2900.

In view of this, we are inclined to turn long on next decline. Below 1.2740-50 would risk weakness to 1.2720-25, however, still reckon downside would be limited to 1.2700-05 (100% projection of 1.3269-1.2940 measuring from 1.3032) and risk from there remains for another rebound to take place later.

Trade Idea Update: EUR/USD – Hold long entered at 1.1765

EUR/USD - 1.1801

Original strategy :

Bought at 1.1765, Target: 1.1865, Stop: 1.1770

Position : - Long at 1.1765

Target : - 1.1865

Stop : - 1.1770

New strategy :

Hold long entered at 1.1765, Target: 1.1865, Stop: 1.1770

Position : - Long at 1.1765

Target : - 1.1865

Stop : - 1.1770

As the single currency has retreated after faltering below resistance at 1.1828, suggesting minor consolidation would be seen, however, as long as 1.1765-70 holds, mild upside bias remains for another rebound, above said resistance at 1.1828 would extend the rise from 1.1662 low to resistance at 1.1847, break there would provide confirmation that the pullback from 1.1910 has ended and encourage for headway to 1.1870-80 but reckon said resistance at 1.1910 would hold from here.

In view of this, we are holding on to our long position entered at 1.1765. Only below 1.1740 support would abort and suggest the rebound from 1.1662 has ended instead, risk weakness to 1.1695-00 first.

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 109.30

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling initially to 108.84 earlier today, the subsequent rebound suggests decline is not ready to resume yet and further consolidation is in store, hence risk of another bounce to 109.55-60 is seen, however, reckon resistance at 109.83 (yesterday’s high) would hold and bring retreat later. Only a break of 109.83 would signal low has been formed at 108.60 earlier, bring further gain to 110.00 and later towards previous resistance at 110.37.

On the downside, below 109.00 would bring test of 108.84 but only break of said support at 108.60 would revive bearishness and confirm recent decline has resumed for further weakness to 108.30 (1.618 times projection of 110.95-109.67 measuring from 110.37), then towards 108.00. As near term outlook is still mixed, would be prudent to stand aside in the meantime.

Storm Threatens to Disrupt US Oil Supply

Oil prices edged higher on Wednesday, after the weekly US EIA inventory data showed yet another drawdown, signaling that the oil market continues to rebalance in a gradual manner. In addition, a tropical storm in the Gulf of Mexico, which is expected to strengthen into a hurricane tomorrow, probably boosted oil prices further as it threatens to disrupt production in the US. Considering that a large portion of US oil production is refined near the Gulf, if this storm does intensify, then we could see further gains in oil prices. That said though, even in case prices spike higher as a result of this weather phenomenon, we would expect any such supply-induced gains to remain relatively short-lived. Unless there is some notable damage to US oil-refining infrastructure, weather factors are unlikely to disrupt supply for long.

WTI traded higher on Wednesday after it found support at 47.50 (S1). Nevertheless, the advance was stopped by the 48.55 (R1) level and then the price retreated somewhat. Given that oil is still trading above the upper bound of the downside channel that contained the price action from the beginning of February until the 25th of July, we still see the possibility for another leg up. A break above 48.55 (R1) could confirm the case and may initially aim for our next resistance of 49.30 (R2).

Having said that though, we have to repeat that we don't expect any possible near-term gains to lead into a major healthy uptrend. We still believe that the range between 51.50 (R3) and 55.00 is the area where US shale producers may be attracted to increase production, something that may put a lid on any possible future gains.

USDCHF: Loses Upside Steam With Further Downside Threats

USDCHF: With the pair continuing to hold on to its downside pressure despite its consolidation threats, more decline is envisaged. On the downside, support lies at the 0.9600 level. A turn below here will open the door for more weakness towards the 0.9550 level and then the 0.9500 level. Its daily RSI is bearish and pointing lower suggesting further weakness. On the upside, resistance resides at the 0.9650 level where a break will clear the way for more strength to occur towards the 0.9700 level. Further out, resistance comes in at the 0.9750 level. All in all, USDCHF faces further downside pressure short term.

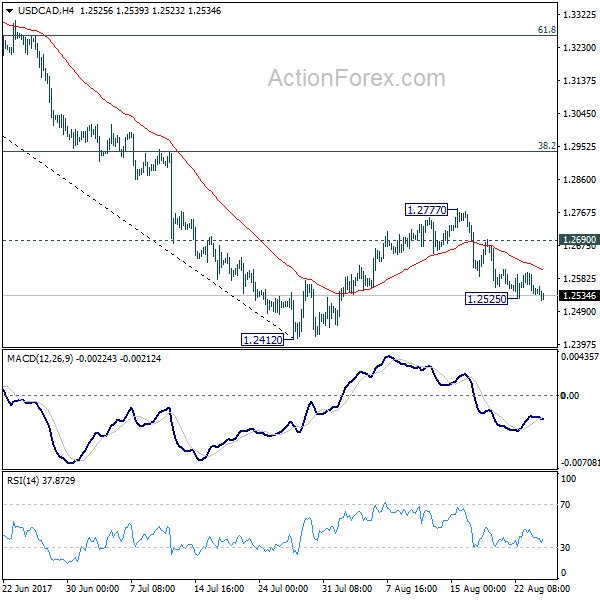

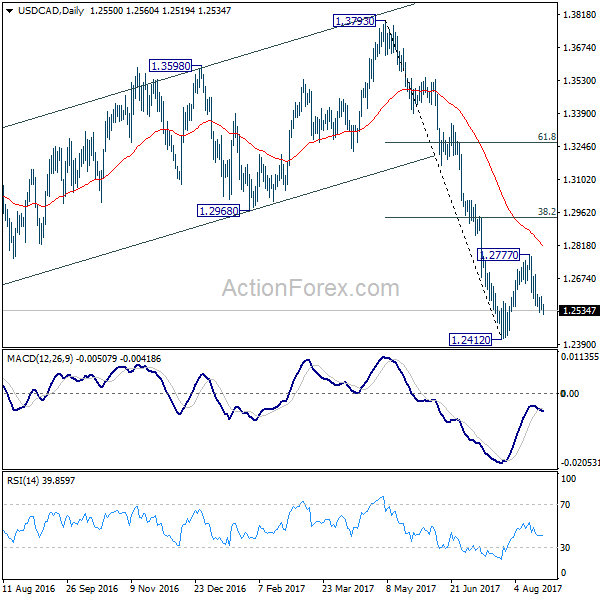

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2527; (P) 1.2562; (R1) 1.2585; More....

USD/CAD's fall from 1.2777 resumed after brief recovery. Intraday bias is back on the downside for retesting 1.2412 low. Break there will resume the larger decline and target next long term fibonacci level at 1.2048. On the upside, above 1.2690 will extend the correction from 1.2412 with another rise. But we'd expect upside to be limited by 38.2% retracement of 1.3793 to 1.2412 at 1.2940 to bring fall resumption eventually.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is still expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Nonetheless, on the upside, sustained break of 1.2968, 38.2% retracement of 1.3793 to 1.2412 at 1.2940 will be the first sign of completion of the correction and will turn focus back to 1.3793 key resistance.