Sample Category Title

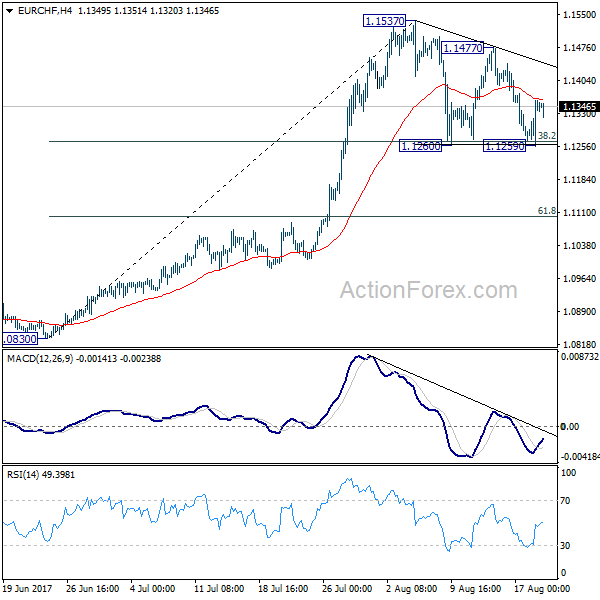

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1283; (P) 1.1321; (R1) 1.1385; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 1.1537 continues. On the upside, break of 1.1477 resistance will argue that the consolidation from 1.1537 has completed and larger rise is resuming. However, firm break of 38.2% retracement of 1.0830 to 1.1537 at 1.1267 will extend the correction to 61.8% retracement at 1.1100 before completion.

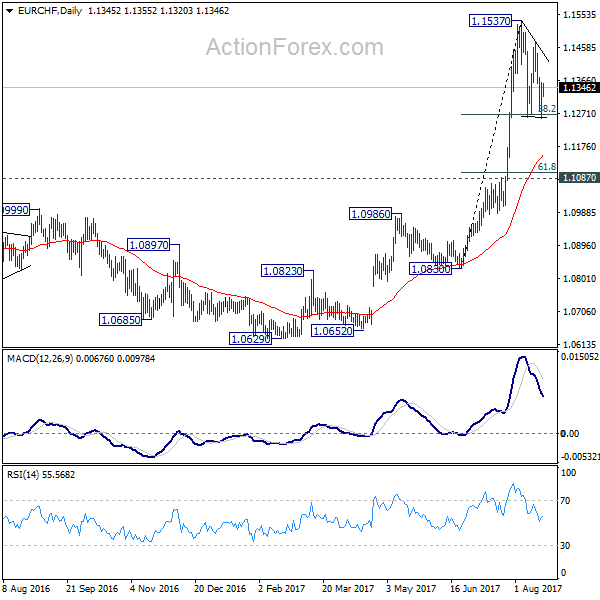

In the bigger picture, firm break of 1.1198 key resistance confirms resumption of the long term rise from SNB spike low back in 2015. In this case, EUR/CHF would eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

USD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Dark cloud cover

• Time of formation: 10 Jul 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Evening doji

• Time of formation: 7 Aug 2017

• Trend bias: Down

USD/JPY – 109.00

The greenback only bounced to 110.95 before dropping again (we recommended in our previous update to sell again at 111.00 and just missed the short entry), bearishness remains for weakness towards this year’s low at 108.13, however, break there is needed to confirm early decline from 118.66 top has indeed resumed and extend fall to 107.50, then towards 106.50-55 (61.8% Fibonacci retracement of 99.01-118.66), having said that, near term oversold condition should prevent sharp fall below there and reckon previous resistance at 105.53 would hold from here.

On the upside, whilst initial recovery to the Tenkan-Sen (now at 109.78) cannot be ruled out, reckon upside would be limited to the Kijun-Sen (now at 110.74) and 111.00 should attract renewed selling interest and bring another decline later. Above the lower Kumo (now at 111.66) would suggest the fall from 114.50 has ended instead, risk a stronger rebound to resistance at 112.20 but reckon upside would be limited to 112.40-45 and price should falter well below 113.00, bring another selloff later..

Recommendation : Sell again at 111.00 for 109.00 with stop above 112.00.

On the weekly chart, despite staging a strong rebound to 110.95, renewed selling interest emerged there and the pair has slipped again since (a doji with a long upper shadow was formed), bearishness remains for the fall from 114.50 to extend weakness towards previous support at 108.13 (2017 low), however, the pair needs to penetrate this level to confirm early fall from 118.66 top has resumed and extend decline to 117.40-50, then 117.00 but downside should be limited to 106.50-55 (61.8% Fibonacci retracement of 99.01-118.66) and previous resistance at 105.53 would turn into support, price should stay above 105.00, bring rebound later.

On the upside, although initial recovery to 109.75-80, then 110.50-60 cannot be ruled out, reckon resistance at 111.05 would limit upside and bring another decline later. Above the Tenkan-Sen (now at 111.55) would risk test of the Kijun-Sen (now at 111.82) but still reckon resistance at 112.20 would limit upside and bring another decline. A weekly close above resistance at 112.20 would suggest first leg of decline from 114.50 has ended instead, risk a stronger rebound to 112.90-00 but still reckon upside would be limited to 113.55-60 and price should falter well below resistance at 114.50, bring another decline later.

Politics And Central Bankers Under Investors’ Radar

Less than a month ago the CBOE volatility index – known as the best indicator of fear in the markets – dropped to a record low of below 9. The declines were a result of steady equity markets, low trading volumes and optimism that the markets were heading higher. This has all changed in the past two weeks, with the fear index rallying from a low of 9.52 to 17.28 – an 81% spike in 4 days from Aug 8 to Aug 11. This was precipitated by rising tensions between the U.S. and North Korea. These tensions lasted for a couple of days, then eased after both sides backed down. However, the calm didn't last long, as President Trump's response to the Charlottesville clash, saw business leaders exiting his advisory councils, and a number of high profile Republicans criticizing and distancing themselves from the President.

The departure of Trump's Chief Strategist Steve Bannon, who was mainly seen as pushing protectionist policies, was not unexpected and was slightly positive for markets, causing U.S. stocks to rally on Friday, but the market ended near lows.

Politics have clearly taken the front seat and another shock will likely lead to a further selloff in equities. Some investors might see the recent fall in prices as an opportunity to buy the dips, but given that valuations are still very high compared to historical averages, many will hold off until seeing meaningful fiscal policy change. Trump's administration will be tested as we get closer to hitting the U.S. debt ceiling. According to the Congressional Budget Office, the debt limit should be raised by mid-October, to avoid defaulting on loan payments, but this time it doesn't seem a done deal.

Given that the economic calendar doesn't hold tier-one data this week, investors and traders will be focusing on the Jackson Hole central bank gathering on 24-26 August. The two stars of the gathering will undoubtedly be Mario Draghi and Janet Yellen. The most recent minutes from the Fed and ECB, shows that inflationary pressures remained absent, despite declining unemployment rates. When looking at bond yields across the globe, investors seem to be convinced that inflation isn't returning anytime soon. However, financial asset prices are worrying central bankers, especially the Fed, which sees valuations as elevated.

With ECB's meeting scheduled on September 7, Euro traders are waiting for signs from President Draghi as to when the central bank will start trimming QE. The single currency managed to overlook ECB's minutes, which revealed that Euro strength is becoming a concern for monetary policy makers. If Draghi does not disclose his plan for tapering QE, the Euro might fall towards 1.16, but I would prefer to buy the dips then selling the rallies, as the ECB have no other choice but to tighten policy.

Technical Outlook: GBPUSD – Risk Of Bearish Continuation On Break Below Daily Cloud

Cable trades in red on Monday and holding within daily cloud, after attempts in past four days failed to close below cloud top.

Fresh weakness tested strong support at 1.2850, provided by daily cloud base and Fibo 61.8% of 1.2588/1.3268 rally.

Eventual break and close below here is needed to signal resumption of broader downtrend from 1.3268 (03 Aug high), after bears paused for last week's consolidation above rising daily cloud.

Negative outlook is supported by bearish setup of daily studies, with bear-cross of 10/55SMA's forming today and offering additional pressure.

Sustained break below 1.2850 would open another key support at 1.2811 (12 July trough) and risk fresh bearish extension.

Broken 100SMA (1.2872) marks initial resistance, ahead of daily cloud top (1.2908) and last week's congestion, reinforced by 55SMA at 1.2928, which is expected to limit extended upticks.

Res: 1.2872, 1.2908, 1.2928, 1.2970

Sup: 1.2850, 1.2811, 1.2749, 1.2700

Will Central Banks Ratchet Up Verbal Intervention?

Central banks around the globe have been increasingly vocal this year, with their trend of repeated verbal interventions sending foreign exchange markets on a wild roller-coaster ride.

The era of cheap money is coming to a timely end, with central banks now on a quest to raise rates at a pace that supports both growth and inflation. Markets will be closely watching the Jackson Hole Symposium on the 24th-26th August, which could provide a joint opportunity for financial heavyweights to signal policy shifts. Although there have been reports that European Central Bank President Draghi, will not deliver a new policy message at the conference, there is still a possibility that he will talk down the resurgent Euro. With July’s ECB meeting minutes revealing concerns over the strengthening Euro, complicating the European Central Bank’s efforts to hit the 2% inflation target, Draghi may verbally intervene at Jackson Hole to weaken the currency.

Other heavyweights such as Janet Yellen and Mark Carney, will also be on the scene with market players, closely scrutinizing any comments made regarding monetary policy. With concerns over stubbornly low inflation and political drama in Washington, weighing on the prospects of higher US interest rates, Yellen may avoid discussions on policy shifts altogether. The unsavory combination of Brexit uncertainty and soft economic fundamentals in the UK continues to weigh on the prospects of higher UK rates and this may be reflected in Mark Carney’s rhetoric at the pending Jackson Hole.

Will EURGBP hit parity?

There is growing speculation that the EURGBP is on a positive trajectory towards parity in the longer term and this is understandable when considering how the pair has appreciated over 800 pips from the 0.8300 support. The improving macro-fundamentals from Europe, continue to support the Euro, while Brexit uncertainty has pressured the Sterling. With the expectations of the ECB QE tapering - fueling the bullish sentiment towards the EURGBP, further upside is on the cards.

From a technical standpoint, the EURGBP is heavily bullish on the daily charts, as there have been consistently higher highs and higher lows. Bulls remain in control above the 0.9000 higher low, with a breakout above 0.9150 encouraging a further increase towards 0.9300. A monthly close above 0.9300 should open a path higher towards 0.9600.

USDJPY Intraday Analysis

USDJPY (109.26): The Japanese yen strengthened strongly against the U.S. dollar last week as price fell back to the support level at 109.15. This was the same support level that price managed to post a reversal earlier in the week. On the 4-hour chart, we can see that price action has managed to recover off the lows and closed above the support level of 109.08. A rebound off this support level could keep USDJPY biased to the upside. Resistance level at 110.72 will be in focus immediately, but above this level, USDJPY could pose a risk of an upside rally towards the next main resistance level at 113.00.

GBPUSD Intraday Analysis

GBPUSD (1.2876): The British pound was seen trading flat near the support level at 1.2847 for the past three days. This price level was previously tested in early July. The rebound off this level is therefore quite likely as GBPUSD could be seen reversing the losses from the past few weeks. Price action in GBPUSD suggests that there is a strong possibility for a rebound back to 1.3000 - 1.3033 level of resistance in the near term. This could also form the potential head and shoulders pattern as a result. A reversal needs to be confirmed at 1.3000 - 1.3033 level however. This would then set the tone for a bearish decline in GBPUSD that could be seen testing the lower support at 1.2628 support, marking the measured move from the head and shoulders pattern. A break out above the previous highs at 1.3200 could however invalidate this downside bias.

EURUSD Intraday Analysis

EURUSD (1.1753): The EURUSD has managed to hold up above the 1.1688 support level multiple times. However, any subsequent bounce off this support has kept EURUSD posting lower highs. This consolidation has led to a descending triangle pattern that is currently forming. With the support now critical, a downside breakout could send the euro sliding towards the support level at 1.1552. In the near term, we expect to see the common currency continue to trade sideways. There is also a risk of an upside breakout in prices. This could come on a price breakout from the falling trend line. To the upside, the euro will need to struggle to break past the previous resistance at 1.18820.

Markets Look To A Quiet Start Ahead Of Jackson Hole Symposium

The U.S. dollar was seen trading mixed by Friday's close as the currency pair failed to hold on to the gains across some of its peers. The U.S. dollar fell sharply against the Japanese yen, while against the euro and the British pound, the greenback was trading rather flat.

Economic data on Friday saw the inflation report from Canada. Coming in line with estimates, monthly inflation rate turned flat as expected following a 0.1% decline previously. The UoM consumer sentiment showed an increase to 97.6, beating estimates of 94.0 while inflation expectations from the UoM remained steady at 2.6%.

Looking ahead, the economic calendar today is light with no major events scheduled. Second tier data includes Canada's wholesale sales. With the Jackson Hole event due to start this Thursday, the markets are likely to take a breather ahead of the key event which will see speeches from ECB's Draghi.

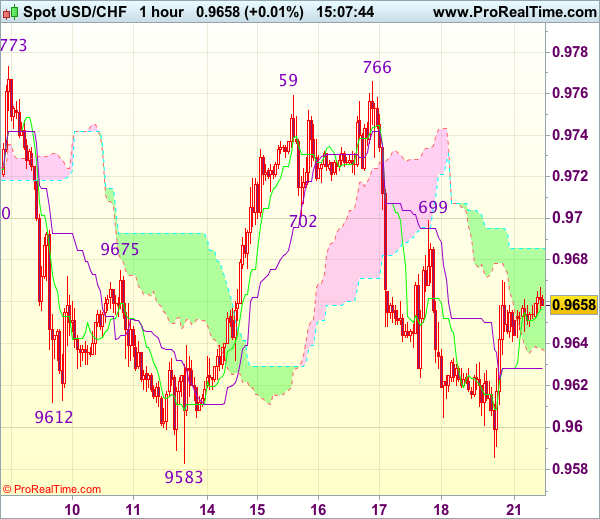

Trade Idea : USD/CHF – Stand aside

USD/CHF - 0.9654

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 0.9656

Kijun-Sen level : 0.9686

Ichimoku cloud top : 0.9637

Ichimoku cloud bottom : 0.9628

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the greenback has rebounded after holding above indicated previous support at 0.9583, retaining our view that further consolidation would take place and another bounce to 0.9699 resistance cannot be ruled out, however, reckon upside would be limited to 0.9730-35 and price should falter below resistance at 0.9766-73 resistance area, bring retreat later.

As near term outlook is still mixed, would be prudent to stand aside for now. Below the Kijun-Sen (now at 0.9628) would bring test of said support at 0.9583, however, break there is needed to revive bearishness and signal another leg of decline from 0.9773 is underway and extend subsequent fall to 0.9550, then 0.9515-20 which is likely to hold on first testing.