Sample Category Title

Brent Oil Extends The Sell-Off

Brent Oil drops like a rock and is very close to hit some important support levels. I’ve said in the previous analysis that the price may drop on the short term because was too overbought. Technically was expected to drop after the last false breakout above the 53.03 static resistance. Is attracted by the confluence between the sliding line (SL) with the minor uptrend line (dotted line). A breakdown through the mentioned support area will accelerate the sell-off. Will drop much deeper if will breakout from the minor ascending channel.

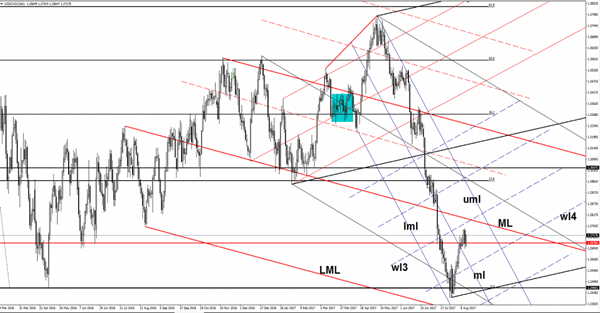

USD/CAD Edges Higher

Price climbs higher after the Friday’s massive drop. It is trading in the green again as the dollar index has managed to rebound and to recover after the minor decrease. Looks like that the behavior will change on the USDX on the daily chart, signaling that we may have a larger rebound. USDX has started to make higher lows on the bullish pressure, but maybe he’ll need a bullish spark from the US economy to be able to climb towards fresh new highs.

The greenback will dominate the currency market if the USDX will have enough energy to jump and stabilize above the 93.81 and more importantly above the 94.00 psychological level. We’ll have a rebound if will stay above the 92.55 previous low.

Looks like we had a false breakdown below the 1.2678 static support, a minor consolidation above it will confirm a further increase. As you already know, the rate could be attracted by the median line (ML) of the major descending pitchfork. The median line is acting as a magnet, is expected to approach and reach also the uper median line (uml) of the minor descending pitchfork after the failure to retest the median line (ml).

A major upside movement will appear only if it will take out the mentioned resistance levels, this scenario will happen if the USDX will jump above the 94.00 psychological level.

You have to be careful because a failure to reach and retest the mentioned resistance levels will send the rate down quickly.

Fed Dudley: A Precursor To Jackson Hole?

Fed Dudley: A precursor to Jackson Hole?

The markets continue to recover from last week’s disorder as US equities orchestrated a splendid showing recouping some of the sharp losses from last Friday as investor confidence returns with the de escalation of North Korea tension.

Dollar Yen bulls are smiling this morning in the wake of Fed Bill Dudley interview with the Associated Press where he was unabashedly hawkish. In what may be a precursor to Jackson Hole, the powerful New York Federal Reserve President believes the Fed’s balance-sheet reduction plan will begin in September and he is still confident of another rate hike this year. But realistically given how slight the markets 2017 rate hike expectations are, how much more bearishness could the FX markets price into the equation?

Oil markets leaked 2 % overnight on the back of weak China data and a stronger greenback. Commodity markets have been on edge since last week’s softer mainland trade data, so the sharp fall in CNY Industrial output will continue to weigh negatively on commodity markets as this is a clear sign that growth momentum in the world’s second largest economy is slowing.

Australian Dollar

The stronger USD and weaker China data have set the sagging tone for the Aussie dollar overnight ahead of today Monetary Policy Meeting Minutes. The weaker China data prints indicate the People’s Bank of China (PBOC ) cooling measures have the impact that economists predicted since the PBOC moved to deleverage.With commodity risk sentiment teetering, selling into commodity currency rallies will remain in vogue, and with base metals falling under renewed pressure, the Aussie will be the preferred short on this view.

Also weighing on regional sentiment President Donald Trump has set the wheels in motion for a US trade investigation of China’s intellectual property policies and, potentially, new tariffs on Chinese imports.

RBA Meeting Minutes revealed little change in the RBA’s view but the Aussie dollar is finding some support in morning trade on the back of improving risk sentiment.

Japanese Yen

A report published this morning stating that North Korea is backing off military escalation is adding more momentum to the haven trade unwind that began yesterday and coupled with some timely Fed speak, USDJPY moved through 110 with little opposition. External factors will continue to drive sentiment, with a more confident sounding Fed and risk sentiment rebounding, it would suggest there is room for USDJPY to extend the current rally over the days ahead. However, keep August 21-31 circled as South Korea & the US’s joint annual military exercise begins. With satellite photos suggested that North Korea seems to be preparing a new submarine launched ballistic missile, I suspect the markets will get testy again.

Euro

The market continues to re-engage the long EUR trade, this market darling is not about to give way anytime soon. It’s going to action not Fed rhetoric to shift the buy on dip sentiment

Elliott Wave Trade Ideas Performance Update

4 positions were entered last week with total profit of 240 points and the positions are listed below.

1 Aug : AUD/USD - Short at 0.8030, exited at 0.7880 (+ 150 points)

8 Aug : EUR/GBP - Short at 0.9080, exited at 0.9080 ( 0 point )

10 Aug: EUR/JPY - Short at 129.50, exited at 128.60 (+ 90 points)

14 Aug: GBP/JPY - Short at 142.50, exited at

| AUD EUR/JPY EUR/GBP CAD GBP GBPJPY

Jan - 15 -275 - 35 -120

Feb + 140 -17 - 40 +11

Mar - 20 +115 +132 - 19

Apr + 30 - 40 +120 + 45

May - 55 +100 - 6 -65 -60

Jun + 81 +150 - 10 +185 -120 +205

Jul - 40 - 60

Aug +150 + 60 + 100 +15 - 20

Sep

Oct

Nov

Dec

Y-T-D + 366 - 22 +167 +463 -170 +110

Gold Dips as North Korean Tensions Ease

Gold has posted losses to start off the week. In North American trade, spot gold is trading at $1283.99, down 0.43% on the day. On the release front, there are no US events on the schedule. On Tuesday, the US releases retail sales and core retail sales, key gauges of consumer spending.

The US economy remains strong, and although consumer confidence levels are high, this hasn't translated into higher consumer spending, a key driver of economic growth. After declines in retail sales in June, the markets are expecting gains in July, and strong readings could lift the US dollar and send gold prices lower. Investors are also keeping an eye on the Federal Reserve, which has said that it will begin trimming its bloated balance sheet of $4.2 trillion, most likely in September. This could weigh on gold prices, as a cut of $60 billion in the balance sheet is equivalent to a rate hike of 25 basis points.

Gold prices have dipped on Monday, as the crisis between North Korea and the US has eased. Last week, tensions soared between the two enemies, sending gold about 2.4%, as investors dumped shares and snapped up the safe-haven metal. Tensions between North Korea and the US remain high, but the prevalent sentiment in the markets is that a diplomatic solution will be found to end the crisis. Still, Donald Trump and Kim Jon-un are unpredictable leaders, and any move by either side could easily ratchet up tensions and unnerve investors. Donald Trump continues to deal with domestic problems as well, and the White House faced stinging criticism from both Republicans and Democrats, as Trump failed to single out white supremacists for the violence in Charlottseville, Virginia, where one person was killed at a demonstration against far-right marchers.

Candlesticks and Ichimoku Trade Ideas Performance Update

5 positions were entered among all 4 currency pairs with total profit of 55 points and the positions are listed below:

8 Aug : USD/JPY - Long at 110.30, exited at 110.25 (- 5 points)

9 Aug : EUR/USD - Short at 1.1770, exited at 1.1770 ( 0 point)

9 Aug : GBP/USD - Long at 1.3000, exited at 1.2965 (- 35 points)

11 Aug : USD/CHF - Long at 0.9610, exited at 0.9705 (+ 95 points)

11 Aug : EUR/USD - Long at 1.1790,

| JPY EUR CHF GBP

Jan + 167 - 85 - 10 + 50

Feb + 200 +150 +93 - 59

Mar -23 -70 -23 - 35

Apr + 65 + 93 + 50 - 40

May - 65 - 35 + 100 -175

Jun -100 -10 - 10 +175

Jul + 85 - 35 - 8

Aug + 75 + 65 + 95 -35

Sep

Oct

Nov

Dec

Y-T-D + 403 +68 +287 -109

Pound Edges Lower, Markets Eye British CPI

The British pound has started the week quietly. In the North American session, the pair is trading at 1.2984, down 0.20% on the day. On the release front, there are no British or US events on the calendar. On Tuesday, the UK releases a host of inflation data, led by CPI. The US will publish retail sales and core retail sales reports.

The crisis between North Korea and the US remains a geopolitical hot spot, but the political temperature is lower this week between Washington and Pyongyang. Last week saw some saber rattling between the two countries, culminating with North Korea threatening to hit Guam with a missile strike. Although both sides are interested in a diplomatic solution, the crisis has unnerved investors, boosting safe-haven assets such as gold and the Japanese yen. Donald Trump has his hands full on the domestic front as well. The White House faced stinging criticism from both Republicans and Democrats, as Trump failed to single out white supremacists for the violence in Charlottesville, Virginia, where one person was killed at a demonstration against far-right marchers.

The British manufacturing sector is showing signs of fatigue, based on a key indicator, Manufacturing Production. The indicator has managed just one gain in 2017, and the June reading of 0.0% is hardly reassuring news. There was no relief from Britain's trade balance, as the deficit climbed to GBP 12.7 billion in June, marking a three month high. Investors remain concerned about Brexit, and the Bank of England has not shied away from warning that Britain's departure from the EU will hurt the British economy. One of the buzz words surrounding Brexit is "transition period", as some politicians have come out in favor of a period between Britain's departure and post-Brexit rules coming into effect. This would minimize the destabilizing effect of Brexit on financial companies, for example. Last week, BoE Deputy Governor Sam Woods said that "some form of implementation period is desirable", although he stopped short of providing any specifics. The concept of a transition period could come up in talks between the two sides if the May government decides that it wants a transition period.

Dollar Climbs as War Tensions Calm; Euro Drifts Lower after Poor Industrial Performance

During European trading hours, the dollar managed to reverse partially from losses made on Friday, after comments by two US civil officials and the South Korean president on Monday eased war tensions between the US and North Korea. Meanwhile, the euro weakened as data out of the eurozone showed that industrial output in the area missed expectations.

Following Trump's comments on Friday, who warned that the US army was "locked and loaded" if North Korea acted unwisely, the South Korean president, Moon Jae-in, said on Monday in a meeting with aides and advisers, that conflicts between the two countries must be resolved "peacefully". The risks of a nuclear war have also diminished following the remarks by the US National security adviser H. R. McMaster and the US Central Intelligence Agency Director Mike Pompeo on Sunday. The former expressed that the country is "not close to a war than a week ago", while the latter supported that the situation was exaggerated and that a potential war would not take place even if the North Korean president continued with missile tests.

The dollar gained against its rivals, with the dollar index rising from 92.96 at the end of the Asian session to 93.18 during afternoon European trading hours.

Demand for safe-haven assets also slowed down amid fewer concerns of a possible nuclear war. Dollar/franc posted the greatest gain in approximately three-weeks, climbing to 0.9687, while dollar/yen was in an uptrend during the day despite upbeat Japanese GDP data released early on Monday.

In other news, eurozone industrial production contracted by 0.6% month-on-month in June after posting the highest growth – specifcally, 1.2% – seen in 2017 during May (downwardly revised from 1.3%). Expectations were for a milder reduction by 0.5%. However, year-on-year, the figure was positive at 2.6%, below the forecasted 2.8% and May's six-year high of 3.9%.

As a response to the data, the euro retreated against the greenback, falling from $1.1806 prior the data release to $1.1788.

Sterling lost ground versus its US counterpart, declining to $1.2969 after UK ministers Phillip Hammond and Liam Fox held on Sunday a joint position that the transition period after Brexit should be limited in duration and should not be used to prevent Brexit.

The aussie and the kiwi continued their downtrend as a consequence of the disappointing Chinese data published during Asian trading and which involved industrial production, retail sales, and fixed capital investment. The aussie traded lower at $0.7862 and the kiwi was down to $0.7287.

The loonie weakened versus the dollar, with dollar/loonie climbing to 1.2707.

Regarding commodity markets, oil prices rebounded from intra-day losses. WTI crude and Brent both last traded up on the day at $49.00 and $52.25 per barrel, up 0.4% and 0.2% on the day respectively. Gold recovered moderately to $1283.14 per ounce after touching a session low of $1278.48.

USD/JPY Rises Despite Strong Japan GDP

The EUR/USD price is dropping after a strong upward impulse at the end of last week following the weaker than expected report on American consumer price index. The increase of inflation in July by only 0.1% reduced the possibility of the third rate hike by the Fed during 2017. The main factor that supports the greenback is some easing in tensions related to the confrontation between the US and North Korea. Investors are waiting for tomorrows data on American retail sales that may possibly lead to high volatility.

The USD/JPY demonstrates confident upward movements amid a stronger US dollar and a lower demand for the Yen as a defensive asset. We should note that those two factors have been able to offset the strong statistics according to which the Japanese economy expanded by 1.0% in the second quarter compared to 0.3% in the previous period.

The Australian dollar has been hit by a number of factors during today's trading session, including the rebound of the US dollar, lower commodities' prices and disappointing macro statistics from the country's main trading partner China. Thus, the industrial production in the second largest economic power in the world slowed to 6.4% in June, that is 0.7% worse than expected. At the same time, retail sales in China during June increased by 10.4% vs the similar period of 2016 while experts anticipated an increase of 10.9%.

EUR/USD

The single currency price has rolled back after it tested the local resistance near 1.1850. The potential of growth is limited by the important 1.1900 mark and its breaking will open the way for a further increase up to 1.2000 and 1.2200. On the other hand, fixing below 1.1800 may become a trigger for a continued fall to 1.1700 and 1.1620. The volatility is likely to remain high tomorrow.

USD/JPY

After a number of attempts to overcome the 108.85 level and to fix below it, the USD/JPY has shown a confident growth within the descending channel and currently is around 109.60. In order to change the trend to positive, the price needs to break through the upper boundary of the channel and to gain a foothold above 110.30. In case of success, the targets will be at 113.00 and 114.70. Currently the price is moving within the descending band and its next goal in case of the fall resumption will be at 108.85.

AUD/USD

The AUD/USD is falling sharply within the limits of the descending channel. In case of updating the local low near 0.7840 we are likely to see the drop to 0.7800. After a rapid movement, we may see the upward correction pointing to the RSI near the oversold zone on the 15-minute chart. In such cases, the quotes may return to 0.7900 and its breaking may trigger a further increase to 0.8000-0.8050.

Yen Lower Despite Strong GDP Report

USD/JPY has edged higher in the Monday session. In North American trade, the pair is trading at 109.83, up 0.33% on the day. The week started on a positive note, as Japan's Preliminary GDP was solid in the second quarter, posting a gain of 1.0%. This easily beat the estimate of 0.6%. On Monday, there are no Japanese or US releases. On Tuesday, the US releases Retail Sales and Core Retail Sales.

The Japanese economy has shown signs of improvement, and this was underscored as Preliminary GDP in Q2. Japan has now posted a sixth consecutive of growth, marking the longest expansion in over a decade. Although exports have declined, domestic demand has rebounded. With a tight labor market and the business sector confident about economic conditions, better times could continue in 2017. The fly in the ointment remains inflation, as BoJ's ultra-easy monetary policy has failed to eliminate the threat of deflation. The BoJ has insisted that it will not tighten policy before inflation climbs closer to the bank's inflation target of 2%, but clearly this goal is unrealistic in the short term, and the BoJ may have to lower its inflation target.

The Japanese yen was one of the winners of last week's crisis over North Korea, as investors shunned the stock markets and sought safe-haven assets such as the yen and gold. USD/JPY dropped 1.3% last week, and the low of 108.74 marked the lowest weekly low since April. Tensions between North Korea and the US remain high, but the prevalent sentiment in the markets is that a diplomatic solution will be found to end the crisis. Still, Donald Trump and Kim Jon-un are unpredictable leaders, and any move by either side could easily ratchet up tensions and unnerve investors. Donald Trump continues to deal with domestic problems as well, and the White House faced stinging criticism from both Republicans and Democrats, as Trump failed to single out white supremacists for the violence in Charlottseville, Virginia, where one person was killed at a demonstration against far-right marchers.