Sample Category Title

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2939; (P) 1.2980; (R1) 1.3004; More...

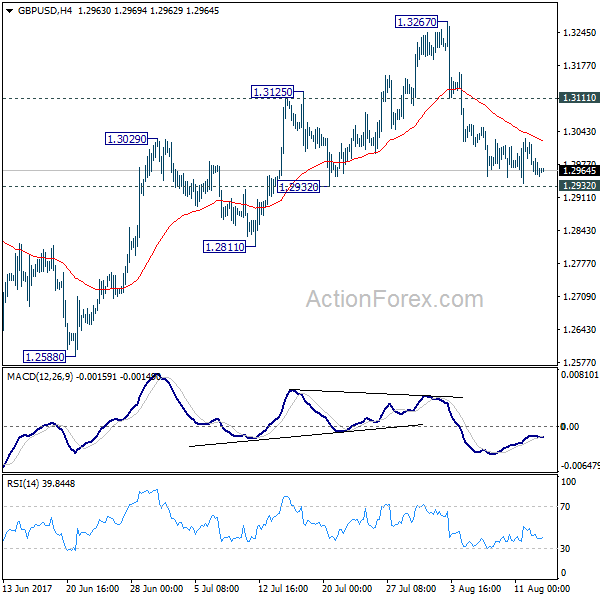

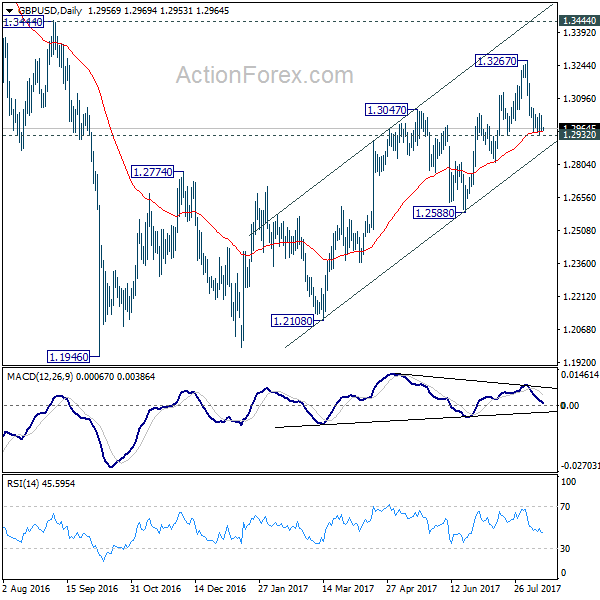

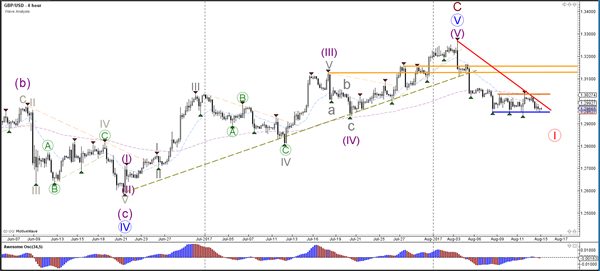

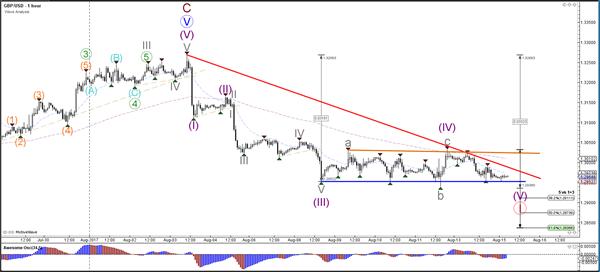

Intraday bias in GBP/USD remains neutral at this point. With 1.3111 resistance intact, near term outlook stays bearish and further fall is expected. As noted before, price actions from 1.1946 are seen as a corrective pattern and could have completed at 1.3267. Break of 1.2932 will affirm this bearish case and target 1.2588 key near term support for confirmation. However, break of 1.3111 resistance will turn bias back to the upside for retesting 1.3267 high instead.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

Elliott Wave View: Dow Future Resuming Higher

Short term Dow Futures (YM_F) Elliott Wave view suggests that rally from 6/29 low is unfolding as a a double three Elliott wave structure. Up from 6/29 low (21138), Minor wave W ended at 22132 and pullback to 21790 ended Minor wave X. Rally from there is unfolding as an impulse Elliott wave structure. Up from 21790, Subminutte wave i ended at 21884, Subminutte wave ii ended at 21815, Subminutte wave iii ended at 21988 and Subminutte wave iv ended at 21946. Expect Subminutte wave v of (a) to complete soon and thus cycle from 8/11 low to end. Index should then pullback in Minutte wave (b) to correct cycle from 8/11 low before resuming higher again. We don't like selling the proposed pullback and expect buyers to appear once Minutte wave (b) pullback is complete in 3, 7, or 11 swing provided pivot at 21787 low stays intact.

Dow Future 1 Hour Elliott Wave Chart

Double Three is the most important pattern in the new Elliott wave theory and probably the most common pattern in the market these days. Double three is also known as a 7 swing structure. It is a very reliable pattern that gives traders good opportunity to trade with a well defined invalidation level and target areas. The image below shows what Elliott Wave Double Three looks like. It has (W), (X), (Y) labels and an internal structure of 3-3-3, which means that all 3 legs has corrective sequences. Each (W) and (Y) is made of 3 waves oscillations & has structure of A, B, C or another W, X, Y of a lesser extent.

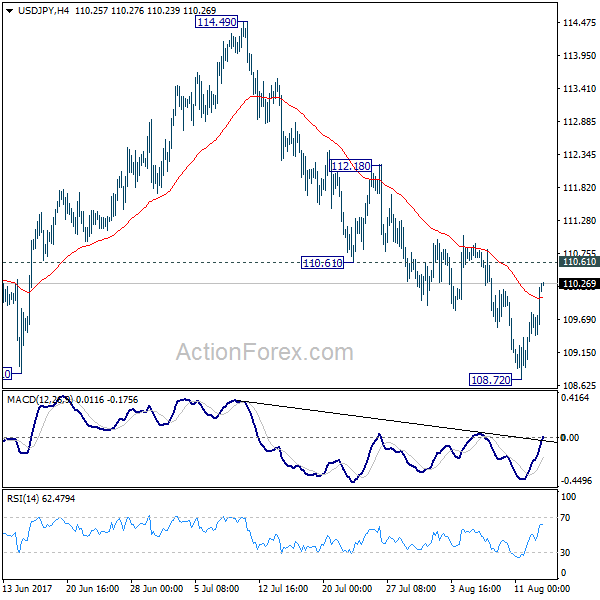

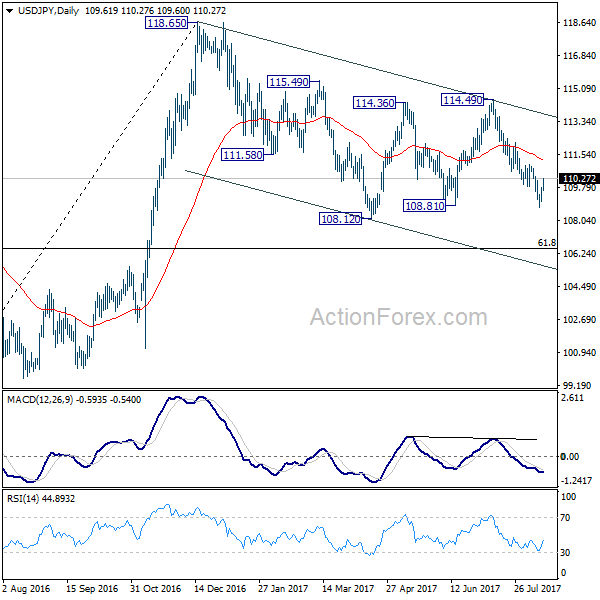

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.18; (P) 109.48; (R1) 109.95; More...

USD/JPY's rebound from 108.72 extends higher today. But it's staying below 110.61 support turned resistance and intraday bias remains neutral. Near term outlook also stays bearish and deeper decline is expected. Firm break of 108.81 support will resume whole corrective fall from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48. However, break of 110.61 will indicate short term bottoming and turn bias back to the upside for 112.18 resistance and above.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

Daily Technical Analysis: USD/JPY Reversal At 109 Support Zone Starts ABC Zigzag

Currency pair USD/JPY

The USD/JPY bounced at the support zone (green lines) of the previous daily bottom and broke above the resistance trend line (dotted orange). The wave structure is therefore favouring a completion of the wave A (brown) at the newest low and the current bullish price action could be a wave A (orange) within wave B (brown).

The USD/JPY is building a wave 5 (purple) within wave A (orange). Price could complete the wave 5 at the targets of wave 5 vs 1+3.

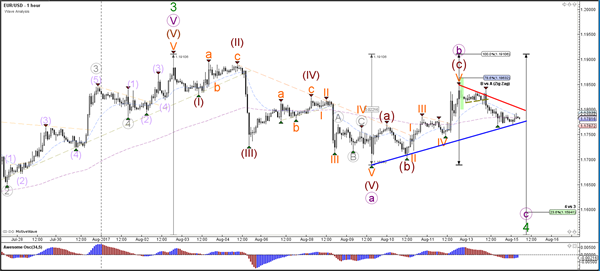

Currency pair EUR/USD

The EUR/USD made a bearish bounce at the Fibonacci levels of wave B vs A. The divergence between the tops (purple line) could create a larger bearish retracement via an ABC correction (purple). The main targets are the 23.6 and 38.2% Fibonacci levels of wave 4 vs 3. A break of the top and 100% Fibonacci level of wave B vs A at 1.1910 could indicate an uptrend continuation.

The EUR/USD potential break above the resistance (red) of the triangle chart pattern could see price move towards the next 78.6% Fibonacci level of wave B vs A whereas a break below support (blue) could see price continue towards the 23.6% Fib of wave 4 (green).

Currency pair GBP/USD

The GBP/USD downtrend is building a pause by moving sideways between support (blue) and resistance (orange). A bearish breakout could indicate the continuation of wave 1 (red).

The GBP/USD sideways zone increases the chance that the current pattern is a choppy wave 4 (purple) correction.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

We typically search for lower-timeframe confirmation between the M15 and H1 timeframes, since most of our higher-timeframe areas begin with the H4. Stops are usually placed 1-3 pips beyond confirming structures.

EUR/USD

Try as it might, the single currency could not muster enough strength to close above August’s opening level at 1.1830 on Monday. In consequence to this, the pair fell away and eventually closed beneath the 1.18 handle, ending the day challenging a H4 demand pegged at 1.1774-1.1748. Perhaps the most compelling factor seen around this zone is the weekly support at 1.1768, which runs through the top edge of this area beautifully.

A long from the current H4 demand is tempting given the fusing weekly support and how strong the underlying trend on the EUR is at the moment. With that being said, however, there are two cautionary points to consider. The first being the 1.18 handle lurking just above the demand. The second point is the daily demand at 1.1650-1.1733 which happens to converge with a H4 trendline support etched from the low 1.1612. With this zone sited underneath the current H4 demand base, there’s a strong possibility that a fakeout may take shape.

Suggestions: The aforementioned H4 demand, even though it boasts weekly support at 1.1768, is not a place we will be looking to buy from today, largely because of the reasons stated above. To that end, our desk will remain on the sidelines until more favorable price action presents itself.

Data points to consider: German Prelim GDP q/q at 7am. US Core retail sales figures at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

GBP/USD

As can be seen on the H4 timeframe this morning, the GBP chewed its way through bids around the 1.30 neighborhood on Monday and proceeded to press back into the current consolidation drawn between 1.3015-1.2953 (yellow zone).

Yesterday’s move to the downside also forced daily price to strongly close beneath a support area at 1.3058-1.2979. With little bullish intent seen registered from this zone last week, we feel this base is now drained and lower prices could be on the cards. A continued move lower from here would likely expose another support area located at 1.2818-1.2752, which happens to fuse with a channel support etched from the low 1.2365 and is also seen glued to the top edge of a weekly demand at 1.2589-1.2759. In addition to this, let’s also remind ourselves where weekly price is trading from at the moment: a weekly supply area coming in at 1.3120-1.2957.

Suggestions: Despite what’s being seen on the higher timeframes at the moment, we will not become sellers in this market UNTIL a close below the 1.2950 neighborhood is seen. This – coupled with a successful retest of 1.2950, a short down to the 1.29 handle, followed closely by June’s opening line at 1.2870/H4 Quasimodo support at 1.2857, is a viable trade in our book.

Data points to consider: UK inflation figures scheduled for 9.30am. US Core retail sales figures at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for H4 price to close below the 1.2950 region and then look to trade any retest seen thereafter ([waiting for a reasonably sized bearish candle to form following the retest – in the shape of either a full, or near-full-bodied candle – is advised] stop loss: ideally beyond the candle’s wick).

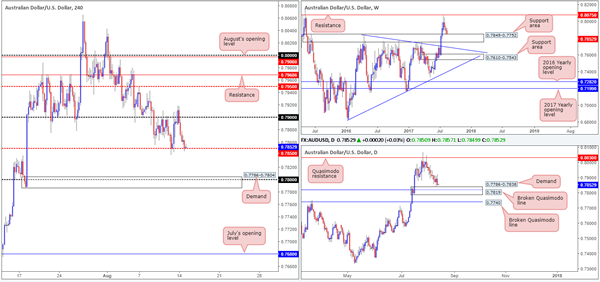

AUD/USD

Kicking this morning’s report off with a look at the weekly timeframe, we can see that the candles recently came into contact with a support area marked at 0.7849-0.7752. There was, as noted in Monday’s report, a mild end-of-week correction seen from the top edge of this base. Looking down to the daily timeframe, the commodity currency is seen lurking just ahead of a demand at 0.7786-0.7838 (encases a daily broken Quasimodo level at 0.7819). The demand, as you can see, boasts a strong-looking base. This, alongside it being positioned within the current weekly support area, could see higher prices from here in the near future.

Recent activity on the H4 timeframe shows price failed to sustain gains beyond the 0.79 handle, and proceeded to fall sharply down to the mid-level support at 0.7850 (denotes the top edge of the aforesaid weekly support area). A violation of this line could lead to a move being seen down to the 0.78 handle, which is seen encased within a H4 demand area at 0.7786-0.7804.

Suggestions: With room being seen on the daily timeframe for price to stretch beyond the H4 mid-level support at 0.7850, we would not feel comfortable buying from this line. From our perspective, an ideal scenario would be for price to reach beyond 0.7850 today and cross swords with the aforementioned H4 demand area. As we believe this is a strong buy zone, our desk has set a pending buy order at 0.7805, with a stop-loss order tucked beneath at 0.7784.

Data points to consider: Australian Monetary policy meeting minutes at 2.30am. US Core retail sales figures at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: 0.7805 ([pending order] stop loss: 0.7784).

- Sells: Flat (stop loss: N/A).

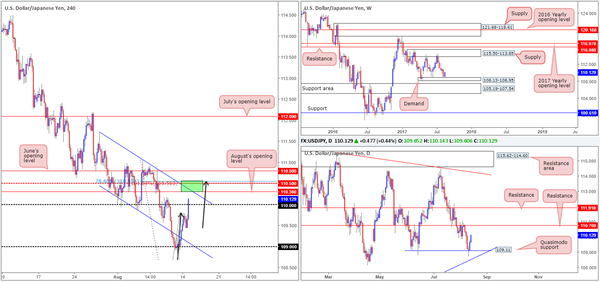

USD/JPY

The US dollar made considerable ground against the Japanese yen on Monday, as geopolitical tensions eased between the US and North Korea (Bloomberg). As you can probably see, this has placed the H4 candles above the 110 handle and in-line for an attack of August’s opening level at 110.30, followed closely by the mid-level resistance at 110.50. What’s also notable from here is the AB=CD completion point at 110.50 (black arrows – 161.8% Fib ext.), the 78.6% Fib resistance at 110.55 (basically representing a Gartley Harmonic sell zone) and a channel resistance extended from the high 111.71.

While a short from the green H4 zone is incredibly tempting, traders may want to consider that weekly action is currently trading from demand at 108.13-108.95. Further adding to this, we do not see much in the way of resistance on the daily timeframe until we meet 110.76.

Suggestions: Despite weekly price trading from demand, a sell from the 110.50 neighborhood on the H4 timeframe is still interesting. Stops will, however, have to be positioned above June’s opening level at 110.80, thus clearing daily resistance at 110.76. The ultimate target from here would, from our perspective, be the neighboring channel support stretched from the low 110.30.

Data points to consider: US Core retail sales figures at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 110.50 region (stop loss: 110.80).

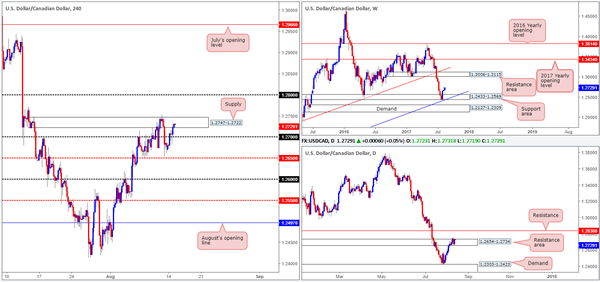

USD/CAD

The US dollar advanced against its Canadian counterpart on Monday, consequently lifting the pair above the 1.27 handle and into the jaws of a H4 supply drawn from 1.2747-1.2722. As noted in Monday’s report, this supply area suffered a minor breach to the upside on Friday, which may have cleared the path north for the bulls to challenge the 1.28 region.

On the weekly timeframe, we do not see any obvious resistance on this scale until the resistance area planted at 1.3006-1.3115. The story on the daily timeframe shows price to be trading around a resistance area given at 1.2654-1.2734. The bears appear to lacking here, thus giving the impression we may see the unit stretch up to the resistance level penciled in at 1.2838.

Suggestions: Based on the above, we feel the current H4 supply zone will likely be taken out today. However, we would not be comfortable buyers in this market until a H4 close above this supply is seen. In order to press the buy button, however, we would require a retest of this area as support and a lower-timeframe buy signal (see the top of this report). The initial take-profit level for this setup would be 1.28, followed by the daily resistance at 1.2838, and quite possibly beyond given what the weekly timeframe shows.

Data points to consider: US Core retail sales figures at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: Watch for H4 price to close above 1.2747-1.2722 and then look to trade any retest seen thereafter ([waiting for a lower-timeframe buy signal to form following the retest is advised] stop loss: dependent on where one confirms this area).

- Sells: Flat (stop loss: N/A).

USD/CHF

An improvement in risk appetite on Monday weakened the demand for safe-haven assets, pushing the US dollar above both August and June’s opening levels at 0.9672/0.9680 and the 0.97 handle. The next level of resistance on the H4 timeframe can be seen at 0.9750, shadowed closely by a Quasimodo resistance line at 0.9764.

Over on the bigger picture, we can see that weekly price reconnected with a weekly trendline resistance extended from the low 0.9257. On the daily timeframe, however, the unit is seen trading within striking distance of a Quasimodo resistance planted at 0.9776.

Suggestions: Technically speaking, this is not a market we would like to be buyers in at the moment. There’s just too much overhead structure to consider! What we are interested in, nonetheless, is a sell from the daily Quasimodo resistance mentioned above at 0.9776, largely because of how well price reacted when it came near to testing the boundary last week, and, of course, the converging weekly trendline resistance!

Data points to consider: US Core retail sales figures at 1.30pm. Swiss PPI numbers at 8.15am GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 0.9776 region ([waiting for a reasonably sized bearish candle to form – in the shape of either a full, or near-full-bodied candle – is advised] stop loss: ideally beyond the candle’s wick).

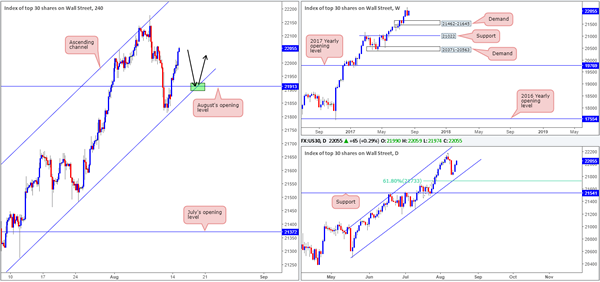

DOW 30

Leaving the H4 channel support line (extended from the low 21273) unchallenged on Monday, the US equity market advanced higher. Running through August’s opening level at 21913, the unit is now seen testing highs of 22059. With both the weekly and daily timeframes showing little resistance on the horizon, a retest of August’s opening level, alongside the aforementioned channel support would, in our humble view, be a nice area to consider entering long from (green zone). However, trendlines are prone to being faked so we would highly recommend being patient and waiting for a H4 bullish candle to take shape in the form of a full, or near-full-bodied candle. This will, of course, not guarantee that the level will hold, but what it will do is show buyer intent from a potential buy zone!

Our suggestions: Keep a close eye on the 21913 region for possible long opportunities.

Data points to consider: US Core retail sales figures at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: 21913 region ([waiting for a reasonably sized bullish candle to form – in the shape of either a full, or near-full-bodied candle – is advised] stop loss: ideally beyond the candle’s tail).

- Sells: Flat (stop loss: N/A).

GOLD:

Demand for the safe-haven metal diminished on Monday as tensions between the US and North Korea eased. From a technical point of view, a selloff in this market was to be expected, as weekly price is seen trading from a resistance area comprised of two weekly Fibonacci extensions 161.8/127.2% at 1312.2/1284.3 taken from the low 1188.1.

Thanks to yesterday’s descent, daily price closed back below the trendline resistance etched from the high 1337.3, and has potentially opened the trapdoor down to a support level pegged at 1258.9. Near-term, however, we have August’s opening level at 1269.3 on the H4 chart to contend with.

Our suggestions: Until we see a H4 close print below August’s opening level, we will refrain from taking any shorts in this market. A close below this monthly line, followed up with a retest and a lower-timeframe sell signal (see the top of this report) would, in our opinion, be enough to confirm a sell trade down to the daily support mentioned above at 1258.9, followed closely by H4 support at 1254.3.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for H4 price to close below 1269.3 and then look to trade any retest seen thereafter ([waiting for a lower-timeframe sell signal to form following the retest is advised] stop loss: dependent on where one confirms this level).

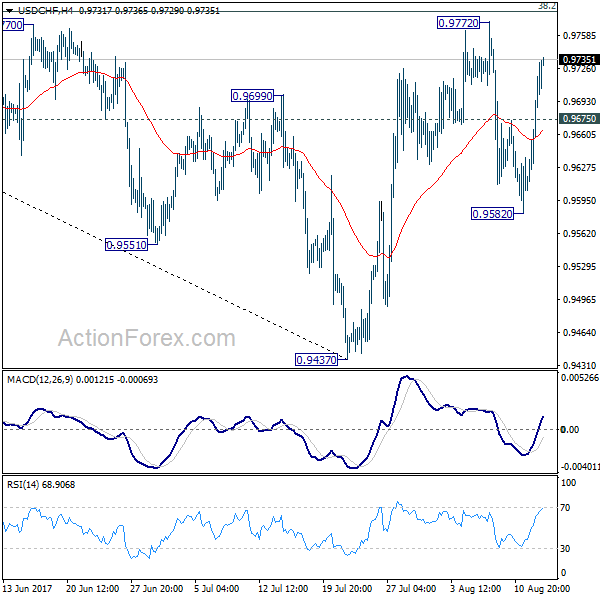

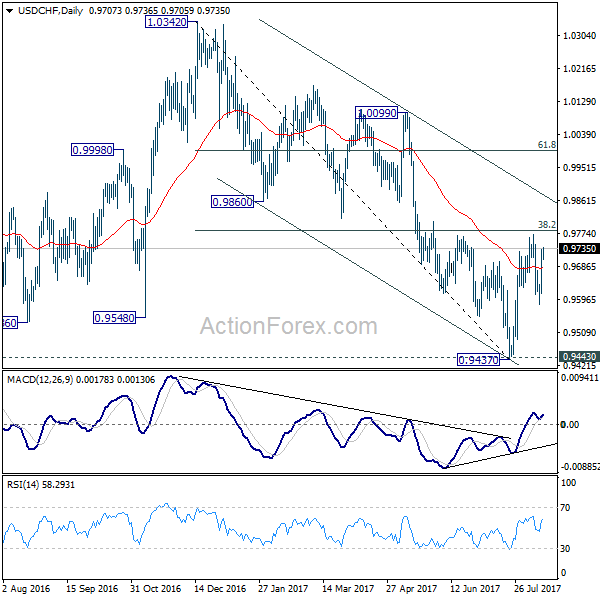

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9642; (P) 0.9687; (R1) 0.9765; More...

Intraday bias in USD/CHF remains on the upside as rebound from 0.9582 is in progress for retesting 0.9772. Decisive break there will revive the bullish case of reversal. That is, whole decline from 1.0342 has completed at 0.9437 after defending 0.9443 support. USD/CHF should then target channel resistance (now at 0.9880) next. On the downside, below 0.9675 minor support will turn intraday bias neutral first. Also, the pair is bounded inside medium term falling channel and limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783 for the moment. Break of 0.9582 will dampen our bullish view and turn bias back to the downside for 0.9437. This could also extend the fall from 1.0342 through 0.9437/43 key support level.

In the bigger picture, current development argues that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996. However, firm break of 0.9443 will carry larger bearish implication and would target next key support at 0.9072.

Dollar Surges against Yen and Franc as Fed Dudley Still Favors Another Hike

Dollar trades notably higher against Japanese Yen and Swiss Franc as comments from a top Fed official revived the speculation of one more hike this year. On the background, risk aversion also receded as threat of imminent war between US and North Korea abated. DOW rebounded 0.62% to close at 21993.71. S&P 500 also gained 1.00% to close at 24.52. Sentiment in Asian session is also positive with Nikkei trading up 1.2% at the time of writing. While the greenback is trying to stage a general rebound, it should be noted that Euro is staying firm too. EUR/USD is bounded in range of 1.1688/1908, maintaining near term bullishness. Also, we don't see any solid buying to push Dollar index back above 94.28 key near term resistance yet.

Fed Dudley favors another rate hike this year

New York Fed President William Dudley, an influential member of FOMC, affirmed that he remained in "favor of doing another rate hike later this year". He prefers a rate hike despite soft inflation as "1) monetary policy is still accommodative, so the level of short-term rates is pretty low, and 2) and this is probably even more important, financial conditions have been easing rather than tightening". He indicated that "financial conditions are easier today than they were a year ago". Dudley added that it is not unreasonable to announce the balance sheet reduction plan in September. He forecast the portfolio would shrink to between USD 2.5-3.5T after five years.

Market's pricing of Fed rate path is back to normal. On Friday just after the release of weak CPI, Fed fund futures priced in 4.1% of a rate cut in September and less than 36% chance of a hike by December. Currently, Fed fund futures are pricing 0% chance of a cut in September. Chance of a rate hike by December is now back at around 50%.

German FM Schaeuble hoped ECB to end ultra-loose policy soon

In Eurozone, German Finance Minister Wolfgang Schaeuble said the he hoped ECB's ultra-loose monetary policy would end in the foreseeable future. He noted that "no one seriously disputes that interest rates are rather too low for the strength of the German economy and the exchange rate of the euro, which is rising now." And in his view, most people expect ECB to take a further step at the upcoming meeting in September.

RBA minutes paint positive outlook

RBA's minutes for the August meeting revealed that policymakers were optimistic over the global and domestic economies. The central bank forecast that the economy would soon be growing at an annual rate of 3%, assuming that there's no major change in the Australian dollar. The central bank added that 'This assumption was one source of uncertainty'. Policymakers went to warn of the Aussie's strength, suggesting that 'a further appreciation of the Australian dollar would be expected to result in a slower pick-up in inflation and economic activity than currently forecast'. Meanwhile, RBA also signaled concerns over the housing market and household debt, while appeared more comfortable over the employment situation. More in RBA's Main Concerns Shifted to Housing Market From Employment

Oil price falls on China slowdown

WTI crude oil dropped notably overnight and is now back trading at 47.6. The decline in crude oil prices was the most in 5 weeks, driven mainly by weakened Chinese demand and bigger-than-expected slowdown in Chinese economic activities at the start of the second quarter. Bloomberg estimated that the country's oil processing dropped 4.4% ,p, to 10.76M bpd in July. The decline was the biggest since 2014. Chinese industry consultant SCI99 noted that state refineries in northwest and southern regions cut runs to 66.9% and 64.68% of capacity, respectively, also the lowest since 2014, last month. Independent refiners were operating at just around 58.78%, a level not seen since May 5.

UK CPI the main focus in European session

Looking ahead, the economic calendar is very busy today. UK inflation will be a key to watch in European session. Headline CPI in UK is expected to climb back to 2.7% yoy while core CPI might rise back to 2.5% yoy. Sterling was under much selling pressure after last month's CPI miss. Another downside surprise today will send GBP/USD through 1.2932 key near term support. German GDP and Swiss PPI will be other features of European session.

From US, main focus will be on retail sales which is expected to stage a rebound in July. Empire state manufacturing index, import price, NAHB housing index and business inventories will also be featured.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9642; (P) 0.9687; (R1) 0.9765; More...

Intraday bias in USD/CHF remains on the upside as rebound from 0.9582 is in progress for retesting 0.9772. Decisive break there will revive the bullish case of reversal. That is, whole decline from 1.0342 has completed at 0.9437 after defending 0.9443 support. USD/CHF should then target channel resistance (now at 0.9880) next. On the downside, below 0.9675 minor support will turn intraday bias neutral first. Also, the pair is bounded inside medium term falling channel and limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783 for the moment. Break of 0.9582 will dampen our bullish view and turn bias back to the downside for 0.9437. This could also extend the fall from 1.0342 through 0.9437/43 key support level.

In the bigger picture, current development argues that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996. However, firm break of 0.9443 will carry larger bearish implication and would target next key support at 0.9072.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Minutes Aug | ||||

| 04:30 | JPY | Industrial Production M/M Jun F | 1.60% | 1.60% | ||

| 06:00 | EUR | German GDP Q/Q Q2 P | 0.70% | 0.60% | ||

| 07:15 | CHF | Producer & Import Prices M/M Jul | 0.00% | -0.10% | ||

| 07:15 | CHF | Producer & Import Prices Y/Y Jul | 0.00% | -0.10% | ||

| 08:30 | GBP | CPI M/M Jul | 0.00% | 0.00% | ||

| 08:30 | GBP | CPI Y/Y Jul | 2.70% | 2.60% | ||

| 08:30 | GBP | Core CPI Y/Y Jul | 2.50% | 2.40% | ||

| 08:30 | GBP | RPI M/M Jul | 0.10% | 0.20% | ||

| 08:30 | GBP | RPI Y/Y Jul | 3.50% | 3.50% | ||

| 08:30 | GBP | PPI Input M/M Jul | 0.40% | -0.40% | ||

| 08:30 | GBP | PPI Input Y/Y Jul | 6.90% | 9.90% | ||

| 08:30 | GBP | PPI Output M/M Jul | 0.00% | 0.00% | ||

| 08:30 | GBP | PPI Output Y/Y Jul | 3.10% | 3.30% | ||

| 08:30 | GBP | PPI Output Core M/M Jul | 0.10% | 0.20% | ||

| 08:30 | GBP | PPI Output Core Y/Y Jul | 2.50% | 2.90% | ||

| 08:30 | GBP | House Price Index Y/Y Jun | 4.30% | 4.70% | ||

| 12:30 | USD | Import Price Index M/M Jul | 0.10% | -0.20% | ||

| 12:30 | USD | Empire State Manufacturing Index Aug | 10.3 | 9.8 | ||

| 12:30 | USD | Advance Retail Sales Jul | 0.40% | -0.20% | ||

| 12:30 | USD | Retail Sales Less Autos Jul | 0.30% | -0.20% | ||

| 14:00 | USD | NAHB Housing Market Index Aug | 64 | 64 | ||

| 14:00 | USD | Business Inventories Jun | 0.40% | 0.30% | ||

| 20:00 | USD | Net Long-term TIC Flows Jun | 91.9B |

EUR/GBP Capped Within Resistance Zone

The EUR/GBP swing high resistance obviously wasn't enough to keep the pair capped, but I wanted to take the opportunity today to discuss why I see a zone rather than a hard level in this particular forex currency pair.

EUR/GBP Daily:

Price is hugging the top of that bullish channel, which is the obvious area of resistance on the EUR/GBP daily chart. But as you can see here, there's also quite the large horizontal resistance zone with no real clear top to draw a single line from.

As you well know, each forex currency pair has a personality all of its own. In my opinion, EUR/GBP just isn't the type of pair that touches support/resistance and then immediately moves away. Like all pairs, it respects major levels, but it consolidates in a lot of sideways price action before moving off or through them.

Now just look back at the 2016 spikes that my horizontal resistance levels have tried to be drawn off and look at the price action at that time. Like I said above, there is definitely a level there, but the sideways choppy price action makes it much more of a zone. What a zone at that!

For me, that channel resistance inside a huge resistance zone just isn't clear enough to cleanly be able to trade the level. The best bet here is to wait and see what sort of reversal pattern that the charts print in here and then zoom in and look for short term support turned resistance to possibly short off.

RBA’s Main Concerns Shifted to Housing Market From Employment

RBA's minutes for the August meeting revealed that policymakers were optimistic over the global and domestic economies. However, they reiterated the warning of the strength of Australian dollar, noting that its appreciation would curb growth and inflation over time. The central bank signaled concerns over the housing market and household debt, while appeared more comfortable over the employment situation. AUDUSD recovered after the release of the minutes.

The central bank appeared less concerned over the job market. At noted in the minutes, 'wage growth had remained low but was still expected to increase a little as conditions in the labor market improved'. It added that 'recent strong employment growth would be likely to contribute to an increase in household disposable income, and therefore consumption growth, over the forecast period'. In June, Australia's unemployment rate stayed unchanged at 5.6%. Yet, the increase in the number of full time jobs (up +62K) unveiled that the employers are more confidence over the economic outlook. The participation rate also added + 0.1 percentage point to 65%.

On the housing market, RBA noted that the rising prices and household balance sheets 'warrant careful monitoring'. The minutes noted that while the conditions in top-tiered cities, such as Sydney and Melbourne, had eased, housing price growth in these cities had 'remained relatively strong'. Housing markets in other regions 'had been declining', though. It added that the 'overall housing credit growth had continued to outpace the relatively slow growth in household incomes'. Indeed, the latest data from CoreLogic suggested that home values increased, from a year ago, in Sydney, Melbourne, Brisbane and Adelaide in the week ended August 13, while Perth edged lower. Meanwhile, the number of homes taken to auction rose to 2 011, compared with 1 857 over the previous week, across the combined capital cities this week. This marked the largest number of auctions held since the last week of June 2017 and approximately one third higher compared with the same week a year ago.

The RBA forecast that the economy would soon be growing at an annual rate of +3%, assuming that there's no major change in the Australian dollar. The central bank added that 'This assumption was one source of uncertainty'. Policymakers went to warn of the Aussie's strength, suggesting that 'a further appreciation of the Australian dollar would be expected to result in a slower pick-up in inflation and economic activity than currently forecast'.

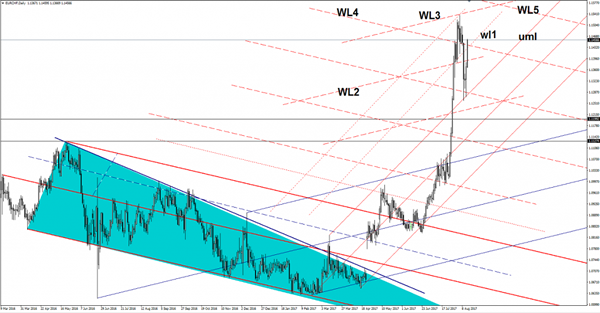

EUR/CHF Registered An Amazing Jump

Price rallies and looks to stabilize in the green zone if possible. Has extended the Friday’s rally and tries to recover after the immense drop. I’ve said in the previous week that the retreat could be completed after the failure to close on the upper median line (uml) of the minor ascending pitchfork.