Sample Category Title

Trade Idea : USD/JPY – Exit short entered at 110.10

USD/JPY - 110.30

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 110.08

Kijun-Sen level : 109.94

Ichimoku cloud top : 109.41

Ichimoku cloud bottom : 109.26

Original strategy :

Sold at 110.10, Target: 109.10, Stop: 110.45

Position : - Short at 110.10

Target : - 109.10

Stop : - 110.45

New strategy :

Exit short entered at 110.10

Position : - Short at 110.10

Target : -

Stop : -

As the greenback has maintained a firm undertone after breaking above resistance at 110.18, suggesting the rebound from 108.73 low is still in progress and near term upside risk remains for further gain to 110.49-50 (100% projection of 108.73-109.80 measuring from 109.42), then towards resistance at 110.83, however, near term overbought condition should prevent sharp move beyond previous resistance at 111.05, risk from there is seen for a retreat later.

In view of this, would be prudent to exit short entered at 110.10 and stand aside for now. below the Kijun-Sen (now at 109.94) would bring test of previous resistance at 109.80 but break of support at 109.42 is needed to signal top is formed and revive bearishness for weakness towards 109.00.

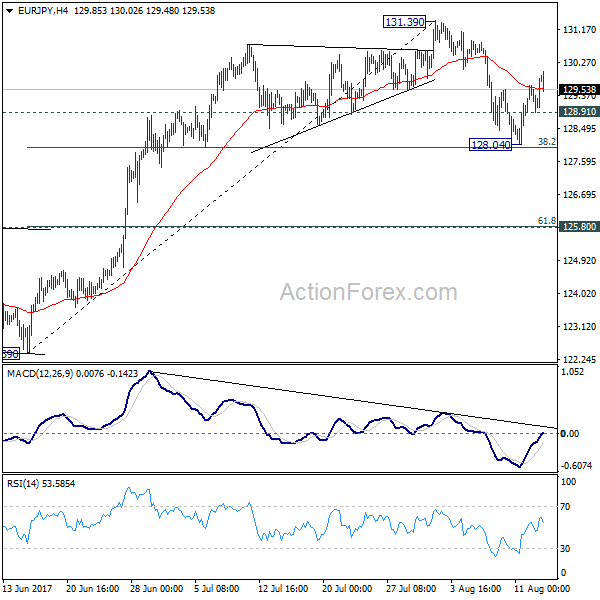

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.82; (P) 129.23; (R1) 129.57; More...

Intraday bias in EUR/JPY remains on the upside as rebound from 128.04 would target retesting 131.39 high. Break there is needed to confirm up trend resumption. Otherwise, we'd likely see more consolidation first. On the downside, below 128.91 minor support will turn bias to the downside for another fall. At this point, we'd still expect strong support from 38.2% retracement of 122.39 to 131.39 at 127.95 to bring rebound. But sustained break of 127.95 will bring deeper decline to 125.80 cluster support (61.8% retracement at 125.82) before completing the correction.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 124.08 resistance turned support holds.

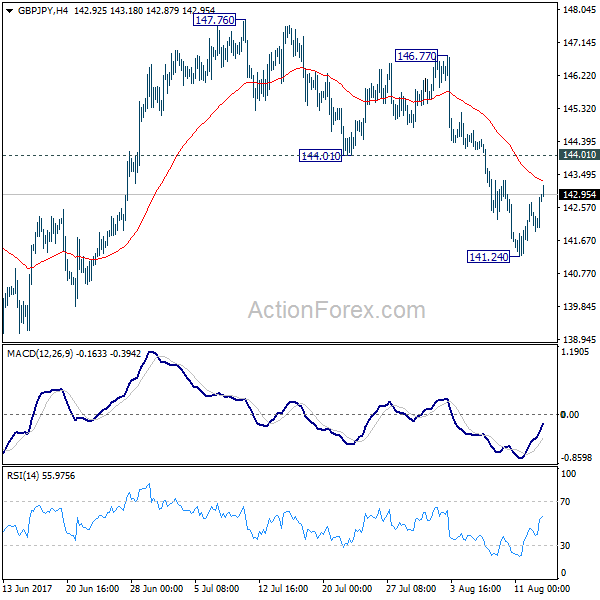

GBP/JPY Daily Outlook

Daily Pivots: (S1) 141.66; (P) 142.19; (R1) 142.68; More

GBP/JPY recovers further today but stays below 144.01 support turned resistance. Intraday bias remains neutral with bearish near term outlook. Below 141.24 will extend the fall from 147.76 to 138.65 support and below. As GBP/JPY is seen as staying in consolidation pattern from 148.42, we'd expect strong support from 135.58 to contain downside. On the upside, break of 144.01 will indicate completion of the decline from 147.76 and turn bias back to the upside.

In the bigger picture, the sideway pattern from 148.42 is extending with another leg. But we'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise from 122.36 is still expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1775

The rise from 1.1687 has been reversed at yesterday's peak at 1.1847 and the bias is already bearish, for a break through 1.1687 low, towards 1.1580.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1850 | 1.1909 | 1.1750 | 1.1580 |

| 1.1909 | 1.2000 | 1.1680 | 1.1480 |

USD/JPY

Current level - 110.25

The bias is still positive as the pair is currently testing 110.30 resistance area. There is a risk of bouncing even higher, towards 111.10 mark, but the outlook on the senior frames remains bearish, for a slide towards 108.10 low. Trigger on the downside is 109.40.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 110.30 | 112.20 | 109.40 | 108.10 |

| 111.10 | 114.50 | 108.10 | 107.00 |

GBP/USD

Current level - 1.2967

Although there is an intraday risk of another attempt at 1.3050, the overall outlook remains bearish, for a slide towards 1.2810 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3050 | 1.3260 | 1.2930 | 1.2930 |

| 1.3100 | 1.3500 | 1.2810 | 1.2810 |

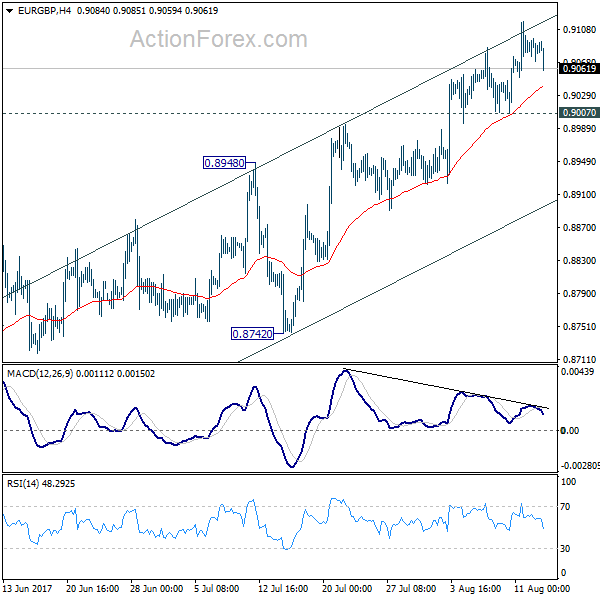

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.9072; (P) 0.9084; (R1) 0.9099; More

With 0.9007 minor support intact, further rise is still expected in EUR/GBP. Current rise from 0.8312 is expected to target a test on 0.9304 high. At this point, there is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to limit upside and bring another fall. On the downside, considering bearish divergence condition in 4 hour MACD, break of 0.9007 support will indicate short term topping. Intraday bias will then be turned back to the downside for 0.8742/8948 support zone.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

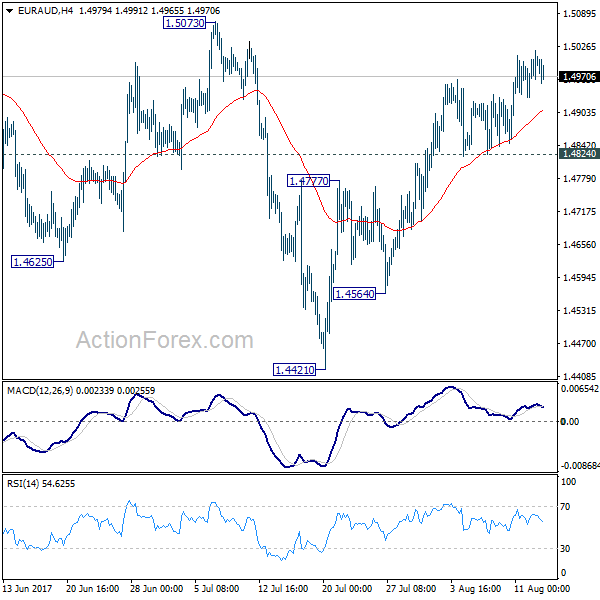

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4951; (P) 1.4985; (R1) 1.5038; More...

With 1.4824 minor support intact, further rise is expected in EUR/AUD to 1.5073 resistance. Correction from 1.5226 should have completed with three waves down to 1.4421 already. Firm break of 1.5073 will likely resume the rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4421 at 1.5411 next. On the downside, however, break of 1.4824 support will dampen our bullish view and turn bias back to the downside for 1.4564 support instead.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the fall from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, another decline will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

Euro Remains Well Bid Above 0.9000 Vs British Pound

Key Highlights

- The Euro after breaching 0.9000 traded as high as 0.9119 against the British Pound.

- There is a key bullish trend line forming with support at 0.9060 on the 4-hours chart of EUR/GBP.

- Germany's Gross Domestic Product preliminary reading for Q2 2017 came in at 0.6% (QoQ), down from the last +0.7%.

- Today, the US Retail Sales figure for July 2017 will be released, which is forecasted to increase by 0.4% (MoM).

EURGBP Technical Analysis

The past few months were mostly bullish for the Euro as it traded above 0.9000 against the British Pound. The EUR/GBP pair recently traded as high as 0.9119 and currently correcting lower.

Looking at the 4-hours chart of EUR/GBP, there is a key bullish trend line forming with support at 0.9060. The recent failure near 0.9120 was from a connecting resistance trend line.

At the moment, the pair is correcting lower and already trading below the 23.6% Fib retracement level of the last wave from the 0.9007 low to 0.9119 high.

There is a chance that EUR/GBP might continue to correct lower towards 0.9060. The mentioned 0.9060 is also the 50% Fib retracement level of the last wave from the 0.9007 low to 0.9119 high.

Therefore, the pair is likely to find buyers near 0.9060. On the upside, an initial resistance is near 0.9100, followed by the recent high of 0.9119.

Germany's Gross Domestic Product

The Euro Zone today saw the release of the German Gross Domestic Product for Q2 2047 (Preliminary reading) by the Statistisches Bundesamt Deutschland. The market was aligned for an increase of 0.7% in the GDP compared with the previous quarter.

The actual result was disappointing, as the German GDP is expected to grow at 0.6% in Q2 2017. It is less than the last +0.7%. In terms of the yearly change, the German GDP is expected to grow at 0.8% in Q2 2017, which is a lot less than the last +3.2% and the forecast +1.9%.

The report pointed out that:

The calendar effect in the first two quarters of 2017 was above average because, in the first quarter, there were 3 working days more and, in the second quarter, there were 3 working days less than a year earlier. When calendar-adjusted, GDP growth in the second quarter of 2017 was 2.1% (following 2.0% in the first quarter of 2017).

Overall, the EUR/GBP pair may continue to correct lower, but more likely to find support near 0.9060 or 0.9010 in the medium term.

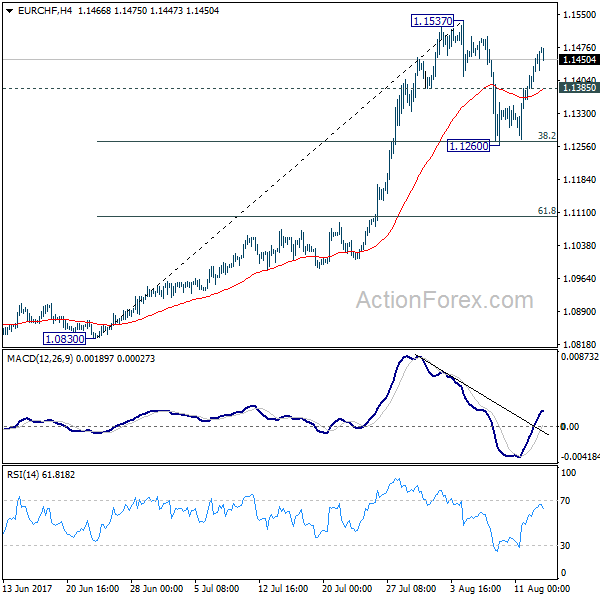

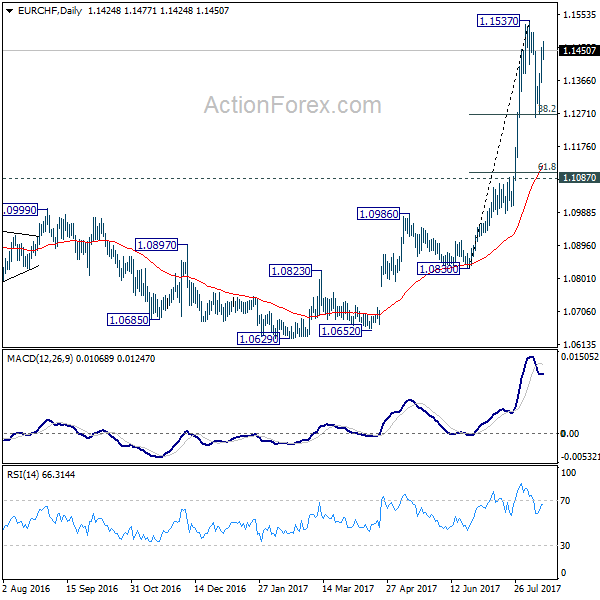

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1389; (P) 1.1425; (R1) 1.1486; More...

Intraday bias in EUR/CHF remains mildly on the upside for retesting 1.1537 resistance. Break there will resumption of up trend from 1.0629. On the downside, below 1.1385 minor support will extend the consolidation from 1.1537 with another rise. In that case, we'd continue to expect strong support from 8.2% retracement of 1.0830 to 1.1537 at 1.1267 to bring rebound. However, firm break of 1.1267 will extend the fall and target 61.8% retracement at 1.1100.

In the bigger picture, firm break of 1.1198 key resistance confirms resumption of the long term rise from SNB spike low back in 2015. In this case, EUR/CHF would eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

European Open Briefing: USD/JPY Made Considerable Ground On Monday

Global Markets:

- Asian stock markets: Nikkei rose 1.30 %, Shanghai Composite up 0.53 %, Hang Seng climbed 0.12 %, ASX up 0.49 %

- Commodities: Gold at $1281.13 (-0.72 %), Silver at $16.88 (-1.40 %), WTI Oil at $47.62 (+0.06 %), Brent Oil at $50.80 (+0.14 %)

- Rates: US 10-year yield at 2.25, UK 10-year yield at 1.06, German 10-year yield at 0.41

News & Data:

- EUR Industrial Production m/m -0.6 % vs -0.4 % expected

- JPY Industrial Production n/m 2.2 % vs 1.6 % expected

- CNY Retail Sales y/y 10.4 % vs 10.9 % expected

- CNY Fixed Asset Investment y/y 8.3 % vs 8.6 % expected

- North Korea Backs Off Guam Missile-Attack Threat – WSJ

- U.S. wages seen growing faster than headline data suggest- RTRS

- China says it will defend interests if U.S. harms trade ties- RTRS

Markets Update:

Asian equity markets extended gains after North Korea's leader signaled that he would delay plans to fire a missile near Guam as the prospect of war between the U.S. and North Korea receded

USD/JPY made considerable ground on Monday, as geopolitical tensions eased between the US and North Korea, the Yen fell over 0.5 percent against the USD from 109.70 up through 110.20 where it has since steadied.

EUR/USD was little changed and seen Trading flat on the day against the dollar at $1.1784. The Euro could not muster enough strength to close above August’s opening level at 1.1830 while the US dollar index added a mere 0.1 percent to 93.480

AUD/USD failed to sustain gains beyond the 0.79 handle yesterday and proceeded to fall sharply down to the mid-level support at 0.7850 before finally rising about 0.3 percent to session highs of 78.71 U.S. cents after the RBA minutes.

Upcoming Events:

- French Bank Holiday

- Italian Bank Holiday

- 06:00 GMT – (EUR) German Prelim GDP q/q

- 07:15 GMT – (CHF) PPI m/m

- 08:30 GMT – (GBP) CPI y/y

- 08:30 GMT – (GBP) PPI Input m/m

- 08:30 GMT – (GBP) RPI y/y

- 12:30 GMT – (USD) Core Retail Sales m/m

- 12:30 GMT – (USD) Retail Sales m/m

- 12:30 GMT – (USD) Empire State Manufacturing Index

- 12:30 GMT – (USD) Import Prices m/m

Market Update – Asian Session: RBA Minutes Reiterate Views

Asia Summary

Asian equity markets opened mostly higher as the risk of conflict between North Korea and the US eased off after Kim Jong Un said he would hold off on an attack on Guam and wait to see how the US behaves before taking any action. This also helped to stabilize currencies in the region. However, a major mover was USD/PHP when it fell to an 11 year low at 51.155. AUD/USD rose slightly but little change in RBA meeting minutes and mixed earnings in Australia failed to give much push. China skipped open market operations but lent CNY399.5B in 1-year medium-term lending facility (MLF) loans at 3.2%, unchanged yield. PBOC also weakened the yuan setting for the first time in 6 days.

Key economic data

(AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index: 111.7 v 113.7 prior

(AU) AUSTRALIA JUL NEW MOTOR VEHICLE SALES M/M: -2.0% V 1.2% PRIOR; Y/Y: 1.8% V 3.6% PRIOR

(AU) RESERVE BANK OF AUSTRALIA (RBA) MEETING MINUTES: GDP GROWTH LIKELY PICKED UP IN Q2, ECONOMY SEEN GROWING AROUND 3% FOR 2018 AND 2019

(JP) Japan Jul Tokyo Condominium Sales y/y: +3.3% v -25.1% prior

Speakers and Press

China/Hong Kong

(CN) China Commerce Ministry (MOFCOM): Hopes US could be ‘prudent’ in review of China’s intellectual property (IP) policy; Will take steps if US takes actions that hurt bilateral trade relations

(CN) China National Energy Administration (NEA): China Jul power consumption: 607.2B KWH, +9.9% y/y (4th consecutive rise)

(CN) China Ministry of Commerce (MOFCOM): China will take actions to defend its interests if the US damages trade ties after President Donald Trump authorized an inquiry into China's alleged theft of intellectual property

(CN) PBOC research bureau head Xu Zhong: Inclusion of banks negotiable certificates of deposit (NCD) in the PBOC's macro-prudential assessment framework from Q1 2018 won’t have major impact on the nation’s banking system

(CN) China National Development and Reform Commission (NDRC) and other government agencies: China is holding back on building new coal-fired power plants to avoid risks from overcapacity and promote a clean energy mix

Australia/New Zealand

(NZ) New Zealand PM English: RBNZ does not need more housing tools; Want the RBNZ to remove loan-to-value ratios (LVRs) - NZ press

Korea

(KR) North Korea KCNA: US should stop its arrogant provocations; Kim Jung Un has discussed ground strike plan with officers

(KR) North Korea Kim Jong Un: Will not attack Guam yet, could change mind based on US actions

(KR) South Korea President Moon: Military action started on Korea peninsula can only be decided by South Korea, will prevent war at all means

Japan

(JP) Japan Fin Min Aso: Housing investment was the biggest driver of growth in Q2 GDP; rising domestic demand covered drop in external demand

Asian Equity Indices/Futures (00:00ET)

Nikkei +1.2%, Hang Seng +0.4%, Shanghai Composite +0.6%, ASX200 +0.7%, Kospi +0.0%

Equity Futures: S&P500 +0.3%; Nasdaq100 +0.5%, Dax +0.4%, FTSE100 +0.2%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1793-1.1768; JPY 110.23-109.61; AUD 0.7877-0.7850; NZD 0.7312-0.7285

Dec Gold -0.7% at $1,281/oz; Sept Crude Oil +0.2% at $47.66/brl; Sept Copper +0.2% at $2.91/lb

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT: 6.6689 V 6.6601 PRIOR (1st weaker setting in 6 days)

(CN) PBoC lends CNY399.5B in 1-year medium-term lending facility (MLF) loans at 3.2%, unchanged yield; confirms that it skipped daily reverse repo operation

(TW) Taiwan sells NT$25B in 20-yr bonds; avg yield 1.591% v 1.798% prior; bid-to-cover 1.97x

Equities notable movers

Hong Kong/China

MMG, 1208.HK Reports prelim H1 Net $113M v -$93M y/y; -4.3%

Wheelock, 20.HK Reports H1 (HK$) Net 6.24B, +5.6% y/y; Rev 33.0B, +21.4% y/y; -4.2%

Japan

FujiFilm, 4901.JP Reports Q1 Net ¥43.8B v ¥12.1B y/y; Op ¥35.8B v ¥29.5B y/y; Rev ¥571.5B v ¥545.9B y/y; +7.5%

Australia

NRW Holdings, NWH.AU Announces 36.8M share purchase plan for existing shareholders at A$0.68/shr to raise A$25M towards the acquisition of Golding Group Pty Ltd; +30%

Domino’s Pizza Entertainment, DMP.AU Reports FY17 Underlying net A$118.5M v A$122Me; EBITDA A$230.9M v A$237Me; Rev A$1.07B v A$1.1Be; Announces A$300M buyback; -14%