Sample Category Title

RBA Talks Down AUD, But The Currency Doesn’t Obey

The RBA kept its policy unchanged today, as was widely anticipated. The statement accompanying the decision contained few surprises, with the Bank appearing content with the strong employment growth over recent months, but maintaining its concerns regarding subdued wage growth. Perhaps the most noteworthy point was that policymakers expressed their discomfort with the latest AUD appreciation. They noted that the higher exchange rate is expected to contribute to subdued prices, and that it is weighing on the outlook for growth and employment.

AUD/USD traded somewhat lower following the RBA decision. Nevertheless, the decline triggered fresh buy orders near the round figure of 0.8000 (S1) and then it recovered all the meeting-related losses. Given that the Bank's attempt to jawbone the currency appeared unsuccessful, we maintain our view that the outlook for AUD remains positive, at least in the short-term. We expect the bulls to remain in the driver's seat and perhaps challenge once again the 0.8070 (R1) resistance, marked by the peak of the 27th of July. A break above that level would confirm a forthcoming higher high and may open the way for our next resistance hurdle of 0.8160 (R2).

As for the bigger picture, we stick to our guns that as long as the rate continues to trade above 0.7800, the upper bound of the long-term wide sideways range that had been containing the price action since the 2nd of March, the broader outlook remains positive as well. In addition, there is little on the Australian economic calendar over the next couple of weeks that could change the sentiment currently surrounding the Aussie. The next major market mover for AUD may be the wage growth data for Q2, due out in mid-August, as they may determine whether the RBA will turn hawkish anytime soon.

USD retreat in full swing as White House turmoil escalates

The US dollar came under renewed selling interest yesterday, particularly against the euro and sterling. End-of-month portfolio rebalancing flows and the latest turmoil at the White House may have been the drivers of the greenback's retreat. In an unexpected turn of events, President Trump fired his communications director, Anthony Scaramucci, just ten days after appointing him. Combined with the replacement of the President's Chief of Staff a few days ago, this frequent recycling of key White House figures likely enhanced speculation that the fiscal-reform promises of the US administration may be further delayed, or perhaps completely derailed. We should also note that there have been media reports recently suggesting Trump's influential Secretary of State, Rex Tillerson, is considering to quit. Bearing all these in mind, we think that the dollar could continue to underperform for a while, amid these political uncertainties and subdued expectations for another Fed hike this year.

EUR/USD edged north on Monday, breaking above the resistance (now turned into support) barrier of 1.1775 (S1). The move confirms a forthcoming higher high on the 4-hour chart, and keeps bias to the upside, in our view. Even if the pair corrects lower to challenge the 1.1775 (S1) as a support this time, we expect buyers to take charge again soon and perhaps target the 1.1880 (R1) hurdle in the near future. A break above that resistance is possible to open the way for our next obstacle of 1.1980 (R2).

Today's highlights:

During the European morning, the UK manufacturing PMI for July will be in focus. The forecast is for the figure to remain unchanged, in which case the reaction in GBP is likely to remain relatively limited. In Eurozone, the flash preliminary estimate of GDP for Q2 is due out and the forecast is for the bloc's economy to have grown at the same robust pace as previously. We also get Eurozone's final manufacturing PMI for July.

From the US, we get a raft of economic data: The core PCE price index for June, personal income and spending data for the same month, as well as the ISM manufacturing PMI for July. Kicking off with the core PCE index, without a forecast available, we see the case for the yearly rate to have held steady, given that the core CPI rate for the month remained unchanged too. Turning to personal income and spending, expectations are for both figures to have risen at the same pace as previously. Last but not least, the ISM manufacturing PMI for July is expected to decline. We think that the reaction in USD may depend primarily on any surprises in the core PCE as well as personal income rates, given the recent softness in US inflation. However, even if we were to see a positive surprise in these indicators, we would expect any positive reaction in USD to remain relatively short-lived, considering the negative sentiment currently surrounding the currency.

AUD/USD

Support: 0.8000 (S1), 0.7950 (S2), 0.7900 (S3)

Resistance: 0.8070 (R1), 0.8160 (R2), 0.8250 (R3)

EUR/USD

Support: 1.1775 (S1), 1.1710 (S2), 1.1615 (S3)

Resistance: 1.1880 (R1), 1.1980 (R2), 1.2100 (R3)

Trade Idea: GBP/JPY – Buy at 145.55

GBP/JPY - 146.05

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

New strategy :

Buy at 145.55, Target: 147.55, Stop: 144.95

Position: -

Target: -

Stop:-

As sterling found renewed buying interest at 144.85 and has staged a strong rebound, suggesting the retreat from 146.55 has ended there and consolidation with upside bias is seen for another test of this level, above there would signal low has been formed at 144.05 early last week and bring a stronger rebound to 146.90-00 and possibly towards 147.30.

In view of this, we are looking to buy sterling on dips. Below said support at 144.85 would abort and prolong consolidation, risk weakness to 144.45-50 but said support at 144.05 would hold from here, bring recovery later. A break of said support at 144.05 would add credence to our view that a temporary top has been formed at 147.75 earlier last month, bring retracement of recent upmove to 143.50, then towards support at 143.30.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

Daily Technical Analysis: EUR/JPY Bullish W Pattern Marks The Possible Uptrend Continuation

The EUR/JPY has been in a steady uptrend marking a zig zag pattern followed by a huge bullish W pattern. At this point we have a possible continuation and a possible retracement to POC zone 129.95-130.10 (D L4, EMA89, 61.8, ATR pivot, historical buyers, bullish order block). Continuation should happen above 130.59 towards 130.80 and 131.10. In the case of retracement to POC, the price should be rejected towards upper levels. However should the price break below 124.90, traders should watch for 129.77, 129.66 and 129.50.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

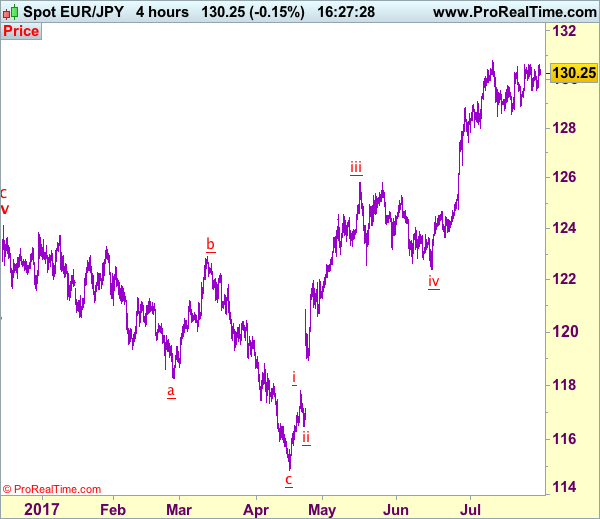

Trade Idea: EUR/JPY – Stand aside

EUR/JPY - 130.39

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Although the single currency has rebounded again after brief pullback and test of recent high of 130.77 cannot be ruled out, break there is needed to confirm recent upmove has resumed and bring further gain to 131.00-10, above there would encourage for headway to 131.50, however, loss of upward momentum should prevent sharp move beyond latter level and reckon 132.00 would hold from here, risk from there is seen for a retreat later.

In view of this, would not chase this move here and would be prudent to stand aside for now. Below 129.95-00 would bring another test of 129.54 support but break there is needed to prolong consolidation below 130.77, bring another corrective fall to 129.20, then 128.90-00, however, reckon downside would be limited and 128.49-57 support should hold, bring another rise later.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Trade Idea: AUD/USD – Hold short entered at 0.8030

AUD/USD – 0.8000

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term up

Original strategy :

Sold at 0.8030, Target: 0.7880, Stop: 0.8090

Position: - Short at 0.8030

Target: - 0.7880

Stop: - 0.8090

New strategy :

Hold short entered at 0.8030, Target: 0.7880, Stop: 0.8090

Position: - Short at 0.8030

Target: - 0.7880

Stop:- 0.8090

Although aussie recovered after finding support at 0.7937 on Friday, as long as last week’s high at 0.8066 holds, further consolidation would be seen with mild downside bias for another retreat, below said support at 0.7937 would add credence to our view that wave iii top is possibly formed at 0.8066, then near term bearishness remains for correction in wave iv to 0.7900, however, reckon previous support at 0.7875-78 would hold and renewed buying interest should emerge there, bring another rise later. Above said resistance at 0.8066 would signal recent upmove is still in progress for headway to 0.8100, then 0.8140-50 but overbought condition should limit upside to 0.8190-00, bring retreat later. We are keeping our latest bullish count that recent impulsive waves is unfolding as (1 2, (i)(ii), i ii) and may extend headway to aforesaid upside targets.

In view of this, we are holding on to our short position entered at 0.8030. A sustained breach below support at 0.7875 would defer and risk correction to 0.7810-20, however, still reckon downside would be limited to 0.7786 and price should stay well above wave i top at 0.7712.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

EURGBP Remains Neutral As Consolidation Phase Extends

EURGBP remains neutral as consolidation continues on the 4-hour chart since the pullback from the high of 0.8994 that was hit on July 21.

The shorter-term 20-period moving average (MA), currently at 0.8941, is providing immediate support.

The bullish breakout from 0.8860 on July 20 (top of a recent range), coincided with the bullish crossover of the 20-period MA with the 50-period one. The 20-period MA has stopped rising and has turned horizontal, while RSI is moving sideways, suggesting that consolidation is likely for EURGBP in the near term.

A move to the downside would find support at the July 27 low of 0.8890. From here, further support is located at 0.8860 and at 0.8760. These are important levels that acted as support and resistance levels in the past.

Looking at the bigger picture, there are no clear signs of a reversal in the slow uptrend that has been taking place since May. In the near term, the market is in a corrective mode, with scope to bounce higher to clear 0.8941 and target the key 0.9000 level which has not been reached since November 2016.

Technical Outlook: EURUSD Broke Above Bull-Channel Upper Trendline, Eyes 1.2000 Barrier

The Euro broke above 1.1800 barrier on Monday's rally and extended larger bull-trend to fresh high at 1.1845, the highest since Jan 2015. The single currency ended month in firm bullish mode, marking the fifth consecutive bullish month and the biggest monthly gains since Mar 2016 and confirming strong bullish stance.

The price action on Tuesday is consolidating within narrow range, holding above 1.1800 handle, now reverted to support and reinforced by broken bull-trendline (former bull-channel upper boundary) and broken 200SMA, which marks solid support.

The wave C, on which the price is currently riding (commenced from 1.1312 trough), met its FE161.8% target at 1.1845 and could extend towards FE 200% at 1.1975 and psychological 1.2000 barrier, where falling thick monthly cloud could limit rally.

Bulls so far ignore strongly overbought studies on daily/weekly charts, however, corrective action should be anticipated. Strong uptrend favors dip-buying strategy, with corrective pullbacks below 1.1800 handle to face support at 1.1693 (rising 10SMA) and expected to hold above ascending 20SMA (currently at 1.1563).

Res: 1.1845, 1.1896, 1.1950, 1.1975

Sup: 1.1800, 1.1776, 1.1723, 1.1693

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

What started as a dull Monday, ended up with the EUR/USD pair reaching a fresh 2017 high of 1.1831, level last seen early January 2015, as mixed US data was not enough to revert the prevailing negative sentiment towards the American currency. The greenback advanced modestly before changing course, holding on to modest gains only against the CAD, undermined by a retracement in oil prices. As for the EUR/USD pair, it settled above the 1.1800 level, helped by a slightly improvement in European inflation according to July preliminary estimates released this Monday. Cope CPI is estimated to have risen by 1.2% yearly basis, beating expectations of 1.1%. Headline inflation remained steady at 1.3%. In Germany, retail sales were up 1.1% in June, above the 0.5% expected, although the annual reading came in at 1.5%, well below market's forecast of 2.7%. In the US, the Chicago PMI fell to 58.9 in July from 65.7 in June, the lowest level in three months, whilst the Dallas index surged to 16.8 from previous 15.0. Pending home sales surged by 1.5% in June, better-than-expected, although low inventories persist, holding back activity.

The macroeconomic calendar will remain quite busy all through the week, with final July PMIs and Q2 GDP for the EU being released early Tuesday, followed by US Personal Income and Spending figures, including PCE inflation, Fed's favorite measure when it comes to take decisions.

From a technical point of view, the EUR/USD pair has reached the top of the daily ascendant channel that led the way since mid April, unable to break it but pressuring it ahead of the Asian opening, signaling a possible upward acceleration on a break above it during the upcoming sessions. In the 4 hours chart, the price has met buying interest on a slide down to a bullish 20 SMA, whilst the Momentum indicator maintains its strong upward slope near overbought levels, whilst the RSI indicator hovers around 70, all of which favors the upside. The immediate resistance is now 1.1845, January 14th 2015 high, followed by the 1.1870 price zone, where the pair presents multiple daily highs and lows from earlier that month. Further gains, particularly if US upcoming data remain soft can see the rally extending up to 1.2101, the high for the mentioned month.

Support levels: 1.1780 1.1750 1.1715

Resistance levels 1.1845 1.1870 1.1910

USD/JPY

The USD/JPY pair extended its July's decline to 110.30 and settled around 110.40, down for a second consecutive day, as escalating tensions between North Korea and the US over the weekend fueled demand for the safe-haven currency at the beginning of the day, while mixed US data kept the greenback subdued in the American afternoon. Japanese industrial production bounced back in June, up by 1.6%, slightly below market's expectations of 1.7%, but well above May's 3.6% decline. Additionally, housing starts surged by 1.7% in June, while orders rose by 2.3%, although the news had little effect on the yen. During the upcoming Asian session, attention will focus on the Nikkei manufacturing PMI, expected unchanged at 52.2. The pair maintains a clear bearish stance intraday, as in the 4 hours chart, the price is further below its 100 and 200 SMAs, with the shortest about to cross below the larger, and technical indicators maintaining strong bearish slopes near oversold readings ahead of the Asian opening. Below the mentioned daily low, the pair has scope to extend its decline towards the 109.80/90 price zone, with a break lower opening doors for a steeper slide towards 108.80, June's monthly low.

Support levels: 110.30 109.85 109.40

Resistance levels: 110.80 111.20 111.60

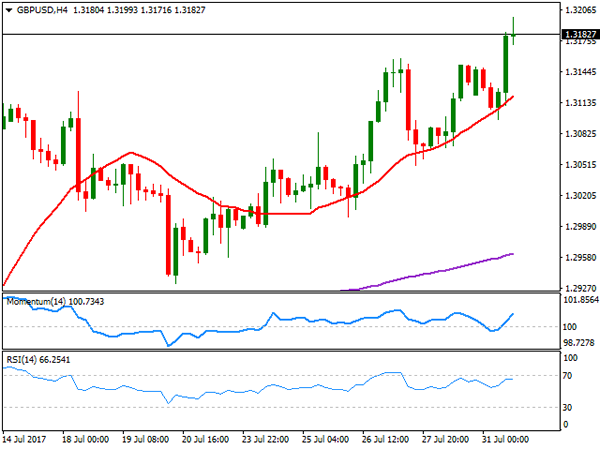

GBP/USD

The GBP/USD pair surged to 1.3199, its highest since September last year, ending the day a few pips below the level, on the back of persistent dollar's weakness. In the UK, mortgage approvals were the lowest in nine months in June according to official money figures, with 64,684 approvals in June, down from 65,109 in May. Consumer credit growth fell modestly, with the annual rate of growth at 10% from 10.4% in the previous month. The report also showed that non-mortgage lending to consumers dropped from £1.8 billion in May to £1.5 billion in the same month. The Markit manufacturing PMI for July in the kingdom to be released this Tuesday is expected at 54.3, although the most relevant event for the week will be the BOE's monetary policy meeting on Thursday, which will bring fresh economic outlooks. From a technical point of view, the 4 hours chart shows that the bullish tone persists ahead of the Asia opening, with the price holding above a bullish 20 SMA and the Momentum indicator heading north above its 100 level, whilst the RSI consolidates around 66, rather reflecting the low volume at this time of the day than suggesting upward exhaustion.

Support levels: 1.3100 1.3060 1.3020

Resistance levels: 1.3160 1.3200 1.3250

GOLD

Spot gold settled at $1,268.32 a troy ounce, marginally lower daily basis, despite a peak of risk aversion at the beginning of the day and dollar's broad weakness. The commodity held near its recent highs, in fact advancing by a few cents, to a fresh July high of 1,270.97, but was unable to extend its rally, most likely retreating on profit taking at the last day of the month. From a technical point of view, the daily chart shows that technical indicators are retreating modestly, still within overbought territory, but the price remains well above all of its moving averages, while sentiment favor the upside, suggesting that any downward corrective movement will likely be corrective. In the shorter term, and according to the 4 hours chart, gold is biased higher, as the price remains well above a bullish 20 SMA, now the immediate support at 1,264.00, whilst the Momentum indicator heads north above its 100 level and the RSI indicator consolidates around 65, in line with additional gains, particularly on an advance beyond 1,271.10, the immediate resistance.

Support levels: 1,264.00 1,254.75 1,245.20

Resistance levels: 1,271.10 1,283.30 1,290.10

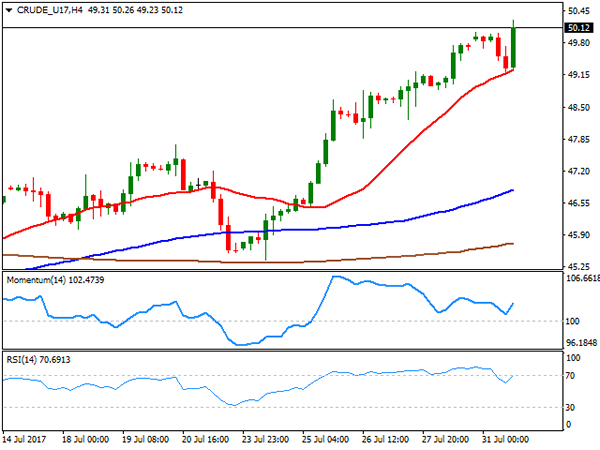

WTI CRUDE OIL

Crude oil prices continued advancing in the last trading day of the month, with West Texas Intermediate crude futures settling at $50.13 a barrel after reaching a high of 50.26. The US benchmark posted its largest monthly gains for this year, holding at its highest in over eight weeks, as tensions in Venezuela and possible sanctions to the country from the US could result in a shortage of heavy oil for US refineries, somehow helping balancing the market. On the negative side, Reuters reported that OPEC oil output has risen this month by 90,000 barrels per day to a 2017 high, while in the US crude oil production rose 59,000 bpd in May to 9.169M bpd vs. revised 9.11M bpd in April. The commodity bounced from a daily low of 49.17 ahead of the close, and the daily chart shows that the price is surpassing its 200 DMA by a few cents, whilst technical indicators have lost upward strength, the Momentum easing, but the RSI holding near overbought levels. In the 4 hours chart, the price found support at a bullish 20 SMA, currently at 49.35, whilst the RSI indicator hovers around 70, but the Momentum lost upward strength, still diverging from price's action.

Support levels: 49.90 49.35 48.80

Resistance levels: 50.20 50.85 52.40

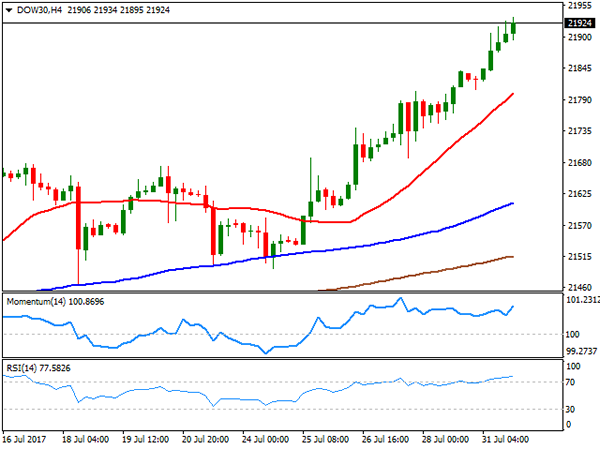

DJIA

Wall Street closed mixed, with the Dow Jones closing at an all-time high of 21,891.12 after adding 60 points. The Nasdaq Composite lost 0.42%, to 6.348.12, while the S&P lost 0.07%, and ended at 2,470.30. The indexes, however, posted monthly gains with the Dow up for fourth consecutive month. Home Depot was the best performer, up 1.03%, followed by Chevron that added 0.99%. El du Pont led decliners with a 2.11% loss, followed by Apple that shed 0.52%. The daily chart for the index shows that it stands near its daily high, and with scope to continue advancing according to the Momentum indicator, holding within positive territory. The RSI in the mentioned chart heads north around 73, while the index remains above all of its moving averages, further supporting gains ahead. In the 4 hours chart, technical indicators extended their advances within overbought levels, whilst the 20 SMA extended its advance below the current level, in line with further gains ahead.

Support levels: 21,814 21,766 21,718

Resistance levels: 21,900 21,945 21,990

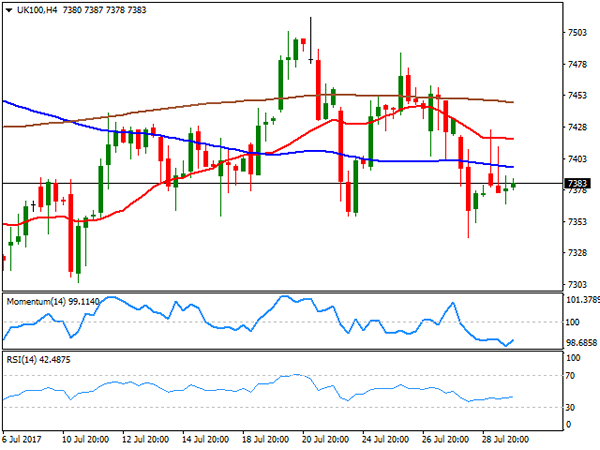

FTSE100

The FTSE 100 managed to hold in the green, despite most European indexes closed lower, lifted by mining-related equities. The London benchmark added 3 points or 0.05% to end at 7,372.00, up for the month by 0.8%. An advance in mining-related equities, and a strong earnings report from HSBC bolstered the index, as the company posted a 5% increase in profits. Utilities were the best performers across the region, after RBC lifted the rating of Seven Trent, up 4.09% and United Utilities that added 2.98%, to "outperform." Leading losers' list were tobacco companies, still pressured by Friday's US FDA announcement on reducing nicotine levels. Imperial Brands lost 5.90%, while British American Tobacco closed 4.97% lower. The daily chart for the index shows that it holds around a flat 100 DMA, while technical indicators hover around their mid-lines, lacking directional strength. In the 4 hours chart, the index remains below all of its moving averages that anyway lack directional strength, whilst indicators aim modestly higher well below their mid-lines, far from suggesting an upward movement ahead.

Support levels: 7,340 7,294 7,257

Resistance levels: 7,398 7,434 7,587

DAX

European equities closed mostly lower in the last trading day of July, losing ground ahead of the close. The German DAX settled at 12,118.25, down 44 points, weighed by EUR's strength, as the common currency reached a fresh 2017 beyond the 1.1800 figure. In June, the index lost 1.7%, mostly due to the sharp appreciation of the local currency, which added 5 cents against the greenback in the same period. Utilities led the way higher, with RWE AG up 1.53% and E.ON up 1.39%. Deutsche Bank led the way lower, losing 2.15%, while the automotive sector remained under pressure, with Volkswagen closing down 1.04% and Daimler shedding 0.86%. The daily chart shows that DAX remains near its lowest since late May, and poised to extend its decline, as technical indicators extended their declines within bearish territory, now nearing oversold territory, whist the 20 DMA extends below the 100 DMA. In the 4 hours chart, the index is also biased lower, with an early advance contained by a bearish 20 SMA, and technical indicators also heading south near oversold readings.

Support levels: 12,085 12,041 12,003

Resistance levels: 12,143 12,199 12,235

Elliott Wave Analysis: Aussie And Its Bullish Scenario

AUDUSD is trading bullish since start of May, which gives us an idea that the bigger complex correction within blue wave B is completed. As such we may say that blue wave C of IV is now in motion, as viewed on the daily chart and it may reach levels near the former swing low at 0.8161 level, before make a new turning point lower.

AUDUSD, Daily

Below we have a 4h chart of AUDUSD, which shows us a nice bigger impulse in motion as part of blue wave C. We can see that waves 1) and 2) are already completed and the largest and steepest wave 3) is also showing some signs of a completion near the 0.8054 region. Well, if that is the case, then a new temporary correction into the following red wave 4) may follow in days ahead and later search for some support around the former black wave 4 and near the Fibonacci ratio of 38.2, where price can again bounce into final wave 5).

AUDUSD, 4H

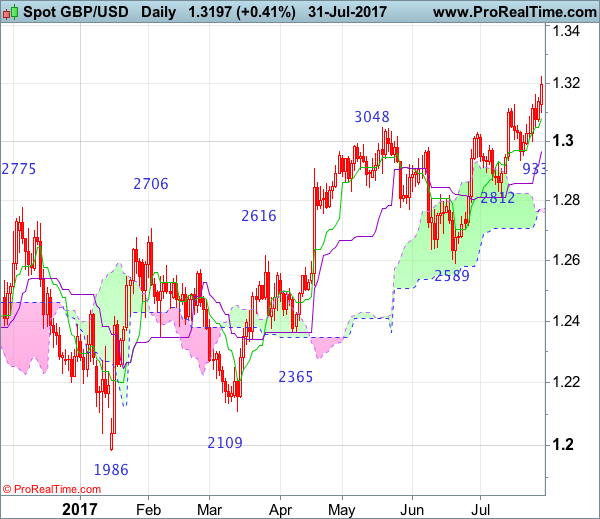

GBP/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 16 Jan 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 18 Apr 2017

• Trend bias: Near term up

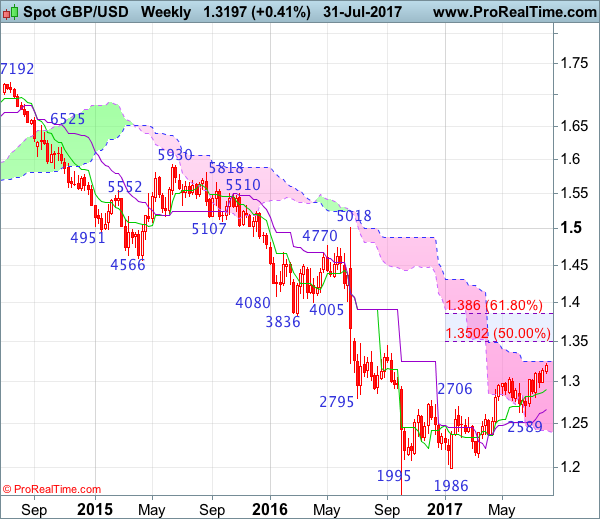

GBP/USD – 1.3193

Cable found renewed buying interest at 1.2933 and has resumed recent upmove, dampening our near term bearishness and upside risk remains for medium term rise from 1.1986 low to extend further gain to 1.3245-50 (61.8% projection of 1.1986-1.3048 measuring from 1.2589) and possibly 1.3300-10, however, near term overbought condition should prevent sharp move beyond resistance at 1.3425 and price should falter well below 1.3500-05 (50% Fibonacci retracement of 1.5018-1.1986), risk from there is seen for a retreat later.

On the downside, whilst pullback to 1.3095-00 cannot be ruled out, reckon the Tenkan-Sen (now at 1.3067) would hold and bring another rise later to aforesaid upside targets. Below 1.2950-55 would defer and risk test of support at 1.2999, then towards the Kijun-Sen (now at 1.2953), however, only a sustained breach below support at 1.2933 would abort and signal a temporary top is formed instead, bring retracement of recent upmove to 1.2890, then towards previous support at 1.2812 which is expected to contain downside.

Recommendation: Stand aside for this week.

On the weekly chart, the British pound has risen again after brief pullback just below 1.3000 level and the breach of resistance at 1.3126 signals the medium term rise from 1.1986 low is still in progress, hence upside bias is seen for this move to extend further gain to the upper Kumo (now at 1.3247), then 1.3300-10, however, near term overbought condition should limit upside to previous resistance at 1.3425 and reckon 1.3500-05 (50% Fibonacci retracement of 1.5018-1.1986) would hold, price should falter below 1.3670-75, bring another decline in Q4.

On the downside, although initial pullback to 1.3095-00 is likely, reckon downside would be limited to 1.3050-55 and said support at 1.2999 should hold, bring another rise later. A weekly close below 1.2999 would suggest a temporary top is possibly formed, bring test of 1.2933 support, break there would add credence to this view, then retracement of recent rise to the Tenkan-Sen (now at 1.2895) and later 1.2812 support would follow, however, downside would be limited to 1.2700-10 and price should stay well above support at 1.2589, bring a rebound later.