Sample Category Title

EURJPY Neutral After Uptrend, Maintains Bullish Bias Above 130

EURJPY is neutral on the 4-hour chart and has been consolidating around the key psychological level at 130.00. After hitting a more-than one-year high of 130.76 on July 11, there was a slight pullback in prices since the market reached overbought conditions, as was indicated by the RSI rising to 70.

Upside momentum has weakened and a neutral phase is expected in the near term. Any corrective move lower would likely find support at 130.00. This is considered to be an important level since it has held as support in the past couple of days. Further weakness below this level may see EURJPY slip towards 128.57 (July 19 low). A fall from here would start to increase downside pressure as the market would be below the Ichimoku cloud. A break from here would target 127.43 (June 30 low).

Looking at the bigger picture, the uptrend that started from the June 15 low of 122.39 to the July 11 high of 130.76 is still intact. There are no signs of a reversal in the uptrend yet. The risk is to the upside based on the bullish market structure on the daily chart. The Tenkan-sen line is above the Kijun-sen line and the market is above the Ichimoku cloud. Meanwhile, RSI remains above 50 in bullish territory.

A successful break above the 130.76 high would open the way towards the next significant high of 132.00 that was reached in January 2016. Such a move would strengthen the medium-term bullish bias.

Technical Outlook: EURUSD – Bulls Are Consolidating Under Weekly 200SMA At 1.1795

The Euro is consolidating under fresh high at 1.1776 posted in Asia, in extension of Wednesday's strong post-Fed rally. The pair is trading at levels last seen in Jan 2015 and looks for clear break above pivotal 1.1735 barrier (Fibo 38.2% of 1.3992/1.0340 descend) to trigger fresh acceleration higher.

The single currency is driven higher by weak dollar which fell further after wording of Fed's statement sent signals that the US central bank might not hike interest rates again this year.

On the other side, technical studies are strongly overbought on larger timeframes, suggesting that bulls might take a breather. Bearish divergence on daily chart slow stochastic is supporting the notion.

The pair faced headwinds ahead of next strong barrier at 1.1795 (weekly 200SMA), which may temporarily cap the action.

Today's close in red would be seen as initial negative signal. First good supports lay at 1.1620 zone (daily higher base, reinforced by rising 10SMA) with key near-term support laying at 1.1525/00 (Fibo 38.2% of the upleg from 1.1188 to 1.1776, reinforced by rising 20SMA) which is expected to contain extended dips.

Otherwise, break and close above 1.1795 pivot would signal bullish continuation and open was towards psychological 1.2000 resistance (also monthly cloud base).

Res: 1.1776, 1.1795, 1.1848, 1.1896

Sup: 1.1681, 1.1620, 1.1583, 1.1525

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD had a bullish momentum yesterday, topped at 1.1739 and hit 1.1747 earlier today in Asian session. The bearish pin bar scenario I showed you yesterday is no longer valid. My bullish mode is now reactivated. The bias is bullish in nearest term testing 1.1750 – 1.1875 area. Immediate support is seen around 1.1700. A clear break below that area could lead price to neutral zone in nearest term testing 1.1640 – 1.1580 support area which is a good place to buy with a tight stop loss. On the upside, a clear break above 1.1875 would expose 1.2000 region.

GBPUSD

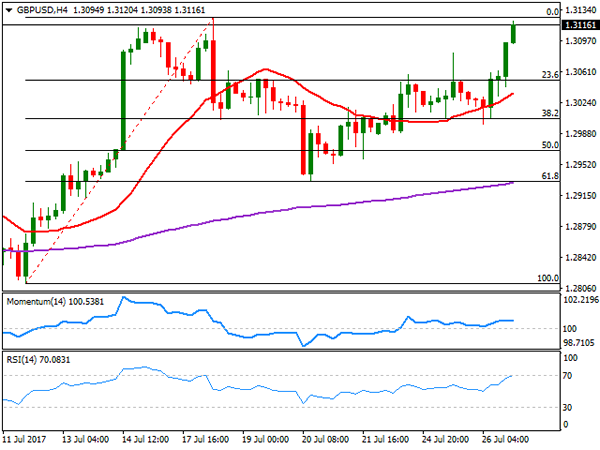

The GBPUSD had a strong bullish momentum yesterday, broke above 1.3100 key resistance and hit 1.3149 earlier today in Asian session. This fact cancels the bearish pin bar scenario and activates my bullish mode. The bias is bullish in nearest term testing 1.3200 before targeting 1.3350 region. Immediate support is seen around 1.3100. A clear break below that area could lead price to neutral zone in nearest term testing 1.3050 – 1.3000 support area which is a good place to buy with a tight stop loss

USDJPY

The USDJPY failed to continue its bullish momentum yesterday bottomed at 111.06 and hit 110.87 earlier today in Asian session. As long as stay above 110.61 the bullish pin bar scenario should remain valid but the bias is bearish in nearest term. A clear break below 110.61 would expose 110.25/00 area before revisit the trend line support as you can see on my daily chart below, which is a good place to buy. Immediate resistance is seen around 111.45. A clear break back above that area could lead price to neutral zone in nearest term testing 112.00 region. Overall I remain neutral.

USDCHF

The USDCHF attempted to push higher yesterday topped at 0.9595 but whipsawed to the downside and closed lower at 0.9506. We have another bearish pin bar as you can see on my daily chart below suggests a bearish view. The bias is bearish in nearest term testing 0.9450 key support. A clear break below that area could trigger further bearish pressure testing 0.9250 area. Immediate resistance is seen around 0.9550. A clear break above that area could lead price to neutral zone in nearest term but overall I remain bearish and any upside pullback should be seen as a good opportunity to sell.

Dollar Bruised By Fed Caution

The Dollar tumbled to fresh 13-month lows against a basket of currencies during early trading on Thursday, after July's Federal Reserve policy statement was presented with a dovish touch. Although the central bank signaled that it would begin shrinking its massive holding of bonds "relatively soon", the concerns over inflation remaining "somewhat below 2%" in the near term simply stole the spotlight. With weakness in inflation presenting a risk to the Federal Reserve's hiking cycle and weighing on the prospects for further interest rate hikes, the Greenback remains vulnerable to steeper losses.

As the Dollar wallows at 13-month lows, investors may direct their attention towards a duo of economic reports later today which could offer further insight into the health of the U.S economy. The U.S Core Durable Goods Order figures will be in focus, with markets expecting a 0.4% m/m print for June, while unemployment claims are expected to hit 241k for the week ended July 22. With the Greenback struggling to nurse its deep wounds, further downside may be on the cards if Core Durable Goods and unemployment claims fail to meet expectations.

From a technical standpoint, the Dollar Index remains heavily bearish on the daily charts as there have been consistently lower lows and lower highs. Bearish investors who were itching for an opportunity to attack prices further, received encouragement in the form of lagging inflation concerns and this was represented in price action on Wednesday. With the currency becoming increasingly sensitive to monetary policy speculations and markets now pricing in a 46.8% probability of a 25 basis point rate hike in December, price weakness is likely to remain a recurrent theme.

Commodity Spotlight – Gold

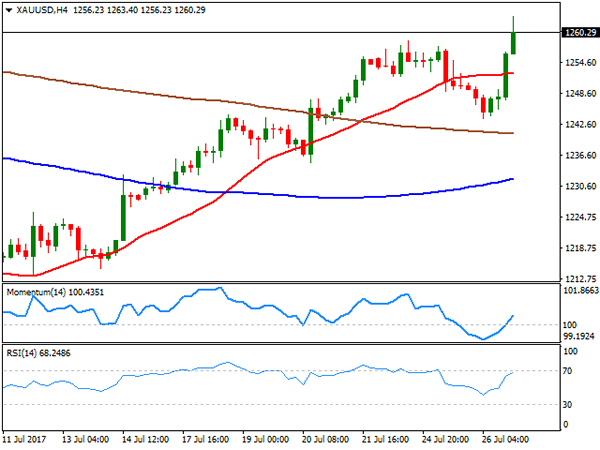

Gold sprinted to a fresh 6-week high above $1260 during late trading on Wednesday, after the Federal Reserve's cautious inflation assessment in July's policy statement weighed on prospects for higher US interest rates. The upside was complimented by a sharply depreciating US Dollar which created a solid foundation for bulls to install fresh rounds of buying. With the zero-yielding metal notoriously known for being dictated by US rate hike expectations, there is a strong possibility of prices marching higher if speculations of the Federal Reserve taking action this year decline even further.

Gold bulls may find further support in the form of Brexit related uncertainty and political risk in Washington that continue to drive the flight to safety in the background. From a technical standpoint, a decisive breakout and daily close above $1260 should encourage a further appreciation higher towards $1268.

EURUSD Bull Run Expected To Remain Intact After Hitting 2½-Year High

EURUSD advanced to its highest level since January 2015 today, hitting 1.1776. The bullish trend was strengthened after prices broke out of a range following a period of consolidation around the key psychological level of 1.1400.

The pair is expected to trend higher as the technical picture is strongly bullish following a crossover of the 50-day moving average above the 200-day moving average on May 23. The 50-day MA continues to point north. Meanwhile, the market is above the daily Ichimoku cloud and the Tenkan-sen and Kijun-sen lines are positively aligned. RSI is trending higher although the indicator has entered overbought territory above 70. This would raise caution for a possible consolidation in EURUSD in the near term.

A decline in prices would find support at the key 1.1600 level. This area has already proven to be strong support in the past few days as drops in prices remained above this level. A break below this would increase downside pressure to target 1.1400.

The overall trend structure and momentum does not favor a very deep retracement and the bull run is expected to remain intact, with scope to rise towards 1.2000. In the meantime, ahead of this, the round level of 1.1800 would be an important barrier to the upside, which if cleared would open the way to the January 2015 high of 1.1870.

Gold Bullish Bias, Hits 1½-Month High

Gold has been advancing it today's trading, hitting a near one-and-a-half-month high of 1264.79.

The RSI is comfortably in bullish territory at 63 and keeps heading higher, indicating that momentum in the very short-term is positive. The overall bias is also to the upside as the MACD is positive and above the red signal line.

If the price continues climbing, the area around the 1270 handle, a rather congested one in the recent past, could provide resistance. Further up, the June 6 eight-and-a-half-month high of 1295.97 would be eyed for additional resistance.

On the downside, the area around the 1255 handle and current level of the 50-day moving average (MA) at 1250.13 could offer support. The region around 1255 has also been a congested one recently. Further declines would shift the focus to the 200-day MA at 1230.05 for additional support.

Regarding the medium-term outlook, given the considerable sideways movement over the last number of months, it looks predominantly neutral though with a bullish tilt after the recent crossing of the price above both the 50- and 200-day MAs.

Overall, the precious metal looks bullish in the short-term and mostly neutral in the medium-term.

Fed’s Inflation Concern Weakens Dollar, Aussie, Kiwi At Two-Year High

It was a relatively quiet data day in forex markets prompting traders to dwell over yesterday's events, namely the Federal Open Market Committee (FOMC) meeting. As a result of the Federal Reserve's dovish tone, the weakness in the US dollar unfolded, with the dollar index hitting a fresh 13-month low. The Australian and New Zealand dollars jumped to two-year highs as traders sold off the greenback.

The Fed confirmed market anticipations of the federal funds rate remaining at the same target range of 1%-1.25% last night. Also, investors got a nod from the FOMC meeting on the reduction of the Fed's balance sheet that will start “relatively soon”. However, the change in the US central bank's tone on inflation, specifically expressing less confidence on the recent weakness in inflation being just temporary, induced a sell-off in the dollar. Dollar/yen slipped below the 111 level during Asian trading but managed to slightly recover to just above the 111 mark as European traders were starting the day. Later in the day, markets will be monitoring monthly orders of durable goods in June, which could impact the dollar significantly.

The Australian and New Zealand dollars hit a two-year high against their US counterpart with the aussie last trading at $0.8039 and the kiwi at $0.7536. The surge in the aussie comes after the currency initially plunged against the greenback on softer than expected inflation data yesterday morning.

The euro continued yesterday's rally on the back of the soft dollar, hitting a fresh high of $1.1776, a position it last held in January 2015. As the Asian session was about to close, the euro retraced some of its earlier gains and was last broadly flat at 1.1730. At 10.8, the Gfk German Consumer Climate index came in above expectations and the prior month's value of 10.6. The euro rose on the news, however the gains didn't last long as the single currency fell soon after.

Sterling continued strengthening against the dollar, with pound/dollar last trading at 1.3141 as the European session was about to start. The uptrend in the pair came despite strong dissatisfaction among Britain's car producers, as they start to feel the strains of Brexit. The number of cars made in the UK in June fell by almost 14% year-on-year to 136,901. Car manufacturers are seeking more clarity from the UK government on its plans for the sector once the country departs the EU. More than half of the cars exported from the UK go to the EU, while domestic demand for cars has weakened in the first half of the year.

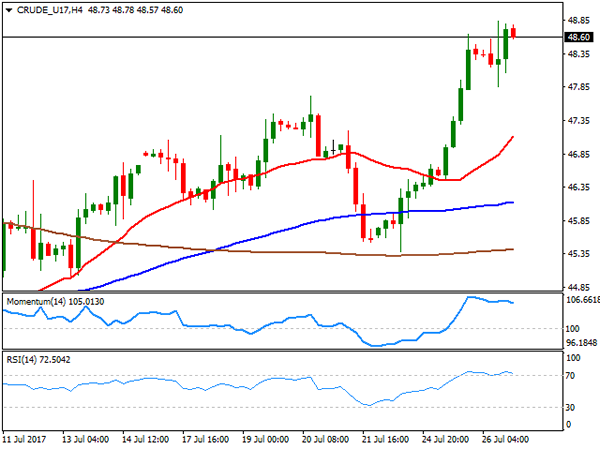

Oil prices rose supported by news that US stockpiles decreased more than expected. At 7.2 million barrels, crude oil inventories fell more than analysts' forecasts of 2.62 million barrels, the Energy Information Administration (EIA) said yesterday. WTI was last up 0.3% at $48.88 a barrel and Brent was at $51.11.

Gold continued strengthening following yesterday's jump on the softness in the US dollar. The precious metal was last trading at $1,261.36 an ounce.

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The EUR/USD pair traded uneventfully around the 1.1640 level, and after falling down to 1.1612, its lowest for the week, but resumed its advance breaking higher and settling at its highest since January 2015, in the 1.1730 region, following the US Federal Reserve monetary policy meeting. The Central Bank failed to surprise investors, keeping rates unchanged, as largely expected and barely changing the wording on the statement, particularly when it comes to reducing the $4.5 billion balance sheet, saying that it will start "relatively soon," and the market understanding it as September. As for inflation, policy makers still believe that it will “stabilize around the Committee’s 2% objective over the medium term," while the labor market has continued to strengthen. With no signs of accelerating its tightening pace, the market resumed dollar's selling, with the greenback now trading near its recent multi-month lows against most of its major rivals.

As for the EUR/USD pair technical outlook, the price has regained ground above its 20 SMA in the 4 hours chart, whilst technical indicators turned sharply higher, maintaining their upward slopes within positive territory, and supporting further gains ahead on a break above the 1.1710 price zone, where the pair topped this week and back in 2015. Beyond the level, the rally could extend up to the 1.1800 price zone, where the pair has its 200 SMA in the weekly chart, and the top of the daily ascendant channel coming from mid-April with little in the way. A reversal in the ongoing bullish trend has become more unlikely, but intraday downward corrective movements can't be disregarded. Still, the pair will remain bullish even in the case of a decline down to 1.1580.

Support levels: 1.1690 1.1650 1.1615

Resistance levels 1.1745 1.1790 1.1840

USD/JPY

The USD/JPY pair fell down to 111.05, down after flirting with levels above 112.00 ahead of Fed's statement. As the US Central Bank failed to surprise, market players resumed dollar's selling, with Treasury yields coming back under pressure. By the end of the US session, the yield on the benchmark 10-year Treasury note slipped to 2.28% from previous 2.33%, while the yield on the 30-year Treasury bond was down to 2.90% from 2.91%. The Japanese calendar had little to offer on Wednesday, and will remain light this Thursday, which means that the pair will keep taking clues from yields and stocks. The decline is being limited by Wall Street's gains, but the risk is clearly towards the downside, although an extension below 110.90 is required to confirm so. The 4 hours chart shows that the pair faltered around its 200 SMA, while the 100 SMA turned modestly lower above the largest, and technical indicators head sharply lower, with the RSI indicator already at 42, supporting the bearish case.

Support levels: 110.90 110.60 110.25

Resistance levels: 111.60 112.00 112.45

GBP/USD

The GBP/USD pair settles above the 1.3100, its highest for the week, compliments to a neutral Fed monetary policy statement. The pair recovered from a daily low of 1.2998, achieved early London. UK data released this Wednesday failed to boost the Pound as the preliminary Q2 GDP figures were soft, as expected. The kingdom is estimated to have grew by 0.3% in the three months to June, with the annual rate resulting then at 1.7%. While the figures were in-line with market's forecast, were also supportive of the current on-hold stance of the BOE, cooling further hopes for a rate hike in the UK. After the release, Finance Minister Hammond, said that while the UK can be proud of the continued growth seen over the past four years, they now need to focus on "restoring productivity growth to deliver higher wages and living standards for people across the country." Anyway, gains came as usual on the back of dollar's broad weakness, with the pair now poised to challenge its yearly high, set this July at 1.3125. The 4 hours chart shows that the price has accelerated above a now bullish 20 SMA, whilst the RSI indicator advances around 69, although the Momentum indicator remains flat within positive territory, all of which supports some further gains ahead. A break above the mentioned yearly high exposes the 1.3180 price zone, where the pair has multiple daily highs and lows from August/September 2016.

Support levels: 1.3090 1.3050 1.3010

Resistance levels: 1.3125 1.3180 1.3230

GOLD

Gold prices rallied to settle at their highest in over a month, with spot ending the day at $1,266.20 a troy ounce after trading as high as 1,263.40. The commodity slipped at the beginning of the day amid a cautious stance among investors, and continued demand for high yielding assets, but turned north after the US Central Bank gave relief to dollar bears. Odds for another rate hike this year diminished after this meeting, now closer to 35%, backing the case for further gold gains. The commodity has regained the bullish stance after some consolidation earlier on the week, as the daily chart shows that the price settled above its 100 DMA, while technical indicators resumed their advances, and stand at fresh monthly highs with strong upward slopes. In the shorter term, and according to the 4 hours chart, the bright metal is also biased higher, as technical indicators re-entered positive territory, heading higher early Asian session, and with the price back above all of its moving averages.

Support levels: 1,258.80 1,245.20 1,236.30

Resistance levels: 1,266.60 1,274.10 1,283.30

WTI CRUDE OIL

Crude oil prices extended their recent rallies on the back of fresh market news, with West Texas Intermediate futures up to $48.84 a barrel intraday, its highest since early June, after the EIA weekly report showed a surprise draw-down in US stocks. According to the report, domestic crude supplies fell by 7.2 million barrels for the week ended July 21, well beyond the 2.6 million barrels' decline expected. WTI closed the day barely below that high at 48.60, maintaining the positive tone according to technical readings, as in the daily chart, the price bounced from its 100 DMA, now a strong dynamic support at 47.86, whilst technical indicators have lost upward strength near overbought levels, but are far from indicating a downward move ahead. In the 4 hours chart, technical indicators are currently consolidating within overbought readings, whilst the price stands far above all of its moving averages. Unless the market offers a negative surprise, WTI can extend up to the 50.00 level during the upcoming sessions, but gains beyond this last are still seen limited.

Support levels: 47.84 47.20 46.60

Resistance levels: 48.80 49.50 50.10

DJIA

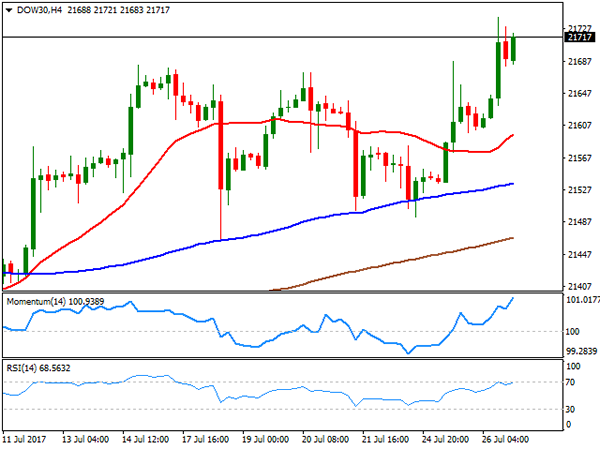

Wall Street had a stellar performance this Wednesday with the three major indexes closing at all-time highs. The Dow Jones Industrial Average added 97 points, and settled at 21,711.01, while the Nasdaq Composite gained 0.16%, to 6,442.75. The S&P was up barely 0.03%, to close at 2,477.83. US stocks rallied ahead of the opening, on the back of strong earnings, retreating ahead of the Fed, but resuming their advances afterwards. Boeing was the best performer within the Dow, up 9.91%, after reporting per-share earnings of $2.89, well above market's consensus of $2.58. Nike led decliners with a 1.77% loss, followed by McDonald's that shed 1.63%. The daily chart maintains the bullish stance seen on previous updates, with technical indicators extending their advances within positive territory and the benchmark further above bullish moving averages. In the 4 hours chart, the Momentum indicator heads north almost vertically within overbought territory, the RSI also aims higher around 66, whilst the 20 SMA gained upward strength far below the current level, supporting additional gains for this Thursday.

Support levels: 21,681 21,649 21,598

Resistance levels: 21,741 21,785 21,830

FTSE100

The Footsie closed the day in the green at 7,452.32, up 17 points, amid gains in the mining sector, also up after ITV raised its dividend saying its 16% fall in first-half pretax profit was in line with its expectations. The share led advancers with a 2.44% gain, while Anglo American added 2.01%. Paddy Power Betfair was the worst performer, ending the day down 2.95%, followed by Glaxo Smith that shed 2.55%. Pound's strength after London's close pressure the index in electronic trading, now around 7,440 and with the daily chart showing that it retains its positive tone, as it still stands above its 20 and 100 DMAs, both converging around 7,385, whilst the Momentum indicator continues heading higher above its 100 level. The RSI indicator in the mentioned time frame is, however, anticipating a probable bearish extension, having turned flat around 52. In the 4 hours chart, the index struggles around its 20 SMA and below the 200 SMA, while technical indicators lack directional strength, hovering around their mid-lines, and in line with the longer term view.

Support levels: 7,485 7,435 7,390

Resistance levels: 7,482 7,518 7,561

DAX

European equities closed higher this Wednesday, with the German DAX adding 41 points to 12,305.11, as banks remained buoyed, although the advance was moderate ahead of the Fed's monetary policy meeting outcome. Within the German benchmark, Commerzbank was the best performer, adding 2.61%, followed by Volkswagen that gained 1.81%. On the negative side, Merck was the worst performer, ending the day 3.30% lower, followed by Daimler that shed 1.22%. The index fell in after-hours trading, following EUR soaring to fresh 2-year highs, now hovering around 12,260 and with the daily chart showing that the index remains below its 20 and 100 DMAs, with the shortest gaining downward strength around the largest, and ready to break higher, and technical indicators hovering within negative territory, with limited upward momentum, maintaining the risk towards the downside. In the 4 hours chart, a bearish 20 SMA capped the upside, while the Momentum aims higher around 100, but the RSI indicator turned south, currently around 39, supporting a bearish extension ahead.

Support levels: 12,234 12,190 12,153

Resistance levels: 12,303 12,354 12,398

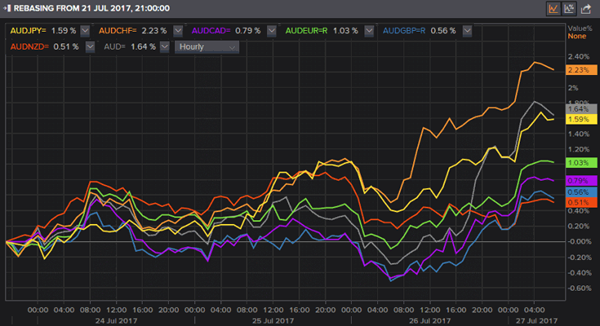

AUD Crosses Break High In Tandem Whilst ASX Remains Stuck In Mud

Only the Swiss Franc has underperformed the USD in relation to AUD this week the 1.9% positive carry takes it to new heights. Whilst ASX continues to frustrate, we lean slightly towards an eventual downside break out of range.

We highlighted this potential trade yesterday and, whilst the downside has indeed begun, thought it worthy of putting it back on your radars as there may be other opportunities to join in. The resistance zone around 1.65 to the monthly S1 perfectly capped yesterday's high and presented a shooting star candle. For those that took the break of yesterday's low or used a sell-limit below 1.65, you're likely in the trade assuming you have not been stopped out. Had the stop been above the monthly S1 then we assume you're still in.

Yesterday's is likely a resistance level which could be used to aid with sell-limit placement. Ideally the stop would be above this level and closer towards 1.65. As the shooting star respected the 8eMA we favour a shallow pullback before the decline continues. The target is around the 1.618 / monthly S1, although we prefer to exit or scale out somewhere above this level.

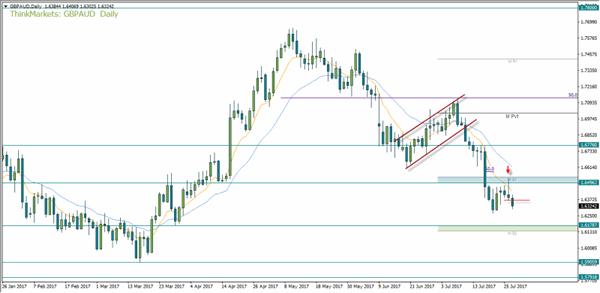

Sentiment on AUD is annoying bullish (to the RBA) and as AUD is outperforming Sterling, GBPAUD is one of your preferred shorts.

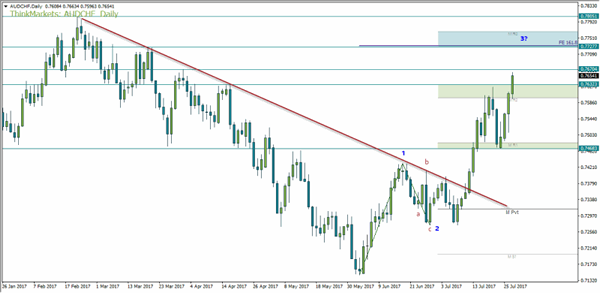

AUDCHF continues to climb higher as AUD takes advantage of the low yielders. Currently on its 5th bullish session we think the move may eventually makes its way up to 0.7727. This area houses the 161.8% projection and March high which may provide an ending for wave 3. As the supposed wave 1-2 was around 50%, it's possible that wave 4 may be shallow (83.2% or higher). Either way momentum favours the bulls and intraday longs are the preferred choice under the current sentiment. If we are to see the rally cool then today's low sits on the monthly R2 which makes it viable support or an area to aid with stop placement.

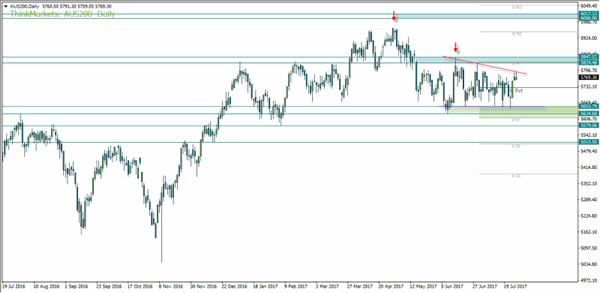

The ASX200 continues to frustrate and has spent the best part of June and July between 5650-5825. The multiple spikes lower which respected 5653.80 initially suggest solid support, yet the lower highs suggest bears have a slight edge which makes the potential for an eventual downside break. Moreover, the June high forms a lower high which failed to test the psychological number of 6000. Therefor our bias is for an eventual downside break.

We really want to see a break below 5625 although a close beneath 5653 could tip us off to such a move. If the bulls are to regain control we would require a break of the red trendline before considering long positions yet, even then, a break of 5825 would be preferred for added confirmation.

AUD On A Tear To RBA’s Despair, 83.40 In Focus

The haevy losses of the USD have undone any efforts from RBA to cap gains with ease, as it breaks milestone after milestone. Technically we could now be headed for 83.40. The haevy losses of the USD have undone any efforts from RBA to cap gains with ease, as it breaks milestone after milestone. Technically we could now be headed for 83.40.

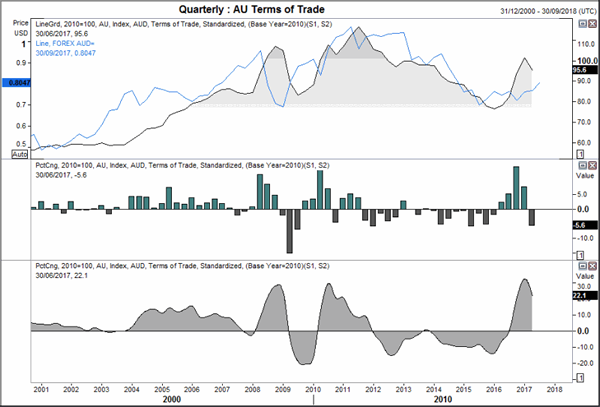

Australia's terms of trade, a measure of export price competitiveness, declined by -5.6% in Q2 to erode some of the 7.6% increase in Q1. This breaks a 4-quarter streak of gains which helped the annual rate move as high as 32.4% in Q1, which has now edged lower to 22.1% YoY.

Export prices were the main culprit as they declined -5.7% QoQ versus +9.4% previously. Imports only declined -0.1% QoQ following a +1.2% gain in Q1. This now brings exports down to 22.5% YoY versus 31.7% previously.

The correlation with the raw terms of trade index compared with the Australian Dollar is strong over the longer-term. They don't always match up in terms of gains on a quarterly basis but the trend is resected. Even with Q2's decline, one could argue that AUD remains below fair value in relation to the terms of trade. If so, then it is another reason the RVA are to be concerned with a rising AUD.

We previously showed the long-term chart for AUD inverted to show the bigger picture. Once flipped upside down the topping pattern appears much clearer when price touched the original neckline. Since breaking above the neckline, the 2016, the 200 wk eMA and now 80c with apparent ease, we think there could be much more upside to come. The milestones it has cut through lie butter are usually levels one would expect to prompt more resistance. And it is this ease of upside breaks alongside the trajectory of the current leg higher which make us think this is the breakout of a large-scale macro move.

If we continue to follow the momentum path of the original leg higher from the 2015 lows, AUD could be headed straight for 0.834. It may find resistance around 0.8466 (2014 high) but we expect it to remain above 80 unless USD can make a quick recovery. If 0.834 is broken then 0.8450 is a viable area for a correction as it marks the 38.2% retracement form the 2015 low to 2011 high.

And this is where the RBA have real issues as they want their currency lower, not higher. We saw the reaction Guy Debelle provided below 80c and we doubt he has changed his mind since. Therefor we must seriously consider the potential for the RBA to cut once more despite fears of further stoking the fire for hot property prices.

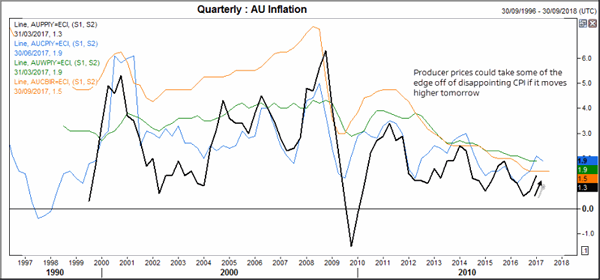

Producer prices will be in focus tomorrow to see if they can throw some support under this week's CPI set. We doubt it will have much of an impact on AUD in the grand scheme of thigs because that is simply hurtling higher due to a great macro unwind of the US Dollar.