Sample Category Title

Pound and Euro Surge on Rising Yields; US Data Lifts Dollar from Doldrums

Risk appetite recovered in European trading on Tuesday as rising government bond yields helped financial stocks, as well as lift the euro and the pound. US treasury yields also moved higher on expectations that the Fed will soon proceed with shrinking its bond portfolio. However, the US dollar was stuck in the doldrums for much of the session as investor caution ahead of the FOMC meeting and political uncertainty weighed on the currency.

The euro surged to a fresh high of $1.1711 today, breaking above the $1.17 level for the first time since August 2015. The single currency was bolstered by a jump in German bund yields, while much stronger-than-expected Ifo data from Germany further supported the euro.

The Ifo's business climate index rose to a record high of 116.0 in July from an upwardly revised 115.2 in June. The figure was well above expectations of a decline to 114.9. The current conditions and expectations indices also both beat forecasts. The Ifo report described German business sentiment as "euphoric", adding that companies were the most satisfied with the current conditions since the country's reunification. The data contrasts with the more disappointing PMI releases from yesterday.

In an additional boost for the euro, the Greek government successfully completed the sale of five-year bonds to private investors - the first since 2014. The sale helped reduce the yield spread between periphery Eurozone government bonds and German bunds.

The pound was also buoyant on Tuesday, advancing to a one-week high of $1.3083. Apart from the weaker dollar, sterling benefited from data from the Confederation of British Industry that showed UK manufacturing output was at its highest since January 1995 in the three months to July, although new orders rose less than expected in July.

The Japanese currency fell back in today's European session as risk sentiment improved but was also under pressure after the Bank of Japan's June meeting minutes revealed that the two new board members who joined the Bank recently argued against an early withdrawal from the stimulus program.

The greenback was unable to find much support from rising US treasury yields, even as the yen experienced broad weakness today. US treasury yields were sharply higher on Tuesday as investors bet that the Fed will signal at its meeting tomorrow the possible start date of its balance sheet reduction. Traders will also be looking to see whether the Fed will be concerned about any persistent weakness in inflation.

Apart from Fed policy, Trump's political woes were at the forefront of investors' minds, and this continued to weigh on the dollar. However, the US currency got a late boost from a surprisingly strong consumer confidence data. The Conference Board's consumer confidence index increased from a downwardly revised 117.3 in June to 121.1 in July, beating expectations of 116.5.

Other data out of the US included the S&P CoreLogic Case-Shiller 20-city home price index. The index was unchanged at an annual rate of 5.7% in May, which was slightly below forecasts of 5.8%.

The dollar firmed to around 111.50 yen after the consumer confidence data, but the dollar index remained not too far from the 13-month lows from earlier in the day, and last stood at 93.84.

In commodities, gold prices reversed lower as the dollar recovered and the yellow metal was trading at $1251.40 an ounce in late European session. Oil prices extended their gains following the latest move by OPEC to curb supply. WTI oil advanced to $47.38 a barrel, while Brent crude was up at $49.65 a barrel.

OPEC Remains Committed to Cutting Output; Oil Rises; Loonie Receives a Boost

Oil prices maintained their positive momentum, rising for a second straight day after OPEC countries called on several of the organization's members to adhere to the deal to reduce output. Adding to momentum for the commodity and further boosting prices was the commitment by Saudi Arabia - the world's number one oil exporter - to cut exports starting next month. The oil-linked loonie gained on the back of these developments, rising to a fresh multi-month high relative to the dollar. Unlike the Canadian dollar, the Russian ruble, another currency closely-related to oil, didn't manage to advance relative to the US currency.

OPEC, as well as non-OPEC producers led by Russia, discussed extending their deal to cut oil supply by 1.8 million barrels per day (bpd) during yesterday's meeting in the Russian city of St. Petersburg. The initial deal which was agreed last year and went into effect in January of this year, was originally expected to last up to the first half of 2017. As the boost it provided to oil prices was temporary, it was extended until March, 2018.

The initial deal's effectiveness to raise prices was in part dented by rising output from US shale producers who attempted to benefit from the increase in prices, placing a ceiling on the stronger upward movement in oil prices that was hoped for by the deal participants. The latest discussions are opening the way for a continuation of the deal beyond March of next year, in an effort to deplete global crude inventories.

Another significant development from yesterday's meeting, is that Nigeria, a major oil producer which was excluded from the initial deal to cut output, has voluntarily agreed to eventually (depending on Nigerian production patterns) join efforts to reduce production. A recent increase in production by Nigeria and Libya, another nation exempted from the initial deal, led to oil prices tumbling recently. Specifically, in late June, WTI and Brent crude both fell to more than eight-month lows of $42.05 and $44.35 a barrel respectively.

Moreover, Khalid al-Falih, the Saudi Energy Minister, stated that his country would reduce its exports to 6.6m bpd in August, by roughly one million barrels per day compared to a year ago. He added that global stockpiles have fallen by 90m barrels during the first six months of the year, though they currently exceed the five-year average for industrialized nations by about 250m barrels. Falih expects global oil demand to grow next year at a magnitude that outpaces the increase in US output. China is anticipated to record a double-digit increase in oil imports in the coming year.

Saudi Arabia and Kuwait have so far cut production by more than agreed, but compliance by Iraq and the United Arab Emirates has not been as strong. This is a consideration that must be addressed according to Saudi Arabia's Falih, who avoided naming specific countries and added that the committee monitoring compliance raised the issue with lagging nations. Alexander Novak, the Russian Energy Minister, said that full compliance would result to an additional 0.2m barrels being removed from the market on a daily basis.

Concluding with market movements, oil prices are posting considerable gains for a second day in a row. WTI and Brent crude oil were trading at $47.26 and $49.51 a barrel in late European trading hours, up 2.0% and 1.9% on the day respectively. In forex markets, dollar/loonie fell to a fresh 15-month low of 1.2480 in today's trading as the oil-linked Canadian dollar is benefitting from higher oil prices (Canada is a major exporter of the commodity). The Russian ruble is not experiencing similar gains as dollar/ruble is looking set for its third consecutive day of advances. The pair last traded at 59.890.

Elliott Wave Analysis: Triangle On AUDUSD Points Higher

AUDUSD can be trading at the end of a triangle correction in wave 4, which means a sharp recovery higher can be around the corner. Ideally we will see the previous blue wave b swing of the triangle correction breached, which would be a confirmation for a completed correction and black wave 5 in progress. Ideally wave 5 will later extend its gains towards the Fibonacci ratio of 138.2/161.8 region.

AUDUSD, 1H

Gold Pulls Back, But Still in a Short-Term Uptrend

Gold prices rose last week, fuelled by continued declines in the US dollar. During the European morning Tuesday, the yellow metal corrected somewhat lower amid a general risk-on sentiment in markets, evident by major stock indices like the S&P 500 hovering near all-time highs, as well as a general sell-off in other safe haven assets like JPY.

Absent some unforeseen risk event, the next major market mover for gold may be tomorrow's FOMC decision. We think risks are tilted towards a slightly more cautious narrative than previously given lacklustre inflation data and as such, we see the case for the dollar to extend its recent losses. Something like that could help the yellow metal resume its latest uptrend.

Gold traded lower during the European morning Tuesday after it hit once again resistance at the 1258 (R1) hurdle. Nevertheless, the slide was limited above the upside support line taken from the low of the 27th of January, and also above the lower bound of the short-term upside-sloping channel that has been containing the price action since the 10th of July.

As long as the rate is trading within that channel the short-term outlook of the yellow metal remains positive. If the bulls prove strong enough to take advantage of the 1245 (S1) support territory, we would expect them to aim for another test near 1258 (R1). A decisive break above that obstacle would confirm a forthcoming higher high on the daily chart and may open the way for our next resistance of 1266 (R2).

Zooming out to the daily chart, we see that the metal continues to trade in the sideways range that's been in place since the end of January, between the 1200 and 1300 territories. The latest recovery began from near the lower bound of the range. This alongside the break above the crossroads of the 1245 (S1) barrier and the upside support line drawn from the low of the 27th of January, increase the likelihood for further upside extensions in our view.

EUR/USD Nears Key 1.1735 Resistance

- European shares advanced strongly (Euro Stoxx +1.0%), rebounding after three days of declines as rising bond yields spurred banks and increasing metal prices helped miners. US stocks climbed on strong corporate earnings from big companies such as Caterpillar, du Pont de Nemours, United Technologies and General Motors.

- German Ifo business climate improved for a sixth month in July. The Ifo index rose to 116.0 from a revised 115.2 in June. That's the highest level since 1991 and compares with a median estimate of a drop to 114.9. The Ifo expectations component also rose from 106.8 to 107.3 while a decline to 106.5 figure was expected.

- American house prices nation-wide cooled modestly from an upwardly revised 5.65% Y/Y in April to 5.58% in May according to the S&P Home Price Index. The S&P 20-City index, that measures home-price changes in 20 US metropolitan regions, also declined from 5.77% Y/Y in April to 5.69% in May while the consensus expected 5.80%.

- Greece will raise €3 billion in its first visit to international bond markets since 2014 as it attempts to turn the page on a debt crisis that forced it to seek multiple international bailouts. The sub-investment grade rated country is selling 5y notes at a yield of 4.625%, after tightening terms twice from an initial target of around 4.875%.

- The two new members of the Bank of Japan's policy board said that the central bank should continue efforts to achieve its 2% price goal and it was premature to debate an exit from the massive monetary stimulus. The first policy meeting for the newcomers will be in September.

- Senator John McCain, who is battling brain cancer, will return to the US Senate today to play what could be a crucial role in salvaging Republican efforts to repeal Obamacare. The tally in the divided chamber was expected to be extremely tight, making McCain's return critical to the repeal effort.

- US Consumer confidence and Richmond Fed Manufacturing index surprised both on the upside of expectations. Consumer confidence surged from 117.3 to 121.1 in July, with an improvement both in the current assessment and expectations components. The Richmond Fed index improved from 11 to 14 in July.

Rates

Core bonds sell-off

Global core bonds lost ground today. The move started at the European opening and accelerated ahead of the start of US dealings. It's hard to pinpoint one specific factor to explain the move. A very strong German IFO-indicator (both current situation and expectations) and an upwardly oriented oil price certainly helped. Several bellwether companies including Caterpillar, announced good earnings and boosted equity market sentiment. The German 10-yr yield's failed test of 0.5% support perhaps inspired some technical Bund selling and suggests we might attack the 2017 high, especially if the Fed tomorrow signals willingness to continue its tightening cycle without attaching too much weight to the current dip in inflation readings. The upcoming US refinancing operation plays in the disadvantage of US Treasuries.

At the time of writing, the US yield curve bear steepens with yields 2.1 bps (2-yr) to 4.8 bps (30-yr) higher. Changes on the German yield curve range between +2.9 bps (5-yr) and +4.8 bps (10-yr). On intra-EMU bond markets, 10-yr yield spreads versus Germany are nearly unchanged.

Greece launched its first benchmark bond since 2014 today. They issued a new 5-yr GGB via syndication. The order book was in excess of €7B, allowing Greece to print €3B. The bond was priced to yield 4.625%, tighter than IPT's at 4.875% and official guidance at 4.75%. With its return to international markets, Greece aims to raise a war chest ahead of the end of the current bailout programme in August next year. The US Treasury starts its end-of-month refinancing operation tonight with a $26B 2-yr Note auction. The WI currently trades around 1.39%. The auction is followed by a $15B 2-yr FRN auction and a $34B 5-yr Note auction tomorrow and a $28B 7-yr Note auction on Thursday.

Currencies

EUR/USD nears key 1.1735 resistance

Today, EUR/USD and USD/JPY initially didn't find a clear trend even as EMU confidence data were very strong. Early in USD dealings, European yields jumped higher again. EUR/USD came within reach of the 1.1714/35 area, but a real test didn't occur (yet). USD/JPY had some tepid intraday gains and trades in the 111.50 area. Even so, euro weakness combined with USD softness remains the name of the game going into tomorrow's Fed policy decision.

Asian equities traded mixed in line with WS. ECB's Mersch said he saw upward risks to EMU growth and stated that he's more assured about a return of inflation to the target. At the same time he reiterated that policy accommodation remains necessary. EUR/USD rebounded to the 1.1660 area on the Mersch headlines, but a test of the recent highs didn't occur. USD/JPY stabilized near 111.

In Europe, the French Business confidence and the German IFO business climate were both stronger than expected. European equities and core yields rose slightly after the data. The euro tried a shy attempt to go higher but almost immediately ran into resistance. EUR/USD returned to the 1.1650 area. USD/JPY slightly gained further ground on a modest rise in core (US & EMU) yields.

Early in US dealings, the focus was on corporate earnings. Most results were better than expected and reinforced the positive risk sentiment from European equity markets. Core bond yields maintained an upward bias. This morning, one could have questioned whether the lack of a euro response to good EMU data pointed to some exhaustion of the euro rally. This afternoon it appeared that this wasn't the case. An new uptrend in European bond yields finally pushed EUR/USD beyond the 1.17 big figure. The 1.1714/36 key resistance came within reach. At the same time, USD/JPY (currently around 111.45) hardly profited from higher core yields and a good risk sentiment. So, for now, the trends of euro strength and USD softness remain in place going into the FOMC decision.

GBP succeeds insignificant comeback

Sterling staged a technical rebound against the dollar and the euro. At the end of last week, the poor results of the first round of negotiations between the UK and the EU weighed on the UK currency. Today's rebound of sterling was primarily technical in nature. The eco news was intrinsically negative for sterling. The IMF downwardly revised the UK 2017 growth forecast to 1.7% Y/Y (from 2.0% in April). IHS markit also reported that its household financial index dropped to the lowest since July 2014 due to rising costs of living. However, all this didn't prevent a modest technical rebound of the sterling. EUR/GBP trades currently in the 0.8945 area. Cable returned north of 1.30. The first estimate of the UK Q2 GDP, to be published on Wednesday, will be the next key factor for sterling trading.

Copper Boosted by Signs of Robust Demand

Copper contract for July delivery hit fresh over five-month high on Tuesday, boosted by signs of robust demand from top consumer China, tight supplies and weak dollar. Copper price skyrocketed on Tuesday, marking the biggest one-day rally since early Feb and rallying 3.25% until now. Tuesday's rally cracked very important barrier at $2.8215 (former recovery high of 12 Feb) and hit new 2017 highs above $2.83 barrier. Strong bullish sentiment can drive the price towards next key resistance at 2.9550 (May 2015 high/Fibo 138.2% projection) on sustained break above 2.8215 barrier. Meanwhile, hesitation at 2.8215, which could results in corrective easing, could be anticipated as daily techs are overbought and bearish divergence formed on daily slow stochastic, as well as on profit-taking action. However, limited downside action is seen, as sentiment remains firmly bullish, with 2.7000 zone (near Fibo 38.2% of 2.4720/2.8315 rally, reinforced by rising daily 20SMA) expected to contain extended dips.

Res: 2.8315; 2.8500; 2.8895; 2.9000

Sup: 2.8000; 2.7670; 2.7467; 2.7155

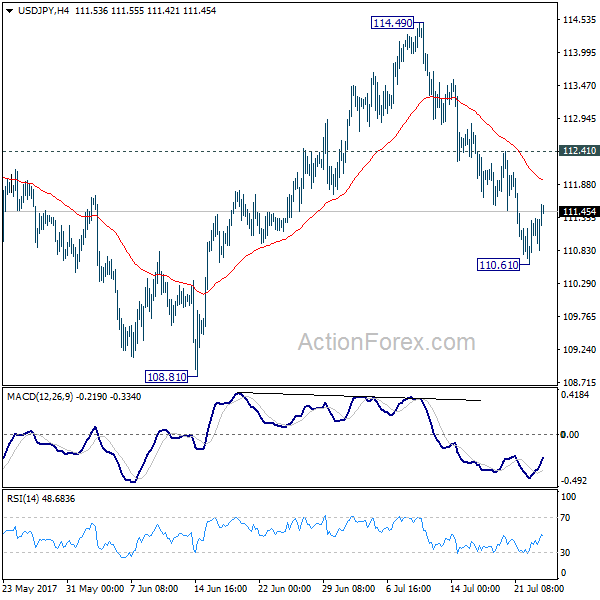

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.70; (P) 111.01; (R1) 111.39; More...

Intraday bias in USD/JPY remains neutral as recovery from 110.61 temporary low continues. Upside should be limited by 112.41 resistance to bring another decline. Below 110.61 will turn bias back to the downside for 108.81 support. Whole correction from 118.65 is possibly resuming. Break of 108.81 will confirm and target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, break of 112.41 will dampen this bearish view and turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

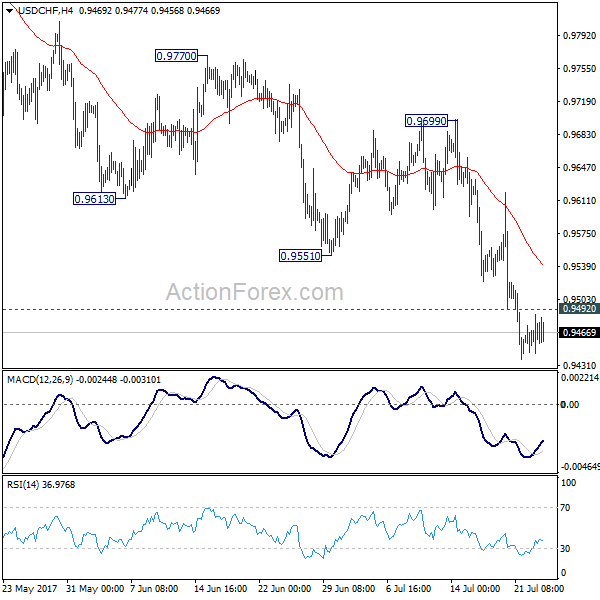

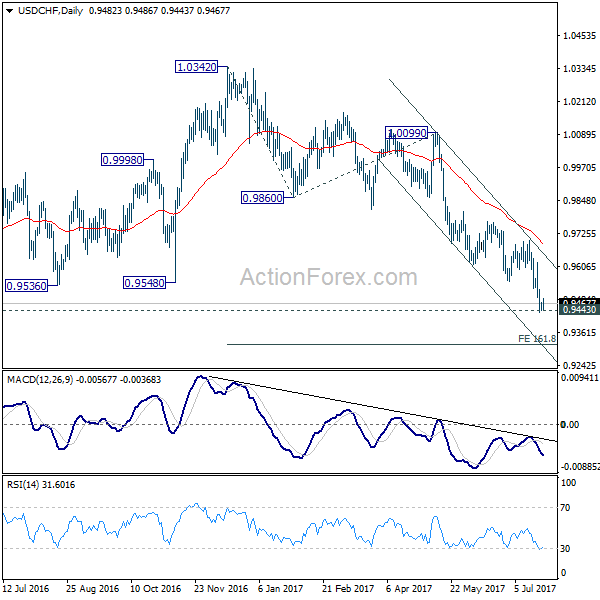

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9447; (P) 0.9461; (R1) 0.9478; More...

With 0.9492 minor resistance intact, intraday bias in USD/CHF remains on the downside for further decline. Sustained trading below 0.9443 key support will extend the down trend from 1.0342 to 161.8% projection of 1.0342 to 0.9860 from 1.0099 at 0.9319. On the upside, above 0.9492 minor resistance will turn bias neutral and bring recovery. But outlook will remain bearish as long as 0.9699 resistance holds.

In the bigger picture, focus is now back 0.9443 key support level. Sustained break there indicate underlying bearish momentum and would target 0.9 handle and possibly below. Meanwhile, strong rebound from current level and break 0.9699 resistance will extend long term range trading between 0.9443/1.0342.

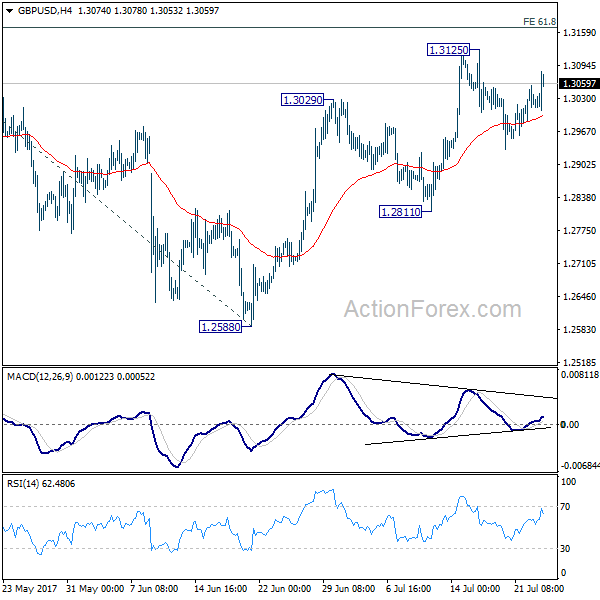

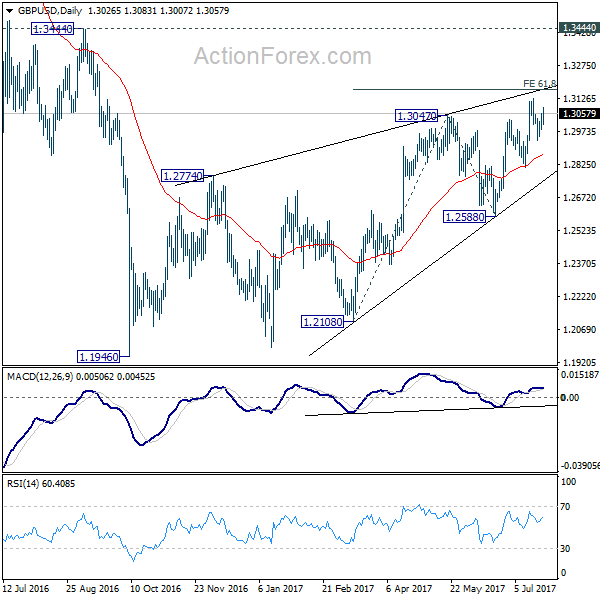

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2992; (P) 1.3024; (R1) 1.3061; More...

Intraday bias in GBP/USD remains neutral for the moment. With 1.2811 support intact, another rise is mildly in favor. Break of 1.3125 will target 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168. Overall, choppy rebound from 1.1946 is seen as a corrective pattern, hence, we'd be cautious on strong resistance from 1.3168 to limit upside. But firm break of 1.3168 will bring further rise towards 1.3444 key resistance. Meanwhile, break of 1.2811 support will be the first sign of reversal and will turn bias to the downside to target 1.2588 key support next.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

Trade Idea: EUR/GBP – Buy at 0.8875

EUR/GBP - 0.8951

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

Original strategy :

Buy at 0.8875, Target: 0.8995, Stop: 0.8835

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.8875, Target: 0.8995, Stop: 0.8835

Position : -

Target : -

Stop : -

Euro’s retreat after rising to 0.8995 on Friday has retained our view that consolidation below this level would be seen and pullback to 0.8900 cannot be ruled out, however, reckon downside would be limited to 0.8875-80 and bring another rise later, above psychological resistance at 0.9000 would extend recent rise to 0.9020 and possibly towards 0.9050 but overbought condition should prevent sharp move beyond latter level, risk from there has increased for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback as 0.8870-75 should limit downside. Only break of support at 0.8829 would abort and confirm top is formed instead, bring correction to 0.8800 first.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.