Sample Category Title

AUD/USD Reaches Top Of Resistance Zone. Will It Now Drop?

How about that Aussie Dollar!

I've had resistance drawn as a zone up here as there are multiple swing highs that are hitting a couple of different levels and the Aussie has continued to be rejected off resistance time and time again.

Taking a look at today's Daily chart however, you can see that price has rallied and tapped the highest extreme of the zone. Just another touch to add to the collection!

AUD/USD Daily:

But let's not get too carried away just yet.

The momentum behind this type of move is exactly why we wait and see if the higher time frame resistance level can actually hold before selling any retests of short term support.

Confirmation is the key factor in avoiding being hit by the freight train of bullish momentum that is just waiting to clean up faders that get their timing ever so slightly out.

GOLD – Faces Further Recovery Higher

GOLD - With the commodity continuing to retrain its recovery, more gain is envisaged. On the downside, support comes in at the 1,210.00 level where a break will turn attention to the 1,200.00 level. Further down, a cut through here will open the door for a move lower towards the 1,190.00 level. Below here if seen could trigger further downside pressure targeting the 1,180.00 level. Conversely, resistance resides at the 1,230.00 level where a break will aim at the 1,240.00 level. A turn above there will expose the 1,250.00 level. Further out, resistance stands at the 1,260.00 level. All in all, GOLD looks to recover further higher.

AUD/USD Breakout Attempt, USD/JPY Trading In The Red, NZD/USD Buying Opportunity?

AUD/USD breakout attempt

Price rallied aggressively in the last days and touched fresh new highs, is strongly bullish on the Daily chart and looks unstoppable. Will increase further if the USDX will slide further, the index has closed the former week at 95.10 level, much below the 95.45 previous low. USDX is under massive selling pressure on the Daily chart, but remains to see what will happen because is very close to hit a major dynamic support.

AUD/USD will be driven by the fundamental factors in the morning, the Chinese data will have a high impact on the Aussie's movement. The Chinese GDP could increase by 6.8% in the second quarter, less versus the 6.9% growth in the former reading period, while the Industrial Production may increase by 6.5% in June, could remain steady at 6.5% for the third month in June.

Moreover the Retail Sales could increase by 10.6%, less versus the 10.7% growth in the former reading period , while the Fixed Asset Investment could increase by 8.5%, less versus the 8.6% estimate.

Price edged higher and is very close to hit the 0.7835 major static resistance, could touch also the upper median line (uml) of the ascending pitchfork, where he could find temporary resistance. The perspective remains bullish as long as the rate is trading within the ascending pitchfork's body.

Will be very important to see how will react when will touch the 0.7835 static resistance, right now we don't have any overbought sign. Technically, a minor drop is favored after the impressive rally, but is premature to say that we'll have a corrective phase in the upcoming days.

We'll have a selling opportunity only if the rate will fail to breakout above the 0.7835 upside obstacle and if will be rejected by this level. I want also to remind you that a valid breakout above the mentioned resistance will confirm a further growth.

USD/JPY trading in the red

Price has turned to the downside after a false breakout above an important static resistance area, continues to move sideways and may will be better to stay away till will have a fresh trading signal.

Is trading right above the 112.50 psychological level and was very close to react and retest a dynamic support level (resistance turned into support). The current decrease is natural after the false breakout above the 23.6% retracement level and after the failure to reach the third warning line (WL3). The Yen will appreciate further if the Nikkei stock index will drop and will stabilize below the 20058 level.

NZD/USD buying opportunity?

The pair increased sharply in the previous week and has managed to close above a major static resistance. The breakout needs confirmation, a minor consolidation above the 0.7324 broken static resistance will bring us a good buying opportunity.

Price will resume the upside movement only if will have enough energy to close above the 0.7367 previous high. Personally, I would like the rate to come to retest the fourth warning line (wl4) before will increase further.

EURUSD – Sets Up To Resume Upside Pressure

EURUSD - The pair continues to hold on to its medium term uptrend with more strength envisaged in the new week. Resistance comes in at 1.1500 level with a cut through here opening the door for more upside towards the 1.1550 level. Further up, resistance lies at the 1.1600 level where a break will expose the 1.1650 level. Its daily RSI is bullish and pointing higher suggesting further strength. Conversely, support lies at the 1.1400 level where a violation will aim at the 1.1350 level. A break of here will aim at the 1.1300 level. All in all, EURUSD faces further upside pressure.

EURGBP – Sells Off After Price Rejection

EURGBP - The cross continues to retain its corrective pullback threats selling off the past week and opening the door for more weakness. Support lies at the 0.8700 level where a violation will turn focus to the 0.8650 level. A break will expose the 0.8600 level. Resistance resides at the 0.8800 level where a violation if seen will turn risk towards the 0.8850 level. Further up, resistance resides at 0.8900 level followed by the 0.8950 level. All in all, EURGBP remains biased to the downside on bear threats.

Betting Against The Fed & USD

The technical breakdowns in the US dollar after Friday's weak data releases raise deeply troubling questions about the currency. The Australian dollar was the best performer last week while the US dollar lagged. CFTC positioning showed the completion of the CAD-whipsaw. The Premium Insights closed out of the GBPUSD long with 120-pip gain and issued a new set of charts on the pair. A new JPY trade was also added earlier in Friday.The technical breakdowns in the US dollar after Friday's weak data releases raise deeply troubling questions about the currency. The Australian dollar was the best performer last week while the US dollar lagged. CFTC positioning showed the completion of the CAD-whipsaw. The Premium Insights closed out of the GBPUSD long with 120-pip gain and issued a new set of charts on the pair. A new JPY trade was also added earlier in Friday.

You can indeed fight the Fed. Betting against the dollar this year has been the best FX trade, as it has over the last week. Policymakers' insistence that growth and inflation are picking up has been repeatedly undermined by soft data.

On Friday, retail sales and CPI data missed estimates and the market threw in the towel. The dollar was beaten up across the board and finished on the weekly lows. The lack of buyers at the lows points to more trouble ahead. In addition, a few dollar charts are breaking down. On Friday, cable rose to the highest since September 2016. Remember, the UK is facing political uncertainty, Brexit uncertainty and poor economic data.

NY Fed's Q3 2017 Nowcast GDP forecast remains at 1.8% and Q2 GDP forecast revised down to 1.9% from 2.0%.

Australia has also struggled this year but on Friday broke above a double-top at 0.7750 and finished the week just a handful of pips away from the 2016 high of 0.7835. CAD, EUR and everything else but USD/JPY is also in a precarious position.

Ultimately, it's still tough to bet against the Fed because they're only a few good data points away from raising rates again but the calendar is light until the final few days of July and that argues for more dollar weakness ahead.

CFTC Commitments of Traders

Speculative net futures trader positions as of the close on Tuesday. Net short denoted by - long by +.

EUR +84K vs +77K prior GBP -24K vs -28K prior JPY -112K vs -75K prior CHF 0K vs 0K prior CAD -9K vs -39K prior AUD +37K vs +32K prior NZD +32K vs +29K prior

The deeply misguided CAD-short trade has virtually been erased. The market piled into bets against the loonie on signs of trouble in the Canadian housing market the story proved to be a canard and the Bank of Canada massacred the trade. Ultimately, the market will get long CAD on signs of rising rates but it will need to lick its wounds first.

The other development is the shift to yen shorts. That's something we focused on last week. The BOJ is the only central bank that isn't making growing hawkish shift, and we learned on Thursday that inflation forecast might even be cut. Those shorts are likely in it for the long haul.

US Dollar: Swoon To Swoon

US Dollar: Swoon to Swoon

Friday's US data led to more USD selling as both US CPI and retail sales for June disappointed.All too familiar themes ensued with the S&P stretching to record highs as the US ten year yields toppled to 2.33 % on a dovish Fed interpretation. And with the odds of any near term US rate hike extinguished, G-10 currencies soared as the AUD, EUR and CAD all established new 2017 high water marks.

The main hurdle to further Fed tightening is inflation, and it will continue to play the decisive role in central bank policy and will ultimately decide the direction for global macro markets throughout the remainder of 2017.

With less than a 50 % December rate hike probabilities priced in and with no supportive Fed speak on the calendar before July 26th, the dollar could struggle. Even more so given the lack of any top tier data to swing sentiment as dealers will be limited to US housing and PMI as data sources, only secondary metrics. There's simply not enough meat on the bone on these US economic data points to push December probabilities much beyond a 50:50 call even on stellar prints. However with five crucial months of inflationary data to go before December's debatable Fed rate hike, the inflation as a transitory debate has a long way to play out yet.

In the absence of any major dollar drivers. G-10 will turn to the latest monetary policy musing by ECB and BoJ, which hold their respective policy meetings on Thursday.

On the one hand, we have the ECB that spooked the bond markets asserting deflationary forces has been conquered. But given the aggressive bond sell off that ensued, the ECB is more likely to temper expectations unfurling some of those market reactions to Draghi's hawkish delivery. Only a big upside surprise in Eurozone CPI(Monday) would be needed to elevate the policy meeting theatrics.

On the other hand, the BoJ found themselves back in the spotlight when they threw a bridle on Yen interest rates with YCC (Yield Curve Control) by conducting an aggressive fixed-rate JGB purchase operation last week. The BoJ is determined to maintain accommodative policy as the JPY NEER is nowhere close to levels that would suggest a policy shift from the BoJ. But given the global bond markets aggressive sell off on the wake of the hawkish central bank narratives, the Fed and the ECB will, in fact, welcome the BoJ policy direction as this will keep the global bond market sell off in check as well the market's implied tightening trajectory from running amok.

Given the market's reaction to only a central bank tapering directive, the real litmus test is when the ECB and FED stop buying bonds. It will happen, and It's Goodbye Yellow Brick Road as far as easy money is concerned

China retail sales, industrial production and GDP data will be the key focus for AUDUSD and NZDUSD traders today. Growth is expected to have cooled to 6.8 percent in the second quarter as Beijing tightens the screws on financial risks, while administrators continue to thwart property speculators and try to reduce pressure on asset bubbles reigning in unbridled credit markets.

EURO

The Euro is trading in rarified air on anticipated shifting yield curve differentials as opposed to anything else suggesting the EURO may slip ahead of this week's ECB meeting as speculative positions are a bit stretched to the top side.

Japanese Yen

Japan is closed for Marine Day day today, but this week the markets will be focused on the BoJ and their anticipated upgrade to the economic assessment. However, given humdrum inflation developments, there's little chance the BoJ will make a move towards monetary tightening.

Australian Dollar

Much to the RBA's chagrin, the weak USD storyline has sent the A$ dollar soaring despite an apparently dovish RBA. Sure there are some indications the economy is picking up, but this does not necessarily mean a call to action for the RBA. However, positioning does suggest the contrary as some start pricing RBA rate hike expectations later this year.

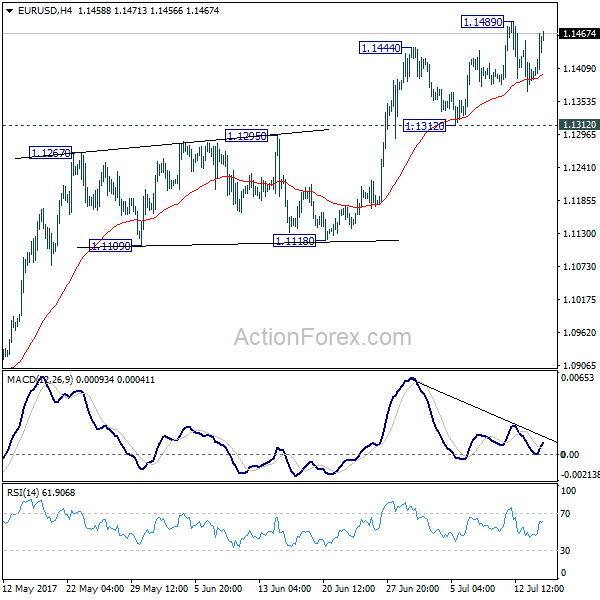

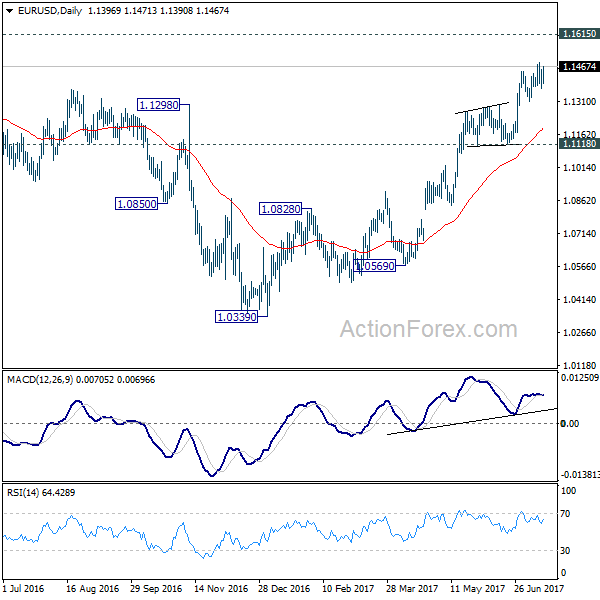

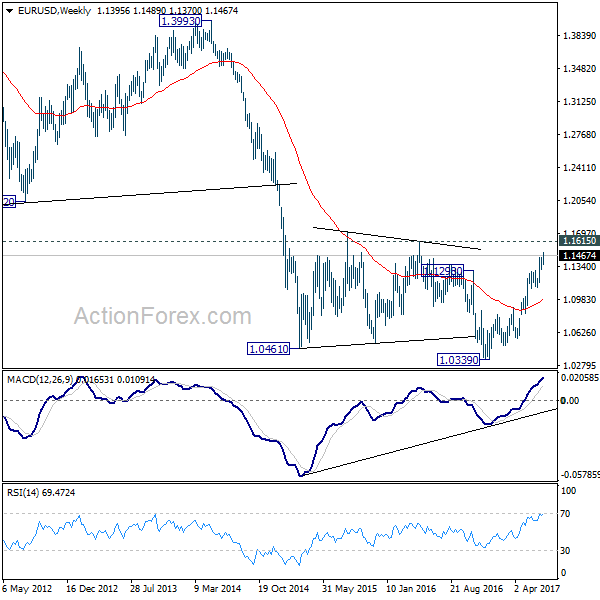

EUR/USD Weekly Outlook

EUR/USD edged higher to 1.1489 last week but retreated since then. Initial bias stays neutral this week and more consolidation could be seen. But Break of 1.1312 will bring deeper fall to 55 day EMA (now at 1.1192). In that case, downside should be contained by 1.1118 support to bring rise resumption. On the upside, break of 1.1489 will extend recent rally from 1.0339 to 1.1615 key resistance next.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1763). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

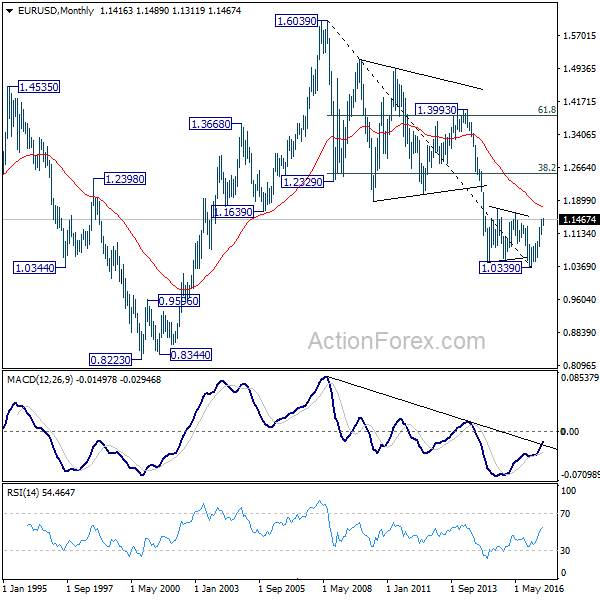

In the long term picture, 1.0339 is now seen as an important bottom as the down trend from 1.6039 (2008 high) could have completed. It's still early to decide whether price action form 1.0339 is developing into a corrective or impulsive move. But in either case, further rally would be seen to 38.2% retracement of 1.6039 to 1.0339 at 1.2516

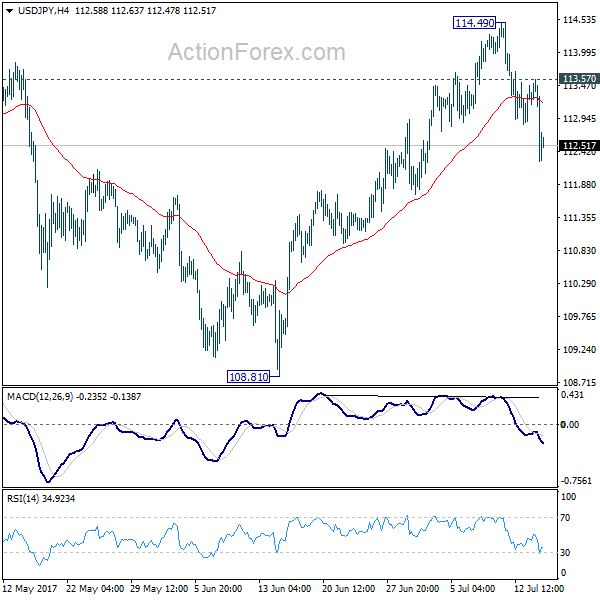

USD/JPY Weekly Outlook

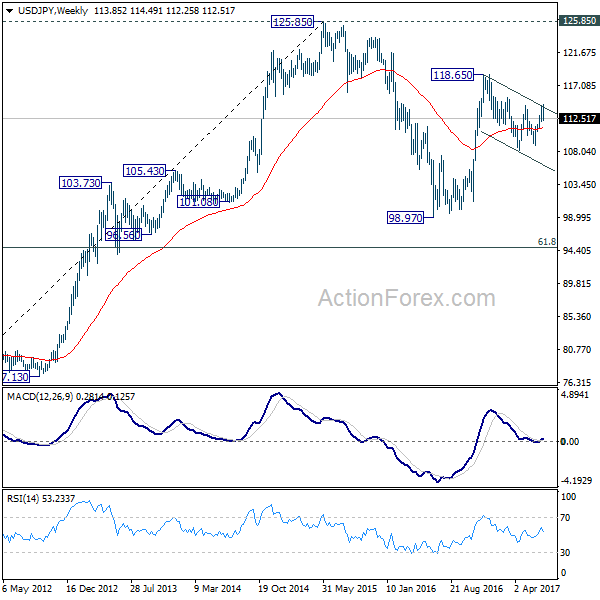

USD/JPY edged higher to 114.49 last week but failed to sustain above 114.36 resistance and reversed. The rejection from 114.49 argues that rise from 108.81 is completed. And, the whole correction from 118.65 is possibly still in progress. Initial bias stays on the downside this week for 55 day EMA (now at 112.01). Sustained break will pave the way to 108.12 and below. On the upside, above 113.57 minor resistance will turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

In the long term picture, the rise from 75.56 long term bottom to 125.85 top is viewed as an impulsive move. Price actions from 125.85 are seen as a corrective move which could still extend. But, up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

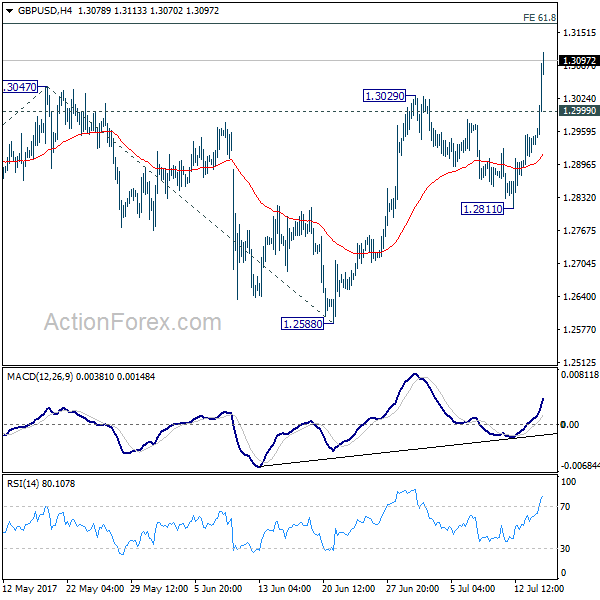

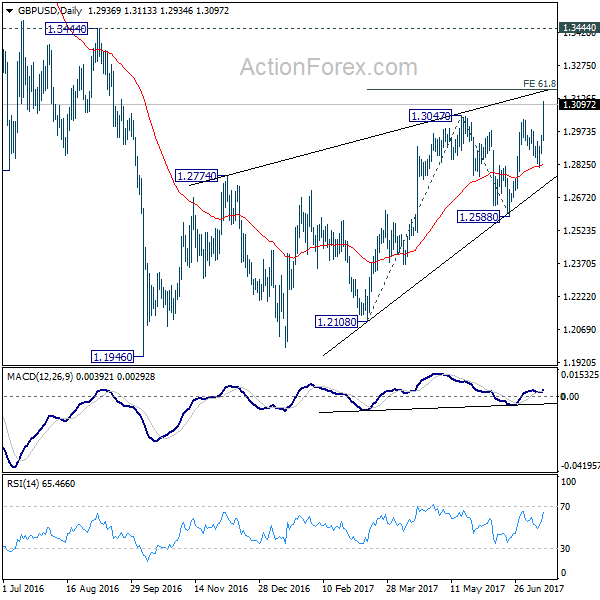

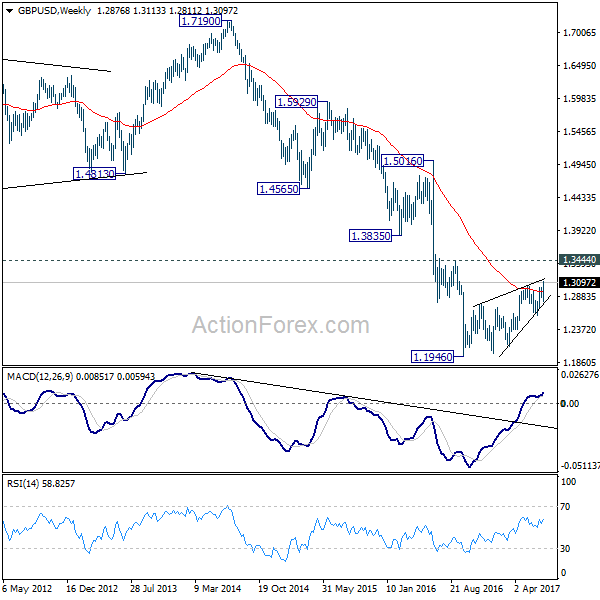

GBP/USD Weekly Outlook

GBP/USD's pull back from 1.3029 completed at 1.2811 last week and subsequent strong rally confirmed resumption of larger rise from 1.1946. Initial bias is now on the upside this week for 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next. We'll be cautious on strong resistance from there to limit upside. But firm break of 1.3168 will bring further rise towards 1.3444 key resistance. On the downside, below 1.2999 minor support will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

In the longer term picture, no change in the view that down trend from 2.1161 is still in progress. On resumption, such decline would extend deeper to 100% projection of 2.1161 to 1.3503 from 1.7190 at 0.9532. However, firm break of 1.3444 should confirm reversal and turn outlook bullish.