Sample Category Title

Yen Unchanged, Markets Await US Retail Sales, CPI

It's been an uneventful Thursday for the yen, as USD/JPY is unchanged on the day. In the North American session, the pair is trading at 113.30. On the release front, there are no Japanese events on the schedule. In the US, PPI posted a weak gain of 0.1%, above the forecast of 0.0%. Unemployment claims ticked lower to 247 thousand, above the estimate of 245 thousand. On Friday, the US releases CPI and retail sales numbers, so traders should be prepared for some movement from USD/JPY.

Janet Yellen's testimony on Capitol Hill on Wednesday was largely a non-event, and her testimony before a Senate Committee on Thursday will likely be more of the same. Yellen's message didn't veer from what the markets have already heard from other Fed policy makers. Yellen reiterated that the Fed planned to raise rates "gradually", and added that the Fed would begin trimming its balance sheet before the end of the year. The Fed chair didn't provide any timelines, but many analysts are circling September for a balance sheet reduction, with a rate hike to follow in December. However, despite Yellen's assurances, the markets remain lukewarm about a rate hike before the end of the year. Investors are concerned that the US economy has slowed down in 2017 and may not need another rate hike. In her testimony, Yellen reiterated said that she believes the factors weighing on inflation are temporary. However, she acknowledged that with inflation well below the Fed's target of 2%, adding that there could be more going on there". For their part, the markets remain skeptical about a rate hike. The CME Group has pegged a December rate increase at just 47%, while other forecasts are pointing to odds as low as 40%. Hints from the Fed will not suffice to bring investors on board – unless growth and inflation numbers move higher, the markets are likely to remain lukewarm about the likelihood of a third rate hike in 2017.

The Bank of Japan will hold a policy meeting next week, and is expected to upgrade its economic growth forecasts in response to the stronger economy. The bank has hinted that it will push back its timeline for inflation reaching the 2% target, which currently does not seem a realistic goal, despite years of ultra-loose monetary policy. Will this happen at the July meeting? The markets may not get an answer until the rate statement is released, as the board members are split between those who expect inflation to rise due to the stronger economy, and those who don't think inflation levels will move upwards. If the pessimists prevail, the bank will delay the timing for hitting the 2% target from its current forecast of "around fiscal 2018" to a later date. The bank has said that it will not reduce its radical stimulus program until inflation levels move higher.

After a short break, the Trump administration's alleged ties with Russia are once again front-page news. This week, Washington is abuzz that Donald Trump Jr. admitted that a Russian official contacted him and offered to provide him with evidence incriminating Hillary Clinton. Predictably, the White House has attacked the media and is trying to distance itself from Trump Jr.'s meeting, but the miscue is one more example of the White House having to shift to damage control mode, rather than focus on its agenda. Trump hasn't been able to pass health care or other legislation through Congress, even though Republicans control both the House of Representatives and the Senate. The latest dark cloud over the White House has dampened investor confidence, and it's a safe bet that this latest crisis is not the last.

Elliott Wave Analysis: GBPUSD Unfolding A New Leg Higher

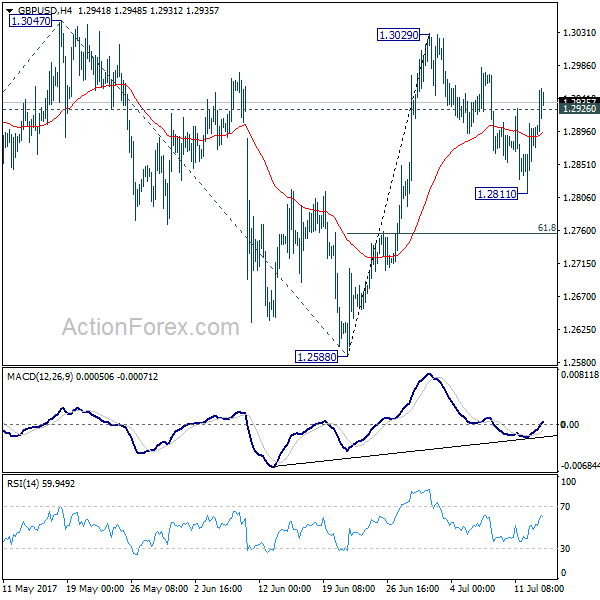

GBPUSD is making a nice bullish rally away from 1.2815 region, where wave B) lows were found. That said current bullish leg can be black wave 1 in the making, with price specifically trading at the end of blue sub-wave three. Ideally a new correction within wave four will follow, and find a new region of support around the previous swing four at 1.2915 level.

GBPUSD, 1H

Sterling Extends Technical Rebound

- European equities traded with a small upward bias and currently record gains of around 0.5%. The German Dax underperforms. US equity indices open marginally higher.

- ECB President Draghi is scheduled to address the Federal Reserve's Jackson Hole conference in August for the first time in three years, according to a person familiar with the matter. In a speech he is expected to give a further sign of the ECB's growing confidence in the eurozone economy and its reduced dependence on monetary stimulus.

- US eco data printed close to consensus. Weekly jobless claims hovered around last week's level (247k from 250k). June headline PPI slowed from 2.4% Y/Y to 2% Y/Y (vs 1.9% Y/Y forecast) while core PPI declined from 2.1% Y/Y to 2% Y/Y.

- The European Banking Authority, the supervisor of supervisors across the EU, said that the majority of banks across the bloc expect their provisions to rise by 18% after the introduction of the rules, called IFRS 9. That compares to an earlier estimate in November that was as high as 30%.

- The rebalancing of global oil markets has become less certain, with OPEC production rising and little evidence that bloated stockpiles are shrinking as expected, the International Energy Agency said. That's a change from two months ago when the IEA said the "rebalancing is here" and was accelerating in the short term.

- The German economy will continue to enjoy solid growth in the second quarter, driven by soaring private consumption and higher construction activity while net foreign trade is unlikely to add to the expansion, the Economy Ministry said. Europe's biggest economy grew by 0.6% Q/Q in the first quarter

- The Swedish krona jumped to its strongest level in more than two months (EUR/SEK 9.5250) after new inflation figures beat forecasts for a second straight month, lending further support to the central bank's recent moves to edge away from monetary stimulus.

Rates

Draghi rumoured to give key speech at Jackson Hole

This week's rebound on global core bond markets initially persisted. Amid an empty eco calendar, investors wondered about yesterday's testimony by Fed chair Yellen before US Congress. Her subtle shift on inflation stressed the potential importance for markets from tomorrow's US CPI (and retail sales) data. Around European noon, core bond markets made a U-turn after the WSJ reported that ECB-president Draghi will address the Fed's Jackson Hole meeting at the end of August. According to officials, he is expected to signal that the ECB will announce at its September 7 meeting that they intend to gradually wind down QE-purchases next year. His appearance would be of symbolic value. His last speech in Jackson Hole dates back to August 2014 and was widely seen as heralding the start of asset purchases. The ECB confirmed Draghi's attendance some hours after the rumours.

At the time of writing, German yields rise 0.5 bps (2-yr) to 1.4 bps (10-yr). Changes on the US yield curve vary between +1.2 bps (2-yr) and +1.9 bps (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany range between -2 bps (France) and +2 bps (Portugal).

The Italian debt agency tapped the on the run 3-yr BTP (€2.75B 0.35% Jun2020), 7-yr BTP (€2.5B 1.85% May2024), 15-yr BTP (€1.23B 2.45% Sep2033) and off the run BTP (€0.77B 4% Feb2037). The total amount sold was the maximum of the €5.75-7.25B on offer. The auction bid cover was 1.51, which is above average for Italian auctions. The Irish treasury (NTMA) tapped two on the run bonds for a combined €0.75B: €0.5B 0.8% Mar2022 and €0.25B 2% Feb2045. The auction met with good demand, resulting in an auction bid cover of 2.27. The NTMA has issued €9.5B bonds so far this year, compared to its stated target range of €9-13B in the bond markets.. The US Treasury ends its refinancing operation tonight with a $12B 30-yr Bond auction. Currently, the WI trades around 2.90%.

Currencies

Dollar looking for guidance 'post-Yellen'

There was no dominant story to guide FX trading today. The dollar remained in the defensive in the wake of yesterday's Yellen testimony, but the pressure eased. Markets await tomorrow's key US eco data. EUR/USD dropped temporary below 1.14, but trades currently again above the big figure. USD/JPY tries to sustain north of 113.

Overnight, Asian equities joined the post-Yellen rebound on WS. Strong Chinese foreign trade data (both imports and exports stronger than expected) supported Chinese and Australian markets. USD/JPY underperformed despite recent attempts by the BoJ to cap the rise in Japanese yields. The pair also didn't profit from the risk-on sentiment. USD/JPY hovered in the low 113 area. EUR/USD traded in the 1.1440 area.

There were no important European data. Most markets were driven by particular, internal dynamics with little consistency across markets. Equities opened strong. At the same time, European yields extended yesterday's decline. The dollar also showed a diffuse picture. USD/JPY remained in the defensive (despite a bid in equities). EUR/USD met stop-loss selling, tumbling to the 1.1371 area. Profit taking on the recent impressive EUR/JPY rally was a factor. Early afternoon, markets turned a bit more volatile on a WSJ headline that Draghi might address the Fed Jackson Hole conference. Will he use this high profile forum to announce further policy normalisation? Whatever the interpretation, the euro bottomed. EUR/USD returned north of 1.14. USD/JPY also bottomed out as did core bond yields.

The US jobless claims and producer prices were very close to expectations. The impact on the dollar was negligible. USD trading remains indecisive with EUR/USD holding in the low 1.14 area. USD/JPY rebounds north of 113.

Sterling extends technical rebound

Sterling regained further ground, extending the rebound that started after good UK labour data yesterday. We see the rebound in the first place as technical in nature. Cable continues to profit from underlying USD softness. A topside test of EUR/GBP was rejected yesterday. The broader euro correction also triggered some further profit taking on EUR/GBP longs. The UK government published the Brexit 'Repeal Bill'. It will probably become a source of political noise, but for now we see no direct impact on sterling trading. BoE's McCafferty further complicated the BoE's monetary policy debate as he raised the issue of reducing the BoE's Balance sheet. His comments might have been slightly supportive for sterling. EUR/GBP trades currently in the 0.8825area. Cable is changing hands in the 1.2950 area.

USDJPY Looks Bearish Marginally above 113 Key-Level on 4-hour Chart

USDJPY, after a strong rally that totally reversed the May-June downward trend, has started a new downtrend once again. The pair is currently forming a bearish short-term bias, breaking its recent upleg and is struggling to hold on to the key level of 113.

According to the technical indicators, the short-term risk is to the downside as both the RSI and the MACD are below their positive thresholds and do not show any sign of upward movement. The RSI has been moving closer to neutral ground under 50, while the MACD has been sloping down in negative territory. Furthermore, another bearish signal is given by the Tenkan-Sen dropping below the Kinjun-Sen.

The market has been recently testing the 23.6% Fibonacci retracement level of the June to July upleg, from 108.77 to 114.48. Should the price fall, a first support could be found in the area near to the 38.2% Fibonacci level of 112.29, where the bottom of the Ichimoku cloud is also located. A deeper decline would hit the 50% Fibonacci mark of 112.63.

Should the pair go up, the zone where the 50-4-hour moving average of 113.48 and the Kinjun- Sen point of 113.67 are placed could provide resistance. Further increases, would target the latest peak of 114.48.

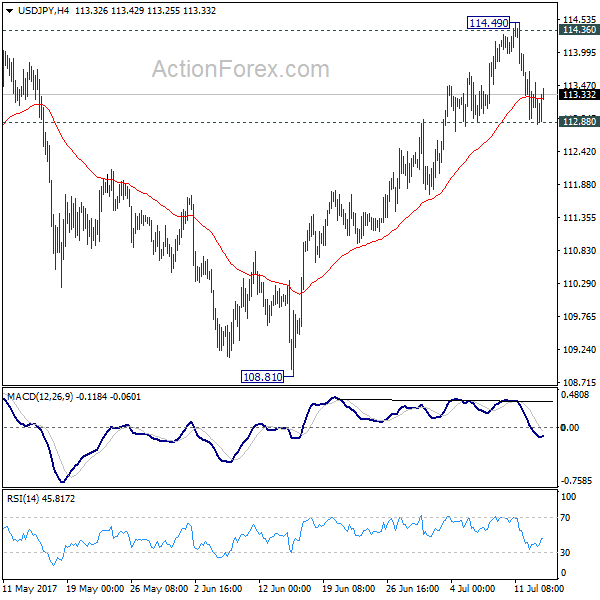

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.73; (P) 113.35; (R1) 113.77; More...

At this point, USD/JPY still holding on to 112.88 support and intraday bias remains neutral for the moment. Firm break of 112.88 will argue that rebound from 108.81 has completed at 114.49 after being rejected by 114.36 key near term resistance. That would also argue that the correction from 118.65 is still in progress. In such case, intraday bias will be turned back to the downside for 55 day EMA (now at 111.98). On the upside, decisive break of 114.36 resistance will confirm that corrective pull back from 118.65 has completed at 108.12. In that case, further rally would be seen to retest 118.65.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

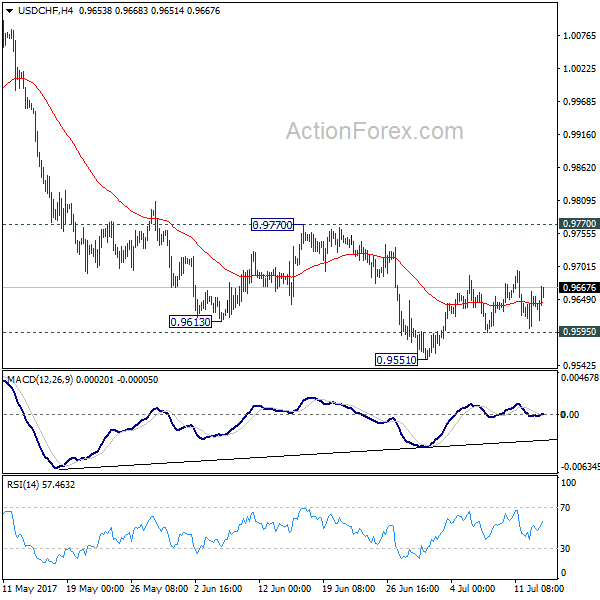

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9616; (P) 0.9639; (R1) 0.9676; More......

Intraday bias in USD/CHF remains neutral for the moment. Consolidation from 0.9551 is still in progress. In case of another rise, upside is expected to be limited by 0.9770 resistance and bring fall resumption. Below 0.9595 minor support will turn intraday bias back to the downside. In such case, USD/CHF should fall through 0.9551 support resume the whole fall from 1.0342 and target 0.9443 key support level next. We'd expect strong support from there to bring rebound. Meanwhile, firm break of 0.9770 will indicate near term reversal, on bullish convergence condition in 4 hour MACD.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

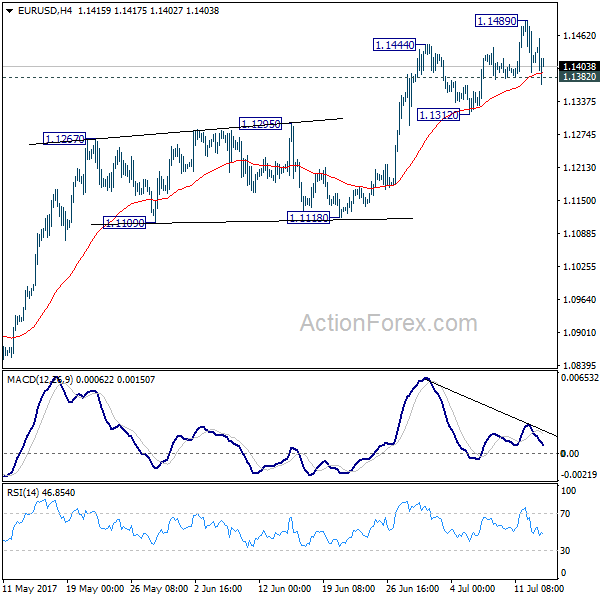

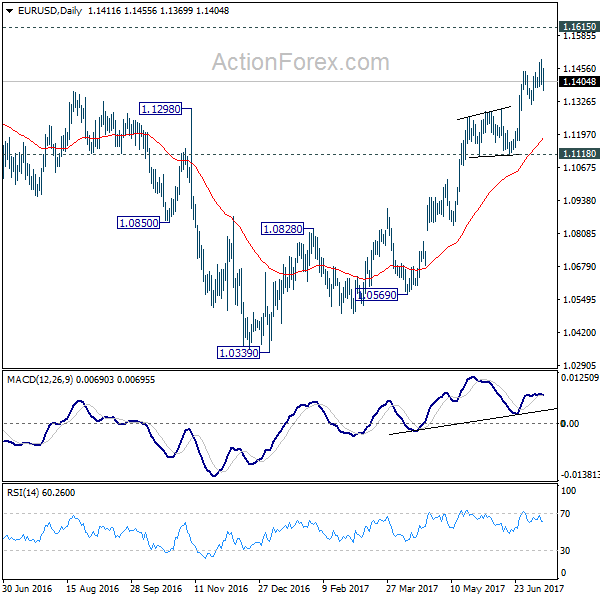

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1372; (P) 1.1430 (R1) 1.1470; More.....

EUR/USD breached 1.1382 minor support but quickly recovered. Intraday bias stays neutral first. Firm break of 1.1382 will suggest short term topping, on bearish divergence condition in 4 hour MACD. In such case, intraday bias will be turned to the downside for pull back to 55 day EMA (now at 1.1182). But downside should be contained by 1.1118 support to bring rise resumption. On the upside, break of 1.1489 will extend recent rally from 1.0339 to 1.1615 key resistance next.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1763). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

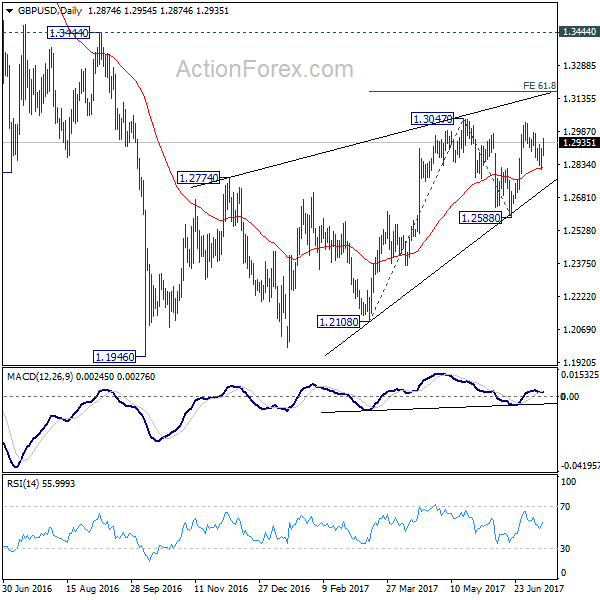

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2827; (P) 1.2867; (R1) 1.2922; More...

GBP/USD's rebound and break of 1.2926 minor resistance suggests that pull back from 1.3029 has completed at 1.2811 already. Intraday bias is turned back to the upside for 1.3029/47 resistance zone. Decisive break there will extend the larger rally to 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next. On the downside, sustained break of 1.2811 and 55 day EMA will dampen our bullish view and turn bias back to the downside for 1.2588 support instead.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

Dollar Stays Soft after Job and Inflation Data, Yen Paring Gains

Dollar trades generally weaker today except versus Yen and Canadian Dollar, where it's consolidating in oversold conditions. The greenback, nonetheless, continues to feel the weight added by dovish testimony of Fed Chair Janet Yellen. Yellen will have the second round of her testimony today but that will likely bring little news. Meanwhile, overwhelming strength is seen in Aussie and Kiwi today, as lifted by rebound in commodity prices and solid Chinese trade data. Euro, on the hand, is also struggling as traders start to turn cautious on ECB policy bets. Sterling is believed to be saved by comments from BoE hawk Ian McCafferty and rebounds against most others.

US: Solid jobs, slower inflation

US initial jobless claims dropped 3k to 247k in the week ended July 8, slightly above expectation of 245k. That's the 123 straight weeks of sub 300k reading. Four week moving average rose 2.25k to 245.75k. Continuing claims stood at 1.95m in the week ended July 1, staying below 2m for 14 straight week. Also from US, headline PPI slowed to 2.0% yoy in June but beat expectation of 1.9% yoy. Core PPI also slowed, to 1.9% yoy, below expectation of 1.9% yoy. Released from Canada, new housing price index rose 0.7% mom in May.

ECB Draghi might signal policy shift at Jackson Hole

There are talks surfacing today that ECB President Mario Draghi could make use of the Fed's Jackson Hole conference in August to address the future of ECB's monetary stimulus. That will be the first appearance in the annual conference in three years. It's generally believed that ECB will formally announce what to do after the current EUR 60b per month asset purchase ends by the year end. And Jackson Hole could be a perfect occasion for Draghi to signal the policy shift.

ECB Governing Council member Ilmars Rimsevics said on Latvian radio today that the quantitative easing problem could continue fro at least " a couple of years" He pointed out that back in June, inflation forecasts were cut to 1.5% this year and 1.3% next. He noted that "shows that the medium-term inflation target of 2 percent is not met, which means that this programme could continue for at least a couple of years."

Released from Germany, CPI was finalized at 0.2% mom, 1.6% yoy in June. From Swiss, PPI dropped -0.1% mom, -0.1% yoy in June.

BoE hawk McCafferty pushed for balance sheet unwinding

BoE hawk Ian McCafferty said in an interview that the central bank should start considering to unwind its GBP 435b assets from the quantitative easing program. While there has been talks about rate hikes, this is so far the first voice regarding unwinding. Meanwhile, McCafferty maintained his views that interest rates should be raised and would continue to vote for a hike in August meeting. He cited the solid job data released earlier this week as the support for his view. Regarding inflation, he expects it to peak at around 3% while consumer growth will slow.

BoJ to revise down inflation forecasts, up growth projections

In Japan, there are continuous speculations on BoJ's forecasts revision in July. Unnamed sources were quoted by newspaper saying the BoJ will lower fiscal 2017 inflation projection from 1.4% to somewhere between 1% and 1.4%. That would be a sensible decision as core inflation stood at 0.4% in May, well off the 2% target. On the other hand, to be in line with recent upgrade in economic assessment, BoJ could also raise growth projections.

China trade data suggests solid external demand and resilient domestic economy

China posted a trade surplus of USD 42.8b in June, widened from prior month's USD 40.8b but missed expectation of USD 43.2b. Exports jumped 11.3% yoy while imports grew 17.2% yoy. The data showed that the economy in China is holding well, with solid global demand for its exports. The domestic economy also showed much resilience. In Yuan terms, trade surplus widened to CNY 294b, up from CNY 282b and beat expectation of CNY 273b.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2827; (P) 1.2867; (R1) 1.2922; More...

GBP/USD's rebound and break of 1.2926 minor resistance suggests that pull back from 1.3029 has completed at 1.2811 already. Intraday bias is turned back to the upside for 1.3029/47 resistance zone. Decisive break there will extend the larger rally to 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next. On the downside, sustained break of 1.2811 and 55 day EMA will dampen our bullish view and turn bias back to the downside for 1.2588 support instead.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS House Price Balance Jun | 7% | 15% | 17% | |

| 01:00 | AUD | Consumer Inflation Expectation Jul | 4.40% | 3.60% | ||

| 03:22 | CNY | Trade Balance (USD) Jun | 42.8B | 43.2B | 40.8B | |

| 03:22 | CNY | Trade Balance (CNY) Jun | 294B | 273B | 282B | |

| 06:00 | EUR | German CPI M/M Jun F | 0.20% | 0.20% | 0.20% | |

| 06:00 | EUR | German CPI Y/Y Jun F | 1.60% | 1.60% | 1.60% | |

| 07:15 | CHF | Producer & Import Prices M/M Jun | -0.10% | 0.00% | -0.30% | |

| 07:15 | CHF | Producer & Import Prices Y/Y Jun | -0.10% | 0.00% | 0.10% | |

| 12:30 | CAD | New Housing Price Index M/M May | 0.70% | 0.20% | 0.80% | |

| 12:30 | USD | PPI M/M Jun | 0.10% | 0.00% | 0.00% | |

| 12:30 | USD | PPI Y/Y Jun | 2.00% | 1.90% | 2.40% | |

| 12:30 | USD | PPI Core M/M Jun | 0.10% | 0.20% | 0.30% | |

| 12:30 | USD | PPI Core Y/Y Jun | 1.90% | 2.00% | 2.10% | |

| 12:30 | USD | Initial Jobless Claims (JUL 08) | 247K | 245k | 248k | 250K |

| 14:00 | USD | Fed Chair Yellen Testifies Before Senate Banking Panel | ||||

| 14:30 | USD | Natural Gas Storage | 72 | |||

| 18:00 | USD | Monthly Budget Statement Jun | -16.2B | -88.4B |

USD/CHF Breakout Attempt, USD/CAD Undecided ahead US Numbers, EUR/JPY Challenging Crucial Support Area

USD/CHF Breakout Attempt

The currency pair is trading in the green ahead the US figures, we'll see how will react after the numbers will be released. We'll have a high volatility later, after the US data, that's why you should be careful not to suffer a heavy loss.

We have a rebound on the USD/CHF, but a further increase will come only if will have enough energy to take out an important dynamic resistance. The greenback needs support from the US economy today so we can take the lead on the short term. USDX moves sideways on the short term, right above the 95.45 previous low, an accumulation movement will bring another leg higher, but right now is premature to say what will happen because the fundamental factors could ruin everything.

Price bounced back from the outside sliding line (sl) and now is pressuring the inside sliding parallel line (sl), only a valid breakout above this level will attract more buyers on the short term. Remains under selling pressure on the Daily chart as long as is trading within the descending pitchfork's body.

Is somehow expected to decrease further after the breakdown below the ascending sliding line (SL), major support could be found at the 0.9498 and lower at the 0.9440 level. USD/CHF moves sideways on the long term, is trapped within an extended range, the corrective phase could end soon if the behavior will change (if will make higher lows).

Is better to stay away from this pair because we don't have trading opportunity, the perspective remains bearish, personally I'll wait for a reversal sign, hoping to catch an upside movement right from the bottom.

USD/CAD Undecided ahead US Numbers

The Loonie appreciated versus the USD in the morning, but now has lost some ground versus its major rival, we'll see what the US data will bring. We may have some volatility in the upcoming hours, you should keep an eye on the economic calendar later to see what will move the price.

Price dropped more than 230 pips in the yesterday's session after the BOC decision to hike the interest rate with 0.25% for the first time in the last 7 years. USD/CAD plunged much below the lower median line (LML) of the major descending pitchfork and found support only at the 1.2678 static obstacle.

The pair squeezed and closed much above the 1.2678 level and above the third warning line (wl3) of the former ascending pitchfork, a rebound could come only after the breakout above the median line (ml) of the minor descending pitchfork.

EUR/JPY Challenging Crucial Support Area

EUR/JPY is into a corrective phase and is pressuring an important support level, maintains a bullish perspective as long as is located somewhere above the 128.50 psychological level.

We had a breakdown below the upper median line (UML) of the major ascending pitchfork today, but this could be a false one and the rate will increase again. Has retested also the 38.2% retracement level and the median line (ml) of the ascending pitchfork. The outlook is bullish as long as is trading above these levels, because a breakdown below this confluence wil accelerate the sell-off.