Sample Category Title

Pound Shows Gain Despite Lukewarm UK Job Numbers

GBP/USD has posted slight losses in the Wednesday session. In North American trade, the pair is trading at 1.2880. On the release front, British employment numbers weakened. Average Earnings Index softened to 1.8%, matching the forecast. Claimant Count Change came in at 6.0 thousand, lower than the estimate of 10.5 thousand. In the US, Janet Yellen testifies before the House Financial Services Committee. On Thursday, the US releases PPI and unemployment claims. As well, Janet Yellen will testify before the Senate Banking Committee.

Is Brexit taking a bite out of the British economy? Last week's PMIs raised concerns, as the gauges of the services, manufacturing and construction sectors all pointed to weaker growth in June. Wednesday's employment numbers were not all that bad, but nevertheless were not as strong as the previous reading. Wage growth dipped to 1.8% in May, compared to 2.1% a month earlier. This marked the first reading below the 2.0% level since February 2016. Unemployment rolls expanded by 6.0 thousand, better than the forecast of 10.5 thousand. Despite softer wage growth, inflation climbed to 2.9%, its highest level in almost 4 years. This has put pressure on the BoE to increase rates, with policymakers at odds over whether to raise rates before the end of the year.

A major consequence of Brexit will be the loss of financial jobs, which will relocate from London to the continent. Frankfurt is the expected destination for many companies which will be downsizing their presence in London, but France is eager for a piece of the pie as well. The new French government wants to project a "finance-friendly" image, and on Tuesday, Prime Minister Edouard Philippe told a banking conference in Paris that he wants the city to become Europe's main financial hub after Brexit. Philippe's comments underscore that France is looking for a bigger role on the international stage, and Brexit is a unique economic and political opportunity for Philippe and President Emmanuel Macron.

All eyes are on Janet Yellen, who testifies before a congressional committee on Wednesday. Yellen's prepared remarks were released ahead of her testimony, and there were no surprises. Yellen said that the Fed is on track to raise rates and begin reducing its balance sheet before the end of the year. The markets are skeptical about another rate hike, despite the Fed optimism. This is largely due to weak inflation numbers. Although the labor market remains close to capacity, this has not translated into stronger wage growth, a key driver of inflation. The CME Group has pegged a December rate increase at just 47%, while other forecasts are pointing to odds as low as 40%. Unless growth and inflation numbers move higher, the markets are likely to remain lukewarm about the likelihood of a third rate hike in 2017.

What’s Next for the Dollar, Stocks, Bonds & Gold?

The Fed's "balance sheet reduction" may have profound implications for the dollar, gold, stocks and bonds. We'll provide an outlook.

It is said forecasts are difficult, especially when they relate to the future. Investors might want to pay attention nonetheless, not so much because I believe I have a crystal ball, but because investing is about managing risk. And there's a risk that I'm right.

Quantitative Tightening

There's a lot to cover, so let's start with what is perceived to be the elephant in the room, the Fed. In suggesting that the Fed would soon initiate balance sheet reduction, Fed Chair Janet Yellen indicated it would be like watching paint dry on a wall. Duly observant, numerous pundits agreed. With due respect, that's a bunch of baloney, but judge for yourself. Unless markets fall apart in the coming weeks, we expect that the formal announcement for the Fed's balance sheet reduction will be made this September, with a gradual stepping up in the amount the Fed will allow to "run off", i.e. the amount of maturing bonds it won't re-invest. The Fed has left many details open to interpretation, but looking at Treasuries alone, at first, $6 billion may be allowed to run off; this is gradually stepped up until $30 billion a month may be allowed to run off. It's not clear at what duration maturing bonds will be reinvested that are above the threshold, but it is plausible to roll those excesses to "fill the gaps" in subsequent months. Differently said, it's perfectly possible that the Fed will indeed allow $30 billion in Treasuries to run off once the program is fully deployed:

In addition, the Fed will allow mortgage-backed securities to run off (MBS). There's really no good reason to look at Treasuries and MBS in isolation; as such, the balance sheet reduction would be $50 billion a month if the program were to be fully deployed:

The Fed hasn't announced how small a balance sheet they want to have; based on our interpretation of discussions of current and former policy makers, this is because the Fed neither knows, nor agrees of where they want to take the balance sheet. It apparently doesn't stop the Fed from preparing the markets that they embarking on this journey because they believe they have years to make up their mind. Notably, as can be seen from the chart above, they might have until 2021. Basically, the Fed can reduce its balance sheet until excess reserves have been eliminated (this level varies on economic activity; the dashed line represents the current level of excess reserves and the potential maximum reduction holding all else equal). Whether the Fed will try to get excess reserves to zero or some other amount is an open question that not even the Fed appears to be able to answer internally.

A more convincing argument I hear as to why low volatility is structural may be that information nowadays gets absorbed more quickly. On the one hand, we have computers scan the news in milliseconds, often trading without human intervention. And we have more computing power, allowing for a more efficient implementation of any investment process. Market makers in exchange traded funds also help in the execution efficiency of markets, possibly exerting downward pressure on volatility. However, let's not forget that volatility lowered in this fashion may have the same implication as low volatility in the building up of any bubble: it is the perceived risk that is lower, not actual risk. Machines are fantastic at certain aspects, be that keeping spreads tight in an exchange traded fund, or scanning Twitter for keywords. Trades initiated in this fashion provide liquidity to the markets, but that liquidity can evaporate rather quickly when the machines go off-line. Let there be a glitch in the markets for whatever reason (say, someone dumps a large number of derivatives in off hours), and today's incarnation of automated traders tend to wait it out. In the meantime, stop loss orders of other market participants may be triggered, possibly causing flash crashes.

If reducing the Fed's balance sheet at a rate of $50 billion a month is akin to watching paint dry, what then is the ECB's activity of purchasing €60 billion a month (its current rate)? Either the Fed or the ECB is pulling our leg here. If printing money is quantitative easing (QE), then balance sheet reduction is quantitative tightening (QT). There has been a lot of debate of what sort of impact QE actually has. Skeptics of QE have pointed out that all bonds trade relative to one another, i.e. an MBS might be a substitute to a Treasury bond which in turn might be a substitute to a German bund; applying a given spread, one can take that exercise further to any number of seemingly "safe" bonds, recognizing that safety is not an absolute concept (and from a US regulatory point of view, only US Treasuries are considered "safe" as the US government can always print money to pay it back). It's in this context that the buying of MBS has been criticized as a useless digression from monetary into fiscal policy. Useless because spreads between MBS and Treasuries haven't been meaningfully impacted; and a digression into fiscal policy because buying MBS rather than Treasuries is fiscal policy given that credit is allocated to a specific sector (housing) of the economy, something in the domain of Congress, not the Fed.

So has Yellen suddenly become a critic of QE by suggesting QT is akin to watching paint dry? I doubt it; much rather, the Fed does what it continuously has been doing since the financial crisis: try to convince the markets with words. If the Fed tells you, rates rather than QT is the primary tool to set rates, it must be true, right? Please just look at the rates, ignore everything else. In the meantime, across the pond at the ECB, Draghi will tell you with a stern look that QE is responsible for everything good that has happened in the Eurozone (and that he isn't responsible for any bad side effects). You shall be excused if you are scratching your head.

It's all about risk premia

I am in the camp that believes QE has been all about compressing risk premia, i.e. the spreads between risky and so-called safe assets. With QE, junk bonds trade at less of a premium over bonds; with a #WhateverItTakes attitude, peripheral Eurozone bonds trade at less of a premium over German bunds. And equities trade at higher valuations and lower volatility? Sound familiar? Not too surprisingly then, the market has had some tantrums when the Fed first started talking about tapering; or when the Fed indicated it might start raising rates.

I'm not alone with this theory; the Fed and other central banks appear to have been petrified that stepping back from ultra-accommodative policies would cause a major revolt in the market. But then magic happened: the market presented the Fed rate hikes on a silver platter. And with two rate hikes out of the way this year, the markets are still holding up. As the markets are holding up, central bankers feel like day traders on a winning streak: they must be geniuses!

Borrowing from the picture depicting Yellen on the pressure cooker above, though, I would caution central bankers not to do a victory lap quite yet. In my mind, to stay with the analogy, some steam has been let out of the pressure cooker; and with the Fed ever more falling behind the curve, the illusion may have been created that real interest rates are moving higher, when indeed only nominal interest rates are moving higher. With QT, think about the pressure cooker shrinking while the contents remain the same; if the content of the pressure cooker is a bunch of hot air, it is well possible to further compress it.

What I'm arguing here is that QT will increase risk premia. Before we discuss implications of rising risk premia, let's consider what's happening at other central banks.

The real elephants

Above, I write about the Fed being "perceived" elephant. Only the perceived elephant, as the Fed may well have freed the shackles from other elephants, meaning the Fed may have enabled other central banks to step away from their ultra-low monetary policy. Some of those pressure cookers have cracked open now, notably the ECB's.

The ECB's program to purchase €60 billion in securities each month is running through the end of this year. As such, the market is expecting that in September, possibly a bit later, the ECB is going to announce what will happen thereafter. It appears Mr. Draghi, possibly emboldened by what's happening at the Fed (although central bankers would never express it this way; it's of course domestic considerations they are evaluating), he recently said:

"As the economy continues to recover, a constant policy stance will become more accommodative, and the central bank can accompany the recovery by adjusting the parameters of its policy instruments - not in order to tighten the policy stance, but to keep it broadly unchanged." ECB speech by ECB President Mario Draghi, June 27, 2017

You read this correctly: the ECB will remove accommodation, but it won't really and it won't call it tightening. Think: watch paint dry on the wall. He tried to pull a Yellen! You can't make this stuff up. In some ways, it reminds me of the dot-com bubble, where companies told analysts what to write into their reports, so as to avoid the necessity for analysts to actually do any thinking of their own.

Except the market didn't take Draghi's bluff and German Bunds sold off. Less than a year ago, Bunds traded at negative yields; in the aftermath of Draghi's comments, they surged from roughly 0.25% to over 0.50%. A big jump for those that watch those markets. In contrast, U.S. Treasuries are yielding 2.37% as of this writing.

Historically, the spread between U.S. Treasuries and German Bunds are highly correlated to the exchange rate between the Euro and the U.S. dollar. As German Bunds are falling (yields rise), the euro has had a tendency to rise when U.S. long-term rates don't move much. Not surprisingly, the euro has rallied quite a bit as part of this ECB induced mini taper tantrum.

To assess where we go from here, consider the following:

- What happens to Treasuries? Some argue QT will cause Treasuries to fall. My take: no, risk premia will rise. More on assets below, but w.r.t. to Treasuries rising risk premia imply deteriorating financial conditions, a headwind to economic growth. That is, Treasuries may end up not changing all that much, possibly even rise.

- What happens to Bunds? According to a standard deviation band we monitor, Draghi's comments caused Bunds to fall by 2 standard deviations versus their historic trend. That's significant and suggests real news (his speech!) caused the change. But what about going forward? Is all unwinding already priced in? This possibility cannot be ruled out, as Treasuries had their highest yields after the taper tantrum in 2013. My take is that Bernanke announced tapering not because the U.S. economy was in great shape, but because Bernanke's term was coming to an end, and he wanted to tie up loose ends. In the U.S., we've had several faulty starts to reform, most notably expectations priced in upon President Trump's election which have since fizzled out. In contrast, reform in the Eurozone is real and ongoing, most recently with French President Macron being elected not only on a strong reform platform, but also with the accompanying majority to be able to implement it. I'm not suggesting reform in the Eurozone will be perfect - it never is; but I am suggesting that real rates have room to move higher, especially relative to U.S. rates, as progress is being made.

Other central banks around the world may also be emboldened to take the foot off the accelerator. The biggest potential to catch up may well be in Sweden, where we have said for years that policy is too accommodative.

You can call the weak dollar a deflating Trump trade, but the Fed may well have initiated a far greater force by enabling other central banks to tighten. Well, don't' count on Japan to follow suit just yet.

Implications for stocks

Stocks are historically correlated to junk bonds, not because they are junk, but because they are both so-called risk assets. Just as their volatility has been compressed with QE, we believe their volatility should rise with QT. We have recently opined as to whether this time is different and volatility will remain low, but the short of it is: don't count on it.

Outbursts in the tech sector are, in the opinion of yours truly, the canary in the coal mine. The buy-the-dip mentality is wearing thin. Similarly, the end of day buying that had become routine may have turned into end-of day selling on several occasions of late. Does that mean that there isn't value out there somewhere? Possibly, but don't come crying to me if you lose money holding stocks in this environment.

Implications for gold

With rates rising, should the price of gold decline? I can see Eurozone based investors getting less enthusiastic about gold as the euro has been rising. That said, rising risk premia may be a positive for the price of gold. Because gold does not have cash flow, there's also no greater discounting of future cash flows as risk premia rise. In contrast, stocks may well be under pressure as risk premia rise. This is an academic way of saying that gold may be a valuable diversifier should stocks suffer.

Closing thoughts on Fed balance sheet

Advocates of a smaller Fed balance sheet have praised the Fed's moves to commit themselves to a reduction, making it more difficult to reverse course, especially since they have stated that interest rate policy will be separate from deciding on the size of the balance sheet. With due respect, I can't get myself to believing in the tooth-fairy anymore. First, let's keep in mind that we are likely to get a new Fed Chair early next year, meaning lots of options are on the table as to what direction a new Chair would take. More importantly, by not providing more specific parameters as to where the Fed wants to take the balance sheet, I would not be surprised if the Fed were to reverse course sooner rather than later. They won't blame it on falling stocks, but on deteriorating financial conditions (the latter may well be Fed talk for the former).

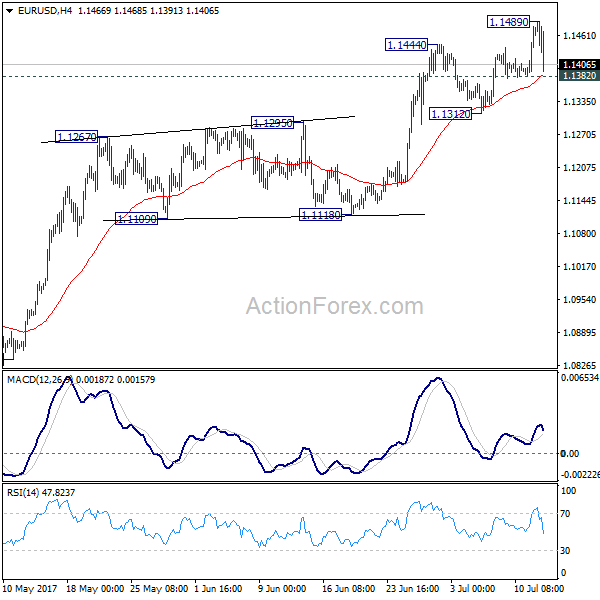

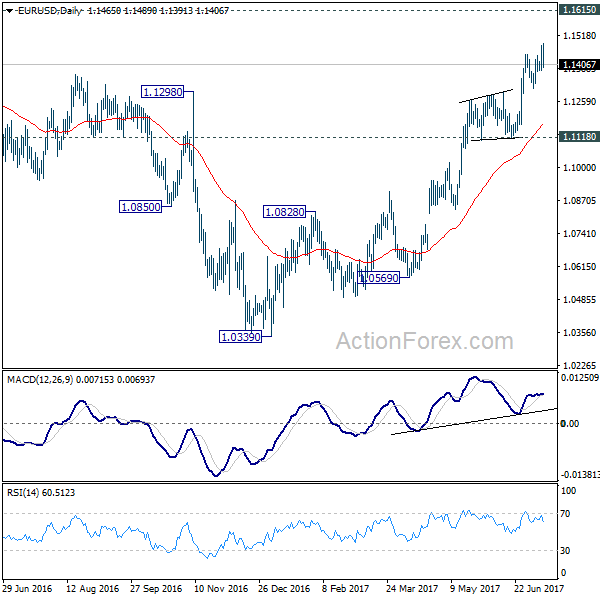

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1406; (P) 1.1442 (R1) 1.1503; More.....

EUR/USD drops sharply after hitting 1.1489 earlier today and intraday bias is turned neutral. On the downside, break of 1.1382 will suggest short term topping, possibly on bearish divergence condition in 4 hour MACD. In such case, lengthier consolidation would be seen before another rally. EUR/USD would dip back to 1.1312 support and below. On the upside, above 1.1489 will extend recent rise from 1.0339 low to 1.1615 resistance.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1763). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

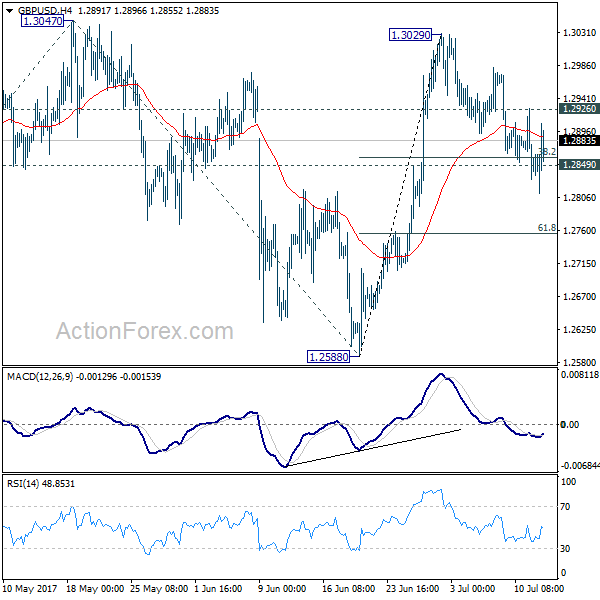

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2808; (P) 1.2868; (R1) 1.2905; More...

Intraday bias in GBP/USD remains neutral as there is no follow through selling below 1.2849 support. On the upside, break of 1.2926 minor resistance will indicate completion of pull back from 1.3029. Intraday bias would then be turned back to the upside for 1.3047 resistance. Break will target 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next. However, sustained break of 1.2849 will dampen our near term bullish view and turn focus back to 1.2588 support.

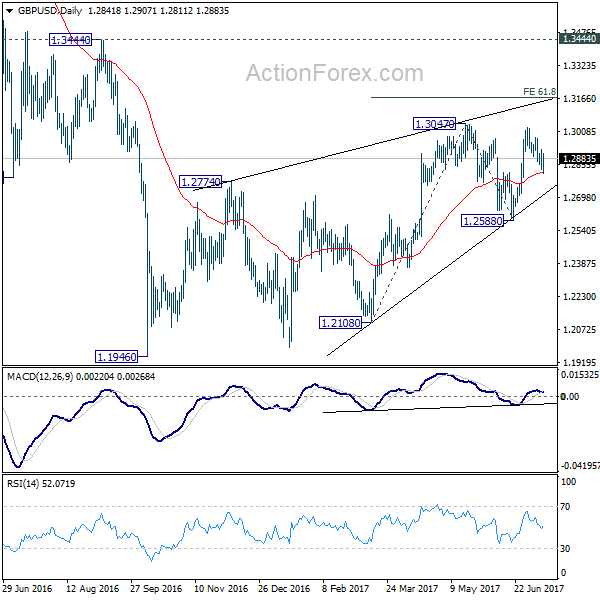

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

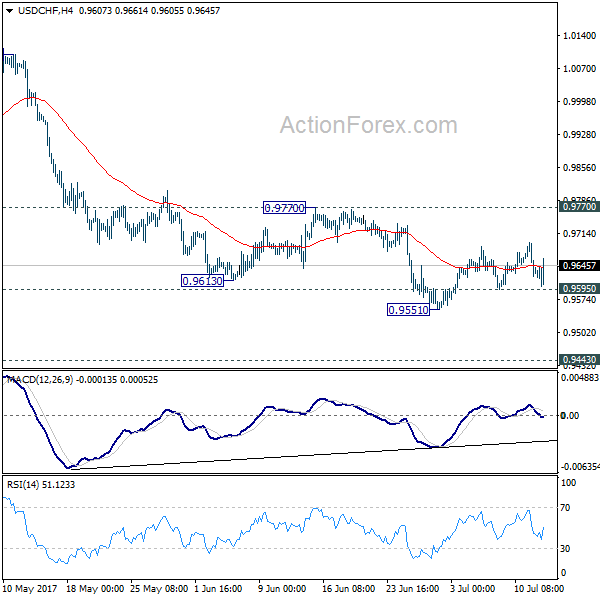

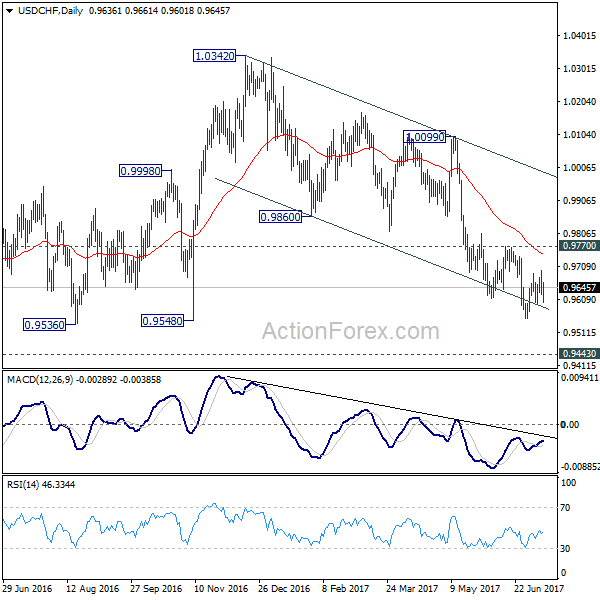

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9609; (P) 0.9652; (R1) 0.9681; More......

Intraday bias in USD/CHF remains neutral for the moment. Consolidation from 0.9551 is still in progress. In case of another rise, upside is expected to be limited by 0.9770 resistance and bring fall resumption. Below 0.9595 minor support will turn intraday bias back to the downside. In such case, USD/CHF should fall through 0.9551 support resume the whole fall from 1.0342 and target 0.9443 key support level next. We'd expect strong support from there to bring rebound. Meanwhile, firm break of 0.9770 will indicate near term reversal, on bullish convergence condition in 4 hour MACD.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

Mixed Dollar Trading on Yellen’s Testimony

- European equities ignored hesitant stock market sentiment on WS yesterday and Asia this morning because of the leaked Trump Jr. emails. Main indices gain more than 1.25%. US stock markets open around 0.6% higher as Yellen's warning on inflation puts an additional rate hike this year marginally in doubt.

- Janet Yellen has acknowledged the Fed is facing uncertainty as to when US inflation will finally pick up in response to the strengthening economy, even as she continued to chart out a course towards gradual rate rises and the unwinding of the central bank's quantitative easing programme.

- British workers saw their pay fall further behind inflation in the three months to May even as the unemployment rate hit a new 42-year low (4.5%). Today's data will have complicated the debate among Bank of England officials over the need for higher interest rates.

- France is at risk of being the only country in breach of the EMU's budgetary rules this year. The EC recommended Athens leave the EMU's "excessive deficit procedure" for countries whose budget deficit exceeds an upper limit of 3% of GDP. Greece is now ready to "turn the page on austerity and open a new chapter of growth".

- Output at the eurozone's factories, mines and utilities rose at the fastest annual pace in more than five years in May (4% Y/Y), a fresh indication that the eurozone's economic recovery picked up in the second quarter. On a monthly basis, industrial production increased by 1.3% (vs 1% M/M consensus).

- OPEC's output rose by roughly 1.4% to 32.61 million barrels a day in June, compared with May, led mainly by production increases in Libya, Nigeria, Angola, Iraq and Saudi Arabia, according to OPEC's closely watched monthly market report. Brent crude traded with a small downward bias today, heading towards $48/barrel.

- High and rising government debt levels are the biggest threat to countries' financial stability as political support for austerity wanes, ratings agency Fitch has warned.

- US President Trump defended his eldest son as "innocent" following emails that showed Donald Trump Jr. welcomed Russian help against his father's rival in the 2016 presidential election, deepening the controversy over purported Russian meddling.

- The Bank of Canada lifted its benchmark lending rate for the first time since 2010 (to 0.75%), reacting to rapid job growth and buoyant property prices, in the latest sign that global policymakers feel comfortable peeling away stimulus measures.

Rates

Subtle warning on inflation lifts US Treasuries

Global core bonds started on a decent footing. The leaked emails which related Trump's eldest son to the Russian government offer an obvious explanation at first sight. However, the story is less straight forward taking into account the recovery of the US dollar and the outperformance of European stock markets. Around European noon, both the Bund and US Note returned to opening levels as investors seemed to throw the towel on the "Trump play". It proved to be premature as core bonds shot higher after the release of Fed chair Yellen's written statement for US Congress. While her statement was nearly a copy from the June policy statement, investors focused on a modest warning on inflation. US Treasuries outperformed German Bunds. The eco calendar included only strong EMU production data, but markets ignored them.

At the time of writing, changes on the US yield curve range between -3.6 bps (2-yr) and -5.5 bps (5-yr). The German yield curve bull flattens with yields 1.2 bps (2-yr) to 3.6 bps (30-yr) lower. The underperformance of the 10-yr yield (+3.6 bps) is due to a benchmark change.

The German Finanzagentur held a €5B 10-yr Bund auction (0.5% Aug2027). Total bids amounted €5.66B, way above the €3.59B average at the previous 4 Bund auctions. The Bundesbank retained €0.99B of the amount on offer for secondary market operations, resulting in an official bid cover of 1.4 (real bid cover: 1.1). The auction tailed 2 cents. The auction yield (0.59%) was the highest since the end of 2015 and might partly explain above average demand. The Portuguese treasury tapped the on the run 10-yr and 30-yr OT's (€0.69B 4.125% Apr2027 & €0.31B 4.1% Feb2045). The combined amount sold was the maximum of the €0.75-1B with an auction bid cover of 1.71. The US Treasury continues its refinancing operation tonight with a $20B 10-yr Note auction. Currently, the WI trades around 2.3%.

Currencies

Mixed dollar trading on Yellen's testimony

The dollar started the session on a weak footing as markets pondered the potential fall-out from the Trump Jr. emails. During the day, focus turned to Yellen's statement before US Congress. Yellen basically maintained the Fed's assessment from June, but soft inflation needs close monitoring. The reaction of the dollar is mixed. USD/JPY remains under pressure. The pair dropped to the 113 area. EUR/USD reversed an initial topside test and is changing hands in the 1.1425 area.

Overnight, Asian equities traded mixed to slightly lower as investors pondered the potential impact of the Trump Jr. emails. The dollar in particular traded in the defensive. The BOJ kept interest rates low by additional bond purchases in the 3-5-yr sector. Even so, it didn't prevent a further setback of USD/JPY. EUR/USD traded also with a positive bias, setting a new correction top in the 1.1489 area. Asian investors were cautious on the dollar ahead of Yellen's testimony before US Congress.

European equities opened with remarkable resilience given the uncertainty in the US and considering the ongoing euro rally. However, there was again little consistency between markets. Core (European) yields initially declined and the rise in EUR/USD took a breather. EUR/USD returned to the mid 1.14 area. USD/JPY also stabilized in the 113.50, awaiting Fed's Yellen testimony. The Bank of Canada's policy decision was also a factor of (second tier) importance as it could be a pointer for global central bank policy normalisation. A rate rise would suggest that the likes of the ECB are also coming closer to a policy shift.

The prepared text of Yellen's testimony before the House Committee basically maintained the message from the June policy statement. The economy is expected to continue to grow at a moderate pace. Risks to the economy are balanced. Inflation remains below target, but this is probably partially due to special factors. Even so, the issue deserves close monitoring. In a first reaction interest rate differentials narrowed further against the dollar. Especially USD/JPY declined further to the low 113 area (even as equities rebounded). EUR/USD tried a retest of the recent lows, but the rebound stalled in the 1.1480 area. Afterwards, some intraday profit taking kicked in. Profit taking on the recent sharp rally in EUR/JPY might have played a role, too. USD/JPY trades in the low 113 area. EUR/USD is changing in hands around 1.1420.

Sterling rebounds on good UK labour market data

Sterling suffered further losses yesterday as markets doubted the scenario of a BoE rate hike in the near future. EUR/GBP rebounded well north of the 0.89 barrier. The glass for sterling was again half full rather than half empty today. The May UK labour market report was solid. The unemployment rate dropped to the historically low level of 4.5% and job growth was stronger than expected. Weekly earnings rose modestly from 1.8% Y/Y to 2.0% Y/Y (1.9% Y/Y was expected). This leaves real wage growth negative given a May inflation reading of 2.9%. The jury is still out what this will mean for the August policy decision. Even so, the report was good enough to trigger some profit taking on sterling shorts. EUR/GBP returned below the 0.89 barrier. The pair trades currently in the 0.8870 area, reversing most of yesterday's gain. Cable also rebounded, partially supported by underlying USD softness. The pair trades currently in the 1.2880 area.

Yen Strengthens as US Political Risk Weighs on Greenback

USD/JPY has posted losses in the Wednesday session. In the North American session, the pair is trading just above the 113 line. On the release front, Japanese PPI was unchanged at 2.1%, matching the forecast. Japanese Tertiary Activity declined 0.1%, its second decline in three months. In the US, Federal Reserve Chair Janet Yellen will testify before the House Financial Services Committee. On Thursday, the US releases PPI and unemployment claims. As well, Janet Yellen will testify before the Senate Banking Committee.

All eyes are on Janet Yellen, who testifies before a congressional committee on Wednesday. Yellen's prepared remarks were released ahead of her testimony, and there were no surprises. Yellen said that the Fed is on track to raise rates and begin reducing its balance sheet before the end of the year. The markets are skeptical about another rate hike, despite the Fed optimism. This is largely due to weak inflation numbers. Although the labor market remains close to capacity, this has not translated into stronger wage growth, a key driver of inflation. The CME Group has pegged a December rate increase at just 47%, while other forecasts are pointing to odds as low as 40%. Unless growth and inflation numbers move higher, the markets are likely to remain lukewarm about the likelihood of a third rate hike in 2017.

Japan's economy has improved in 2017, buoyed by a stronger global economy. This has translated into increased demand for Japanese goods and has boosted the manufacturing and export sectors. The Tankan Manufacturing Index jumped to 17 in the first quarter, its strongest showing since 2014. On Tuesday, Preliminary Machine Tool Orders improved in June to 31.1%, up from 24.4% a month earlier. We'll get a look at Preliminary Industrial Production on Friday. The indicator recorded a strong gain of 4.0% in April, but the markets are braced for a sharp downturn in June, with an estimate of -3.3%.

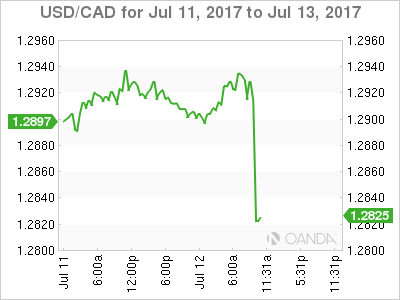

Bank of Canada (BoC) Hikes Rates, Loonie Soars

The Bank of Canada raised its policy rate Wednesday to +0.75% from 0.50%, its first increase in seven years, on an improving economic outlook that's soaking up unused labor and production capacity at a "significant" pace.

USD/CAD down -0.6% to C$1.2834

Comments:

- BOC: Recent Data Have Bolstered Confidence in Outlook

- BOC: Canadian Economy "Has Been Robust"

- BOC: Outlook "Warrants Withdrawal of Some" Monetary Stimulus

- BOC: Future Rate Decisions to Be Guided By Data

- BOC: Mindful of Trade-Policy Uncertainty, Financial Stability

- BOC: "Significant Amount" of Economic Slack Has Been Absorbed

- BOC: Output Gap to Close By End of 2017

- BOC: Upgrades 2017 Growth to 2.8%, 2018 Growth to 2%

- BOC: Forecasts 3% Annualized Growth in 2Q, 2% in 3Q

- BOC: Growth Becoming More Sustainable; Broadening Across Regions, Sectors

- BOC: Exports Should Make "Increasing Contribution" to Growth

- BOC: Softness in CPI Due to Temporary Factors

- BOC: Expects Inflation to Return "Close" to 2% Target By Mid-2018

- BOC: Appropriate To Raise Rates Given Lag Between Monetary Policy, Future CPI

DAX Posts Gains as Markets Optimistic Ahead of Yellen Testimony

The DAX index has posted gains in the Wednesday session, as the index is up 0.70% on the day. Currently, the DAX is at 12,525.50. On the release front, German WPI improved to 0.0%, but fell short of the estimate of 0.2%. Eurozone Industrial Production impressed with a gain of 1.3%. In the US, Federal Reserve Chair Janet Yellen will testify before the House Financial Services Committee. Yellen testifies before the Senate Banking Committee on Thursday. On Thursday, Germany publishes Final CPI, which is expected to show a weak gain of 0.2%.

Germany has been the catalyst of an improved eurozone economy, but Europe's largest economy has not been immune to chronically weak inflation levels. German WPI, an important inflation index, came in at a flat 0.0% in June. The ECB has taken pains to reiterate that it has no plans to exit its aggressive stimulus program until inflation climbs closer to the ECB's target of 2.0%. However, the central bank has stumbled in getting its message across, as evidenced by the euro rally after the markets seized on Mario Draghi's comments at the recent ECB forum of central bankers. We'll get a look at German Final CPI on Thursday. The index has looked weak in second quarter readings, and the estimate for June is just 0.2%.

Aside from strong economic growth, Germany can also boast fiscal stability, despite trying economic conditions in the eurozone. The question of the fiscal stance of the eurozone as a whole was a key topic as eurozone finance ministers met in Brussels this week. Germany has opposed attempts to define the bloc's fiscal stance as expansionary, and at the Monday meeting, the finance ministers agreed to water this down to a"broadly neutral" stance. The European Commission wants to see France and Italy work on trimming their substantial deficits. As for Germany, which is in much better fiscal shape, the Eurogroup of finance ministers has called on the country to divert more resources to investment and public spending.

The Trump show is again on center stage in Washington, with more revelations about alleged secret ties between Russia and the Trump administration during the US election. This week's breaking news is that Donald Trump Jr. admitted that a Russian official contacted him and offered to provide him with evidence incriminating Hillary Clinton. Trump and the White House are trying to lower the flames and put a positive spin on the meeting, but the media and lawmakers (including Republicans) aren't about to let Trump off the hook. This crisis is just the latest miscue for the Trump administration, which hasn't been able to pass any significant laws through Congress, even though Republicans control both the House of Representatives and the Senate. The latest dark cloud over the White House has dampened investor confidence in the US economy, and European stock markets could take advantage of the latest political scandal in the US.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2884; (P) 1.2914; (R1) 1.2943; More....

USD/CAD's decline continues today and reaches as low as 1.2815. Intraday bias remains on the downside. Current decline from 1.3793 is on course to retest 1.2460 low. On the upside, break of 1.2942 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The second leg should have finished at 1.3793. Break of 1.2460 will extend such correction to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.