Sample Category Title

Canadian Dollar Surges as BoC Raises Overnight Rate to 0.75%, Open to Further Hike

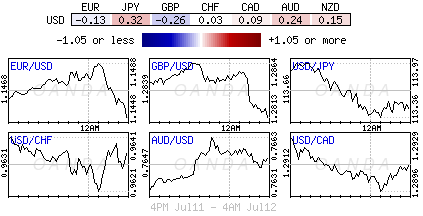

Canadian Dollar surges broadly as BoC delivered the highly anticipated rate hike as widely expected. The overnight rate target was raised by 25bps to 0.75%. More importantly, the central bank delivered a upbeat outlook and adopts an open stance to further policy adjustments. USD/CAD extends recent decline to as low as 1.2824 and is still on course to retest 2016 low at 1.2460. EUR/CAD drops through recent support at 1.4649 and is heading to 1.4597 key near term support level.

BoC noted that "recent data have bolstered the Bank's confidence in its outlook for above-potential growth and the absorption of excess capacity in the economy." And "acknowledges recent softness in inflation but judges this to be temporary."

GDP growth is expected to moderate to 2.8% in 2017, 2.0% in 2018 and 1.6% in 2019. More importantly, "output gap is now projected to close around the end of 2017, earlier than the Bank anticipated in its April Monetary Policy Report (MPR)."

Regarding inflation, BoC acknowledged that three measures of core inflation all remained below 2%. But said that "the factors behind soft inflation appear to be mostly temporary, including heightened food price competition, electricity rebates in Ontario, and changes in automobile pricing". It projects inflation to return to 2% by the middle of 2018.

BoC concluded by stating that "future adjustments to the target for the overnight rate will be guided by incoming data as they inform the Bank's inflation outlook, keeping in mind continued uncertainty and financial system vulnerabilities." This suggests that it's open to further rate hike if data supports.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2884; (P) 1.2914; (R1) 1.2943; More....

USD/CAD's decline continues today and reaches as low as 1.2815. Intraday bias remains on the downside. Current decline from 1.3793 is on course to retest 1.2460 low. On the upside, break of 1.2942 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The second leg should have finished at 1.3793. Break of 1.2460 will extend such correction to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.

(BOC) Bank of Canada Increases Overnight Rate Target to 3/4 Per cent

The Bank of Canada is raising its target for the overnight rate to 3/4 per cent. The Bank Rate is correspondingly 1 per cent and the deposit rate is 1/2 per cent. Recent data have bolstered the Bank's confidence in its outlook for above-potential growth and the absorption of excess capacity in the economy. The Bank acknowledges recent softness in inflation but judges this to be temporary. Recognizing the lag between monetary policy actions and future inflation, Governing Council considers it appropriate to raise its overnight rate target at this time.

The global economy continues to strengthen and growth is broadening across countries and regions. The US economy was tepid in the first quarter of 2017 but is now growing at a solid pace, underpinned by a robust labour market and stronger investment. Above-potential growth is becoming more widespread in the euro area. However, elevated geopolitical uncertainty still clouds the global outlook, particularly for trade and investment. Meanwhile, world oil prices have softened as markets work toward a new supply/demand balance.

Canada's economy has been robust, fuelled by household spending. As a result, a significant amount of economic slack has been absorbed. The very strong growth of the first quarter is expected to moderate over the balance of the year, but remain above potential. Growth is broadening across industries and regions and therefore becoming more sustainable. As the adjustment to lower oil prices is largely complete, both the goods and services sectors are expanding. Household spending will likely remain solid in the months ahead, supported by rising employment and wages, but its pace is expected to slow over the projection horizon. At the same time, exports should make an increasing contribution to GDP growth. Business investment should also add to growth, a view supported by the most recent Business Outlook Survey.

The Bank estimates real GDP growth will moderate further over the projection horizon, from 2.8 per cent in 2017 to 2.0 per cent in 2018 and 1.6 per cent in 2019. The output gap is now projected to close around the end of 2017, earlier than the Bank anticipated in its April Monetary Policy Report (MPR).

CPI inflation has eased in recent months and the Bank's three measures of core inflation all remain below 2 per cent. The factors behind soft inflation appear to be mostly temporary, including heightened food price competition, electricity rebates in Ontario, and changes in automobile pricing. As the effects of these relative price movements fade and excess capacity is absorbed, the Bank expects inflation to return to close to 2 per cent by the middle of 2018. The Bank will continue to analyze short-term inflation fluctuations to determine the extent to which it remains appropriate to look through them.

Governing Council judges that the current outlook warrants today's withdrawal of some of the monetary policy stimulus in the economy. Future adjustments to the target for the overnight rate will be guided by incoming data as they inform the Bank's inflation outlook, keeping in mind continued uncertainty and financial system vulnerabilities.

Information note

The next scheduled date for announcing the overnight rate target is September 6, 2017. The next full update of the Bank's outlook for the economy and inflation, including risks to the projection, will be published in the MPR on October 25, 2017.

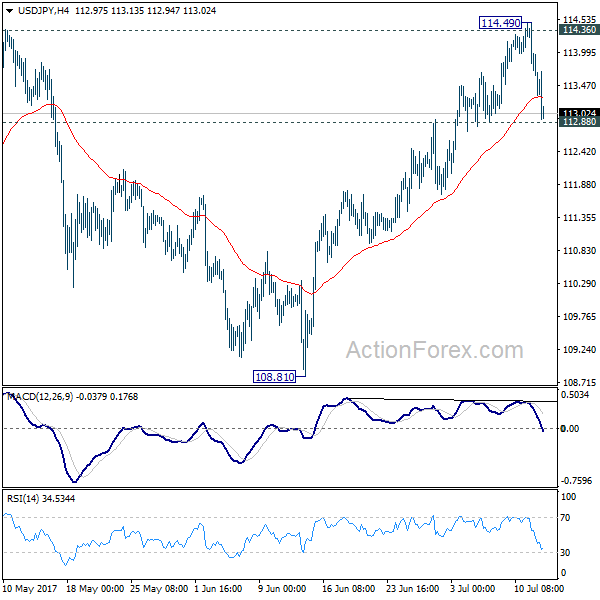

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.60; (P) 114.05; (R1) 114.38; More...

Intraday bias in USD/JPY remains neutral with focus on 112.88 minor support. Firm break there will argue that rebound from 108.81 has completed at 114.49 after being rejected by 114.36 key near term resistance. That would also argue that the correction from 118.65 is still in progress. In such case, intraday bias will be turned back to the downside for 55 day EMA (now at 111.94). On the upside, decisive break of 114.36 resistance will confirm that corrective pull back from 118.65 has completed at 108.12. In that case, further rally would be seen to retest 118.65.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Dollar Mixed as Fed Yellen Sounds Balanced, Sterling Rebounds on Job Data

Dollar trades mixed in early US session as Fed chair Janet Yellen sounds balanced in her prepared speech for the testimony to Congress. The greenback is trying to rebound against Euro at the time of writing. Though, that's mainly due to Euro's own weakness after yesterday's rally. And the greenback is staying weak against Yen and Aussie. Sterling rebounds today on better than expected job data and is firm against Dollar too. Canadian Dollar is treading water as markets await BoC rate decision.

Fed Yellen sounds balanced

In her prepared remarks for the Congressional testimony, Fed chair Janet Yellen warned that there are "considerable uncertainty always attends the economic outlook," and "there is, for example, uncertainty about when -- and how much -- inflation will respond to tightening resource utilization." Nonetheless, for now, she maintained that the Fed "continues to expect that the evolution of the economy will warrant gradual increases in the federal funds rate over time." And, Fed should start reducing the USD 4T balance sheet this year.

Regarding the economy, Yellen said that "ongoing job gains should continue to support the growth of incomes and, therefore, consumer spending; global economic growth should support further gains in U.S. exports; and favorable financial conditions, coupled with the prospect of continued gains in domestic and foreign spending and the ongoing recovery in drilling activity, should continue to support business investment." Also, "these developments should increase resource utilization somewhat further, thereby fostering a stronger pace of wage and price increases."

Sterling rebounds on job data, Broadbent confirmed his stance

Sterling rebounds today as supported by better than expected employment data. Unemployment rate dropped to 4.5% in the quarter to May, hitting the lowest level in 42 years since 1975. Unemployment dropped 64k during the quarter to just under 1.5m. Average weekly earnings rose 1.8% 3moy in May, in line with consensus. Claimant count rose 6k in June versus expectation of 10.4k.

BoE Deputy Governor Ben Broadbent clarified his stance on monetary policy in a newspaper interview. He said that "there is reason to see the committee moving in that direction" regarding rate hike, but "there are still a lot of imponderables." And, "it is a bit tricky at the moment to make a decision." But overall "I am not ready to do it yet". It's now clear that Broadbent will not vote for a rate hike in August BoE meeting.

EU Barnier: Still major differences with UK on Brexit

EU's chief Brexit negotiator Michael Barnier warned that there are still major differences between EU and UK regarding citizens rights. And he complained that "the British position does not allow those persons concerned to continue to live their lives as they do today." Also, he emphasized that the European Court of Justice has to be the "ultimate guarantor of those rights".

Barnier also hit back at UK Foreign Secretary Boris Johnson's comment that EU could "go whistle" over the demand regarding the divorce bill. Barnier said that "I'm no hearing any whistling, just the clock ticking". He reiterated that "it's not an exit bill, it is not a ransom" and, "we won't ask for anything else than what the UK has committed to as a member."

Australian consumer confidence improved

Australia Westpac consumer confidence snapped three months of decline and rose 0.4% in July. However, Westpac noted that "this is the eighth consecutive month where the Index has printed below 100 indicating that pessimists continue to outnumber optimists. The Index is not sending encouraging signals about the outlook for consumer spending." Meanwhile, they expect RBA to be on hold "throughout the remainder of 2017 and 2018". And, "a cautious consumer; a slowing housing market; and a weakening in the labour market with limited prospects of any boost to wages growth all point to another year of steady policy".

Subdued Inflation Facilitates PBOC's Monetary Policy

The set of June data released so far has pointed to a steady growth trend in China, the world's second largest economy. Released earlier in the week, headline CPI stayed unchanged at 1.5%yoy in June, shy of consensus of 1.6%. Persistently soft food price (on deflation) continued to put downward pressure on the headline reading. For instance, pork plummeted -16.7 and egg price fell -9.3%.PPI, upstream price levels, steadied at 5.5% in June, in line with expectations. Subdued inflation offers the government room to maintain its targeted tightening measures, focusing on cracking down overheating asset prices. Yet, soft PPI suggested that growth in industrial profits would be limited. More in China's Watch: Subdued Inflation Facilitates PBOC's Monetary Policy.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.60; (P) 114.05; (R1) 114.38; More...

Intraday bias in USD/JPY remains neutral with focus on 112.88 minor support. Firm break there will argue that rebound from 108.81 has completed at 114.49 after being rejected by 114.36 key near term resistance. That would also argue that the correction from 118.65 is still in progress. In such case, intraday bias will be turned back to the downside for 55 day EMA (now at 111.94). On the upside, decisive break of 114.36 resistance will confirm that corrective pull back from 118.65 has completed at 108.12. In that case, further rally would be seen to retest 118.65.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Jun | 2.10% | 2.10% | 2.10% | |

| 0:30 | AUD | Westpac Consumer Confidence Jul | 0.40% | -1.80% | ||

| 4:30 | JPY | Tertiary Industry Index M/M May | -0.10% | -0.60% | 1.20% | 1.40% |

| 8:30 | GBP | Jobless Claims Change Jun | 6.0K | 10.4K | 7.3K | |

| 8:30 | GBP | Claimant Count Rate Jun | 2.30% | 2.30% | ||

| 8:30 | GBP | ILO Unemployment Rate 3M May | 4.50% | 4.60% | 4.60% | |

| 8:30 | GBP | Average Weekly Earnings 3M/Y May | 1.80% | 1.80% | 2.10% | |

| 9:00 | EUR | Eurozone Industrial Production M/M May | 1.30% | 1.00% | 0.50% | 0.30% |

| 14:00 | CAD | BoC Rate Decision | 0.75% | 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | -6.3M | |||

| 15:15 | CAD | BoC Press Conference |

(FED) Chair Janet L. Yellen – Semiannual Monetary Policy Report to the Congress

Chairman Hensarling, Ranking Member Waters, and other members of the Committee, I am pleased to present the Federal Reserve's semiannual Monetary Policy Report to the Congress. In my remarks today I will briefly discuss the current economic situation and outlook before turning to monetary policy.

Current Economic Situation and Outlook

Since my appearance before this committee in February, the labor market has continued to strengthen. Job gains have averaged 180,000 per month so far this year, down only slightly from the average in 2016 and still well above the pace we estimate would be sufficient, on average, to provide jobs for new entrants to the labor force. Indeed, the unemployment rate has fallen about 1/4 percentage point since the start of the year, and, at 4.4 percent in June, is 5‑1/2 percentage points below its peak in 2010 and modestly below the median of Federal Open Market Committee (FOMC) participants' assessments of its longer-run normal level. The labor force participation rate has changed little, on net, this year--another indication of improving conditions in the jobs market, given the demographically driven downward trend in this series. A broader measure of labor market slack that includes workers marginally attached to the labor force and those working part time who would prefer full-time work has also fallen this year and is now nearly as low as it was just before the recession. It is also encouraging that jobless rates have continued to decline for most major demographic groups, including for African Americans and Hispanics. However, as before the recession, unemployment rates for these minority groups remain higher than for the nation overall.

Meanwhile, the economy appears to have grown at a moderate pace, on average, so far this year. Although inflation-adjusted gross domestic product is currently estimated to have increased at an annual rate of only 1-1/2 percent in the first quarter, more-recent indicators suggest that growth rebounded in the second quarter. In particular, growth in household spending, which was weak earlier in the year, has picked up in recent months and continues to be supported by job gains, rising household wealth, and favorable consumer sentiment. In addition, business fixed investment has turned up this year after having been soft last year. And a strengthening in economic growth abroad has provided important support for U.S. manufacturing production and exports. The housing market has continued to recover gradually, aided by the ongoing improvement in the labor market and mortgage rates that, although up somewhat from a year ago, remain at relatively low levels.

With regard to inflation, overall consumer prices, as measured by the price index for personal consumption expenditures, increased 1.4 percent over the 12 months ending in May, up from about 1 percent a year ago but a little lower than earlier this year. Core inflation, which excludes energy and food prices, has also edged down in recent months and was 1.4 percent in May, a couple of tenths below the year-earlier reading. It appears that the recent lower readings on inflation are partly the result of a few unusual reductions in certain categories of prices; these reductions will hold 12-month inflation down until they drop out of the calculation. Nevertheless, with inflation continuing to run below the Committee's 2 percent longer-run objective, the FOMC indicated in its June statement that it intends to carefully monitor actual and expected progress toward our symmetric inflation goal.

Looking ahead, my colleagues on the FOMC and I expect that, with further gradual adjustments in the stance of monetary policy, the economy will continue to expand at a moderate pace over the next couple of years, with the job market strengthening somewhat further and inflation rising to 2 percent. This judgment reflects our view that monetary policy remains accommodative. Ongoing job gains should continue to support the growth of incomes and, therefore, consumer spending; global economic growth should support further gains in U.S. exports; and favorable financial conditions, coupled with the prospect of continued gains in domestic and foreign spending and the ongoing recovery in drilling activity, should continue to support business investment. These developments should increase resource utilization somewhat further, thereby fostering a stronger pace of wage and price increases.

Of course, considerable uncertainty always attends the economic outlook. There is, for example, uncertainty about when--and how much--inflation will respond to tightening resource utilization. Possible changes in fiscal and other government policies here in the United States represent another source of uncertainty. In addition, although the prospects for the global economy appear to have improved somewhat this year, a number of our trading partners continue to confront economic challenges. At present, I see roughly equal odds that the U.S. economy's performance will be somewhat stronger or somewhat less strong than we currently project.

Monetary Policy

I will now turn to monetary policy. The FOMC seeks to foster maximum employment and price stability, as required by law. Over the first half of 2017, the Committee continued to gradually reduce the amount of monetary policy accommodation. Specifically, the FOMC raised the target range for the federal funds rate by 1/4 percentage point at both its March and June meetings, bringing the target to a range of 1 to 1-1/4 percent. In doing so, the Committee recognized the considerable progress the economy had made--and is expected to continue to make--toward our mandated objectives.

The Committee continues to expect that the evolution of the economy will warrant gradual increases in the federal funds rate over time to achieve and maintain maximum employment and stable prices. That expectation is based on our view that the federal funds rate remains somewhat below its neutral level--that is, the level of the federal funds rate that is neither expansionary nor contractionary and keeps the economy operating on an even keel. Because the neutral rate is currently quite low by historical standards, the federal funds rate would not have to rise all that much further to get to a neutral policy stance. But because we also anticipate that the factors that are currently holding down the neutral rate will diminish somewhat over time, additional gradual rate hikes are likely to be appropriate over the next few years to sustain the economic expansion and return inflation to our 2 percent goal. Even so, the Committee continues to anticipate that the longer-run neutral level of the federal funds rate is likely to remain below levels that prevailed in previous decades.

As I noted earlier, the economic outlook is always subject to considerable uncertainty, and monetary policy is not on a preset course. FOMC participants will adjust their assessments of the appropriate path for the federal funds rate in response to changes to their economic outlooks and to their judgments of the associated risks as informed by incoming data. In this regard, as we noted in the FOMC statement last month, inflation continues to run below our 2 percent objective and has declined recently; the Committee will be monitoring inflation developments closely in the months ahead.

In evaluating the stance of monetary policy, the FOMC routinely consults monetary policy rules that connect prescriptions for the policy rate with variables associated with our mandated objectives. However, such prescriptions cannot be applied in a mechanical way; their use requires careful judgments about the choice and measurement of the inputs into these rules, as well as the implications of the many considerations these rules do not take into account. I would like to note the discussion of simple monetary policy rules and their role in the Federal Reserve's policy process that appears in our current Monetary Policy Report.

Balance Sheet Normalization

Let me now turn to our balance sheet. Last month the FOMC augmented its Policy Normalization Principles and Plans by providing additional details on the process that we will follow in normalizing the size of our balance sheet. The Committee intends to gradually reduce the Federal Reserve's securities holdings by decreasing its reinvestment of the principal payments it receives from the securities held in the System Open Market Account. Specifically, such payments will be reinvested only to the extent that they exceed gradually rising caps. Initially, these caps will be set at relatively low levels to limit the volume of securities that private investors will have to absorb. The Committee currently expects that, provided the economy evolves broadly as anticipated, it will likely begin to implement the program this year.

Once we start to reduce our reinvestments, our securities holdings will gradually decline, as will the supply of reserve balances in the banking system. The longer-run normal level of reserve balances will depend on a number of as-yet-unknown factors, including the banking system's future demand for reserves and the Committee's future decisions about how to implement monetary policy most efficiently and effectively. The Committee currently anticipates reducing the quantity of reserve balances to a level that is appreciably below recent levels but larger than before the financial crisis.

Finally, the Committee affirmed in June that changing the target range for the federal funds rate is our primary means of adjusting the stance of monetary policy. In other words, we do not intend to use the balance sheet as an active tool for monetary policy in normal times. However, the Committee would be prepared to resume reinvestments if a material deterioration in the economic outlook were to warrant a sizable reduction in the federal funds rate. More generally, the Committee would be prepared to use its full range of tools, including altering the size and composition of its balance sheet, if future economic conditions were to warrant a more accommodative monetary policy than can be achieved solely by reducing the federal funds rate.

Thank you. I would be pleased to take your questions.

DAX Posts Gains as Markets Optimistic Ahead of Yellen Testimony

The DAX index has posted gains in the Wednesday session, as the index is up 0.70% on the day. Currently, the DAX is at 12,525.50. On the release front, German WPI improved to 0.0%, but fell short of the estimate of 0.2%. Eurozone Industrial Production impressed with a gain of 1.3%. In the US, Federal Reserve Chair Janet Yellen will testify before the House Financial Services Committee. Yellen testifies before the Senate Banking Committee on Thursday. On Thursday, Germany publishes Final CPI, which is expected to show a weak gain of 0.2%.

Germany has been the catalyst of an improved eurozone economy, but Europe's largest economy has not been immune to chronically weak inflation levels. German WPI, an important inflation index, came in at a flat 0.0% in June. The ECB has taken pains to reiterate that it has no plans to exit its aggressive stimulus program until inflation climbs closer to the ECB's target of 2.0%. However, the central bank has stumbled in getting its message across, as evidenced by the euro rally after the markets seized on Mario Draghi's comments at the recent ECB forum of central bankers. We'll get a look at German Final CPI on Thursday. The index has looked weak in second quarter readings, and the estimate for June is just 0.2%.

Aside from strong economic growth, Germany can also boast fiscal stability, despite trying economic conditions in the eurozone. The question of the fiscal stance of the eurozone as a whole was a key topic as eurozone finance ministers met in Brussels this week. Germany has opposed attempts to define the bloc's fiscal stance as expansionary, and at the Monday meeting, the finance ministers agreed to water this down to a"broadly neutral" stance. The European Commission wants to see France and Italy work on trimming their substantial deficits. As for Germany, which is in much better fiscal shape, the Eurogroup of finance ministers has called on the country to divert more resources to investment and public spending.

The Trump show is again on center stage in Washington, with more revelations about alleged secret ties between Russia and the Trump administration during the US election. This week's breaking news is that Donald Trump Jr. admitted that a Russian official contacted him and offered to provide him with evidence incriminating Hillary Clinton. Trump and the White House are trying to lower the flames and put a positive spin on the meeting, but the media and lawmakers (including Republicans) aren't about to let Trump off the hook. This crisis is just the latest miscue for the Trump administration, which hasn't been able to pass any significant laws through Congress, even though Republicans control both the House of Representatives and the Senate. The latest dark cloud over the White House has dampened investor confidence in the US economy, and European stock markets could take advantage of the latest political scandal in the US.

USDCHF Weakens, Eyes Further Bearishness

USDCHF: With the pair closing lower on Tuesday, further bearishness is envisaged. On the downside, support lies at the 0.9600 level. A turn below here will open the door for more weakness towards the 0.9550 level and then the 0.9500 level. Its daily RSI is bearish and pointing lower suggesting further weakness. On the upside, resistance resides at the 0.9700 level where a break will clear the way for more strength to occur towards the 0.9750 level. Further out, resistance comes in at the 0.9800 level. All in all, USDCHF faces further downside threats on price rejection.

USD/CAD Hike or Disappointment? USD/JPY Rejected by Resistance Area, EUR/GBP Targeting New Peaks

USD/CAD Hike or Disappointment?

We have a busy day as the Bank of Canada will publish the Overnight Rate, as you already know, the economists have forecasted an increase from 0.50% to 0.75%. A rate hike will help the Loonie to stay higher and to try to increase versus its rivals.

We'll see what will happen because the rate hike could be priced in and the USD/CAD could ignore this big event. Price is trading in the green and is fighting hard to 1.2943 yesterday's high, has climbed above a broken support, but unfortunately is still under massive selling pressure.

Maybe will be better to stay away this pair later because we may have a huge volatility and you could suffer a heavy loss. I want to say that a disappointment coming from the BOC will send the USD/CAD much higher on the short term.

Is struggling to increase after the massive sell-off, has found support right above the median line (ML) of the major descending pitchfork, signalling that is too oversold to drop further. Actually we have a false breakdown below the confluence area formed by the median line (ml) of the minor descending pitchfork with the second warning line (wl2) of the former minor ascending pitchfork.

Technically, we should have another leg higher on the short term after the failure to reach the ML and after the false breakdown, but we'll see how will react after the BOC. The next upside target will be at the 23.6% retracement level, 1.3047 static resistance and at the upper median line (uml) of the minor descending pitchfork.

USD/JPY Rejected by Resistance Area

Looks like that the minor upside momentum is completed and now we could have a minor decrease on the short term. Has decreased today also because the Nikkei stock index has slipped lower today to test and retest the 20058 static support (resistance turned into support).

The USD/JPY continues to move sideways after the failure to stabilize above the 114.00 psychological level, also dropped below the 113.50 level. Will increase further only if the JP225 index will have enough energy to stay above the 20058 and to climb towards the 20320 previous high.

USD/JPY founded strong resistance right above the short term 23.6% retracement level and now plunged much below the long term 23.6% retracement level. Is approaching the upside line of the former symmetrical triangle, where he could find support again, could only retest the chart pattern before will increase again. A larger increase will be confirmed only after a valid breakout above the WL3.

EUR/GBP Targeting New Peaks

Price rallied in the yesterday's session and broken above a strong dynamic resistance and looks like that we have confirmation that will increase further in the upcoming weeks.

Has found temporary resistance at 0.8948 today and could decrease to test and retest the wl2 broken resistance before will climb much higher. Price has finally escaped from the extended sideways movement, the major upside targets are at the 0.9226 level and at the upper median line (UML) of the ascending pitchfork.

Dollar Sluggish ahead of Yellen’s Testimony

The Greenback was neatly packaged and delivered to bears during Tuesday's trading session, following reports of emails that show President Donald Trump's eldest son met with a Kremlin-linked Russian lawyer prior to the US general elections last November. This fresh revelation has added to the political uncertainty in Washington and may delay the proposed tax reforms & infrastructure spending plans. With the Dollar Index under intense selling pressure on the daily charts, Dollar bullish investors are likely to search for fresh inspiration to support prices from Janet Yellen's Congress testimony later today.

Yellen is scheduled to testify on the economy before the House Financial Services Committee this afternoon; her remarks will be closely scrutinized for clues on when the Federal Reserve plans to raise rates. While markets expect Yellen to reiterate her hawkish remarks and upbeat outlook on the US economy, this may not be enough to support the US Dollar. Investors not only need fresh insight on when the Federal Reserve plans to raise rates, but also require greater clarity on the timings and magnitude of the balance sheet reduction. It will also be very interesting to hear Yellen's thoughts on falling inflation rates and tepid wage growth, and how these may impact the Fed's path to monetary policy normalization.

A situation where nothing new is brought to the table may punish the vulnerable Greenback further. From a technical standpoint, the Dollar Index is pressured on the daily charts. A breakdown below 95.50 may open a direct path towards 95.00.

Sterling gifted a lifeline

Sterling bulls were offered a lifeline on Wednesday following a mixed UK employment report that slightly eased some Brexit-related concerns. The UK employment market continued to display resilience against Brexit, with the unemployment rate falling to 4.5% for the three months to May, marking a landmark 42-year low. Despite the encouraging jobs picture, wage growth disappointed, signalling another fall in total earnings. With inflation outpacing wage growth, British consumers are seeing their spending power diminish and as such, may fuel concerns over the longevity of the UK's consumer-driven economic growth. This simply takes us back to the question - will the Bank of England be willing to raise interest rates during such fragile economic conditions? Markets may pay very close attention to the UK's macro fundamentals, political developments in Westminster and Brexit talks for further clues on what actions the BoE may take.

Will BoC Poloz Lift The Loonie Higher?

The Bank of Canada is widely expected today (10:00 am EDT) to raise its benchmark policy rate for the first time in seven years. It would be a strong signal from policy makers that the Canadian economy is on the path to recovery after years of tepid growth following the global slump in commodities.

The majority who expect a rate hike of +25 bps to +0.75% cite the bullish shift in central bank communications about the outlook and data signalling Canadian output is expanding at its fastest pace in nearly three years.

However, inflation is not pressing, but most G7 economies indicate that they can live with interest rates a tad higher than they are at present and still generate solid growth.

Not all agree that a rate rise is warranted today, if the BoC fails to deliver, given weak inflation and wage gains, and uncertainty that remains over the Trump administration's trade policy, watch how quickly the loonie (C$1.2921) gets sold off.

Nevertheless, if Poloz fails to hike would be irresponsible, given the recent rhetoric, and definitely lead to more market confusion about the effectiveness of BoC's communication policies.

Fed Chair Janet Yellen will also begin two days of testimony before Congress, with traders focusing on her assessment of financial conditions.

Note: The only major central banks expected to have moved to +1% base rate over the next year are the Fed and BoC.

1. Global Stocks encounter thin trading

In Japan, the Nikkei shed -0.5% while the broader Topix dropped -0.4% in thin trade before Fed's Janet Yellen's comments later today. A stronger yen (¥113.40) in the wake of a fresh controversy for U.S President Trump's administration hit exporters.

In Hong Kong, the Hang Seng rallied +0.6% for the third straight day to a two-year closing high, boosted by China fund flows and investors' bargain hunting.

In China, stocks ended lower overnight as investors paused for breath ahead of Ms. Yellen's address to Congress. The blue-chip CSI300 index fell -0.3%, while the Shanghai Composite Index shed -0.2%. The “Nifty 50” hit a 23-month high before edging -0.2% lower.

In Europe, stocks have opened higher and are maintaining momentum. On the FTSE 100 energy stocks are being supported by an increase in oil prices.

U.S stocks are set to open little changed (+0.03%).

Indices: Stoxx50 +0.6% at 3,484, FTSE +0.8% at 7,387, DAX +0.4% at 7,384, CAC-40 +0.8% at 5,180, IBEX-35 +0.4% at 10,495, FTSE MIB +0.8% at 21,280, SMI +0.7% at 8,935, S&P futures +0.03%.

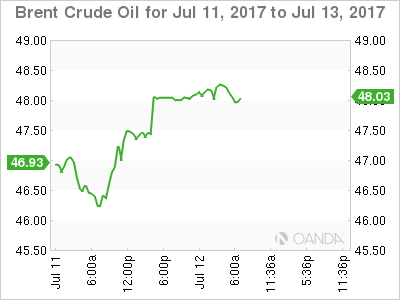

2. Oil gets a lift from inventory levels

Oil prices are better bid ahead of the U.S open in response to a fall in U.S fuel inventories and a cut in the U.S government's forecast for crude output next year which raised hopes that a supply glut is easing.

Note: API data yesterday indicated that U.S crude inventories fell by -8.1m barrels. Official inventory data from the EIA is due at 10:30 am EDT.

Also supporting prices, the EIA said yesterday it expected U.S. crude oil production to rise by less than previously forecast next year due to a lower price outlook.

Brent crude is up +86c, at +$48.38 a barrel, while U.S light crude (WTI) has gained +93c to +$45.97.

Crude 'bears' believe that despite further upside could be expected in the short term amid the speculations of a cut in U.S production, theses gains may be limited by the firm oversupply dynamics of the markets.

Note: Brent prices are -17% below their 2017 opening despite a deal OPEC to cut production from January. U.S oil production has risen over +10% since mid-2016 to +9.34m bpd.

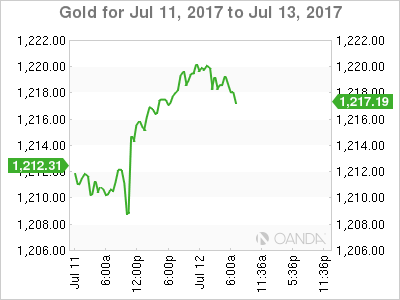

Yesterday, Gold registered its biggest intraday percentage gain since June 23 and silver registered its biggest intraday percentage rise in over a month. Currently, the yellow metal is little changed at +$1,217.97 an ounce and silver is +0.4% higher at +$15.80.

3. Yields curves look for further guidance

Fed Chair Janet Yellen is likely to reinforce the message of her June meeting's press conference, guiding the market toward an announcement of balance sheet normalization and a rate-rise by end-2017.

Comments from Fed's Mester (hawkish, non-voter) overnight noted reversing QE sooner rather than later is preferable, while the Fed's Brainard (voter) indicated it was appropriate to reduce balance sheet soon if economic data holds up and that policy makers should move cautiously on further rate increases to help boost inflation back to +2% target.

Ahead of the open, U.S 10-year note yields have dropped -1 bps to +2.36%. The yield on Aussie 10-year bonds have fallen -3 bps to +2.72%, halting five days of gains. In Japan, the BoJ again raised outright purchases of 3 and 5-year government notes to contain the recent increase in medium-term yields.

In Germany, this morning's 10-year Bund auction (4B, 2027) posted the highest funding cost since an auction in January 2016. The average yield was +0.59% with a bid-to-cover ratio of +1.4.

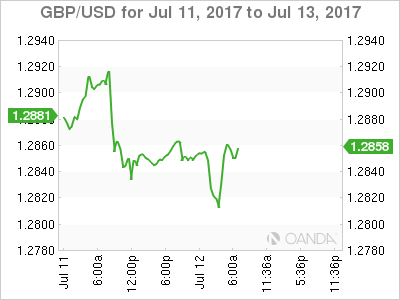

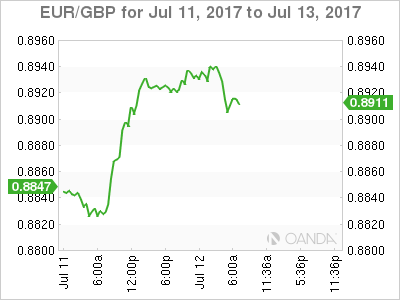

4. Sterling's whippy price action

The pound came under pressure; printed new week lows (£1.2812), when the Bank of England Deputy Governor Ben Broadbent said he was not yet ready to vote for a rise in the key interest rate, citing the many uncertainties surrounded the outlook for the economy.

However, the it has since recouped its losses and then some (£1.2862, €0.8911) after U.K data showed that three-month wage growth came in above expectations and higher than in the previous quarter.

Average earnings ex-bonuses rose +2% in the three-months to May, more than the +1.8% expected.

The better-than-expected data is supportive for BoE 'hawks' that have suggested interest rates should rise this year.

5. Eurozone Industrial Output Picks Up Speed

Data this morning showed that Eurozone's factories, mines and utilities output rose at the fastest annual pace in more than five years in May (+1.3% m/m and +4% y/y). The market was expecting a rise of +0.8% m/m, and +3.6% y/y – It's further proof that the regions recovery has picked up Q2.

Note: The Eurozone economy grew at the fastest rate in two years during Q1, outpacing the U.S, the U.K. and Japan.