Sample Category Title

Australia’s Trade Surplus Sharply Widened In May

For the 24 hours to 23:00 GMT, the AUD slightly declined against the USD and closed at 0.7607.

LME Copper prices declined 0.5% or $29.0/MT to $5818.0/MT. Aluminium prices rose 0.5% or $9.5/MT to $1913.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7600, with the AUD trading 0.09% lower against the USD from yesterday's close.

Earlier in the session, data revealed that Australia's seasonally adjusted trade surplus widened more-than-expected to a level of A$2471.0 million in May, amid a surge in exports and following a revised trade surplus of A$90.0 million in the previous month. Market anticipation was for the country's trade surplus to expand to A$1100.0 million.

The pair is expected to find support at 0.7570, and a fall through could take it to the next support level of 0.7540. The pair is expected to find its first resistance at 0.7631, and a rise through could take it to the next resistance level of 0.7662.

Going ahead, investors will focus on Australia's AiG performance of construction index for June, slated to release overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Services Sector Activity Across The Euro-Zone Slowed Less Than Initially Estimated In June

For the 24 hours to 23:00 GMT, the EUR marginally declined against the USD and closed at 1.1351.

On the data front, the Euro-zone's final Markit services PMI fell less than initially estimated to a level of 55.4 in June, compared to a drop of 54.7 registered in the preliminary print. In the prior month, the PMI had recorded a level of 56.3. On the other hand, the region's seasonally adjusted retail sales grew more-than-expected by 0.4% on a monthly basis in May, compared to a rise of 0.1% in the prior month.

Separately, growth in Germany's services sector cooled less than initially estimated to a level of 54.0 in June, but remained at a five-month low level, while the flash estimate had indicated a fall to a level 53.7. In the previous month, the PMI had recorded a reading of 55.4.

The greenback traded mixed against a basket of major currencies, after minutes from the Federal Reserve's (Fed) June meeting showed that committee members are still divided over the outlook for US inflation and when to start reducing the balance sheet.

According to minutes, policymakers were not able to agree upon how soon to start winding down their $4.5 trillion balance sheet as some wanted to announce a start to the process by the end of August but others wanted to wait until later in the year. Further, a few members expressed concerns over subdued inflation but most officials voiced confidence that inflation will recover after recent soft readings.

On the economic front, the final durable goods orders eased 0.8% in May, revised from preliminary figures that had recorded a fall of 1.1%. Durable goods orders had recorded a revised drop of 0.9% in the prior month. Moreover, the nation's factory orders declined more-than-anticipated by 0.8% in May, compared to market consensus for a fall of 0.5%.

In the previous month, factory orders had fallen 0.3%. In the Asian session, at GMT0300, the pair is trading at 1.1338, with the EUR trading 0.11% lower against the USD from yesterday's close.

The pair is expected to find support at 1.1311, and a fall through could take it to the next support level of 1.1284. The pair is expected to find its first resistance at 1.1367, and a rise through could take it to the next resistance level of 1.1396.

Moving ahead, market participants will anxiously await the release of the European Central Bank's recent meeting minutes, slated in a few hours, to get cues on whether the bank is closer to begin scaling back its monetary stimulus. Additionally, the US ADP employment report, ISM non-manufacturing PMI and the initial jobless claims data, slated to release later in the day, will keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Britain’s Services Sector Expanded At Its Weakest Pace In Four Months In June

For the 24 hours to 23:00 GMT, the GBP rose 0.06% against the USD and closed at 1.2936.

On the data front, Britain's Markit services PMI fell to a four-month low level of 53.4 in June, highlighting that heightened political and Brexit uncertainties are taking their toll on the economy. In the previous month, the PMI had recoded a level of 53.8, while market participants were anticipating the PMI to drop to a level of 53.5.

In the Asian session, at GMT0300, the pair is trading at 1.2931, with the GBP trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.2901, and a fall through could take it to the next support level of 1.2870. The pair is expected to find its first resistance at 1.2955, and a rise through could take it to the next resistance level of 1.2978.

In absence of any major economic news in the UK today, investor sentiment will be governed by global macroeconomic factors.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD marginally rose against the JPY and closed at 113.16.

In the Asian session, at GMT0300, the pair is trading at 113.07, with the USD trading 0.08% lower against the JPY from yesterday's close.

The pair is expected to find support at 112.70, and a fall through could take it to the next support level of 112.34. The pair is expected to find its first resistance at 113.56, and a rise through could take it to the next resistance level of 114.06.

Looking ahead, Japan's flash leading and coincident indices for May, scheduled to release tomorrow, will be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Lower, Ahead Of Swiss Inflation Data

For the 24 hours to 23:00 GMT, the USD declined 0.06% against the CHF and closed at 0.9641.

In the Asian session, at GMT0300, the pair is trading at 0.9650, with the USD trading 0.09% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9627, and a fall through could take it to the next support level of 0.9605. The pair is expected to find its first resistance at 0.968, and a rise through could take it to the next resistance level of 0.9711.

Moving ahead, investors will look forward to Switzerland’s consumer price index data for June, slated to release in a few hours.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Loonie Extends Its Losses, Ahead Of Canada’s Building Permits Data

For the 24 hours to 23:00 GMT, the USD rose 0.15% against the CAD and closed at 1.2957.

In the Asian session, at GMT0300, the pair is trading at 1.2973, with the USD trading 0.12% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2932, and a fall through could take it to the next support level of 1.2892. The pair is expected to find its first resistance at 1.3014, and a rise through could take it to the next resistance level of 1.3056.

Ahead in the day, traders will keep a close watch on Canada's building permits and international merchandise trade data, both for May.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Swissy Setting Up For Another Tumble

Key Points:

- A reversal could be seen earlier than anticipated.

- Selling pressure likely to stem from bearish technical bias.

- Losses could extend to a 12-month low at 0.9531.

The Swissy looks about ready to make an about face as its rally appears to have run short on momentum. This is largely indicated by the technical bias which remains firmly bearish – even if the pair has managed to claw its way back the 50.0% Fibonacci level. As a result of this, the USDCHF could begin to track towards the 0.9531 handle in the coming days which would be a 12-month low.

First things first, it’s worth taking a closer look at exactly why we expect to see the pair reverse shortly –especially given that we had originally forecast a rally up to at least the 0.97 handle. Primarily, the formation of a shooting star (sometimes called a pin candle) during the prior session can be attributed to sparking concerns of an early reversal. Ordinarily, such a candle wouldn’t be nearly enough to pose a real threat to the uptrend. However, due to numerous other technical indicators also remaining bearish in spite of the rally, fears that bulls are losing control are notably heightened.

In particular, it has been noted that the parabolic SAR and EMA’s have yet to shake their strongly bearish bias. This should make it fairly easy for the bears to put pressure on the pair once the decline has resumed and this view is only reinforced by the ADX reading which has been above that key 20.0 reading since May – the beginning of the most recent long-term rout for the USDCHF. Overall, the technical outlook is fairly grim and the movement of the stochastics out of oversold territory certainly won’t be helping matters either.

If we do see this pair begin to slump yet again, we expect it to reach as low as 0.9531 rather quickly. Losses past this point are currently looking unlikely as the 0.9531 mark does represent at 12-month low and the Swissy will almost certainly be flirting with becoming oversold upon reaching this price. Nevertheless, it will be worth taking a look at the pair closer to the time as it could continue to track lower if the MACD and signal line crossover – a feat that isn’t actually looking too unlikely.

Ultimately, monitor the USDCHF as we move forward as the pair could have some solid moves instore for us yet. As discussed, the technical bias is suggesting that the bears are likely to be staging a comeback this week which could result in some notable losses. Nonetheless, also keep an eye on the fundamental side of things as any particularly robust US employment data could upset the applecart as this week comes to an end.

GOLD – Recovers, Looks To Strengthen Further

GOLD - The commodity has halted its weakness and triggered a recovery higher as it lookd for more correction. On the downside, support comes in at the 1,215.00 level where a break will turn attention to the 1,210.00 level. Further down, a cut through here will open the door for a move lower towards the 1,200.00 level. Below here if seen could trigger further downside pressure targeting the 1,190.00 level. Conversely, resistance resides at the 1,230.00 level where a break will aim at the 1,240.00 level. A turn above there will expose the 1,250.00 level. Further out, resistance stands at the 1,260.00 level. All in all, GOLD looks to recover further on correction

Market Morning Briefing: It Is A Critical Moment For Pound

STOCKS

Dow (21478.17, -0.01%) has not been able to move above 21570 in the last few sessions but at the same time the bears at resistance near 21500/600 do not seem to be strong enough to push the index sharply to lower levels. While it sustains above 21400, upside possibility remains high.

Dax (12453.68, +0.13%) seems to be bouncing from levels near 12300. The interim support turned resistance at 12500 is important for now and while the index trades below 12500, we could possibly see another leg of rejection after the ongoing “pause phase” which could last for another 2-3 sessions.

Shanghai (3208.66, +0.05%) bounced sharply to close above 3200, breaking the ongoing sideways movement within 3200-3170 levels. A rise towards 3220 is possible before a slight dip is seen. Overall medium term looks bullish towards 3250.

Nikkei (20027.42, -0.27%) is testing immediate support near 19980 and if that holds, we could see a rise back towards 20250 in the next couple of sessions.

Nifty (9637.60, +0.25%) was stable yesterday, trading above 9600. While it sustains at current or higher levels, our initial target of 9700 could be tested soon. A few sessions of sideways consolidation is possible before resumption of an upward rally. For now, near term looks bullish.

COMMODITIES

Gold (1223) is trading within the range of 1190-1230 and Silver (16.00) is within 15.80-16.50. We will remain bearish on Bullion while gold and silver are trading below 1250 and 16.50 levels respectively. We are now awaiting U.S. non-farm payrolls for June, due on tomorrow at 6:00 pm IST, for more insight into Fed policy and the future path of U.S Dollar.

No directional movement had been seen in Copper (2.66) also as it is trading within the range of 2.66-2.78.If 2.66 holds then we might see 2.82 within few days of time otherwise it might come back towards 2.55 levels. We will remain bullish on copper while it is trading above 2.55 levels.

Brent (47.97) and WTI (45.30) fell just a day before of the release of U.S weekly crude oil inventory data (8:30 pm IST,expected -2.4M B), as traders wanted to book profits after a streak of 8 up days in a row. As we have said that this short term rally hasn’t affected the midterm bearishness while Brent and WTI are trading below 54 and 51 levels. In very short term time frame, 48 (Brent) and 45.80 (WTI) could be the pivots, where the price action may determine the near to medium term path. A surplus or a less than expected shortage in weekly inventory could bring further bearish possibilities towards 44 (Brent) and 42.10 (WTI) into consideration

FOREX

No set date for US Fed balance sheet reduction and concerns over persistent soft inflation limits Dollar strength.

Dollar Index (96.28) has retreated a bit from our resistance of 96.50-60 and Euro (1.1338) still trades above the support of 1.1290, keeping bidirectional possibilities still open despite our preference for further Dollar strength in the coming days. As discussed in the last two days, till now, most of the majors are in a normal correction and further break of major supports are required before the downtrend can be confirmed. Therefore we wait for clarity.

Dollar Yen (113.04) is stuck in a range of 112.75-113.50 for the last 3 sessions but the bias remains bullish for 114.30-115.00 till the support of 112.60 holds.

It is a critical moment for Pound (1.2933) as it must rise right now if it has to keep the immediate upside momentum intact. Failure to rise today may rob it of the upside momentum and the support of 1.2880 may be challenged.

Aussie (0.7598) breached the support of 0.7580 briefly before recovering but now the lower support of 0.7530-15 come into focus which may be tested by the next week.

Dollar Rupee (64.78) spent the day in the range of 64.60-90 for the day and this range may continue for the rest of the week.

INTEREST RATES

The US yields may remain stable today but could start falling from current levels in the coming sessions. The 30YR (2.85%) could come off towards 2.83% while the 10YR (2.33%) and the 5Yr(1.93%) could move down to 2.30% and 1.90% respectively .

The Japanese yields are all rallying upwards and look bullish for the medium term. the 5YR, 10YR and 30Yr are a trading at -0.05%, 0.09% and 0.88%. the 30YR may head towards long term resistance near 1.12 while there could be less scope on the upside for the 10Yr and the 5Yr.

The UK yields have also risen sharply in the last few sessions but could now pause for some sessions or maybe dip slightly before resuming the near term uptrend. Medium term looks bullish.

The German yields are also trying to rise and could eventually move up with interim dips. But also note long term resistances are hovering above current levels and could push the yields lower in the longer run.

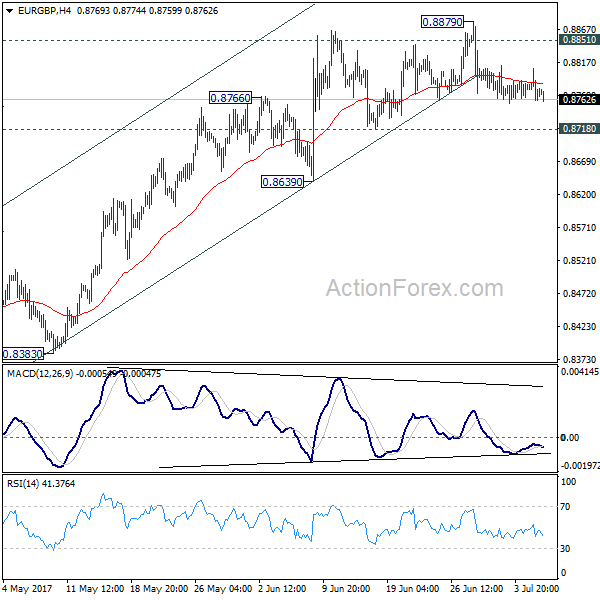

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8755; (P) 0.8782; (R1) 0.8802; More...

Intraday bias in EUR/GBP remains neutral for consolidation below 0.8879. On the downside, break of 0.8718 support will argue that rise from 0.8312 has completed. In that case, intraday bias with be turned back to the downside for lower side of the range at 0.8312. Meanwhile, break of 0.8879 and sustained trading above 0.8851 will pave the way to retest 0.9304 high.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.