Sample Category Title

Japan’s industrial output slips -2.3% mom in Nov, indecisive fluctuation continues

Japan's industrial production declined -2.3% mom in November, outperforming expectations of a -3.4% mom drop, but marking the first contraction in three months.

The decrease was driven by weaker exports of semiconductor manufacturing devices and cars, highlighting challenges in external demand. Out of 15 industrial sectors, 11 recorded declines, while 3 sectors reported gains.

Production machinery saw a significant -9.1% drop, largely due to falling exports of chip-making equipment to China and Taiwan, while motor vehicle output fell -4.3%, and fabricated metal products dropped -5.7%.

Despite the slump, the Ministry of Economy, Trade, and Industry maintained its view that industrial production "fluctuates indecisively," while warning of risks tied to the economic outlooks of the US and China.

Looking ahead, METI's poll of manufacturers predicts a rebound, with output expected to rise 2.1% in December and an additional 1.3% in January.

Separately, retail sales posted a robust 2.8% yoy gain, exceeding expectations of 1.5%, signaling resilience in domestic demand.

Japan’s Tokyo CPI core rises to 2.4% in Dec, but core-core dips to 1.8%

Japan's Tokyo core CPI (excluding food) rose from 2.2% yoy to 2.4% yoy in December, marking its highest level since August but falling short of expectations for 2.5%. The increase was largely driven by a 13.5% yoy surge in energy prices, reflecting the phase-out of government subsidies for gas and electricity bills. However, when excluding utility costs, inflation pressures appear steady.

Core-core CPI (excluding food and energy) softened to 1.8% yoy from 1.9% yoy, while services inflation edged up slightly from 0.9% to 1.0%. Meanwhile, headline inflation accelerated to 3.0% yoy from 2.6% yoy, with energy and food prices, including rice, contributing significantly to the increase too.

The uptick in Tokyo inflation highlights lingering pressures from rising utility and food costs, which may weigh on consumer spending and deter firms from implementing further price hikes. These factors, coupled with broader signs of economic weakness, could delay BoJ ’s timeline for raising interest rates.

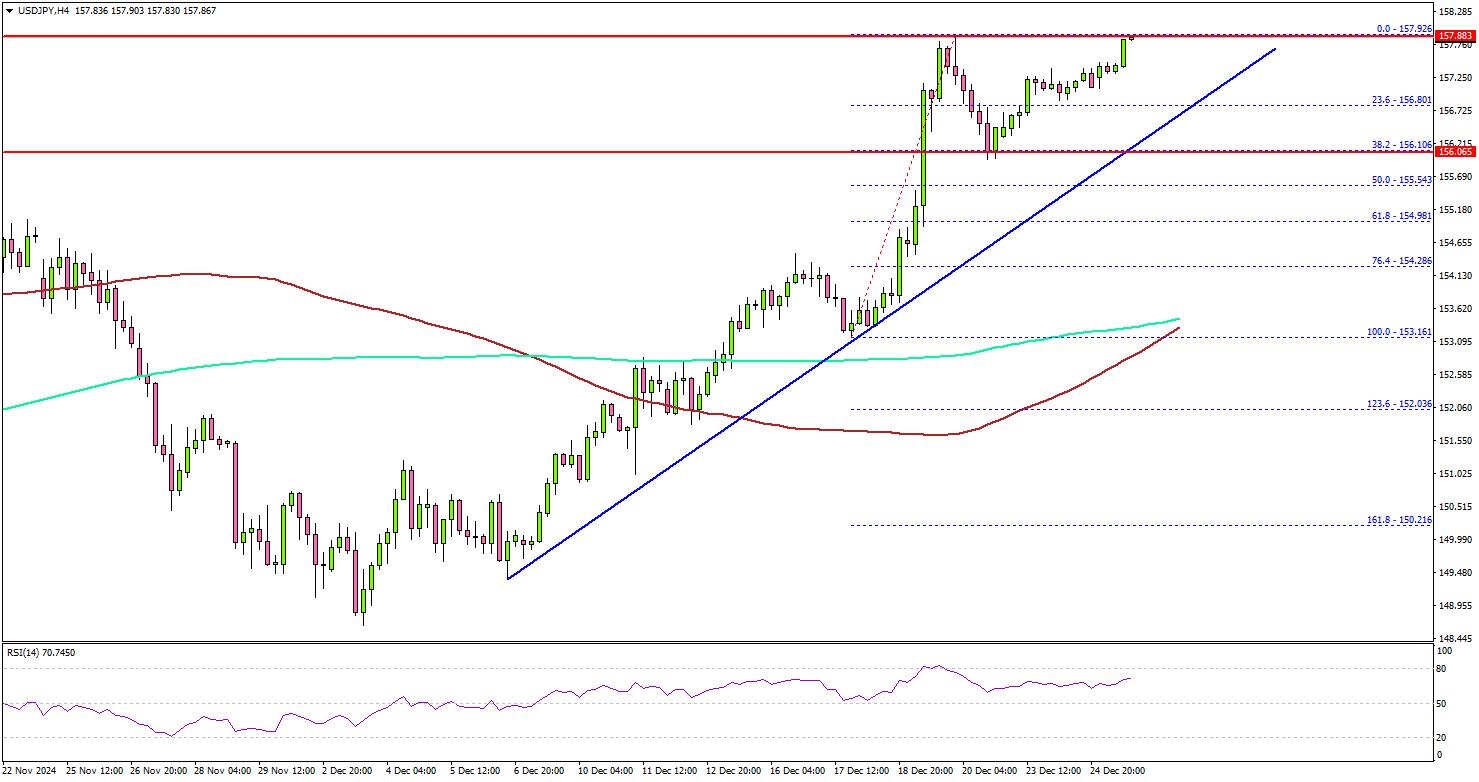

USD/JPY Sets Sights on Fresh Gains: Bulls In Control

Key Highlights

- USD/JPY started a fresh increase above the 156.00 resistance zone.

- A major bullish trend line is forming with support at 156.80 on the 4-hour chart.

- EUR/USD is still consolidating below the 1.0450 resistance zone.

- Bitcoin failed to regain traction and declined from $100,000.

USD/JPY Technical Analysis

The US Dollar started a fresh increase above the 155.50 and 156.00 resistance levels. USD/JPY cleared the 157.00 level to move further into a positive zone.

Looking at the 4-hour chart, the pair settled well above the 156.50 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The bulls remained in control and might aim for more gains.

On the upside, the pair could face resistance near the 158.20 level. The next major resistance is near the 158.80 level. A close above the 158.80 level could set the tone for another increase.

In the stated case, the pair could rise toward the 160.00 resistance. On the downside, immediate support sits near the 156.80 level. There is also a major bullish trend line forming with support at 156.80 on the same chart.

The next key support sits near the 155.50 level. Any more losses could send the pair toward the 154.80 level. Any more losses might send the pair toward the 154.00 level.

Looking at Bitcoin, the bulls failed to push the price above $100,000 and there was a fresh bearish reaction.

Upcoming Economic Events:

- US Wholesale Inventories for Nov 2024 (preliminary) – Forecast +0.2%, versus +0.2% previous.

Elliott Wave View: EURGBP Rally Expected to Fail

Short Term Elliott Wave view of EURGBP suggests decline from 8.8.2024 high ended as wave (1) at 0.8219 as an impulse. Down from 8.8.2024 high, wave 1 ended at 0.8295 and rally in wave 2 ended at 0.844. Wave 3 lower ended at 0.826 and rally in wave 4 ended at 0.8375. Down from there, wave ((i)) of 5 ended at 0.8268 and wave ((ii)) of 5 ended at 0.8364. Wave ((iii)) of 5 lower ended at 0.8225 and wave ((iv)) of 5 ended at 0.8327. Final wave ((v)) of 5 ended at 0.8222. This completed wave (1) in higher degree.

Wave (2) corrective rally is in progress with internal subdivision as a zigzag Elliott Wave structure. Up from wave (1), wave A ended at 0.8313 and pullback in wave B ended at 0.8268. Wave C higher is in progress as an impulse structure. Up from wave B, wave ((i)) ended at 0.8314 and pullback in wave ((ii)) ended at 0.8272. Near term, as far as pivot at 0.8219 low stays intact, expect pullback to find support in 3, 7, 11 swing for further upside. Target higher for wave (2) is 100% – 161.8% Fibonacci extension of wave A. This area comes at 0.836 – 0.8419 where sellers can appear for 3 waves pullback at least.

EURGBP 60 Minutes Elliott Wave Chart

EURGBP Elliott Wave Video

https://www.youtube.com/watch?v=CMXDHJK1wpY

AUDUSD Wave Analysis

- AUDUSD reversed from resistance level 0.6270

- Likely to fall to support level 0.6200

AUDUSD currency pair recently reversed down from the resistance level 0.6270 (former multi-month support from the start October of 2023, acting as the resistance after it was broken yesterday).

The downward reversal from the resistance level 0.6270 stopped the previous minor correction iv – which belongs to sharp sub-impulse 3 of the higher impulse wave (3) from September.

AUDUSD can be expected to fall to the next support level 0.6200, which stopped the previous impulse wave iii earlier this month.

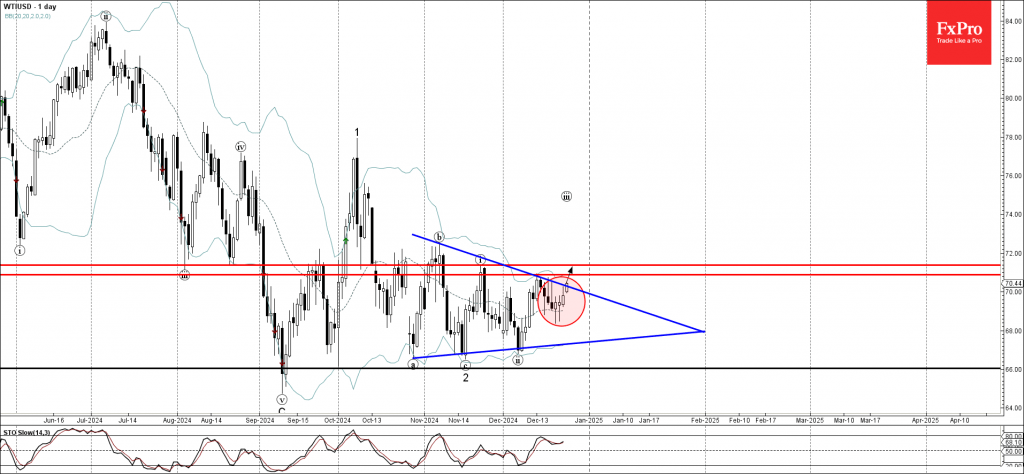

WTI Wave Analysis

- WTI broke daily Triangle

- Likely to rise to resistance level 70.90

WTI crude oil today broke the resistance trendline of the daily Triangle from the end of October, inside which the price has been moving from October.

The breakout of this Triangle continues the active short-term impulse wave (iii) of the higher order impulse wave 3 from the middle of November.

WTI crude oil can be expected to rise to the next resistance level 70.90, the breakout of which can lead to further gains toward 71.40.

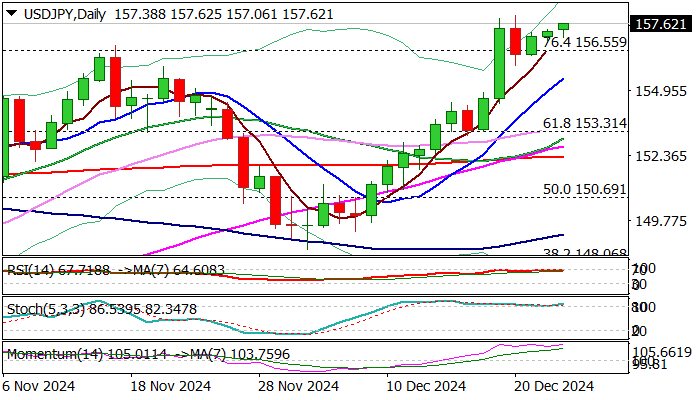

USD/JPY Outlook: Bulls Gold Grip in Lower-Volume Boxing Day Trading

USDJPY keeps firm tone in holiday-thinned trading on Thursday and pressuring last Friday’s peak at 157.92 (the highest since mid-July).

The pair is on track for the fourth consecutive weekly gain and for over 5% monthly advance in December.

Hawkish signals from Fed on expectations that inflation will remain elevated for some time and continue to obstruct plans for rate cuts, as well as wide gap between Fed and BoJ monetary policies, continue to support the pair.

Near term price action has established above broken Fibo barrier at 156.67 (76.4% retracement of 161.98/139.57 correction) which now offers solid support, followed by rising daily Tenkan-sen (155.19) and key supports at 153.62/40 (daily cloud top / daily Kijun-sen / broken Fibo 61.8%).

Strong bullish momentum and multiple golden crosses on daily chart support bullish near-term outlook, with thick rising daily Ichimoku cloud underpinning the action.

However, initial warning from overbought conditions should be considered, while traders continue to closely watch the action from Bank of Japan after they have sent a signal in a shape of verbal intervention, with markets expect that the authorities may act somewhere above 160 mark, similar to intervention in July.

Res: 155.95; 156.95; 157.61; 158.00.

Sup: 157.00; 156.55; 155.88; 155.19.

BTC/USD Fails to Surpass $100,000: Bitcoin Price Forecasts for 2025

Forbes analysts predict 2025 will be a pivotal year for Bitcoin, solidifying its position as a global financial asset. Their key forecasts include:

→ Regulatory Shifts: A change in SEC policies is expected to foster growth in the cryptocurrency sector, driving the cryptocurrency market capitalisation from approximately $3.3 trillion to $8 trillion.

→ Strategic Reserves: One of the leading G7 or BRICS nations will adopt Bitcoin as a strategic reserve asset. Analysts likely hint at the United States, where Trump is reportedly considering the creation of a Bitcoin strategic reserve.

→ DeFi Expansion: Bitcoin-based DeFi is expected to flourish, supported by second-layer networks like Stacks. This could expand the total value locked (TVL) in the DeFi ecosystem to $24 billion.

→ New Crypto Funds: After the successful launch of Bitcoin ETFs, more funds may emerge, including those centered on staking.

→ Corporate Adoption: Major companies like Apple or Google, part of the Magnificent Seven, might add Bitcoin to their reserves as accounting standards improve.

While Forbes analysts refrain from making direct price predictions for 2025, their optimistic perspective suggests BTC/USD is likely to sustain its long-term growth trajectory.

Short-Еerm Сoncerns

In the short term, Bitcoin faces challenges. According to the BTC/USD chart today, the price dropped below $96,000 after failing to stay above the key psychological level of $100,000.

This decline reinforces bearish momentum, as the price has moved into the lower half of the ascending channel formed following Trump’s election victory. Bulls are struggling to regain control and push the price back into the upper half of this channel.

If the trend persists, BTC/USD price could test the lower boundary of the blue channel in 2024, increasing the risk of a bearish breakout.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*At FXOpen UK, Cryptocurrency CFDs are only available for trading by those clients categorised as Professional clients under FCA Rules. They are not available for trading by Retail clients.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

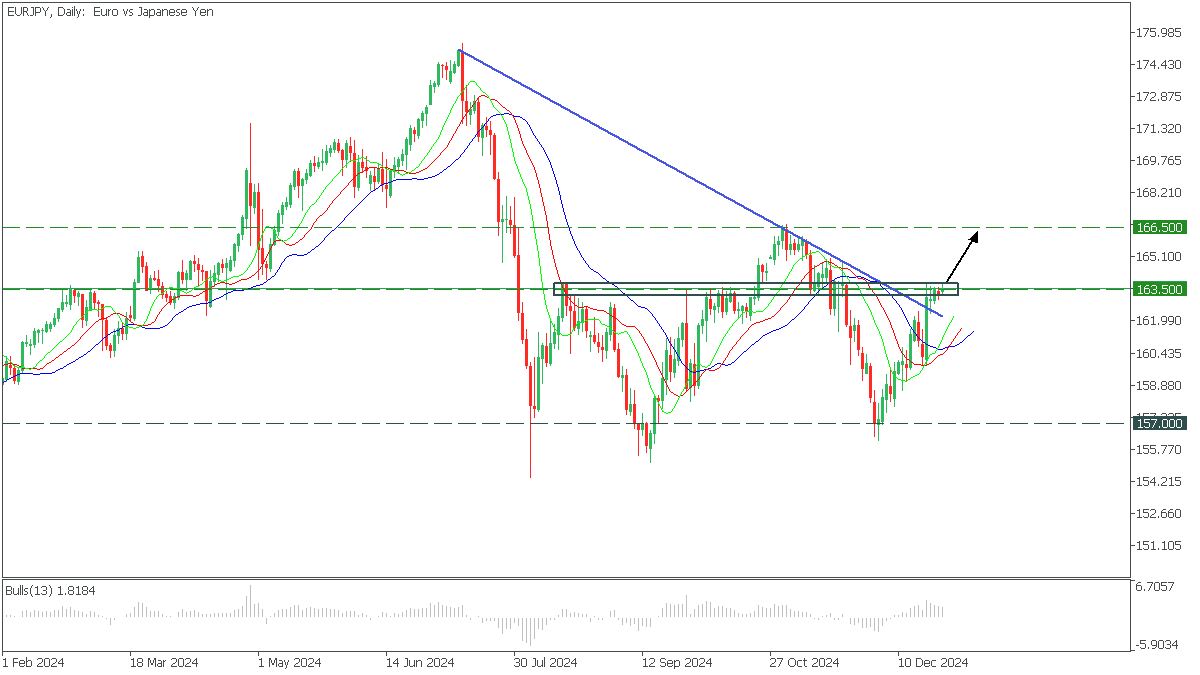

EURJPY: Upside Opportunity

EURJPY, Daily

In the Daily timeframe, EURJPY broke the trend line after a short-term decline and is consolidating at an important resistance. On the Alligator, the lips crossed the jaw, indicating the possibility of further upside.

- We can consider buying EURJPY on consolidation above 163.500 with a target to 166.500;