Sample Category Title

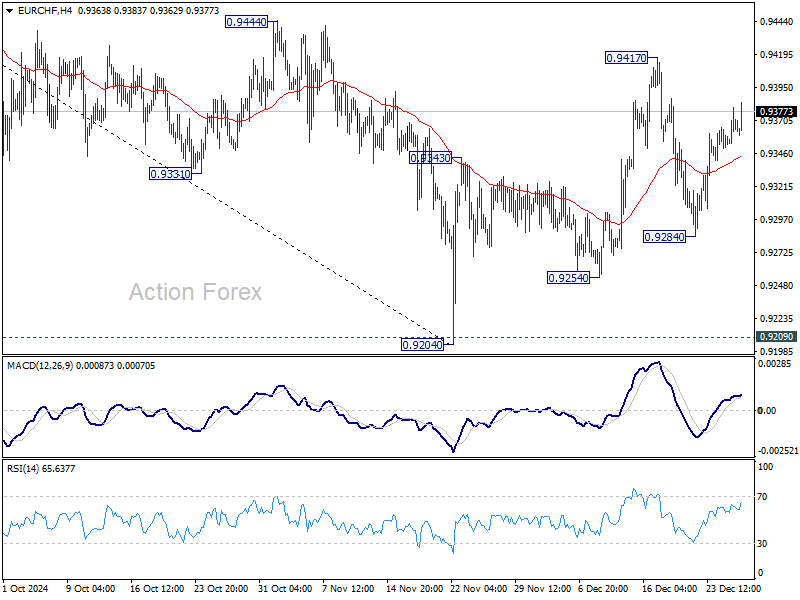

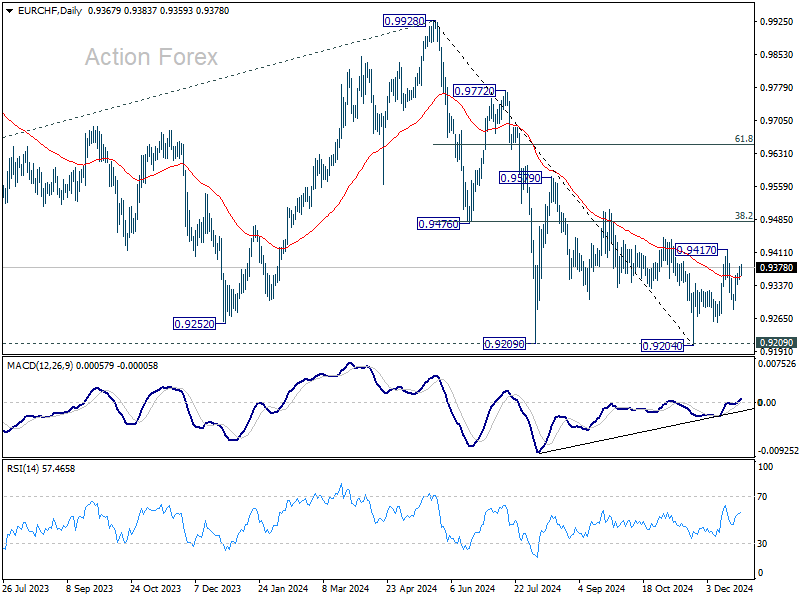

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9352; (P) 0.9367; (R1) 0.9382; More....

Intraday bias in EUR/CHF remains neutral for the moment. Corrective rebound from 0.9204 could have completed at 0.9417. Another fall is in favor and below 0.9284 will target 0.9254 support first. Break there will bring retest of 0.9204 low.

In the bigger picture, a medium term bottom is probably in place at 0.9204. More consolidations would be seen above there with risk of stronger rebound to 38.2% retracement of 0.9928 to 0.9204 at 0.9481. But outlook will remain bearish as long as 0.9481 holds and another fall through 0.9204 to resume larger down trend is in favor.

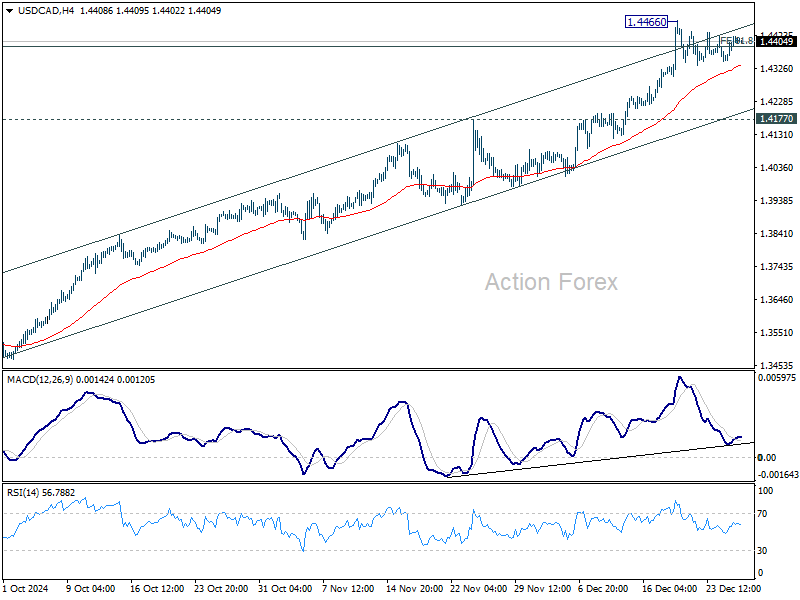

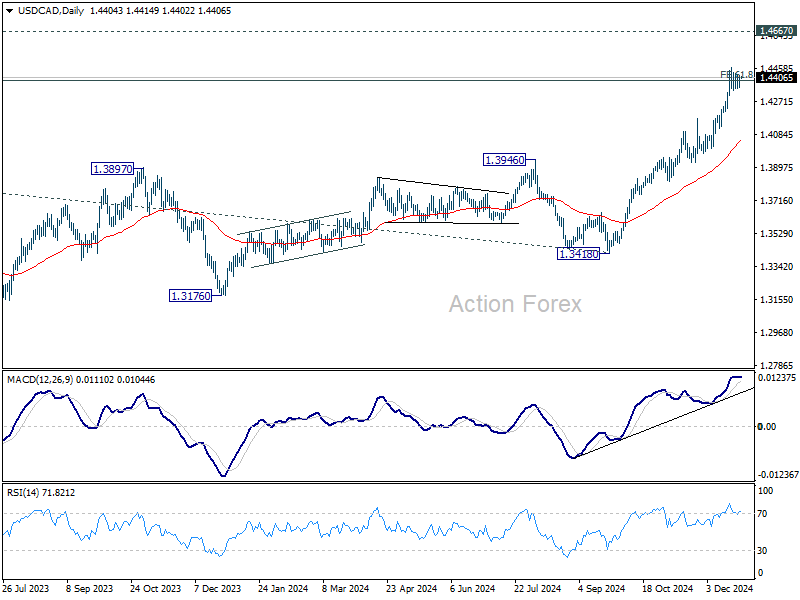

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4364; (P) 1.4393; (R1) 1.4435; More...

Intraday bias in USD/CAD remains neutral with consolidation from 1.4466 temporary top extending. While deeper pull back cannot be ruled out, outlook will stay bullish as long as 1.4177 resistance turned support holds. On the upside, break of 1.4466 and sustained trading above 1.4391 will pave the way to retest 1.4667/89 long term resistance zone.

In the bigger picture, up trend from 1.2005 (2021) is in progress and met 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391 already. Sustained trading above there will pave the way to 1.4667/89 key resistance zone (2020/2015 highs). Medium term outlook will remain bullish as long as 55 W EMA (now at 1.3729) holds, even in case of deep pullback.

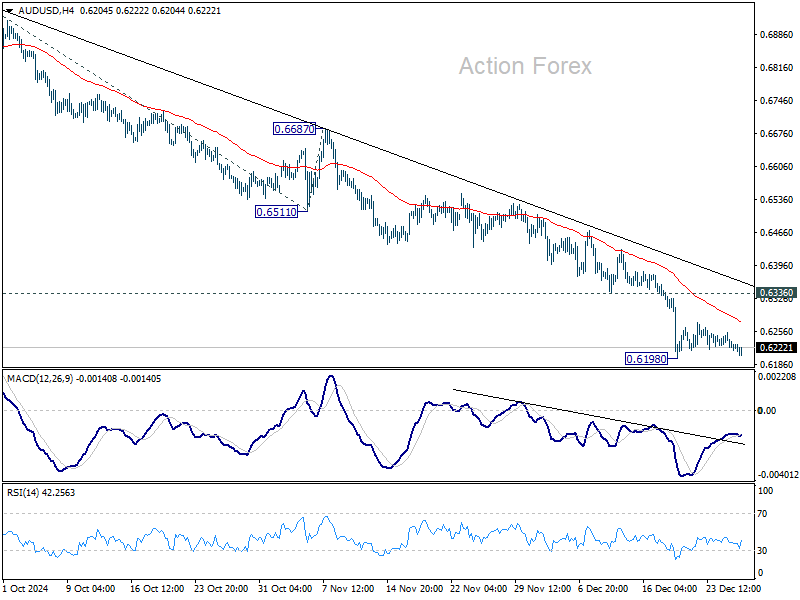

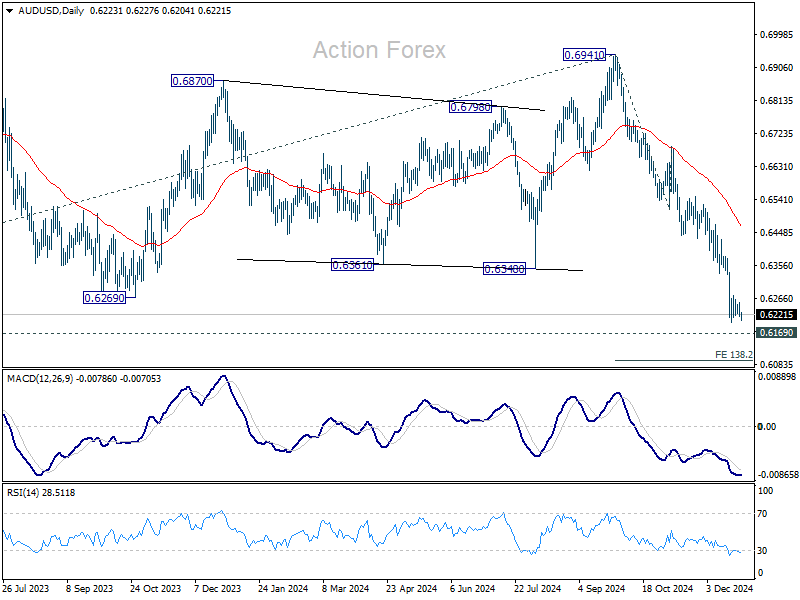

AUD/USD Daily Report

Daily Pivots: (S1) 0.6206; (P) 0.6231; (R1) 0.6245; More...

AUD/USD is staying in consolidations above 0.6198 temporary low and intraday bias remains neutral. Consolidations should be relatively brief as long as 0.6336 support turned resistance holds. Break of 0.6198 will resume the fall from 0.6941 to 0.6169 long term support, and then 138.2% projection of 0.6941 to 0.6511 from 0.6687 at 0.6074. Nevertheless, firm break of 0.6336 will bring stronger rebound lengthier correction before staging another decline.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6588) holds.

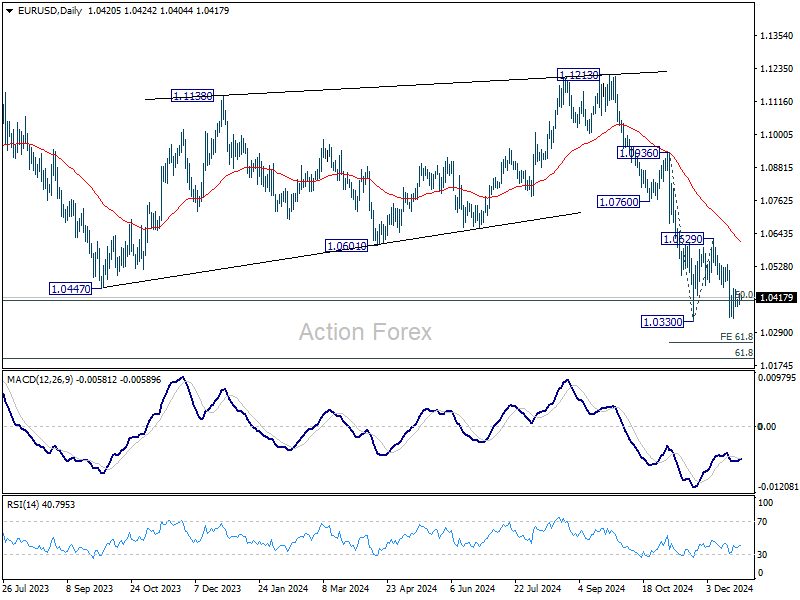

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0399; (P) 1.0414; (R1) 1.0439; More....

Intraday bias in EUR/USD remains neutral for the moment. While stronger recovery cannot be ruled out, outlook will remain bearish as long as 1.0629 resistance holds. Firm break of 1.0330 will confirm decline resumption and target 61.8% projection of 1.0936 to 10330 from 1.0629 at 1.0254, and then 100% projection at 1.0023.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

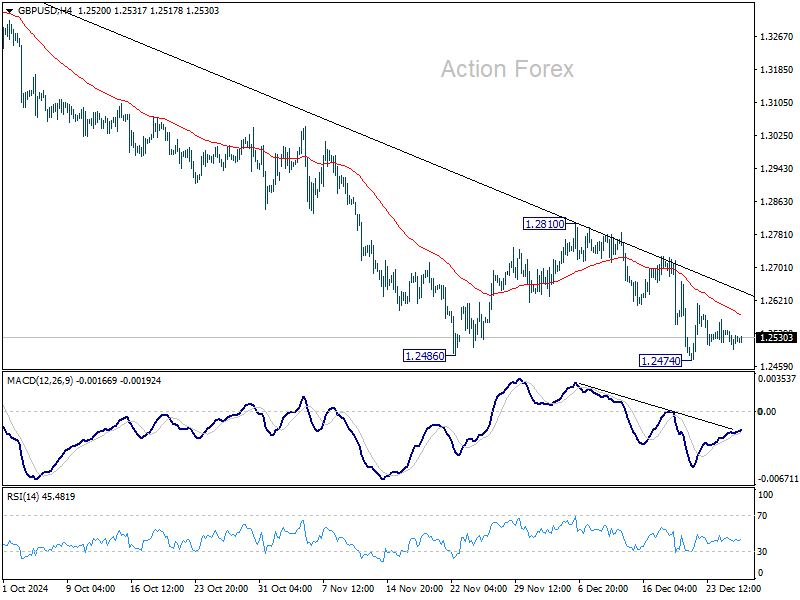

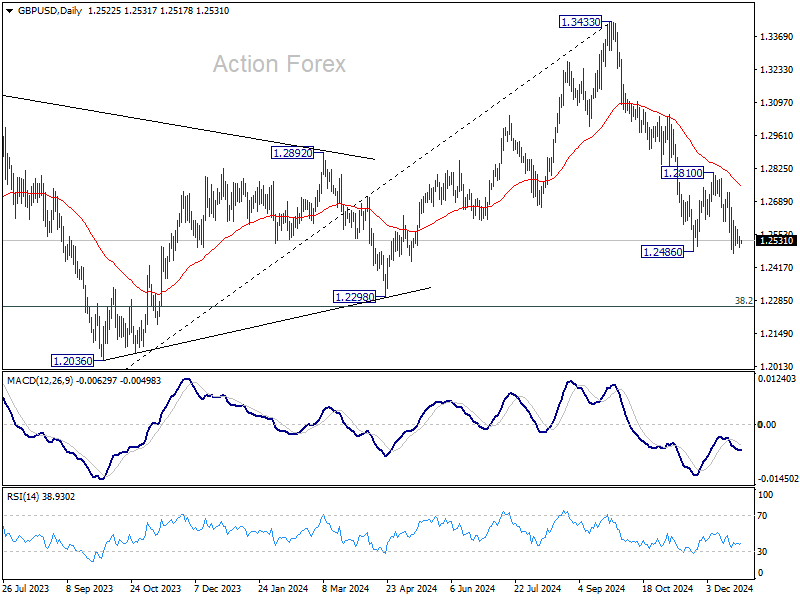

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2498; (P) 1.2530; (R1) 1.2559; More...

Intraday bias in GBP/USD remains neutral as consolidations continue above 1.2474 temporary low. While another recovery cannot be ruled out, outlook will stay bearish as long as 1.2810 resistance holds. On the downside, break of 1.2474 will resume the fall from 1.3433 to 1.2298 cluster support zone.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

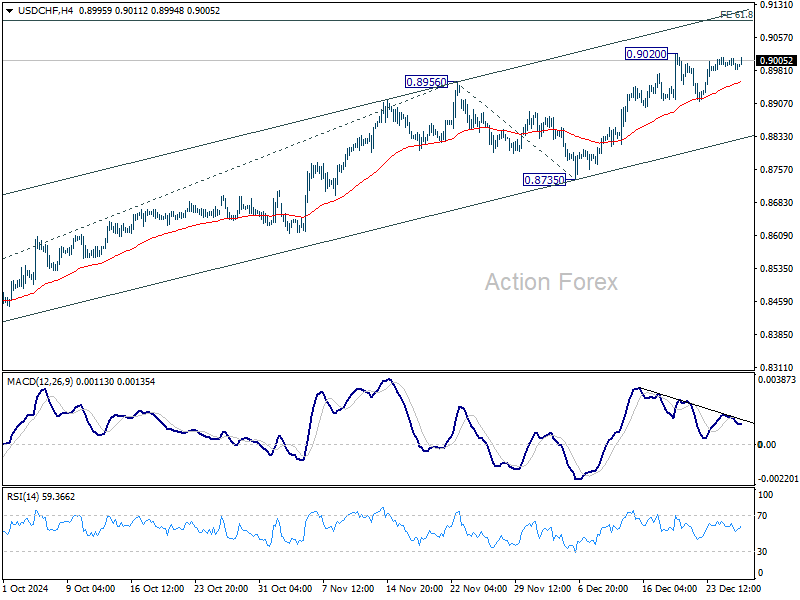

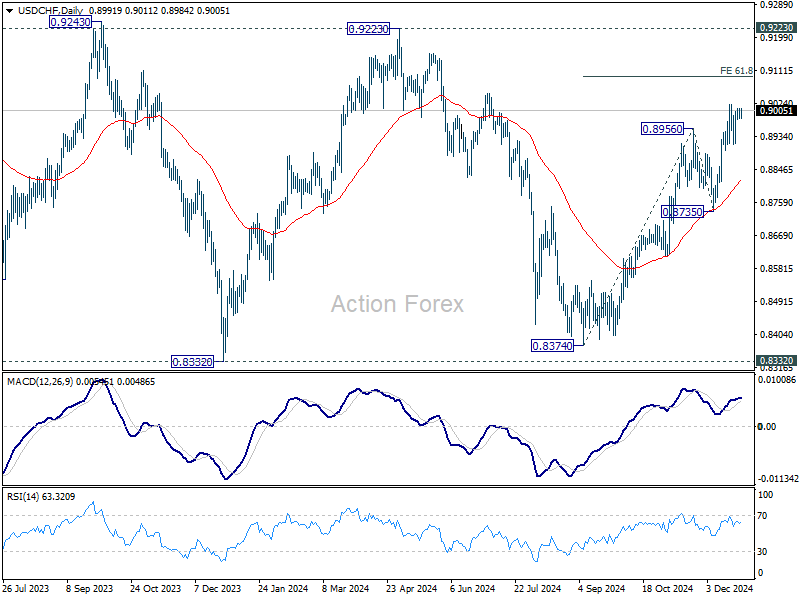

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8979; (P) 0.8994; (R1) 0.9004; More…

Intraday bias in USD/CHF remains neutral as sideway consolidations continue below 0.9020. While another pull back might be seen, downside should be contained above 0.8735 support to bring another rally. Above 0.9020 will resume the rise from 0.8374 and target 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

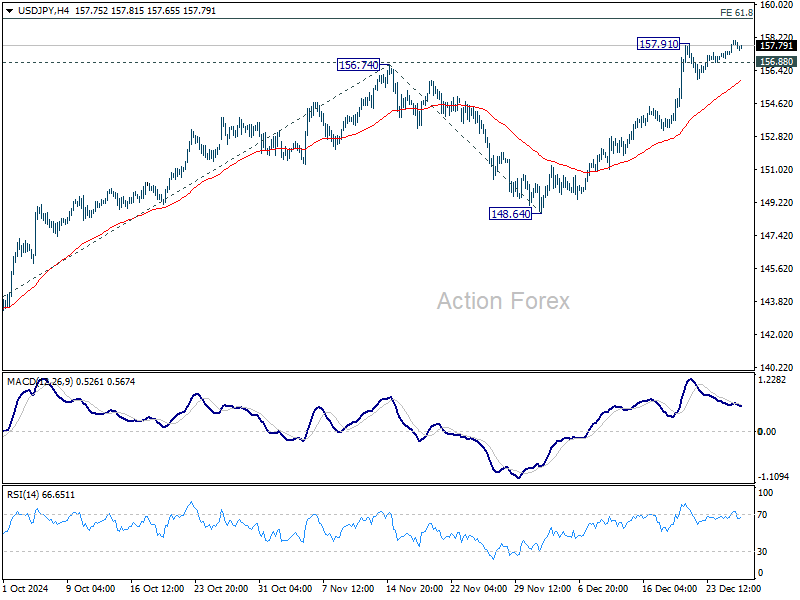

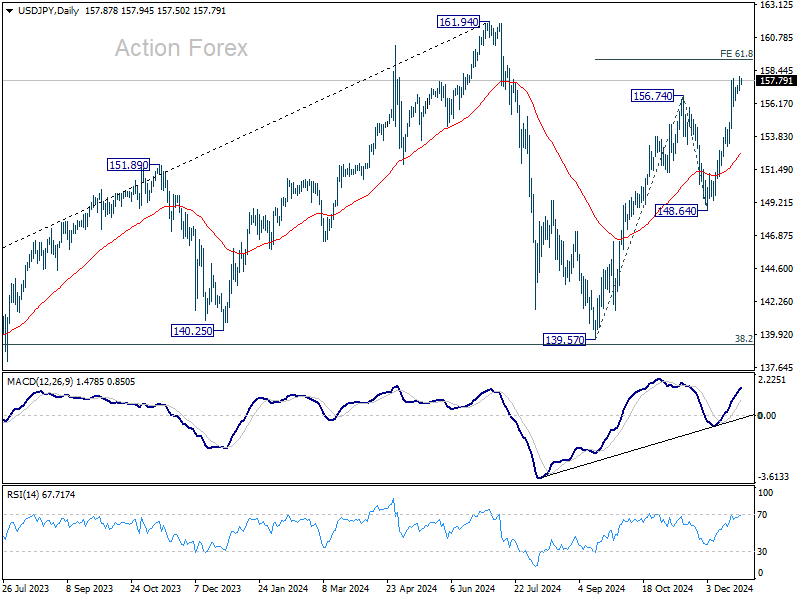

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.32; (P) 157.70; (R1) 158.42; More...

USD/JPY's rally is trying to resume by breaching 157.91 temporary top and intraday bias is back on the upside. Rise from 139.57 is extending to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. Firm break there will pave the way back to 161.94 high. On the downside, though, below 156.88 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Yen Slides on BoJ Caution and Soft Inflation, Verbal Intervention Curbs Losses

Yen saw broad declines during Asian session, briefly falling below 158 against Dollar, but the selloff was quickly mitigated by verbal intervention, as least partially.

The decline was triggered by weaker-than-expected Tokyo inflation data. Stripping out energy and food prices, core-core inflation remained relatively stable, signaling limited urgency for BoJ to proceed with further rate hikes in the near term.

This aligns with the cautious tone seen in the BoJ’s December meeting summary, which revealed deep divisions among policymakers. While a minority of hawks pushed for "forward-looking" and "preemptive" actions, the majority seemed favoring a measured approach, citing concerns over wage growth and external risks.

Verbal intervention from Japanese officials helped limit losses in Yen, nevertheless. Finance Minister Katsunobu Kato reiterated the government’s commitment to addressing excessive currency movements, stating, "The Japanese government has been alarmed by foreign exchange developments, including those driven by speculators, and will take appropriate action against excessive moves." While this provided temporary relief, it was insufficient to reverse Yen's broader weakness.

For the week so far, Dollar is currently the strongest, supported by lingering strength from Fed’s recent hawkish outlook. However, the greenback's momentum remains constrained, with gains capped below last week’s highs amid thin year-end holiday trading. Euro has emerged as the second-strongest currency, followed by Loonie. Yen has taken the weakest spot, followed by Swiss Franc and Aussie. Both Kiwi and Sterling are positioning in the middle.

Looking ahead, market activity is expected to remain subdued through the rest of the week, with an ultra-light economic calendar offering little to stir volatility. The sole notable release is US goods trade balance, which is unlikely to prompt significant moves. Barring surprises, trading volumes are expected to remain low until after the New Year holiday next week.

BoJ summary highlights division on timing of rate hikes

BoJ Summary of Opinions from its December 18–19 meeting revealed a divided board on the timing of monetary policy normalization. While some members advocated for action soon, citing upside risks to prices, others expressed caution due to slow wage growth, soft overseas demand, and heightened uncertainties.

One member emphasized that with economic activity and prices aligning with BoJ’s outlook, risks to inflation were becoming "skewed to the upside." The member argued for a "forward-looking, timely, and gradual" adjustment of monetary policy. Similarly, another member noted that the sustained increase in prices over the past three years, partly driven by Yen's depreciation, would likely contribute to higher underlying inflation, warranting "preemptive" rate hikes.

Conversely, more dovish members maintained that the current risks to prices "do not suggest a pressing need" for rate hike. One member cited uncertainties surrounding tax and fiscal policies in Japan and the stance of the incoming US administration as reasons to maintain the current policy stance, emphasizing a risk management approach.

Overall, the BoJ board appears focused on assessing the outcomes of next year’s spring wage negotiations and the impact of US policy shifts before making further moves toward policy normalization.

Japan's Tokyo CPI core rises to 2.4% in Dec, but core-core dips to 1.8%

Japan's Tokyo core CPI (excluding food) rose from 2.2% yoy to 2.4% yoy in December, marking its highest level since August but falling short of expectations for 2.5%. The increase was largely driven by a 13.5% yoy surge in energy prices, reflecting the phase-out of government subsidies for gas and electricity bills. However, when excluding utility costs, inflation pressures appear steady.

Core-core CPI (excluding food and energy) softened to 1.8% yoy from 1.9% yoy, while services inflation edged up slightly from 0.9% to 1.0%. Meanwhile, headline inflation accelerated to 3.0% yoy from 2.6% yoy, with energy and food prices, including rice, contributing significantly to the increase too.

The uptick in Tokyo inflation highlights lingering pressures from rising utility and food costs, which may weigh on consumer spending and deter firms from implementing further price hikes. These factors, coupled with broader signs of economic weakness, could delay BoJ ’s timeline for raising interest rates.

Japan's industrial output slips -2.3% mom in Nov, indecisive fluctuation continues

Japan's industrial production declined -2.3% mom in November, outperforming expectations of a -3.4% mom drop, but marking the first contraction in three months.

The decrease was driven by weaker exports of semiconductor manufacturing devices and cars, highlighting challenges in external demand. Out of 15 industrial sectors, 11 recorded declines, while 3 sectors reported gains.

Production machinery saw a significant -9.1% drop, largely due to falling exports of chip-making equipment to China and Taiwan, while motor vehicle output fell -4.3%, and fabricated metal products dropped -5.7%.

Despite the slump, the Ministry of Economy, Trade, and Industry maintained its view that industrial production "fluctuates indecisively," while warning of risks tied to the economic outlooks of the US and China.

Looking ahead, METI's poll of manufacturers predicts a rebound, with output expected to rise 2.1% in December and an additional 1.3% in January.

Separately, retail sales posted a robust 2.8% yoy gain, exceeding expectations of 1.5%, signaling resilience in domestic demand.

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.32; (P) 157.70; (R1) 158.42; More...

USD/JPY's rally is trying to resume by breaching 157.91 temporary top and intraday bias is back on the upside. Rise from 139.57 is extending to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. Firm break there will pave the way back to 161.94 high. On the downside, though, below 156.88 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Santa in Japan

Those glued to their screens, hoping for Santa’s arrival, were left disappointed. The major US indices weren’t in good shape yesterday even after a mixed bag of US jobs data showed that the continuing jobless claims in the US advanced to the highest levels in more than 3 years – a sign that it takes longer for people in the US to find a new job. But alas, the bad news did little to boost the Federal Reserve (Fed) doves and support the equity rally. The US 2-year yield fluctuated between 4.30-4.35% range, the S&P500 was slightly down on Thursday, Nasdaq 100 retreated 0.13% and even Bitcoin gave back the Xmas day gains and is settling near the $96K level this morning. But the Dow Jones – which has been going against its tech-heavy major peers lately was very slightly up – by 0.07%, and the mid and small caps eked out better performances. The Russell 2000 gained up to 90% - as a sign of rotation toward smaller and less technology heavy pockets of the market.

In China, equities are better bid since Chinese authorities pledge on Tuesday to sell a record amount of 3 trillion yuan worth of special treasury bonds next year to give support to the economy. The money would be used to boost consumption and investment. But China’s path to recovery will be bumpy. The data released a few hours earlier showed that the industrial profits continue to plunge. They have been almost 5% lower y-o-y last month. And the workforce in finance and property shrank over the past years for the first time on record; the number of people working for developers dived by 27% since the end of 2023.

Santa is in Japan this Xmas

The Nikkei index surged past the 40’000 mark on the back of a weakening yen as the bears are out and selling the yen since the Bank of Japan (BoJ) bypassed a rate hike earlier this month, and more importantly, said that they would wait until next March/April to have more clarity on how the Trump policies will play out. As such, the USDJPY spent Xmas bumping its head against the 158 offers. Today, the yen looks stronger on the back of a freshly released set of stronger-than-expected economic data showing that inflation in Tokyo rose to 3% in December, while retail sales in the country jumped to 2.8% in November, and the contraction in industrial production unexpectedly slowed during the same month. But the BoJ hawks are hard to convince. As it has been the case for most of 2024, the only thing that cools down the yen selloff is the threat from the Japanese officials to intervene and buy the yen. Therefore, buying the dips in the USDJPY is still interesting, and buying the Japanese stocks remains a popular thing to do.

Elsewhere, in the FX, the US dollar index was mostly steady this week – as most traders in major economies were busy dining and wining in Xmas parties. But the latter didn’t prevent the EURUSD from gently pushing lower on rising – and funded - worries that the newly formed French government will face the same faith than the previous one: a divided government that will unlikely approve a reasonable budget proposal to bring the ballooning deficit toward 5%. And the deficits that spiral higher is generally not great news for the euro as the French-German 10-year spread is preparing to close the year near 80bp – the highest since the European sovereign debt crisis a decade ago.

Across the Channel, hope that 2025 will bring good health to the UK economy - ideally with improved relations with once-loved and cherished ones - persists, but the path remains shaky. Cable has been testing the 1.25 support with a greater chance to break the latter to the downside than otherwise. Elsewhere, the AUDUSD is testing the 62 cents support while the USDCAD is trying to find support near the 1.44 this morning – it looks like Trump’s proposal to make Canada the 51st state of the United States didn’t improve sentiment... The rising political risks in Canada, combined to unsupportive oil prices continue to back a further advance in the USDCAD.

Speaking of oil, it’s the same, old narrative. The barrel makes an attempt above the 50-DMA, but remains topped by offers before reaching the 100-DMA – which currently stands near the $71.30pb level. Yesterday’s API data showed a more than 3-mio barrel retreat in US oil inventories. But the drawback barely vacuumed the bulls in, and the weekly data has little power to reverse the bearish trend that will stay intact below the $72.85pb level, which is the major 38.2% Fibonacci retracement on the latest selloff. Crude is set to close the year in the bearish consolidation zone, still waiting for China to get better and to narrow the global supply glut that’s expected to average near 1mbpd in 2025, according to the IEA.

BoJ summary highlights division on timing of rate hikes

BoJ Summary of Opinions from its December 18–19 meeting revealed a divided board on the timing of monetary policy normalization. While some members advocated for action soon, citing upside risks to prices, others expressed caution due to slow wage growth, soft overseas demand, and heightened uncertainties.

One member emphasized that with economic activity and prices aligning with BoJ’s outlook, risks to inflation were becoming "skewed to the upside." The member argued for a "forward-looking, timely, and gradual" adjustment of monetary policy. Similarly, another member noted that the sustained increase in prices over the past three years, partly driven by Yen's depreciation, would likely contribute to higher underlying inflation, warranting "preemptive" rate hikes.

Conversely, more dovish members maintained that the current risks to prices "do not suggest a pressing need" for rate hike. One member cited uncertainties surrounding tax and fiscal policies in Japan and the stance of the incoming US administration as reasons to maintain the current policy stance, emphasizing a risk management approach.

Overall, the BoJ board appears focused on assessing the outcomes of next year’s spring wage negotiations and the impact of US policy shifts before making further moves toward policy normalization.