Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1152; (P) 1.1170 (R1) 1.1180; More....

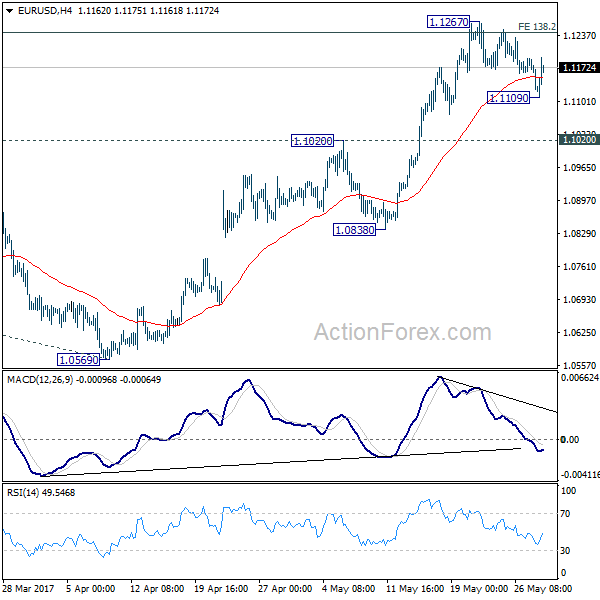

EUR/USD dips to 1.1109 earlier today but recovers quickly. Intraday bias remains neutral as the consolidation from 1.1267 is still in progress. Overall, we remain cautious on strong resistance from 1.1245/98 (138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245) to limit upside and bring reversal. But another rise is still mildly in favor as long as 1.1020 resistance turned support holds. Decisive break of 1.1298 will carry larger bullish implication and target 1.1615 resistance next. On the downside, break of 1.1020 will indicate rejection from 1.1245/98 and turn bias to the downside for 1.0838 support.

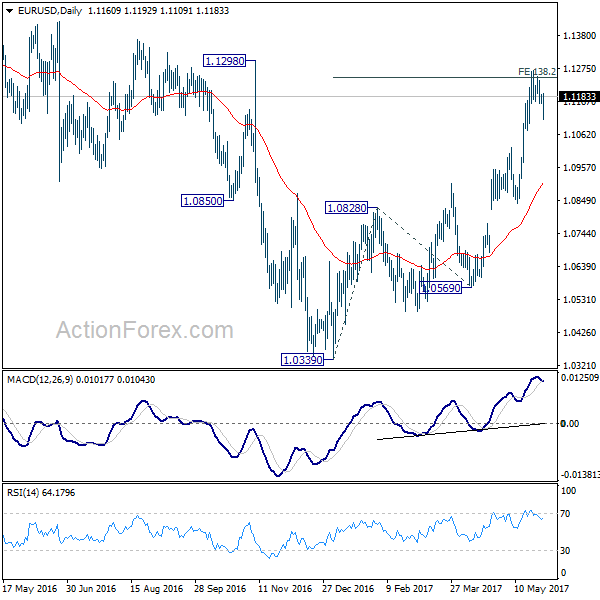

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0888). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

Euro Pares Loss as ECB Said to Discuss Changing Forward Guidance in June

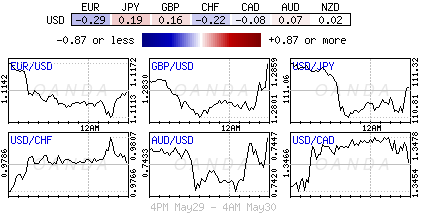

Dollar trades mixed in early US session after release of a batch of economic data. While Euro stays down for the day, it's already pared back much of the earlier loss. At the time of writing, Canadian dollar is the weakest major currency today as WTI crude oil dips below 50 handle again. That's followed closely by Euro and Dollar. Released in US, S&P Case-Shiller 20 cities house price rose 5.9% yoy in March. US Personal income rose 0.4% in April, spending rose 0.4%. PCE core slowed to 1.5% yoy. From Canada, current account deficit widened to CAD -14.1b in Q1. IPPI rose 0.6% mom in April, RMPI rose 1.6% mom in April.

Dallas Fed Kaplan: US growth won't take off

Dallas Fed president Robert Kaplan said in an interview that growth in US is unlikely to take off and therefore "removal of accommodation should be done gradually and patiently". He pointed out growth in "labor force" and "productivity" as the two drivers of GDP. And Kaplan noted that the "problem is labor force growth is very sluggish" and it's going to be that way in the "next 10 years". That's because "population is aging labor force growth therefore is slowing". Nonetheless, he still expects two more rate hikes this year.

Regarding US President Donald Trump's growth policies, Kaplan also offered his views. He noted that tax reform "could be helpful". But if it's a "tax cut financed by increasing the deficit", he's concerned that it "may give a short-term bump to GDP growth, but not a sustainable bump to GDP". And, "over the horizon we'll have similar growth that we have now, except we'll have more leverage, we'll have higher debt to GDP and I think that will be negative for economic growth."

ECB to discuss hawkish change in forward guidance in June

Reuters reported that ECB policymakers will discuss in the upcoming meeting a hawkish change in the upcoming forward guidance. That is, ECB could drop the pledge to add to stimulus if needed. An unnamed governing council member was quoted saying that political risk is clearly down after French election and economic indicators were by and large positive. However, another source noted that the positive environment has been "relatively short" compared to the "long periods of crises". Hence, it's not "responsible to base a major policy shift on such a short upswing".

While ECB may not make any move, not even in the language, it's believed that the central bank should start to do something by latest September. This is with the consideration that the current asset purchase program will end in December. And one way or the other, ECB has to prepare the markets for any policy moves. Euro dipped sharply overnight on surging risks of an early Italian election. But the common currency recovers after the news report on ECB.

Economic data from Eurozone are mildly disappointing today. Eurozone business climate dropped to 0.9% in May, down from 1.1, below expectation of 1.11. Economic confidence dropped to 109.2, down from 109.7, below expectation of 110.0. Industrial confidence rose to 2.8, up from 2.6 but missed expectation of 3.1. Services confidence dropped to 13.0, down from 14.2 and missed expectation of 14.1. German CPI slowed to 1.5% yoy in May, down from 2.0% and below expectation of 1.6%. German import price index dropped -0.1% mom, below expectation of 0.1% mom. French GDP, though, rose more than expected by 0.4% qoq in Q1.

UK PM May: Brexit negotiation the "one, fundamental, defining issue" for the election

UK Prime Minister Theresa May emphasized today that Brexit negotiation is "the one, fundamental, defining issue" voters should consider casting their vote in the election on June 8. She noted that the Conservative has a plan for a "new deep and special partnership with the European Union that returns control to Britain". May is very clear on her tough stance on Brexit negotiations as she said before that "no deal is better than a bad deal", and, "we have to be prepared to walk out". UK's Brexit Secretary David Davis warned that UK has to be "quite tough" with EU as Brussels won't play fair. On the other hand, Labour leader Jeremy Corbyn set out a totally different approach and emphasized that "there's going to be a deal" and "we will make sure there is a deal".

The negotiation is scheduled to start on June 19. Ahead of that, EU's chief Brexit negotiator Michel Barnier urged the European MPs to be vigilant throughout the negotiation. Barnier wanted that once it leaves EU, UK could be "tempted to distance itself from our standards" like consumer projection or financial stability. And, he urged to ensure that this "inevitable divergence" won't become "unfair competition". And he emphasized "full transparency for these negotiations". He reiterated his stance with EU leaders that "sufficient progress" is needed on the issues of the "divorce bill", citizens right and Ireland border arrangements before the talk of a trade deal.

Swiss KOF economic barometer decreased "substantially"

Swiss KOF Economic Barometer dropped to 101.6 in May, down from 106.3 and missed expectation of 106.2. While the reading stood slightly above the long-term average, it did decrease substantially as compared to April. KOF noted that the decreased was due to negative contributions from manufacturing, export development, domestic consumption, financial and construction sectors. And inside manufacturing "the negative outlook was mainly visible in the paper, metal and electronic industries."

Released earlier today, New Zealand building permits dropped -7.6% mom in April. Australia building approvals rose 4.4% mom in April. Japan unemployment rate was unchanged at 2.8% in April, household spending dropped -1.4% yoy, retail sales rose 3.2% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1152; (P) 1.1170 (R1) 1.1180; More....

EUR/USD dips to 1.1109 earlier today but recovers quickly. Intraday bias remains neutral as the consolidation from 1.1267 is still in progress. Overall, we remain cautious on strong resistance from 1.1245/98 (138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245) to limit upside and bring reversal. But another rise is still mildly in favor as long as 1.1020 resistance turned support holds. Decisive break of 1.1298 will carry larger bullish implication and target 1.1615 resistance next. On the downside, break of 1.1020 will indicate rejection from 1.1245/98 and turn bias to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0888). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Apr | -7.60% | -1.80% | -1.20% | |

| 23:30 | JPY | Unemployment Rate Apr | 2.80% | 2.80% | 2.80% | |

| 23:30 | JPY | Household Spending Y/Y Apr | -1.40% | -0.70% | -1.30% | |

| 23:50 | JPY | Retail Trade Y/Y Apr | 3.20% | 2.20% | 2.10% | |

| 1:30 | AUD | Building Approvals M/M Apr | 4.40% | 3.00% | -13.40% | -10.30% |

| 6:00 | EUR | German Import Price Index M/M Apr | 0.10% | -0.50% | ||

| 6:45 | EUR | French GDP Q/Q Q1 P | 0.30% | 0.30% | ||

| 7:00 | CHF | KOF Leading Indicator May | 106.2 | 106 | ||

| 9:00 | EUR | Eurozone Business Climate Indicator May | 1.11 | 1.09 | ||

| 9:00 | EUR | Eurozone Economic Confidence May | 110 | 109.6 | ||

| 9:00 | EUR | Eurozone Industrial Confidence May | 3.1 | 2.6 | ||

| 9:00 | EUR | Eurozone Services Confidence May | 14.1 | 14.2 | ||

| 9:00 | EUR | Eurozone Consumer Confidence May F | -3.3 | -3.3 | ||

| 12:00 | EUR | German CPI M/M May P | -0.10% | 0.00% | ||

| 12:00 | EUR | German CPI Y/Y May P | 1.60% | 2.00% | ||

| 12:30 | CAD | Current Account (CAD) Q1 | -11.4B | -10.7B | ||

| 12:30 | CAD | Industrial Product Price M/M Apr | 0.80% | |||

| 12:30 | CAD | Raw Materials Price Index M/M Apr | -1.60% | |||

| 12:30 | USD | Personal Income Apr | 0.40% | 0.20% | ||

| 12:30 | USD | Personal Spending Apr | 0.40% | 0.00% | ||

| 12:30 | USD | PCE Deflator M/M Apr | 0.20% | -0.20% | ||

| 12:30 | USD | PCE Deflator Y/Y Apr | 1.70% | 1.80% | ||

| 12:30 | USD | PCE Core M/M Apr | 0.10% | -0.10% | ||

| 12:30 | USD | PCE Core Y/Y Apr | 1.50% | 1.60% | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Mar | 5.60% | 5.90% | ||

| 14:00 | USD | Consumer Confidence May | 120 | 120.3 |

CAC Ticks Higher on Mixed French Numbers

The French stock market continues to have a quiet week. In the Tuesday session, the CAC is trading at 5,327.50 points. On the release front, there are no eurozone events. French indicators were mixed. Preliminary Consumer Spending rebounded in April with a gain of 0.5%, following two declines. This was short of the estimate of 0.8 percent. Preliminary GDP remained unchanged at 0.4 percent in the first quarter, edging above the estimate of 0.3 percent. On Wednesday, the eurozone publishes CPI Flash Estimate and France will release Preliminary CPI.

ECB President Mario Draghi testified before a EU parliamentary committee on Monday, but there were no dramatic statements or hints from the ECB head. Draghi acknowledged that the euro-area economy was improving, but said that inflation and wage growth remained weak, and the ECB would continue its asset-purchase program. The scheme is due to wind up in December, and stronger eurozone numbers had raised speculation that the central bank might revisit its monetary stance and perhaps taper the program at the June policy meeting. However, Draghi appears to be putting the markets on notice that the June policy meeting will be a non-event, and if there are any changes to monetary policy, they will likely be minor in nature.

There were plenty of questions marks about the eurozone economy at the start of 2017. Britain's vote to leave the European Union stunned and stung Europe, with EU members wondering who would pull out of the club next. The jitters increased as Donald Trump was sworn in as US president, who ran on a protectionist campaign of "America first". Just four months later, skies are looking blue for the euro-area. Although Donald Trump has managed to tussle with German Chancellor Angela Merkel and Brexit remains a serious challenge for the EU, the political and economic landscape has improved considerably. Fears of a populist wave across the continent have receded, as nationalist, anti-EU parties failed to win elections in the Netherlands and France. On the economic front, indicators continue to point upwards, as unemployment has dropped and growth is higher. The EU Spring Forecast has forecast Eurozone GDP to rise 1.7% in 2017 and 1.8% in 2018, with growth in the EU expected at 1.9% for both years. Investors have jumped on the bandwagon, as the CAC has climbed 10.4% since the start of 2017.

Euro Geopolitical Fears Sap Risk Appetite

Political risk in the euro area is not dead and is currently weighing on the EUR along with Draghi's 'dovish' message yesterday that emphasised that the eurozone still requires substantial stimulus – if so, its suggests that there is little likelihood of an imminent QE tapering announcement at next weeks ECB meeting.

The probability of Italian snap elections has risen substantially, despite the baseline scenario is still for general elections to be held next-year. The momentum for early elections has grown in recent sessions and if they were to be held under the new voting system that has been reportedly agreed across parties, the odds are rising that the anti-establishment parties could win the government.

Under the above scenario, investors should expect volatility in Italian and periphery assets to increase in the coming weeks.

Euro zone finance ministers failed to agree with the IMF on Greek debt relief or to release new loans to Athens last week, but did come close enough to aim to do both at their June meeting. What's Greece to do?

Markets focus will be on today's PCE release (08:30 am EST), the Fed's preferred measure of inflation.

1. Global stocks finding little or no traction

With China, Hong Kong and Taiwan markets again closed for holiday's overnight led to thin trading conditions.

In Japan, the Nikkei share average inched down -0.02% overnight as the market felt the weight of a stronger yen (¥110.89) on risk aversion, while the broader Topix rallied +0.2% after erasing an earlier decline of -0.5%.

In South Korea, the Kospi dropped -0.4%, falling for a second day from record highs as investors booked profits.

In Singapore, the Straits Times Index slid -0.4%.

In Europe, indices trade lower across the board with notable under performance from the French CAC, and German DAX with dovish Draghi comments on the Eurozone economy weighing on sentiment. On the FTSE 100 airline stocks trade lower.

In the U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 -0.5% at 3563, FTSE -0.3% at 7524, DAX flat at 12624, CAC-40 -0.7% at 5298, IBEX-35 -0.2% at 10858, FTSE MIB -0.3% at 20731, SMI -0.4% at 8993, S&P 500 Futures -0.1%.

2. Oil slips on oversupply worries despite OPEC deal, gold shines

Oil prices remain on the back foot, pressured by market concerns that production cuts by OPEC and some non-OPEC members may not be enough to drain a global glut that has depressed the market for the past three-years.

Ahead of the U.S open, benchmark Brent crude is down -40c a barrel at +$51.89 after having gained +14c yesterday. U.S light crude has fallen -20c to +$49.60

OPEC and other oil producers, including Russia, agreed last week to keep a tight rein on supply until the end of Q1, nine-months longer than originally planned back in November 2016.

The collective output by OPEC and other producers will be held around -1.8m bpd below its level at the end of 2016.

Technically, the market is still trying to decide if OPEC has done enough to balance supply and demand. Nevertheless, the problem for OPEC is oil supply in the U.S, where shale production continues to boom.

Market price action since the May 25 decision would suggest that the market was expecting much deeper cuts and a longer deal. Despite the ongoing cuts, oil prices have not been able to rally much beyond +$50 per barrel.

Data last week showed that U.S. drillers have added rigs for 19-consecutive weeks to reach 722, the highest in two years.

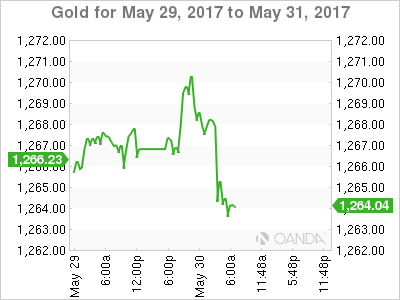

Gold has edged up to touch a one-month high overnight, with investors turning to the safe-haven asset as geopolitical tensions sap their appetite for risk. Spot gold has rallied +0.1% to +$1,267.30 per.

3. Euro periphery yields rally

Geopolitical risks in Europe have periphery yields backing up. Italian 10-year government yields have backed up +13 bps to + 2.20% on reports that Italy's main parties are close to an agreement on a new voting law and that former PM Renzi said he favored an election in autumn. The threat of an anti-Euro party governing Italy is expected to have Italian assets underperforming in the short to medium term.

In the U.S, the Fed has strongly signalled that it will raise interest rates next month, but officials have promised to keep a close watch on inflation, and their preferred gauge – personal-consumption expenditures price index or PCE – will be in the spotlight this morning at 08:30 am EST. The yield on 10-year Treasuries declined less than one basis point to +2.24%.

Down-under, Aussie 10-year yields fell -2bps to +2.39%.

4. Dollar steady

Modest risk-off is playing out in FX space going into today's key PCE inflation data and China manufacturing PMI's this week.

Note: Both reports have shown underwhelming prints over the past two-months.

A new round of political worries over Greece, Italy and Britain has the respected regional currencies under pressure.

The EUR/USD (€1.1162) has drifted from its recent seven-month highs made last week as a plethora of May inflation data backs the ECB's view that extraordinary monetary accommodation will remain in place for the foreseeable future.

Sterling (£1.2854) is beginning to find resistance to the topside as more polls show the gap between PM May's Conservatives and Labour narrowing. The pound is currently trading in 'no-man's land' after probing above £1.3000 last week.

Note: Conservative Party's lead continues to erode (Opinium Poll: Con: +45% (-1); Labour +35% (+2); ComRes Poll: Con: +46% (-2); Labour +34% (+4); ORB/Telegraph Poll: Con: +44% (-2); Labour +38% (+4).

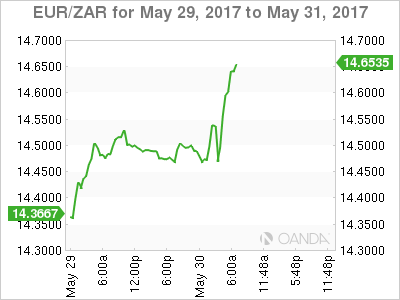

The ZAR ($13.0700) continues to exhibit volatility. The rand weakened yesterday after South Africa President Zuma survived another confidence motion from within his ruling party. However, the currency recovered after reports circulated that the DA office would file charges against the President.

5. Japan near full employment, but no inflation, German inflation falls

Japan has a labor shortage, but the labor structure is not allowing wage inflation.

Data overnight shows that Japan's jobless rate remains at its 23-year low of +2.8%, while household spending again remains relatively soft.

Japan's April overall household spending y/y is -1.4% vs. -0.9%e – a 14th consecutive month of declines.

Data released by six German states this morning suggest that German consumer price inflation fell a little more than expected in May, to about +1.5% from +2.0% in April. The market consensus was looking for a +1.6% reading.

Regional releases hint at a pick-up of food inflation this month, but energy inflation dipped, in line with expectations, given the fall in oil prices.

Market Update – European Session: German And Spanish CPI Data Gives Credibility That ECB Can Wait For Any Exit...

Notes/Observations

Plethora of May inflation data backs Draghi view that extraordinary monetary accommodation to stay for now

European confidence data mixed in session (France beats; Euro Zone misses)

US and UK participants return from an extended weekend; China markets (Shanghai and HK) closed for holiday

Overnight

Asia:

Japan Apr Jobless Rate: 2.8% v 2.8%e v 2.8% prior (matches lowest rate since Jun 1994), Job-To-Applicant Ratio: 1.48 v 1. 46e (Highest since November 1990)

Japan Apr Overall Household Spending Y/Y: -1.4% v -0.9%e (14th straight decline)

China foreign exchange trade system (CFETS): To launch a national transaction gauge to improve the interbank benchmark interest rate system and improve the efficiency of monetary policies; effective Wed, May 31ste

Europe:

ECB's Draghi reiterated that economic outlook was improving with downside risks moderating; firmly convinced that Euro Area still needed policy support (in-line with press conference

ECB's Weidmann (Germany): expansionary ECB policy was appropriate in principle in light of subdued price pressures. Timing of ECB normalization was a legitimate question

German press reports noted that Greek government was prepared for the possibility of going without the next bailout payment of €7B if creditors did not agree on debt relief for the country (later refuted by Greece govt)

PM May reiterated stance that was prepared to walk away from Brexit talks without a deal with the EU if the agreement was not good enough for the country

Times/Survation Poll on Parliamentary elections: Support for UK Conservatives at 43%; Labour at 37%

Opposition Labour Party leader Corbyn: Would be open to Scotland referendum talk with SNP if Labour party wins next month's elections

Economic Data

(NL) Netherlands May Producer Confidence: 6.1 v 8.3 prior

(DE) Germany Apr Import Price Index M/M: -0.1% v +0.1%e; Y/Y: 6.1% v 6.3%e

(FR) France May Consumer Confidence: 102 v 101e (10-year high)

(FR) France Apr Consumer Spending M/M: 0.5% v 0.8%e; Y/Y: -0.5% v +0.6%e

(FR) France Q1 Preliminary GDP (2nd reading) Q/Q: 0.4% v 0.3%e; Y/Y: 1.0% v 0.8%e

(DE) Germany May CPI Saxony M/M: -0.1% v -0.1% prior; Y/Y: 1.6 v 2.1% prior

(CH) Swiss May KOF Leading Indicator: 101.6 v 106.0e

(ES) Spain May Preliminary CPI M/M: -0.1% v 0.0%e; Y/Y: 1.9% v 2.1%e

(ES) Spain May Preliminary CPI EU Harmonized M/M: 0.0% v -0.1%e; Y/Y: 2.0% v 2.1%e

(SE) Sweden Q1 GDP Q/Q: 0.4% v 0.9%e; Y/Y: 2.2% v 2.9%e

(SE) Sweden Apr Retail Sales M/M: 1.3% v 0.8%e; Y/Y: 4.5% v 2.8%e

(DE) Germany May CPI Brandenburg M/M: -0.1% v -0.1% prior; Y/Y: 1.4% v 1.8% prior

(DE) Germany May CPI Hesse M/M: 0.0% v 0.0% prior; Y/Y: 1.7% v 2.1% prior

(DE) Germany May CPI Bavaria M/M: -0.1% v -0.1% prior; Y/Y: 1.4% v 1.9% prior

(DE) Germany May CPI Baden Wuerttemberg M/M: -0.1% v 0.0% prior; Y/Y: 1.5% v 2.0% prior

(DE) Germany May CPI North Rhine Westphalia M/M: -0.2% v +0.1% prior; Y/Y: 1.6% v 2.1% prior

(PT) Portugal May Consumer Confidence: # v -1.8 prior; Economic Climate Indicator: # v 1.8 prior

(EU) Euro Zone May Business Climate Indicator: # v 1.11e; Consumer Confidence (Final): # v -3.3e, Economic Confidence: # v 110.0e, Industrial Confidence: # v 3.1e, Services Confidence: # v 14.2e

(PT) Portugal May Consumer Confidence: +0.2 v -1.8 prior; Economic Climate Indicator: 2.0 v 1.8 prior

Fixed Income Issuance:

(DK) Denmark sold total DKK3.68B in 3-month and 6-month bills

(ZA) South Africa sold total ZAR vs. ZAR2.65B indicated in 2040, 2044 and 2048 bonds

(IT) Italy Debt Agency (Tesoro) sold total €5.75B vs. 4.75-5.75B indicated range in 5-year and 10-year BTP Bonds

Sold €3.0B vs €2.5-3.0B indicated in 1.20% Jan 2022 BTP; Avg Yield: 0.88% v 1.04% prior; Bid-to-cover: 1.39x v 1.59x prior

Sold €2.75B vs €2.25-2.75B indicated in 2.2% June 2027 BTP; Avg Yield: 2.15% v 2.29% prior; Bid-to-cover: 1.49x v 1.32x prior

(IT) Italy Debt Agency (Tesoro) sold €1.75 vs. €1.25-1.75B in Feb 2024 CCTeu (Flating-rate bond); Avg Yield: 0.92% v 0.93% prior; bid-to-cover: 1.41x v 1.29x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.5% at 3563, FTSE -0.3% at 7524, DAX flat at 12624, CAC-40 -0.7% at 5298, IBEX-35 -0.2% at 10858, FTSE MIB -0.3% at 20731, SMI -0.4% at 8993, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes

European Indices trade lower across the board with notable under performance from the French CAC, with dovish Draghi comments on the Eurozone economy slightly souring sentiment.

Corporate data flow has been light today, with Airliners in focus. Ryanair trades lower after inline results and initial FY18 guidance which was slightly below consensus. British Airways parent Int Con Group is under pressure after a systems failure over the weekend led to the cancellations of 100s of flights effecting some 75K passengers. Elsewhere Akzo Nobel shares trade lower after chances of a tie up with PPG diminishes after a high court ruling rejecting shareholder request to oust its Chairman.

Equities

Consumer discretionary [Ryanair [RYA.UK] -1.1% (Earnings), International Consolidated Airlines [IAG.UK] -3.0% (Flight disruptions and cancellations over the weekend), Aryzta [ARYN.CH] -2.4% (Earnings, CFO comments)]

Materials: [ Akzo Nobel [AKZA.NL) -1.8% (Court rejects investor requests over PPG take over rejection)]

Industrials: [Porr Ag [ABS2.DE] -1.5% (Earnings)]

Technology: [Kainos Grp [KNOS.UK] -4.5% (Earnings)]

Speakers

Greece govt spokesperson Tzanakopoulos refuted earlier reports that Greece would reject next tranche of aid

Spain PM Rajoy: 2017 GDP growth on track to reach 2.7%. Country might recover its pre-crisis GDP level in H1

IEA: Norway should prepare for lower oil revenues in the future

Japan ruling coalition partner Komeito party leader: PM Kuorda has achieved a degree of success; any new BOJ Gov should avoid making dramatic changes

PBOC Advisor Sheng Songcheng saw no condition for monetary easing in 2017

Currencies

The USD was steady as dealers noted a new round of political worries over Greece, Italy and Britain simmered.

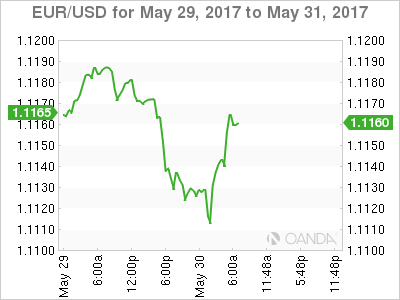

The EUR/USD drifted from recent 6 1/2 month highs made last week as a plethora of May inflation data backs Draghi view that extraordinary monetary accommodation to stay for now. Pair at 1.1140 area just ahead of the NY morning.

GBP finding headwinds as more polls show gap between Conservatives and Labour narrowing. GBP/USD trading in the mid-1.28 area after probing 1.30 last week.

ZAR currency (Rand) continued to exhibit volatility. The rand weakened on Monday after South Africa President Zuma survived another confidence motion from within his ruling party. However, the currency recovered after reports circulated that the DA office would file charges against the President.USD/ZAR back above the 13 handle

Fixed Income

Bund futurestrade at 162.14 down 10 ticks, well above last week's close as subdued euro zone inflation is likely to keep investors running to German government bonds. Resistance lies near the 168.81 level followed by 163.54. A break of the 161.65 support level could see lows target 159.96 followed by 157.50.

Gilt futurestrade at 129.25 higher by 1 tick, as markets return from a long holiday weekend. Last week's rally took out both the 129.00 handle and the 129.14 April 18th high. Price finds key support at the 128.68 support level. An acceleration lower could test the 127.43 region. Resistance stands at 129.75 then 130.28 followed by 132.80.

Monday's liquidity report showed Friday's excess liquidity rose to €1.6330T a rise of €7B from €1.6260T prior. Use of the marginal lending facility rose to €242M from €238M prior.

Corporate issuancesaw $36.25B issued last week, ahead of last week's forecast of $35B. For the week ahead, analysts eye issuance to come in around $20B.

In Euro denominated issuance €28.6B came to market last week via 33 issuers and 41 tranches.

Looking Ahead

(BE) Belgium May CPI M/M: No est v 0.2% prior; Y/Y: No est v 2.3% prior

(ES) Spain Apr YTD Budget Balance: No est v -€5.6B prior

05:30 (EU) ECB allotment in 7-Day Main Refinancing Tender

05:30 (HU) Hungary Debt Agency (AKK) to sell 3-month Bills

05:30 (BE) Belgium Debt Agency (BDA) to sell €1.2-1.6B in 3-Month and 6-month Bills

06:00 (PT) Portugal Apr Industrial Production M/M: No est v -0.6% prior; Y/Y: No est v 1.9% prior

06:00 (PT) Portugal Apr Retail Sales M/M: No est v -2.4% prior; Y/Y: No est v 4.7% prior

06:00 (IE) Ireland May Unemployment Rate: No est v 6.2% prior

06:15 (FI) ECB's Liikanen (Finland) speaks at Austrian central bank conference

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil May FGV Inflation IGPM M/M: -0.8%e v -1.1% prior; Y/Y: 1.7%e v 3.4% prior

07:30 (BR) Brazil President Temer at investment forum

08:00 (DE) Germany May Preliminary CPI M/M: -0.1%e v 0.0% prior; Y/Y: 1.6%e v 2.0% prior

08:00 (DE) Germany May Preliminary CPI EU Harmonized M/M: -0.1%e v 0.0% prior; Y/Y: 1.5%e v 2.0% prior

08:00 (ZA) South Africa Apr Budget Balance (ZAR): No est v 3.1B prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Apr Personal Income: 0.4%e v 0.2% prior; Personal Spending: 0.4%e v 0.0% prior; Real Personal Spending (PCE): 0.2%e v 0.3% prior

08:30 (US) Apr PCE Deflator M/M: +0.2%e v -0.2% prior; Y/Y: 1.7%e v 1.8% prior

08:30 (US) Apr PCE Core M/M: +0.1%e v -0.1% prior; Y/Y: 1.5%e v 1.6% prior

08:30 (CA) Canada Apr Industrial Product Price M/M: No est v 0.8% prior; Raw Materials Price Index M/M: No est v -1.6% prior

08:30 (CA) Canada Q1 Current Account: -$12.0Be v -$10.7B prior

09:00 (US) Mar S&P / Case-Shiller 20-City M/M: 0.90%e v 0. 69% prior; Y/Y: 5.61%e v 5.85% prior; House Price Index (HPI): No est v 193.49 prior

09:00 (US) Mar S&P / Case-Shiller (overall) HPI Y/Y: No est v 5.76% prior, House Price Index (HPI): No est v 185.56 prior

09:00 (EU) Weekly ECB Forex Reserves:

09:00 (CL) Chile Apr Manufacturing Production Y/Y: -1.0%e v +1.9% prior; Industrial Production Y/Y: -3.3%e v -8.3% prior

09:00 (CL) Chile Apr Total Copper Production: No est v 378.3K tons prior

09:00 (DE0 Merkel's Chief Economic aide on G20 in Berlin

09:00 (RU) Russia announces weekly OFZ bond auction

10:00 (US) May Consumer Confidence: 119.8e v 120.3 prior, Expectations Index: No est v 106.7 prior, Present Situation Index: No est v 140.6 prior

10:30 (US) May Dallas Fed Manufacturing Activity: 15.0e v 16.8 prior

10:30 (CA) Canada to sell 3-month, 6-month and 12-month Bills

11:00 (BR) Brazil to sell I/L 2022, 2026, 2035 and 2055 Bonds

11:30 (US) Treasury to sell 4-week Bills

11:30 (US) Treasury to sell 3-Month and 6-month Bills

15:30 (MX) Mexico Apr YTD Budget Balance (MXN): No est v 309.1B prior

16:00 (US) Weekly Crop Progress Report

US Data Eyed Ahead Of June Fed Meeting

- US inflation, income and spending key ahead of June Fed meeting;

- Draghi's monetary support comments and Greek speculation weigh on EUR in early trade.

US equity markets are expected to open slightly lower after the long bank holiday weekend, with traders looking to the income, spending and inflation data from the US to spark things back to life.

With markets still heavily pricing in a rate hike at the next meeting in a couple of weeks, there is the potential for disappointment yet again today. The upward revision to first quarter growth may have settled people's nerves a little but a weak inflation report today could raise questions ahead of the June meeting. We've already had some policy makers raising concerns about the lack of inflation and a weak number today may be just enough to convince them to hold off on raising rates for a little longer.

The income and spending data will also be of interest, with consumer activity of course being so important for the US economy. Both income and spending are expected to have grown by 0.4% in April which is consistent with the retail sales data and comes following a very disappointing first quarter. Strong figures today would be consistent with the current Fed belief that the slowdown in the first quarter was transitory, as it proved to be over the last few years.

The euro has been under some pressure this morning, particularly against the yen which has strengthened across the board, with comments from ECB Mario Draghi and Greek loan repayment reports weighing on the currency in early trade. Draghi's claim that the eurozone still needs an extraordinary amount of monetary support would suggest the central bank may not be as keen to reign in its stimulus program as has been speculated. That said, the scale of the sell-off combined with the rebound we've already seen, would suggest investors still expect further reductions in stimulus later this year.

The rebound has also be aided by a Greek government spokesman denying reports over the weekend that the country is considering opting out of its loan repayment in deny unless lenders come to an agreement on debt relief next month. Debt relief continues to be a major sticking point for negotiations, with the IMF insistent that something must be done in order to make the county's debt sustainable. Of course, this still remains a controversial issue, particularly in Germany where the public will head to the polls later this year. Should Angela Merkel come to an agreement on debt relief just ahead of the election, it could be damaging for her so it'll be interesting to see how she gets around it.

DAX Edges Higher, Markets Eye German Preliminary CPI

The DAX index continues to have a quiet week. In the Tuesday session, the DAX is trading at 12,613.75 points. On the release front, German Import Prices declined 0.1%, short of the forecast of +0.2%. Later in the day, Germany releases Preliminary CPI, which is expected to decline 0.1%. On Tuesday, Germany releases Retail Sales and the Eurozone publishes CPI Flash Estimate.

The markets were all ears on Monday as ECB President Mario Draghi testified before the EU parliamentary committee for economic affairs. Draghi acknowledged that the euro-area economy was improving, but said that inflation and wage growth remained weak, requiring the ECB to continue its asset-purchase program. The scheme is due to wind up in December, and stronger data had raised speculation that the central bank might revisit its monetary stance and perhaps taper the program at the June policy meeting. Draghi’s message remains one of caution, and appears to be putting the markets on notice that any moves in June will likely be of a minor nature.

There were serious questions about the eurozone economy at the start of 2017. Britain’s stunning vote to depart the European Union sent shock waves across the continent, with EU members fearing that the move could invigorate euro-skeptics and threaten the integrity of the EU. The jitters increased as Donald Trump was sworn in as US president, who ran on a protectionist campaign of “America first”. Fast forward to the month of May, and the picture has brightened considerably. Donald Trump has managed to tussle with German Chancellor Angela Merkel and Brexit remains a serious challenge for the EU, but the political and economic landscape has shifted for the better. Fears of a populist wave across the continent have receded, as nationalist, anti-EU parties failed to win elections in the Netherlands and France. On the economic front, indicators continue to point upwards, as unemployment has dropped and growth is higher. The EU Spring Forecast has forecast Eurozone GDP to rise 1.7% in 2017 and 1.8% in 2018, with growth in the EU expected at 1.9% for both years. Investors have climbed on the bandwagon, as the DAX has jumped 10.3% since the start of the year, and continues to hit record highs.

The US economy slowed down considerably in the first quarter of 2107, and there are no indications as of yet that we’ll see a rebound in the second quarter. Will this lead to the Fed rethinking a June rate hike? The markets don’t appear concerned, as the odds of a 0.25% rate hike have increased to 84%. At the same time, the likelihood of a rate hike in the second half of 2017 are low. The odds for a September rate are just 26%, with the markets unclear on whether the Fed will make further moves this year if inflation remains below the Fed target. Political concerns are a serious worry, as the Trump administration is embroiled in scandals, with several congressional investigations probing into Trump’s alleged connections with Russian politicians. A weakened White House raises doubts if Trump will be able to keep his election promises to lower taxes and cut government spending.

Euro Edges Higher, German CPI Next

The euro has posted small gains in the Tuesday session, after starting the week with losses. Currently, EUR/USD is trading at 1.1140. On the release front, German Import Prices declined 0.1%, short of the forecast of +0.2%. Later in the day, Germany releases Preliminary CPI, which is expected to decline 0.1%. In the US, today's highlight is CB Consumer Confidence, which is expected to remain steady at 120.1 points. On Tuesday, Germany releases Retail Sales and the Eurozone publishes CPI Flash Estimate. The US will release Pending Home Sales.

The markets were all ears on Monday as ECB President Mario Draghi testified before the EU parliamentary committee for economic affairs. Draghi acknowledged that the euro-area economy was improving, but said that inflation and wage growth remained weak, requiring the ECB to continue its asset-purchase program. The scheme is due to wind up in December, and stronger data had raised speculation that the central bank might revisit its monetary stance and perhaps taper the program at the June policy meeting. Draghi's message remains one of caution, and appears to be putting the markets on notice that any moves in June will likely be of a minor nature.

There were plenty of questions marks about the eurozone economy at the start of 2017. Britain's vote to leave the European Union stunned and stung Europe, with EU members wondering who would pull out of the club next. The jitters increased as Donald Trump was sworn in as US president, who ran on a protectionist campaign of “America first”. Just four months later, the picture is much brighter for the euro-area. Donald Trump has managed to tussle with German Chancellor Angela Merkel and Brexit remains a serious challenge for the EU, but the political and economic landscape has shifted for the better. Fears of a populist wave across the continent have receded, as nationalist, anti-EU parties failed to win elections in the Netherlands and France. On the economic front, indicators continue to point upwards, as unemployment has dropped and growth is higher. The EU Spring Forecast has forecast Eurozone GDP to rise 1.7% in 2017 and 1.8% in 2018, with growth in the EU expected at 1.9% for both years. Investors have shown their approval by snapping up the euro, which has jumped 6.5% since the start of the year.

The US economy slowed down considerably in the first quarter of 2107, and there are no indications as of yet that we'll see a rebound in the second quarter. Will this lead to the Fed rethinking a June rate hike? The markets don't appear concerned, as the odds of a 0.25% rate hike have increased to 84%. At the same time, the likelihood of a rate hike in the second half of 2017 are low. The odds for a September rate are just 26%, with the markets unclear on whether the Fed will make further moves this year if inflation remains below the Fed target. Political concerns are a serious worry, as the Trump administration is embroiled in scandals, with several congressional investigations probing into Trump's alleged connections with Russian politicians. A weakened White House raises doubts if Trump will be able to keep his election promises to lower taxes and cut government spending.

Technical Outlook: Spot Gold – Corrective Action To Precede Fresh Upside

Spot Gold price eased on Tuesday from fresh four week high at $1270 and returned into thick daily cloud, hitting session low at $1261. Bullish technicals are reinforced by positive sentiment on renewed safe-haven demand that supports the yellow metal's price. In addition, repeated close above $1264 Fibo 61.8% pivot was bullish signal for extension towards next target at $1276. Current pullback could be seen as corrective action which should be ideally contained by rising 10SMA/Tenkan-sen at $1258. However, extended pullback cannot be ruled out as slow stochastic is back into overbought territory and formed bearish divergence that may signal further easing. Top of thick 4-hr cloud at $1255 and last Friday's low at $1253 are next good supports which should keep downticks limited to avert risk of retesting key near-term support at $1245 (daily cloud base).

Res: 1267, 1270, 1276, 1280

Sup: 1261, 1258, 1255, 1253

Euro Takes A Hit

The common European currency took a hit during the Asian morning Tuesday. Even though there was no clear catalyst behind this move, market chatter attributes it primarily to a media report released overnight suggesting that Greece may opt out of its next bailout payment, if it is unable to strike a debt relief deal with its creditors. We have to note though, that only one German newspaper reported this story. As such, unless we see more related reports, we doubt that market focus will remain on this issue for very long.

Instead, we think that today, investors will likely shift their attention to Germany's CPI data for May (see below), amid heightened speculation the ECB is set to appear slightly more optimistic soon. In this respect, Draghi's remarks yesterday did not reveal much. He mostly stuck to his script, reiterating that even though the bloc's economy is improving, underlying inflationary pressures remain subdued and thus, substantial monetary stimulus is still necessary.

Interestingly enough though, he repeated that at the June meeting, policymakers will have updated economic forecasts and will be able to make their judgement on the distribution of risks surrounding growth and inflation. In our view, this suggests a small change in language may indeed be on the cards soon. The ECB could signal that the risks surrounding the outlook for growth are no longer tilted to the downside, and instead echo the recent view of 'some members' in the April minutes that the risks are 'broadly balanced'.

Today's highlights:

During the European day, Germany's preliminary CPI figures for May will be in focus. The forecast is for the nation's inflation rate to have declined notably. We see the risks surrounding that forecast as skewed to the upside, perhaps for a smaller-than-anticipated decline, considering that the preliminary Markit composite PMI for the month showed that German businesses raised their prices at one of the steepest rates in six years. Should Germany's CPI rate surprise to the upside, it could raise some speculation for a positive surprise in the bloc's print that is due to be released the following day and thereby, bring EUR under renewed buying interest.

EUR/USD tumbled overnight, falling below the support (now turned into resistance barrier) of 1.1160 (R1). During the early European morning Tuesday, the price looks to be headed for a test near the support zone of 1.1100 (S1). We think that the pair could stay near that key level and wait for Germany's CPI. If indeed we see a positive surprise, the rate could rebound and test the 1.1160 (R1) barrier, where a clear break could set the stage for further upside recovery towards 1.1230 (R2). On the other hand, if the nation's CPI rate declines in line with the consensus, the latest pullback could continue. A decisive break below 1.1100 (S1) could initially aim for 1.1070 (S2).

From Sweden, we get GDP data for Q1. The forecast is for GDP growth to have slowed somewhat in quarterly terms, but to have accelerated in yearly terms. We also get retail sales for April from both Sweden and Norway.

From the US, we get personal income and spending data, all for April. The forecast is for both the income and the spending rates to have risen from the previous month. We also get the core PCE price index for April, though no forecast is available for the yearly figure. The monthly figure is anticipated to rise 0.1% mom, which would drag the yearly rate down to +1.4% yoy from +1.6% yoy. In case of strong personal income and spending data but a soft PCE print, we are likely to see a choppy reaction in USD. We think that in order for the currency to assume a clear direction afterwards, we would need to see a notable surprise in at least one of these figures.

USD/JPY traded lower yesterday, after it hit resistance near the 111.50 (R1) barrier. In case US data are strong today, the pair could recover some of its latest losses and rebound to test the 111.50 (R1) level again. On the other hand, overall disappointing data could generate some doubts as to whether a Fed June rate hike is indeed as likely as market pricing currently suggests (84%) and thereby lead to further downside in this pair. An initial break below 110.50 (S1) could see scope for declines towards the next support at 110.20 (S2).

We have three speakers on the agenda: ECB Executive Board members Ewald Nowotny and Erkki Likanen, as well as Fed Board Governor Lael Brainard. We think market focus may be primarily on Brainard, as she will be speaking about monetary policy, a topic she did not spend too much time on during her recent appearances. Considering that she will be speaking after the core PCE print is out, her view on inflation may be of particular interest to investors ahead of the June policy meeting.

EUR/USD

Support: 1.1100 (S1), 1.1070 (S2), 1.1020 (S3)

Resistance: 1.1160 (R1), 1.1230 (R2), 1.1270 (R3)

USD/JPY

Support: 110.50 (S1), 110.20 (S2), 109.70 (S3)

Resistance: 111.50 (R1), 112.10 (R2), 113.10 (R3)