Sample Category Title

USD/CAD Canadian Dollar Lower Even As USD Caught In Political Drama

USD/CAD Canadian Dollar Lower Even as USD Caught in Political Drama

The Canadian dollar was lower versus its American counterpart on Tuesday. The loonie had no support from oil prices as concerns about Libyan output will tip the scales in favour of the oil glut remaining in the market despite the efforts of the Organization of the Petroleum Exporting Countries (OPEC) and other major producers to cut production levels for another 9 months.

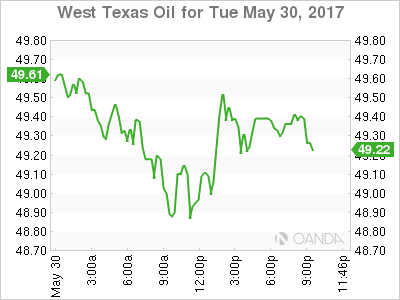

The price of West Texas remains under $50 after the news that Libyan production will return to 800,000 daily barrels after the disruption in the Sharara field has been sorted. The release of weekly inventories on Thursday at 11:00 am EDT will be a powerful driver of oil prices as there is a lot of scepticism in the market about the expected results from the OPEC cut agreement extension when the US shale industry is rapidly ramping production.

The Canadian stock market was mixed as Scotiabank beat earnings forecasts bringing solid results for Canadian banks after their surprise downgrade by Moody's. The ratings agency deemed that the housing market is facing a speculative bubble that threatens the banks. Energy stocks fell alongside the price of oil and in general the stock market was subdued as political risks rose in Europe and the United States.

The USD/CAD gained 0.043 percent in the last 24 hours. The currency pair is trading at 1.3454 after producer prices rose in Canada for the eight month in a row. Canadian fundamentals have been mixed and tomorrow's release of the Canadian monthly GDP will bring clarity on the direction of the loonie.

The US dollar got a boost from Fed Speaker Brainard as the known dove deemed a rate hike soon to be appropriate. Investors are pricing in the possibility of a rate hike in June as 88.8 percent using the CME Fedwatch tool methodology based on Fed funds futures prices. Consumer confidence was lower than expected earlier today but remains strong at 117.9. The paradigm between a strong consumer confidence but weak retail sales continues as Americans are opting to save. Employment data has been the strongest evidence of a recovery, but the headline numbers are not enough for the U.S. Federal Reserve that is now more focused on wage growth. The U.S. non farm payrolls (NFP) report will be published this Friday, June 2 at 8:30 am EDT, with a forecast of 186,000 new jobs added in May.

The price of oil lost 0.611 percent on Tuesday. The West Texas Intermediate is trading at $49.42 as concerns that the OPEC and other major producers agreement to extend the production cut might not be enough to curb the current glut in crude inventories. Energy prices fell in 2014 as Saudi Arabia pushed a market share grab strategy by ramping up production to drive prices and force US shale producers into default. The strategy backfired as low rates helped shale operations service their debts even at lower prices and the OPEC is now caught in a vicious circle where it is up to them to rebalance the market by removing the excess production.

Weekly US crude inventories are usually published on Wednesday's but due to the Memorial Day holiday it will be pushed back a day to Thursday at 11:00 am EDT.

Market events to watch this week:

Wednesday, May 31

8:30 am CAD GDP m/m

9:30 pm AUD Private Capital Expenditure q/q

9:30 pm AUD Retail Sales m/m

Thursday, Jun 1

4:30 am GBP Manufacturing PMI

8:15 am USD ADP Non-Farm Employment Change

8:30 am USD Unemployment Claims

10:00 am USD ISM Manufacturing PMI

11:00 am USD Crude Oil Inventories

Friday, Jun 2

4:30 am GBP Construction PMI

8:30 am CAD Trade Balance

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

Uncertain Fed & Uncertain UK Politics

The Fed's Brainard gave the strongest hint yet that low inflation won't dissuade a June hike but at the same time warned the Fed may pause afterwards. The New Zealand dollar led the way, while the Canadian dollar lagged. A UK election polls sent the pound plunging in early Asia-Pacific trade. The latest video for Premium subscribers is found below.

The April PCE report had something for everyone. The dollar initially rallied on the headlines because core PCE rose 0.2% m/m, slightly more than the +0.1% consensus. USD/JPY ticked 25 pips higher to 111.20 but that was the high for US trading.

Weighing on the dollar was a decline in year-over-year core inflation to 1.5% from 1.6%. It was expected but it extends the trend of slipping core inflation. Downward revisions to personal income also weighed but were balanced by rosy numbers on rising service sector salaries.

The change of a June hike rose to 88% from 84% according to the CME's Fedwatch measure but the dollar later declined. A big reason is because of eroding faith in longer term rate hikes.

Later in the day, the Fed's Brainard warned the FOMC may need to reassess its projected rate hikes. For the moment, she said it was premature to make that call and that's a signal that a June 14 rate rise is coming. But along with that hike, the statement is now more likely to include language that indicates more hikes will only come if inflation rises.

The bond market is now beginning to question whether those hikes will come at all. The 10-year yield fell 3.7 bps to 2.21% and is closing in on the post-election low of 2.16%. The US dollar is following yields lower.

Meanwhile, the pound took a sharp spill briefly below 1.28 in early Asia-Pacific trading. The trigger was a poll from YouGov that modeled the distribution of votes across ridings. It showed Theresa May's Conservatives winning but falling 16 seats short of a majority. That would seriously jeopardize Brexit negotiations and cripple the government.

From here, the focus will shift to China where the official PMIs are due at 0100 GMT. The manufacturing measure is forecast to slip to 51.0 from 51.2. the prior non-manufacturing reading was 54.0.

Note that it's also the final trading day of the month so flows could be a factor.

Consumer Confidence Declines Modestly in May

The Consumer Confidence Index fell slightly more than expected in May, with the overall index falling 1.5 points to 117.9. All of the decline was in the expectations component, which fell 2.8 points.

Consumers Remain Relatively Upbeat About Jobs and Income

The Consumer Confidence Index declined slightly more than expected, as the overall index fell 1.5 points to 117.9. Even with the drop, consumer confidence remains relatively solid. The overall index remains above the average for the six full months of data since the election, which had raised hopes that some growth-oriented fiscal stimulus would be enacted this year. That still may happen, but consumers have clearly scaled back their expectations. After hitting a post-recession high of 112.3 in March, the expectations series has fallen 9.7 points over the past two months.

The decline in expectations does not signal any increase in anxiety about the economy. The proportion of consumers expecting business conditions to increase, more jobs to be created and incomes to increase over the next six months spiked during the first three months of this year and has come back down from its cycle highs. All three series remain solidly positive, with more than twice as many consumers expecting business conditions to get better over the next six months than to get worse. At least twice as many consumers also expect their income to rise over the next six months than expect it to fall.

Employment prospects are likely the most important driver of consumer confidence today. The proportion expecting fewer jobs to be created over the next six months fell 1.8 points in May and is now at its lowest level since September 2000. The improvement is consistent with the continued slide in weekly unemployment claims and drop in the unemployment rate.

Improving employment conditions were responsible for the all of the increase in the present situation component, which rose 0.4 points to 140.7 in May. The proportion of consumers stating that jobs were hard to get tumbled 1.2 points in May to 18.2, while the proportion stating that jobs were plentiful fell 0.4 points to 29.9 percent. The labor market differential, which takes the difference between these two series, rose 0.8 points to 11.7.

Consumers took a slightly more cautious view of current business conditions, with the proportion stating present business conditions were good falling 1.4 points to 29.4 percent and the proportion stating present conditions were normal rising 1.4 points to 56.9. The proportion of consumers rating present conditions as bad in May was unchanged at 13.7. The employment components of the Conference Board survey are often looked to for any possible clues for the upcoming employment report. This May data were up on balance, but not decisively.

Buying plans for automobiles, homes and major appliances all declined. While these data are notoriously volatile, all three series hit their lowest levels this year. This bears watching but runs counter to recent reports citing improving consumer finances.

Solid Spending in April, Confirms Q2 Rebound is on Track

Personal income and spending both rose 0.4% in April, in line with the consensus forecasts.

Personal spending rose 0.2% in real terms, led by a 1.1% increase in durable goods. Services spending was largely flat in real terms, after a sizeable rebound in March (+0.6%).

Consumer prices rose 0.2% in April, bringing the year-on-year inflation rate to 1.7% (from 1.8% in March). Core prices (excluding food & energy) also rose 0.2% month-on-month - bringing year-on-year price growth to 1.5% (from 1.6% previously).

The personal saving rate was steady in April at 5.3%.

Key Implications

The second quarter rebound in consumer spending is right on track. Solid spending in April, combined with upward revisions to March data put spending on track to grow slightly above a 3% annualized pace. The good news is that personal spending gained momentum through the soft first quarter. The jump up in spending on durable goods is particularly encouraging that despite Q1 weakness, consumers remain confident to purchase big ticket items.

Another bright spot in the report was the continued gains in real income growth. After decelerating sharply at the end of 2016, real personal income grew at a 3.8% annualized pace over the past three months. That combined with solid job growth should underpin healthy consumer spending through the remainder of the year.

The weakness in core inflation in recent months may provide some fodder for the doves on the FOMC to delay further rate hikes until inflation pressures become clearer. Given the strength in the labor market, and the number of one-time factors that have put downward pressure on inflation recently, we think the Fed will be inclined to look past the recent softness and hike rates a quarter point in June.

Political Uncertainty Re-Emerges in Europe, Euro Volatility Spikes

Political uncertainty re-emerged in Europe shortly after the being improved on French presidential election. Now, it is Italy's turn with a snap election later this year becoming increasingly likely. With major parties converging to a deal on a new electoral law, an early election might take place in coming months, probably synchronizing that of German's in September. The euro reacted negatively and declined to the lowest level in more than a week before rebound. The 10-year Italian-German yield spread soared to almost the highest level in a month on concerns that the rapidly-rising Five Star Movement, the populist, euro-skeptic political party, could eventually become part of the coalition in Italy and destablize European Union again.

Three major parties support German inspired system

The latest development is that at least three (Partito Democratico, Five Star Movement, and Forza Italia) out of the 4 major parties have shown support to the German-inspired electoral system, using proportional representation with a 5% threshold. The system is bad for small parties. As such, small political parties including the conservative Brothers of Italy, the centrists led by Foreign Minister Angelino Alfano, and the Progressive and Democratic Movement (MDP), which split off from the PD earlier this year, have opposed the reform. Yet, one advantage of the new system is that it reduces fragmentation in the parliament.

Opinion polls have suggested that it would be a neck and neck race between the anti-EU, populist Five Star Movement, led by Beppe Grillo Gianroberto Casaleggio, and the social- democratic Partito Democratico, lead by former PM Matteo Renzi. The market is concerned that the sentiment of anti-globalization and protectionism in EU would grow big again if Five Star Movement manages to become the largest party in Italy.

UK General Election on June 8

In a separate note, the UK general election would be held on June 8. The latest opinion poll suggested that Labors are narrowing the gap with Tories, increasing the uncertainty of the election outcome. Recall that PM Theresa May called for the election in order to cement her mandate in the Brexit negotiation with the EU. Her confidence was anchored by the strong support for Tories at the time with some polls showing that Tories at almost double the vote share of the Labour Party. However, the lead has dropped from almost 20 to below 10 recently. While a Tories' majority is still expected, the failure to get a landslide victory would likely increase the hurdle for the UK's Brexit negotiation with the EU, due to conflicting opinions at home.

Technical Outlook: EURUSD Recovery from Session Low

Recovery from session low at 1.1109 spiked to the levels near 1.1200 after news that ECB may upgrade risk assessment and possibly talk about ramping up extra stimulus on June 8 meeting, hit the wires. Positive outlook for economic growth that is already biased higher, what ECB chief Draghi has already mentioned in his recent speeches may shift ECB's policymaker's view of persisting downside risk and signal possible change in policy stance. The Euro's rally is now showing signs of running out of steam, as the pair eased quickly from fresh session high at 1.1193 and returned near the mid-point of today's 1.1109/1.1193 recovery rally. Initial probe above the upper pivot at 1.1181 (10SMA) was so far short-lived and capped by hourly cloud (spanned between 1.1184 and 1.1205), with close above 10SMA needed to generate stronger bullish signal and shift near-term focus higher. However, near-term structure is expected to stay biased higher while the price remains above 1.1145 (hourly 20SMA/near Fibo 61.8% of 1.1109/1.1193 upleg). Otherwise, increased risk of return to 1.1100 pivot and possible break lower would come in play on loss of 1.1145 support.

Res: 1.1181; 1.1193; 1.1207; 1.1234

Sup: 1.1145; 1.1130; 1.1100; 1.1060

Euro Erases Early Losses. Dollar Fails to Convince

- Main European equity indices trade between flat and -0.5%, recovering part/all opening losses. US stock markets open nearly unchanged after the long weekend.

- Most US eco data printed in line with expectations. Personal income and spending both rose by 0.4% M/M in April. The PCE deflator slowed from 1.9% Y/Y to 1.7% Y/Y and the core PCE from 1.6% Y/Y to 1.5% Y/Y. The S&P/Case-Shiller 20-city home price index climbed 5.89% in March, the fastest rate since 2014. Consumer confidence disappointed, declining from 119.4 to 117.9, but remaining near historically high levels.

- ECB policymakers are set to take a more benign view of the economy and will even discuss dropping some of their pledges to ramp up stimulus if needed, sources told Reuters. ECB Hansson said that the outlook for the economy has improved so the question now is how quickly central bank support can be reduced without jeopardizing growth.

- EMU economic confidence dropped back from its post-financial crisis high in May, as a fall in services and retail trade confidence translated into softer sentiment figures. German inflation slowed in May, dropping to 1.4% Y/Y from 2% Y/Y in April while economists predicted a reading of 1.5% Y/Y.

- Donald Trump has repeated his criticism of Germany's trade surplus with the US and under-spending on defence, ramping up tensions with Berlin after Angela Merkel made watershed comments about the fragile state of the western alliance over the weekend.

- Dallas Fed Kaplan believes that there will be two more rate hikes this year, which could occur as the central bank reduces its balance sheet. However, Kaplan is not basing his forecast on the idea that the economy is about to take off.

- A Greek government spokesman denied a German newspaper report on Tuesday that it was considering opting out of a loan repayment in July if lenders could not agree on debt relief. "It is not true," government spokesman Tzanakopoulos told Reuters. "There will be a solution on June 15."

Rates

Bonds shrug off eco data

Global core bonds had an uneventful trading session, shrugging off a batch of eco data. EMU eco data printed on the softer side of consensus, including a larger setback of German inflation (2% Y/Y to 1.4% Y/Y). They strengthen ECB president Draghi's case of a very gentle normalisation process. Sources told Reuters that the ECB would start changing its forward guidance, by dropping its easing bias. US eco data (including a small decline of PCE inflation) were in line with expectations and triggered a very small, temporary, uptick in the US Note future. Most investors kept sidelined though with more US eco figures scheduled later this week (ADP, manufacturing ISM, payrolls). European stock markets flat-lined or even recovered some of the opening losses while oil prices continued their way south. None of these markets left a trace on the Bund or the Note future though.

At the time of writing, changes on the German yield curve range between -0.3 bps (10-yr) and +0.9 bps (2-yr). The US yield curve bull flattens with yields 0.4 bps (2-yr) to 2.3 bps (30-yr) lower. On intra-EMU bond markets, 10-yr yield spread changes versus Germany range between -2 bps and +1 bp with Greece underperforming (+5 bps).

The Italian debt agency kicked off this week's EMU bond supply by tapping the on the run 5-yr BTP (€3B 1.2% Apr2022) and 10-yr BTP (€2.75B 2.2% Jun2027). The combined amount sold was the maximum of the targeted €4.75-5.75B. The auction bid cover was 1.43, which is average for Italian standards. Additionally, Italy raised €1.75B via the floating rate CCTeu (Oct2024).

Currencies

Euro erases early losses. Dollar fails to convince

Different themes guided trading in the major FX cross rate today. Early this morning, euro weakness prevailed as markets pondered whether EMU political risk would again become an issue for trading. However, the euro found its composure even as EMU data were slightly softer than expected. The US data brought no surprise . EUR/USD and USD/JPY showed some intraday swings, but in the end, trading showed no clear trend.

Overnight, Asian markets started with a cautious risk-off bias, but the losses were limited and largely erased as the session proceeded. The yen was well bid. Decent Japanese eco data and a cautious risk sentiment (headlines on political uncertainty in Europe) both supported the Japanese currency. USD/JPY dropped below 111 and tested a first minor support in the 111.80/90 area. EUR/USD was sold early in Asia and settled in the 1.1120/40 area.

The headlines on political uncertainty in Greece and Italy also weighed on the euro and European equities at the start in Europe. EUR/USD touched an intraday low in the 1.1110 area. A spokesman of the Greek government denied that Greece considered defaulting. The euro started a gradual intraday rebound. The EMU eco data (EC economic sentiment and German inflation) were slightly softer than expected. Germany inflation printed at a low 1.4% Y/Y. However, the reports had no big (negative) impact on euro trading.

At the onset of the US session, the euro rally even accelerated as the inevitable 'sources' said that the ECB will discuss the removal of its easing bias at next week's meeting. EUR/USD spiked temporary to the high 1.11 area. Early in afternoon trading, US president Trump in a tweet repeated that the big trade deficit with Germany and the low contribution of Germany to Nato were bad for the US. Tthe bickering between the US and Germany leaves no big traces on global markets and on FX trading in particular for now. However, the issue deserves close monitoring. The US income and spending data (including the deflators) were perfectly in line with expectations. If anything the dollar temporary gained a few ticks as another negative US data surprise was avoided. Especially USD/JPY profited, trying to regain the 111 big figure. EUR/USD is changing hands around 1.1170/75 area. Despite a poor start for the euro this morning, the dollar also still fails to stage a convincing comeback.

Sterling selling slows, but picture remains fragile.

Since mid-last week, sterling came under pressure as polls showed that PM May's conservative party lost a big part of its lead over labour. Sterling selling eased (temporary) this morning as there was no indication that the lead is eroding further after a television debate of May and Corbyn yesterday evening. EUR/GBP dropped to the 0.8655 area. Cable touched an intraday top in the 1.2885/90 area. However, sterling momentum dwindled again during the US trading session. EUR/GBP trades in the high 0.86 area. Cable is changing hands in the 1.2850 area as sterling softens and dollar caution keep each other in balance.

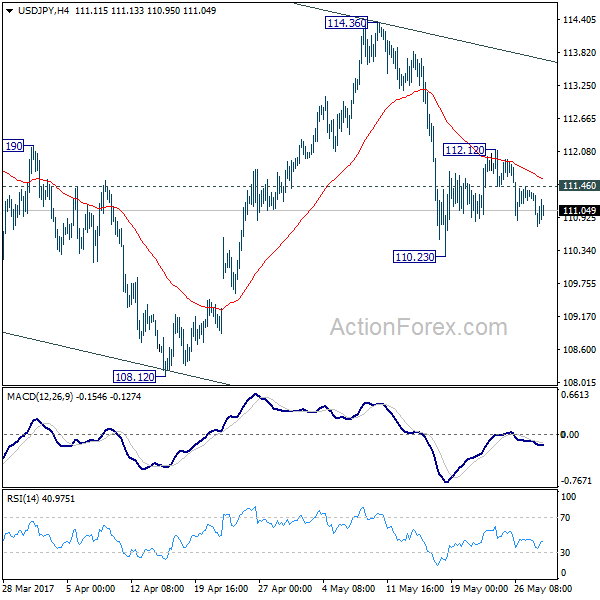

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.10; (P) 111.28; (R1) 111.44; More...

Intraday bias in USD/JPY remains mildly on the downside for 110.23. Break will resume the fall from 114.36 to 108.12 and below. . Note again that decline from 118.65 is seen as a correction. In that bearish case, we'll look for bottoming signal again at 61.8% retracement of 98.97 to 118.65 at 106.48. On the upside, above 111.46 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9743; (P) 0.9759; (R1) 0.9786; More.....

Intraday bias in USD/CHF remains neutral as consolidation from 0.9691 continues. We'd continue to expect upside to be limited by 0.9858 support turned resistance and bring fall resumption. Whole decline from 1.0342 is still in progress and below 0.9691 will target 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. We'll start to look for reversal signal below there.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.

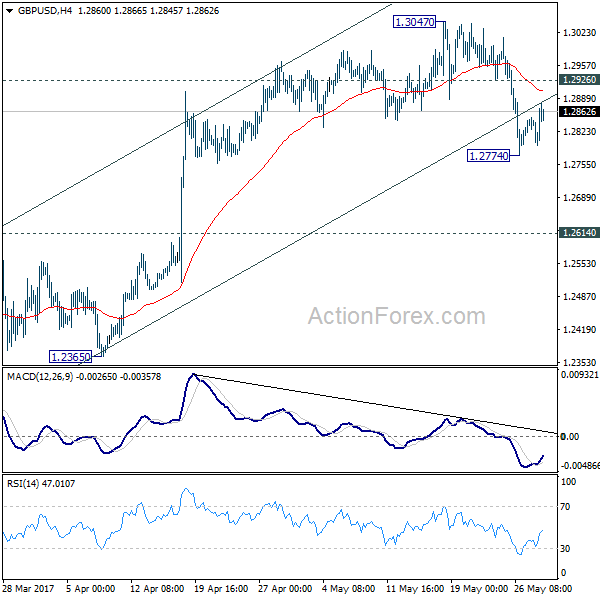

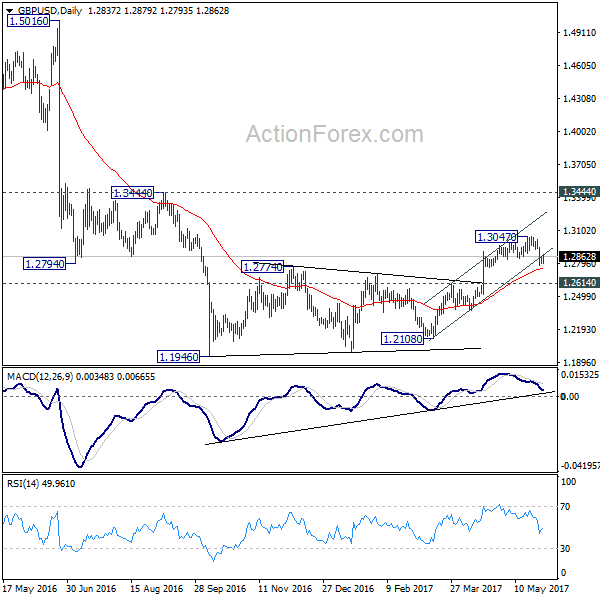

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2804; (P) 1.2827; (R1) 1.2859; More...

Intraday bias in GBP/USD remains neural for consolidation above 1.2774 temporary low. We're holing on to view that rise from 1.2108 is completed. Hence, upside of current recovery should be limited by 1.2926 minor resistance and bring another decline. Below 1.2774 will target 1.2614 resistance turned support next. Break there should also indicate completion of whole consolidation pattern from 1.1946 and target a retest on this low. Meanwhile, above 1.2926 minor resistance will turn focus back to 1.3047 high instead.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.