Sample Category Title

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

We typically search for lower-timeframe confirmation between the M15 and H1 timeframes, since most of our higher-timeframe areas begin with the H4. Stops are usually placed 1-3 pips beyond confirming structures.

EUR/USD

Leaving the 1.11 handle unchallenged, the shared currency shifted northbound yesterday. The H4 mid-level resistance at 1.1150 was easily cleared, allowing price to shake hands with the 1.12 barrier going into the early hours of the US segment, which for now is holding as resistance. What's also notable from a technical perspective is the potential H4 bullish pennant (1.1075/1.1268) that's forming on top of a daily support at 1.1142. What's concerning though is that this H4 bullish formation is also actually taking shape beneath a formidable weekly supply area coming in at 1.1533-1.1278!

Our suggestions: Basically, we're looking for price to continue compressing within the current H4 pennant and then break out to the upside. Should this occur, as per the black arrows, we'd be looking to trade long from from 1.1150, and target 1.12 as an initial take-profit zone. We plan on holding the remainder of the position for a potential run up to 1.1253 (underside of daily supply) and then the underside of weekly supply at 1.1278.

Data points to consider: German Retail sales at 7am, EUR CPI figures at 10am. FOMC member Kaplan speaks at 1pm, US pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Watching for price to compress within the current H4 pennant and break out north for a possible retest of 1.1150.

- Sells: Flat (stop loss: N/A).

GBP/USD

After failing to sustain gains beyond the H4 mid-level resistance at 1.2850 yesterday, the pair, in recent hours, brought the unit back down to the 1.28 handle. With this psychological barrier likely worn out, we still have our eye on the H4 Quasimodo support level seen plotted below at 1.2769.

The stops taken from 1.28 would likely provide enough liquidity for the big boys to begin buying this market at 1.2769. What's more, let's remember that we are also trading from a weekly support at 1.2789! Therefore, there is a good chance price will bounce from 1.2769 and at least reach 1.28.

Our suggestions: Based on the above points, our desk believes the aforementioned H4 Quasimodo support level is stable enough to consider a buy trade from, with a stop-loss order placed below the pattern's apex at 1.2748. However, be sure to reduce risk to breakeven once price tests 1.28 as we do expect the bears to put up a fight here.

Data points to consider: FOMC member Kaplan speaks at 1pm, US pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: 1.2769 region ([possible market order] stop loss: 1.2748).

- Sells: Flat (stop loss: N/A).

AUD/USD

Trade update: stopped for breakeven at 0.7440).

The Aussie closed in positive territory yesterday, as the US dollar drove lower. This consequently formed a nice-looking daily engulfing candle that smothered both Friday and Monday's action. Over on the H4 timeframe, we saw the demand marked with a green arrow around 0.7420 hold price and send the pair back above the H4 mid-level resistance coming in at 0.7450. To the upside, we now see May's opening level lurking nearby at 0.7481, followed closely by the 0.75 handle.

Despite daily price printing a bullish engulfing candle, which to some is considered a buy signal, it might be worth taking note that weekly price remains trading from a resistance area planted at 0.7524-0.7446. So, with that in mind, where do we go from here?

Our suggestions: Personally, we are going to sidestep any long setups we come across today. Buying when we know weekly price is trading from supply is just too risky for our liking. Also, as much as we love monthly opening levels, we will not be trading short from May's level. Instead, we have our eye on the 0.7512/0.75 area, which comprises of a H4 resistance at 0.7512, a H4 trendline resistance etched from the high 0.7610 and the round number 0.75 (shaded in red). While this sell zone is planted nicely within the limits of the current weekly supply, there's still a chance that daily price could force the H4 candles to fake north to touch base with the underside of daily supply at 0.7523. Therefore, waiting for a reasonably sized H4 bearish candle to form, preferably a full-bodied candle, before pulling the trigger is advised.

Data points to consider: Chinese manufacturing data at 2am. FOMC member Kaplan speaks at 1pm, US pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 0.7512/0.75 ([waiting for a reasonably sized H4 bear candle to form – preferably a full-bodied candle – is advised] stop loss: ideally beyond the candle's wick).

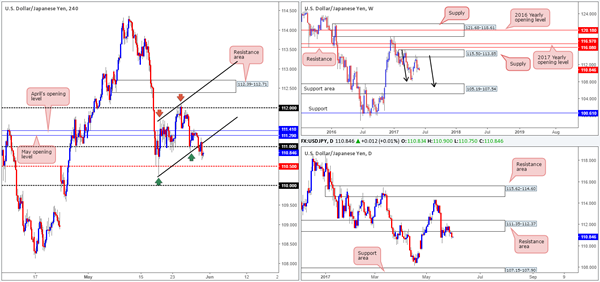

USD/JPY

Alongside US equities, the USD/JPY punched lower yesterday. The move, as you can see, punctured the H4 channel support taken from the low 110.23 (ties in nicely with the 111 handle), and clocked a low of 110.66. With this in view, our desk is watching for H4 price to retest the 111 boundary as resistance for a possible short. Why here, and where would we target?

Why we're looking for shorts is simply because weekly bears remain in a relatively strong position after pushing aggressively lower from supply registered at 115.50-113.85. We know there's a lot of ground to cover here, but this move could possibly result in further downside taking shape in the form of a weekly AB=CD correction (see black arrows) that terminates within a weekly support area marked at 105.19-107.54 (stretches all the way back to early 2014). Furthermore, daily price continues to defend the resistance area penciled in at 111.35-112.37. The next area on the hit list from here falls in at 107.15-107.90: a support zone that's glued to the top edge of the said weekly support area.

In regards to possible take-profit targets, the initial level of interest stands at 110.50. But, as we already know from the higher-timeframe structures, H4 price could very well drive much lower than this!

Our suggestions: Following a retest of 111, we'd also like to see bearish intent in the form a lower-timeframe confirming sell signal (see the top of this report).

Data points to consider: FOMC member Kaplan speaks at 1pm, US pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 111 region ([waiting for a lower-timeframe signal to form following the retest is advised] stop loss: dependent on where one confirms this level).

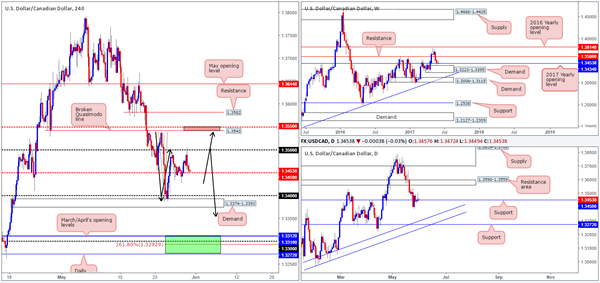

USD/CAD

Kicking this report off with a look at the weekly chart, we can see that price remains trading around the 2017 yearly opening level at 1.3434. Directly below sits a demand base coming in at 1.3223-1.3395, which was tested during last week's session. Down on the daily chart, the unit continues to linger around support seen at 1.3450. To the upside, we have a resistance area planted at 1.3598-1.3559, and below there's a support line at 1.3272 which happens to intersect with two trendline supports (1.2968/1.3027).

Bouncing over to the H4 chart, we see the following:

To the upside, there's a potential H4 AB=CD bearish pattern (taken from the low 1.3387) taking shape that terminates just ahead of a H4 broken Quasimodo line drawn from 1.3542/H4 mid-level resistance at 1.3550 and a daily resistance area at 1.3598-1.3559. The small (red) area marks a possible zone where price could bounce.

To the downside, we also see a potential H4 AB=CD 161.8% Fib ext. at 1.3292 taken from the high 1.3540. This number helps form a strong-looking (green) buy zone. 1.3272/1.3312: holds the following structures:

Daily support at 1.3272.

1.33 handle.

March/April's opening levels at 1.3310/1.3312.

Daily trendline support confluence (1.2968/1.3027).

Also of note is the H4 buy zone is seen lodged within the lower limits of the weekly demand at 1.3223-1.3395!

Our suggestions: As you can see, both zones hold a reasonable amount of confluence and have the potential to reverse price. To be on the safe side, however, we would recommend not entering blindly at these areas. Wait for additional confirmation in the form a reasonably sized H4 rotation candle, preferably a full-bodied candle, before committing to a trade.

Data points to consider: FOMC member Kaplan speaks at 1pm, US pending home sales at 3pm. Canadian growth data at 1.30pm GMT+1.

Levels to watch/live orders:

- Buys: 1.3272/1.3312 ([waiting for a reasonably sized H4 bull candle to form – preferably a full-bodied candle – is advised] stop loss: ideally beyond the candle's tail).

- Sells: 1.3550/1.3542 ([waiting for a reasonably sized H4 bear candle to form – preferably a full-bodied candle – is advised] stop loss: ideally beyond the candle's wick).

USD/CHF

As can be seen from the H4 candles this morning, the 0.98 handle elbowed its way into the spotlight yesterday and held steady as a resistance. With price fading from this number, we saw the unit enter back within the limits of a H4 range fixed between 0.9774/0.97. This consolidation is interesting due to it forming just ahead of a daily Quasimodo support level at 0.9678. What's also notable is the fact that this daily barrier is positioned just ahead of a weekly Quasimodo support pegged at 0.9639.

Over on the bigger picture, we see very little structure stopping daily price from reaching the said Quasimodo level. With that in mind, we feel that the Swissy will eventually punch below the current H4 range and challenge this daily base line.

Our suggestions: A fakeout through 0.97 that connects with the aforementioned daily Quasimodo support is a valid long, in our opinion. The reason being is there are likely a truckload of sell stops lingering just below 0.97. These stops, when filled, become sell orders, and thus give the big boys liquidity to buy into from the daily Quasimodo! So, with that in mind, should price whipsaw through 0.97, test 0.9678, and close back above 0.97, we will look to enter long, targeting the top edge of the H4 range at 0.9774.

Data points to consider: FOMC member Kaplan speaks at 1pm, US pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: 0.97 region ([wait for price to fakeout beyond the 0.97 handle – touch 0.9678 – and then close back above 0.97, before looking to commit to a position] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

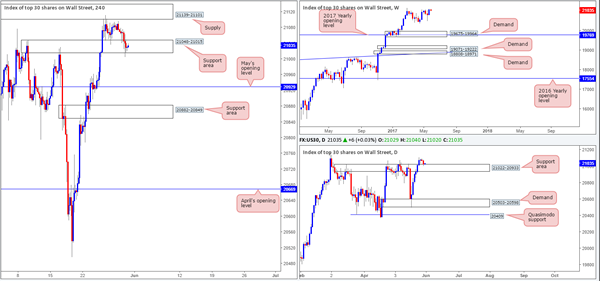

DOW 30

US equities took a hit yesterday and even marginally breached the lower edge of a H4 support area coming in at 21048-21015. This recent down move has also brought the unit down to the top edge of a daily support area drawn from 21022-20933, which should, technically speaking, hold price higher.

Despite yesterday's bearish move, our team remains biased to the upside since we are trading around record highs at the moment. However, entering long from the current H4 support zone is not something our team would feel comfortable with knowing that there's a nearby H4 supply lurking just above at 21139-21101.

Our suggestions: Waiting for the H4 supply mentioned above at 21139-21101 to be taken out is likely the safer route, before considering hunting for longs. Therefore, until we see a decisive close above this area, our desk will remain patiently waiting on the sidelines.

Data points to consider: FOMC member Kaplan speaks at 1pm, US pending home sales at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Watching for H4 price to close above H4 supply at 21139-21101 before looking to long this market.

- Sells: Flat (stop loss: N/A).

GOLD

In recent sessions, the price of gold retreated and clocked a fresh low of 1259.2. The move began after H4 price chalked in a bearish selling wick that pierced 1270.5/1268.6 (May's opening level and a H4 AB=CD 127.2% Fib ext. [taken from the low 1245.9]). As we write, the yellow metal looks poised to extend these losses and shake hands with demand registered at 1252.9-1256.5.

Over on the bigger picture, daily supply at 1271.0-1261.7 remains in a firm position, and could very well be the catalyst that forces H4 price down to the said demand. Up on the weekly chart, however, bullion is seen lurking between demand marked at 1194.8-1229.1 and two weekly Fibonacci extensions 161.8/127.2% at 1313.7/1285.2 taken from the low 1188.1 (green zone).

Our suggestions: Entering long from the current H4 demand is tempting, since weekly price shows little stopping further upside taking shape. However, you would have to contend with the possibility of going up against daily sellers from the aforementioned supply! And, in addition to this, there's also a chance that H4 price may look to ignore the demand altogether and head down to March/April's opening levels at 1245.9/1248.0.

We're not against buying from the H4 demand, but we are wary. With that being the case, we will assess how H4 price behaves once/if gold challenges this zone. Should a H4 bull candle present itself, preferably in the form of a full-bodied candle, we would, dependent on the time of day, consider a long from here, targeting the 1268.0 neighborhood.

Levels to watch/live orders:

- Buys: 1252.9-1256.5 ([waiting for a reasonably sized H4 bull candle to form – preferably a full-bodied candle – is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

Daily Technical Analysis: GBP/USD Wave-4 Pullback To 61.8% Fib Ahead Of UK Elections

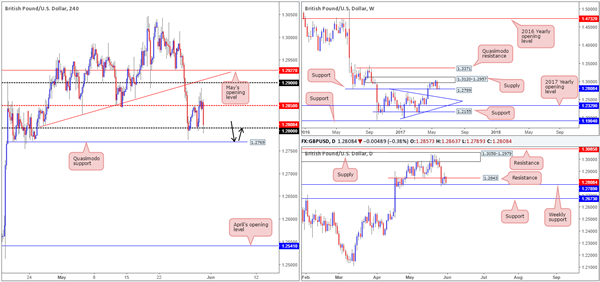

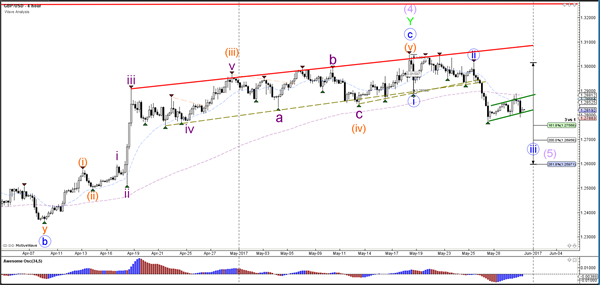

Currency pair GBP/USD

The British Pound weakened last week ahead of the UK elections which will take place on Thursday 8 June 2017. Some opinion polls are showing a shrinking lead for the current Prime Minister Theresa May of the Conservative party and a rebound for the Labour opposition party but a full week of campaigning still remains in front of the UK.

The GBP/USD channel (green lines) is a bear flag chart pattern and a potential bearish break could see price continue with wave 3 (blue). A bullish break above the channel, however, could change the wave structure.

The GBP/USD completed an ABC (grey) correction at the 50-61.8% Fibonacci zone of wave 4 (orange).

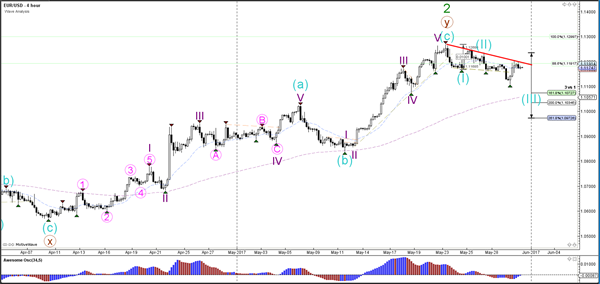

Currency pair EUR/USD

The EUR/USD made a deep retracement back to the resistance trend line (red), which is a key bounce or break spot. A bearish bounce could confirm the current wave structure whereas a bullish break invalidates it.

The EUR/USD stopped at the 78.6% Fibonacci resistance level and has reached a major bounce or break spot.

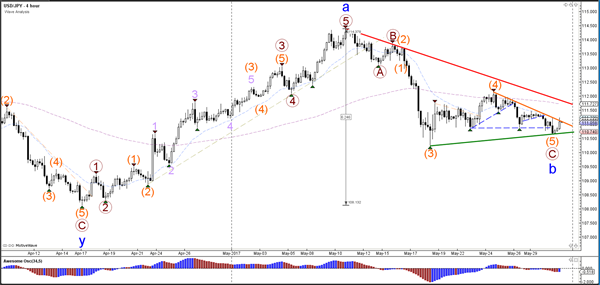

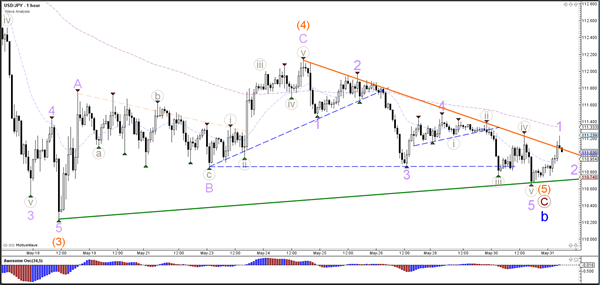

Currency pair USD/JPY

The USD/JPY could have completed a truncated 5th wave (orange), which means that wave 5 does not break the bottom (or top) of wave 3 (orange).

The USD/JPY seems to have completed 5 internal waves twice (grey/purple) within wave 5 (orange). A bullish break above resistance (orange) could confirm the current wave structure whereas a break below support (green) invalidates it.

European Open Briefing: The Euro Recovered Slightly

Global Markets:

- Asian stock markets: Nikkei down 0.15 %, Shanghai Composite and ASX 200 gained 0.15 %, Hang Seng rose 0.10 %

- Commodities: Gold at $1260 (-0.20 %), Silver at $17.26 (-0.95 %), WTI Oil at $49.35 (-0.60 %), Brent Oil at $51.95 (-0.55 %)

- Rates: US 10 year yield at 2.22, UK 10 year yield at 0.99, German 10 year yield at 0.29

News & Data

- China Manufacturing PMI 51.2 vs 51.0 expected

- China Non-Manufacturing PMI 54.5 vs 54.0 previous

- Japan Industrial Production 4.0 % vs 4.3 % expected

- South Korea Retail Sales m/m 0.7 % vs -0.1 % previous

- South Korea Industrial Production m/m -2.2 % vs 0.8 expected

- South Korea Industrial Production y/y 1.7 % vs 5.0 % expected

- New Zealand ANZ Business Confidence 14.9 vs 11.0 previous

- Australia Private Sector Credit m/m 0.4 % vs 0.4 % expected

- Asia stocks rise as China factories see steady growth, sterling soft – RTRS

- China factory PMI growth holds up in May, steel sector activity speeds up – RTRS

- Oil falls as rising Libyan, U.S. output undermines cuts – RTRS

Markets Update:

The British Pound came under further pressure after polls showed that UK Prime Minister May's lead is decreasing. GBP/USD was clearly rejected at 1.2880 resistance, and while 1.2775 support held, further losses seem likely in the near-term. The uncertainty around the UK election surprised the markets a bit, which were expecting that May's lead will continue to hold.

The Euro recovered slightly, but is struggling to gain momentum. Resistance is seen at 1.12 and 1.1230, while key support lies at 1.11. A break sub-1.11 would suggest losses could extend to 1.10 soon.

Traders are now looking forward to the Euro Zone inflation figures, which will be released this morning at 10:00 BST. There have speculations that the ECB might signal a shift in their monetary policy soon amid improving economic conditions. A higher than expected inflation print could further fuel that and boost the Euro.

USD/JPY bounced amid broad USD strength and a solid performance of global equity markets. However, the pair will need a clear break above 112 to gather some momentum.

Upcoming Events:

- 07:00 BST – German Retail Sales

- 07:45 BST – French CPI

- 08:55 BST – German Unemployment Rate

- 10:00 BST – Euro Zone CPI

- 10:00 BST – Euro Zone Unemployment Rate

- 13:30 BST – Canadian GDP

- 14:45 BST – US Chicago PMI

- 15:00 BST – US Pending Home Sales

Australia’s Private Sector Credit Climbed In April

For the 24 hours to 23:00 GMT, the AUD rose 0.27% against the USD and closed at 0.7458.

LME Copper prices declined 1.1% or $63.0/MT to $5608.0/MT. Aluminium prices declined 0.3% or $6.5/MT to $1943.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7449, with the AUD trading 0.12% lower against the USD from yesterday's close.

Early morning data indicated that Australia's private sector credit climbed 0.4% on a monthly basis in April, at par with market expectations. The private sector credit had registered a revised similar rise in the prior month.

Elsewhere, in China, Australia's largest trading partner, the NBS manufacturing PMI remained unchanged at a level of 51.2 in May, compared to market expectations for a drop to a level of 51.0. Moreover, the nation's NBS non-manufacturing PMI advanced to a level of 54.5 in May, after recording a level of 54.0 in the previous month.

The pair is expected to find support at 0.7420, and a fall through could take it to the next support level of 0.7391. The pair is expected to find its first resistance at 0.7477, and a rise through could take it to the next resistance level of 0.7505.

Going ahead, traders would keep a close watch on Australia's retail sales data for April, set to be released tomorrow.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

German Annual Inflation Slowed More-Than-Expected In May

For the 24 hours to 23:00 GMT, the EUR rose 0.33% against the USD and closed at 1.1173.

On the data front, Germany's preliminary consumer price index (CPI) climbed less-than-expected by 1.5% on an annual basis in May, rising at its slowest pace in six months, thus supporting the European Central Bank's (ECB) notion that underlying inflation in the common currency region still lacks sustainable uptrend. Meanwhile, markets expected the CPI to advance 1.6%, following a gain of 2.0% in the previous month.

Separately, the Euro-zone's final consumer confidence index rose to a level of -3.3 in May, meeting flash estimates and compared to a revised reading of -3.6 in the previous month.

Macroeconomic data indicated that personal spending in the US grew at its quickest pace in four months, after it rose 0.4% on a monthly basis in April, meeting market expectations, thus underscoring expectations that the world's largest economy is poised to rebound after a lacklustre growth in the first quarter. In the prior month, personal spending had registered a revised rise of 0.3%. Further, the nation's personal income recorded a rise of 0.4% MoM in April, in line with market expectations. Personal income had registered a rise of 0.2% in the previous month.

In other economic news, the US CB consumer confidence index unexpectedly fell to a three-month low level of 117.9 in May, defying investor consensus for an advance to a level of 119.5. In the prior month, the index had recorded a revised reading of 119.4. Also, the nation's Dallas Fed manufacturing business index surprisingly rose to a level of 17.2 in May, compared to a level of 16.8 in the previous month, while markets anticipated the index to ease to a level of 15.0.

Meanwhile, the Federal Reserve (Fed) Governor, Lael Brainard, stated that an interest rate hike is likely coming soon, but warned that if the recent slowdown persists, it could cause the Fed officials to reassess the path of monetary policy trajectory.

In the Asian session, at GMT0300, the pair is trading at 1.1175, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.1122, and a fall through could take it to the next support level of 1.1068. The pair is expected to find its first resistance at 1.1217, and a rise through could take it to the next resistance level of 1.1258.

Looking ahead, market participants will focus on the Euro-zone's unemployment rate and inflation data, both for May along with Germany's jobs report for May and retail sales data for April, slated to release in a few hours. Additionally, the US Fed Beige Book report and pending home sales data for April, will keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

UK’s GfK Consumer Confidence Edged Up To A 4-Month High Level In May

For the 24 hours to 23:00 GMT, the GBP declined 0.1% against the USD and closed at 1.2807.

In the Asian session, at GMT0300, the pair is trading at 1.2829, with the GBP trading 0.17% higher against the USD from yesterday's close.

Overnight data revealed that UK's GfK consumer confidence index unexpectedly improved to a level of -5.0 in May, notching its highest level in four months and confounding market expectations for a drop to a level of -8.0. In the previous month, the index had registered a reading of -7.0.

The pair is expected to find support at 1.2785, and a fall through could take it to the next support level of 1.274. The pair is expected to find its first resistance at 1.2881, and a rise through could take it to the next resistance level of 1.2932.

Ahead in the day, traders would keep a close watch on UK's net consumer credit and mortgage approvals data, both for April.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japanese Industrial Output Posted Its Biggest Jump In Nearly 6 Years In April

For the 24 hours to 23:00 GMT, the USD declined 0.38% against the JPY and closed at 110.84.

In the Asian session, at GMT0300, the pair is trading at 111.17, with the USD trading 0.3% higher against the JPY from yesterday's close.

Overnight data indicated that Japan's preliminary industrial production rebounded 4.0% on a monthly basis in April, surging to its highest level since June 2011. Markets were expecting industrial production to climb 4.2%, after recording a fall of 1.9% in the prior month.

The pair is expected to find support at 110.81, and a fall through could take it to the next support level of 110.46. The pair is expected to find its first resistance at 111.38, and a rise through could take it to the next resistance level of 111.60.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Switzerland’s KOF Leading Indicator Dropped In May

For the 24 hours to 23:00 GMT, the USD declined 0.31% against the CHF and closed at 0.9758.

On the macro front, Switzerland's KOF leading indicator fell more-than-anticipated to a level of 101.6 in May, compared to market expectations for a fall to a level of 105.8. In the prior month, the leading indicator had recorded a revised reading of 106.3.

In the Asian session, at GMT0300, the pair is trading at 0.9756, with the USD trading marginally lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9726, and a fall through could take it to the next support level of 0.9696. The pair is expected to find its first resistance at 0.9797, and a rise through could take it to the next resistance level of 0.9838.

Looking ahead, market participants await the release of Switzerland's UBS consumption indicator for April, slated in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Loonie Trading Higher, Ahead Of Canada’s GDP Growth Data

For the 24 hours to 23:00 GMT, the USD slightly declined against the CAD and closed at 1.3469.

On the macro front, Canada's current account deficit widened more-than-expected to a level of C$14.1 billion in 1Q 2017, from a revised deficit of C$11.8 billion in the previous quarter. Markets were anticipating the country's deficit to rise to a level of C$12.0 billion.

In the Asian session, at GMT0300, the pair is trading at 1.3461, with the USD trading 0.06% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.3439, and a fall through could take it to the next support level of 1.3416. The pair is expected to find its first resistance at 1.3495, and a rise through could take it to the next resistance level of 1.3528.

This afternoon will bring a crucial Canadian release, namely gross domestic product (GDP) for March and first quarter.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

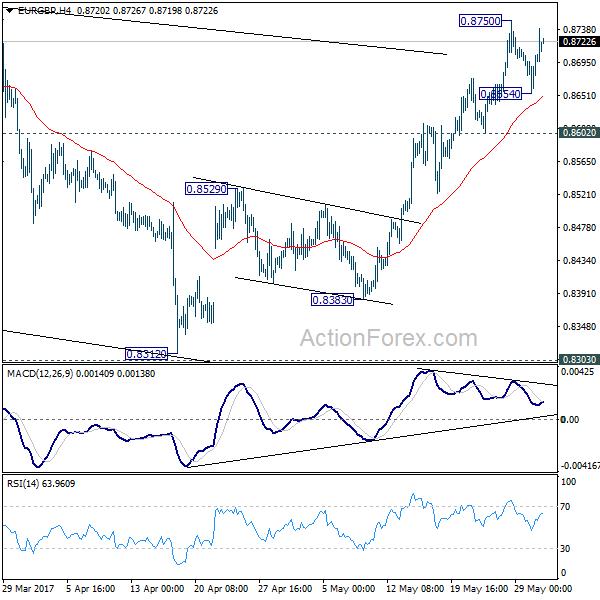

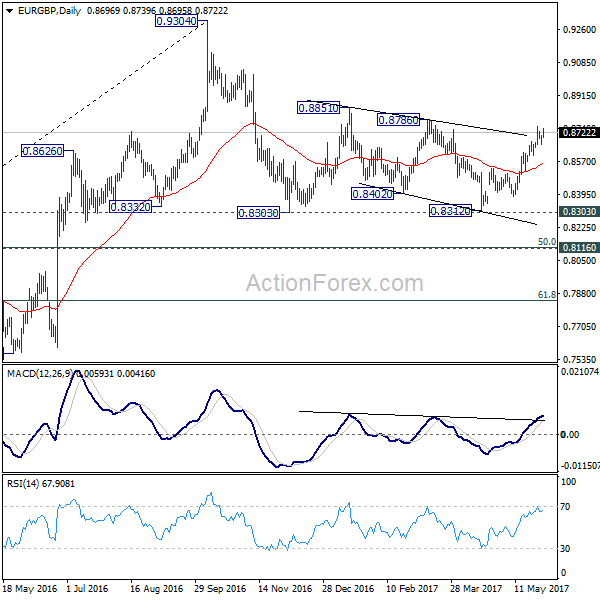

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8667; (P) 0.8686; (R1) 0.8717; More...

EUR/GBP recovers after dipping to 0.8654 but it's staying below 0.8750. Intraday bias remains neutral first and some more consolidations could be seen. But near term outlook will remain mildly bullish as long as 0.8602 support holds and further rally is expected. Above 0.8750 will target 0.8786 resistance first. Break of 0.8786 would pave the wave for retesting 0.9304 high. Break of 0.8602, however, will argue that the rebound from 0.9312 has completed and turn bias back to the downside for 0.8529 first.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. The leg from 0.9304 should have completed after taking 0.8332 structural support. But it's too early to say that larger rise from 0.6935 is resuming. Rejection from 0.9304 will extend the consolidation with another falling leg. Meanwhile, firm break of 0.9304 will target 0.9799 (2008 high). In case of another decline, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound.