Sample Category Title

EUR/USD Inches Lower Amid Draghi’s Speech

USD higher amid dovish Draghi, focus on this week US data to gauge Fed's next move

The US dollar rose across the board on Tuesday after a day off for US and UK investors. The Japanese yen was the only G10 currency that was able to keep its head above the water, thanks to solid April's retail sales data (3.2%y/y versus 2.3% median forecast). The single currency accelerated its debasement amid dovish comment from Mario Draghi before the European Parliament. Yesterday, the president of the ECB made clear that the institution wasn't ready to unwind its fiscal stimulus amid rising uncertainties on the inflationary outlook. Investors rushed into German bunds and sent yields to multi-week lows dragging the euro lower. The German 5-year yields slid to -0.44%, while the 2-year one fell to -0.72%.

After rallying strongly during the second half of May, EUR/USD came under pressure recently as investors have already discounted monetary tightening in the EU, while slowly pricing in the upcoming rate hike by the Federal Reserve. We anticipate further downside, with the 1.10 (psychological threshold and Fibonacci 38.2% on April-May rally) level as first target.

However, our bullish outlook for the USD remains highly depend on the upcoming US data as the Fed needs a solid ground to lift borrowing costs consistently. The Fed's favourite measure of inflation, the core personal expenditure, is due for release today and is expected to have eased to 1.5%y/y in April, down from 1.6% in March. Investors will also monitor closely developments in wage growth – will be released on Friday – as it could give a boost to inflation measures. On the other, the unemployment rate and NFP will most likely remain in the background as the recent impressive numbers fail to translate into higher salaries for US people.

Draghi's comments are sending the euro lower

ECB Governor Mario Draghi remains convinced that the Eurozone needs an extra support stemming from current monetary policy. He mentioned that verbal intervention will stay in the toolbox used by policymakers to fight against European economy lower use of capital resources which represents the main obstacle in order to send inflation back to 2% ECB target. For the time being, the monthly bond purchases will stay at €60 billion.

Data wise, Eurozone inflation has declined to 1.5% from 1.9% in April. Despite the fact it has been a while that this conclusion has been drawn, we can certainly say that massive easing has not boosted inflation yet. Angela Merkel is concerned by the negative aspects of the monetary policy expansion and the German Chancellor starts to believe that the single currency is too weak.

Currency wise, we think that the EUR/USD pair is going towards 1.10 in the short-term. We therefore believe that there is no much time before markets start to price back economic uncertainties in the Eurozone.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1126

Yesterday's test of 1.1190 has failed an the downtrend has been renewed, reaching a new low at 1.1110. The outlook remains bearish below 1.1160, for a slide towards 1.1020. Minor intraday support lies at 1.1080 and crucial on the upside is 1.1190.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.1160 |

1.1300 |

1.1080 |

1.1022 |

|

1.1190 |

1.1300 |

1.1020 |

1.0838 |

USD/JPY

Current level - 110.84

The intraday bias is negative below 111.50, for a test of 110.20 lows. An eventual break through 111.50 key hurdle will challenge 113.00 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

111.50 |

114.30 |

110.20 |

109.40 |

|

112.00 |

115.60 |

110.20 |

108.12 |

GBP/USD

Current level - 1.2817

The corrective pattern above 1.2775 is still underway and there is a risk of bouncing higher, through 1.2850, towards 1.2910-30 resistance area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.2850 |

1.3120 |

1.2770 |

1.2770 |

|

1.2930 |

1.3500 |

1.2705 |

1.2610 |

ECB President Mario Draghi Says Accommodative Monetary Policy Still Needed

'For domestic price pressures to strengthen, we still need very accommodative financing conditions, which are themselves dependent on a fairly substantial amount of monetary accommodation.' - Mario Draghi, European Central Bank

The European Central Bank President Mario Draghi gave a speech at the European Parliament in Brussels on Monday. The ECB President acknowledged improving economic growth, but stated that stimulus and support measures were still needed to boost inflation. Apart from that, Draghi also pointed to weak wage growth in the Euro zone. Meanwhile, markets expected the Central bank to make a move at its June meeting amid pressures coming from more conservative economies, but Draghi's dovish comments on Monday weakened the odds. However, analysts suggested that the Bank would likely improve its economic outlook at its next meeting amid solid economic growth and Emmanuel Macron's victory in the French Presidential Election. The ECB President said that inflation was far behind the Bank's 2% target and, therefore, policymakers were forced to keep rates and asset purchases unchanged. Following Draghi's speech, analysts predicted that the next key decision for the ECB would unlikely come up until the autumn, when policymakers will need to decide whether to extend the Quantitative Easing programme or not.

Australian New Building Approvals Rebound Last Month

'The failure of the April print to meaningful recoup the prior month's plunge means quarterly approvals growth in Q2 remains in negative territory.' - Tom Kennedy, JP Morgan

Australian building approvals rose more than expected in April, official figures revealed on Tuesday. The Australian Bureau of Statistics reported that new approvals climbed 4.4% to 17,414 on a seasonally adjusted basis in April, following the preceding month's upwardly revised fall of 10.3% and surpassing expectations for a 3.2% increase. Still, the number of building approvals was down 17.2% year-over-year, suggesting that the recent construction boom faded. Apartments contributed the most to the reported month's climb. The ABS also reported that building approvals for private sector dwellings, excluding houses, surged 9.6% to 8,039 in April, compared to March's drop of 18.2%. However, despite April's gain, approvals for private dwellings were down 26.5% on an annual basis. Meanwhile, private sector housing approvals rose 0.5% to 9,137 after falling 2.7% in March. Year-over-year, they were down 7.5% in April. The value of new approvals advanced 7.2% last month, compared to March's drop pf 15.4%. The value of residential and non-residential building rose 8.2% and 5.5%, respectively.

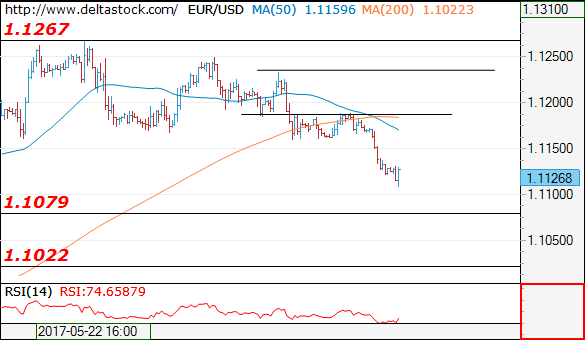

EUR/USD Analysis: Consistent With Forecast

'The euro slipped with emerging currencies after Mario Draghi's dovish message to the European Parliament.' – Garfield Clinton Reynolds, Bloomberg

Pair's Outlook

As it was expected the common European currency retreated down to the weekly S1 at the 1.1141 level against the US Dollar. However, it can be observed that the pair is already heading even lower, as the weekly S1's attracting force has been already left behind. The next support, which will hinder the decline of the common European currency against the Greenback, will be the weekly S2 at 1.1097. Moreover, it is possible that during the week the pair will decline as low as 1.1050 mark, where nearby a strong support cluster is located at.

Traders' Sentiment

SWFX traders remain bearish, as 61% of open positions are short. However, only 52% of trader set up orders are to sell the Euro.

.

GBP/USD Analysis: Retests Wedge’s Support

'Any declines are now classified as corrective and should be well supported ahead of 1.2500 in favour of a higher low and bullish resumption.' – LMAX Exchange (based on PoundSterlingLive)

Pair's Outlook

The GBP/USD pair behaved in accordance with expectations yesterday, having recovered only half way towards the weekly pivot point. A failure to post solid gains is likely to result in more weakness today, with the monthly PP at 1.2762 being the main target. The Cable has another relatively strong support area around the 1.27 mark, but only another disappointing political event is to have sufficient strength for a leg that far down. On the other hand, the wedge's lower boundary could still have the strength to trigger a rebound, but technical indicators are unable to confirm this possibility, as they turned from bullish to mixed.

Traders' Sentiment

There are 52% of traders being long the Sterling today (previously 51%), while the share of purchase orders slid from 53 to 51%.

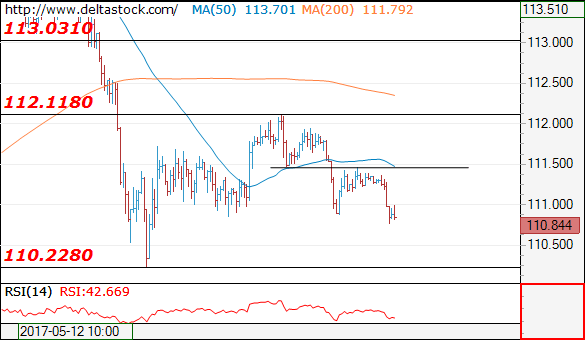

USD/JPY Analysis: Keeps Sliding Down

'The markets are used to news of North Korea's missile tests by now, and the dollar/yen is unlikely to move much unless there is some further escalation of the situation.' – Sony Financial Holdings (based on Reuters)

Pair's Outlook

The USD/JPY currency pair opened the week with flat trade, but with the bearish momentum slightly prevailing. No changes are expected in yesterday's outlook, as risks are still skewed to the downside, as technical indicators are suggesting. The 55-day SMA and the weekly PP form a rather tough resistance around 111.40, which is likely to prevent the Greenback from recovering, but a tough demand cluster rests circa 110.35 as well. The given pair is expected to remain within this trading range of 100 pips in anticipation of the Friday's US NFP data.

Traders' Sentiment

Traders' sentiment remains moderately bearish, with 58% of all open positions being short (previously 57%). At the same time, the portion of orders to acquire the US Dollar inched slightly up. The orders now take up 51% of the market.

Gold Analysis: Remains Below 1,270 Mark

'The ongoing political uncertainty in the market is really driving safe-haven buying at the moment.' – Daniel Hynes, ANZ (based on Reuters)

Pair's Outlook

On Tuesday morning the yellow metal remained near previous sessions levels. Although it was expected that the commodity price will decline as low as the weekly PP at the 1,261.80 level, the bullion has continued to pound the resistance of the monthly PP at 1,269.77 for more than the last 24 hours. It is most likely that a fundamental event will set the short term direction of the bullion. It is either going to retreat to the weekly PP or break the monthly resistance and surge. In the case of a surge the metal's price is most likely going to jump to the weekly R1 at 1,275.49, which marks the beginning of a notable resistance cluster.

Traders' Sentiment

SWFX traders remain almost neutral, as 52% of open positions are long. Meanwhile, 66% of pending commands are set to buy the metal.

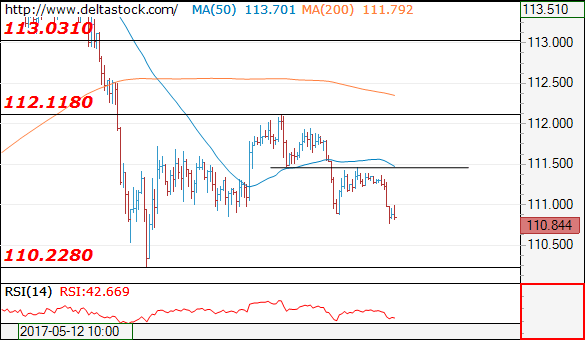

Technical Outlook: USDJPY – Fresh Risk-Off Mode Pushes The Pair Lower

The dollar came under pressure on fresh risk-off mode that increased demand for safe haven and sent the pair to two-week low at 110.77 in early Tuesday's trading. Fresh bearish signal is generating for further easing that may extend towards key near-term support at 110.23 (18 May low, reinforced by rising 200SMA), after multiple failure to clearly break above daily cloud top at 111.80. Asian trading was capped by thick hourly cloud (cloud base lies at 111.26) with additional bearish pressure building on formation of 10/55SMA bear cross at 111.35. Firm bearish structure of technical studies on lower timeframes and daily technicals in bearish setup maintain negative outlook. Violation of 110.23 trigger and psychological 110.00 support (also daily cloud base) would generate strong bearish signal for extension of larger bear-leg from 114.36 (11 May peak). Plethora of strong barriers between 111.35 and 111.80 is expected to cap corrective upticks.

Res: 111.35, 111.46, 111.68, 111.80

Sup: 110.77, 110.67, 110.23, 110.00

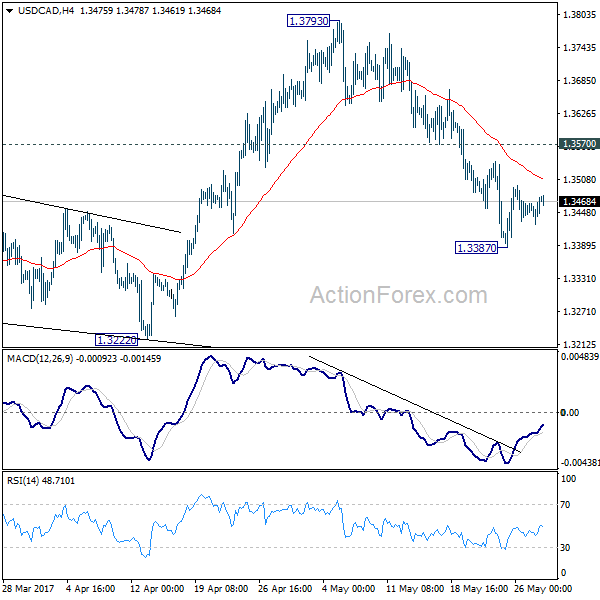

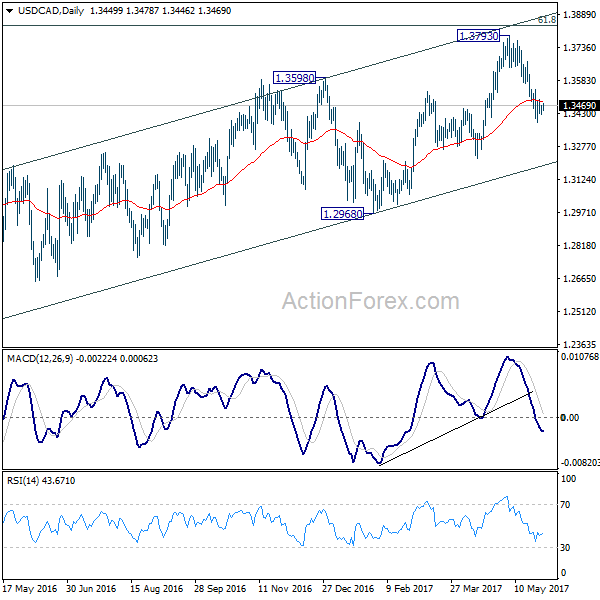

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3432; (P) 1.3449; (R1) 1.3471; More....

Intraday bias in USD/CAD remains neutral for the moment. Some consolidation would be seen above 1.3387 temporary low. But upside of recovery should be limited by 1.3570 resistance and bring fall resumption. At this point, we're still favoring the case that rise from 1.2968 has completed. And the larger rise from 1.2460 could have finished too. Below 1.3387 will target 1.3222 support first. Break of 1.3222 will affirm our bearish view and target 1.2968 key support level for confirmation. However, break of 1.3570 will turn focus back to 1.3793 high instead.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and could have completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.