Sample Category Title

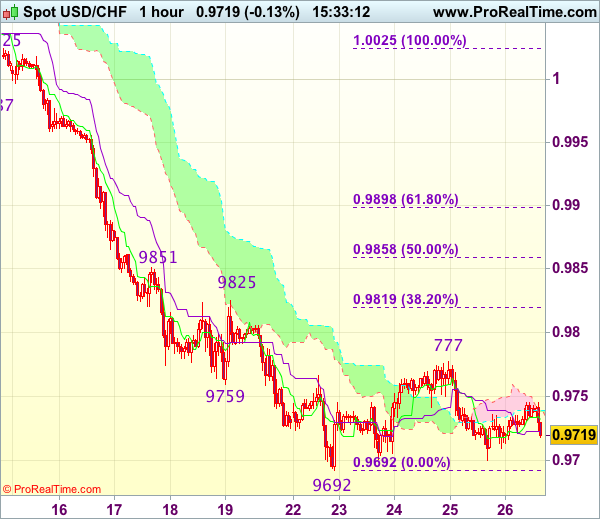

Trade Idea : USD/CHF – Hold long entered at 0.9700

USD/CHF - 0.9715

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9728

Kijun-Sen level : 0.9723

Ichimoku cloud top : 0.9739

Ichimoku cloud bottom : 0.9738

Original strategy :

Bought at 0.9700, Target: 0.9800, Stop: 0.9700

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9700

New strategy :

Hold long entered at 0.9700, Target: 0.9800, Stop: 0.9700

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9700

The greenback met resistance at 0.9777 and has retreated, suggesting caution on our long position entered at 0.9700 but as long as support at 0.9692 holds, further consolidation would be seen with mild upside bias for another rebound, above said resistance at 0.9777 would add credence to our view that temporary low is formed, bring retracement of recent decline to 0.9800, then 0.9819-25 (38.2% Fibonacci retracement of 1.0025-0.9692 and previous resistance) but price should falter below resistance at 0.9851 (also just below 50% Fibonacci retracement at 0.9858), bring another decline later.

In view of this, we are holding on to our long position entered at 0.9700. Below said support at 0.9692 would signal recent decline has resumed and extend weakness to 0.9670-75 but reckon downside would be limited to 0.9650 and 0.9620-25 should hold, bring another rebound later.

Trade Idea : GBP/USD – Hold long entered at 1.2960

GBP/USD - 1.2883

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2897

Kijun-Sen level : 1.2938

Ichimoku cloud top : 1.2989

Ichimoku cloud bottom : 1.2971

Original strategy :

Bought at 1.2960, stopped at 1.2925

Position : - Long at 1.2960

Target : -

Stop : - 1.2925

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Sterling ran into heavy selling pressure at 1.3015 yesterday and has dropped sharply, price just broke below 1.2866 support earlier today, suggesting top has indeed been formed at 1.3048 earlier and downside bias is seen for this the erratic decline from there to extend weakness to previous support at 1.2844, then 1.2831, however, near term oversold condition should prevent sharp fall below 1.2800 and reckon 1.2770-75 would hold from here.

In view of this, would not chase this fall here and would be prudent to stand aside for now. Above previous support at 1.2926 (now resistance) would defer and suggest an intra-day low is formed instead, bring a stronger rebound to 1.2950 but upside should be limited to 1.2990-00.

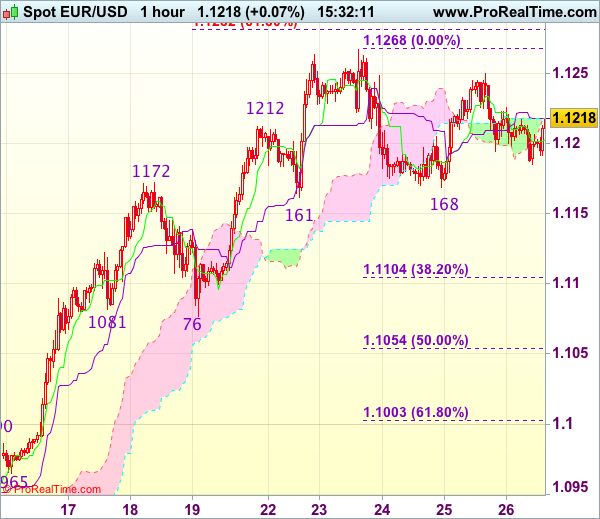

Trade Idea : EUR/USD – Stand aside

EUR/USD - 1.1220

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1203

Kijun-Sen level : 1.1218

Ichimoku cloud top : 1.1218

Ichimoku cloud bottom : 1.1217

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the single currency retreated after meeting resistance at 1.1250 yesterday, as euro found support at 1.1185 and has rebounded, suggesting consolidation with mild upside bias would be seen today, however, a break of said resistance is needed to retain bullishness and signal pullback from 1.1268 has ended, bring retest of this level, once this resistance is penetrated, this would signal recent upmove has resumed and extend gain to 1.1280-85 (61.8% projection of 1.0839-1.1172 measuring from 1.1076) and possibly towards 1.1300-10.

On the downside, below 1.1185 would bring another corrective fall to 1.1161-68 support but break there is needed to signal top has been formed at 1.1268, bring retracement of recent upmove to 1.1130 but reckon downside would be limited to 1.1100-05 (38.2% Fibonacci retracement of 1.0839-1.1268) and price should stay well above support at 1.1076, bring rebound later.

Technical Outlook: GBPUSD Slides Further After Weak GDP / Pre-Election Polls

Bears accelerated in Asia on Friday, following Thursday's close in red after attempts above psychological 1.3000 barrier were capped by falling weekly cloud.

Thursday's red daily candle with long upper shadow signaled rising downside risk, as the pair came under fresh pressure after weaker than expected UK Q1 GDP.

Additional pressure came on release of the latest polls showing narrowing lead of UK Conservative party against Labour party ahead of June 8 elections.

UK PM May party's lead narrowed to 5 points (Tories 43% vs Labour 38%), falling to the lowest after having a comfortable lead of 9 points last week.

The pound remains offered in early Europe, with end of week profit taking expected to put further pressure on the pair.

Technical studies turned bearish on lower timeframes as cable took out initial pivots provided by 10/20 SMA's at 1.2948/32 and acceleration lower also broke below daily Kijun-sen at 1.2901 on daily chart.

Near-term focus turned to key supports at 1.2844/30 (12 / 4 May troughs) break below which would risk extension towards next pivotal support at 1.2786 (Fibo 38.2% of 1.2365/1.3047).

Current pullback is seen as correction of larger uptrend from 1.2108 (14 Mar low) and should be ideally contained at 1.2790 zone, according to wave principles, as the pair is currently riding on the fourth (corrective) wave of five-wave cycle from 1.2108.

Break below 1.2790 pivot would signal stronger correction.

Upside is expected to stay protected by broken 10SMA / daily Tenkan-sen at 1.2950 zone.

Res: 1.2901, 1.2950, 1.2962, 1.3000

Sup: 1.2844, 1.2830, 1.2786, 1.2706

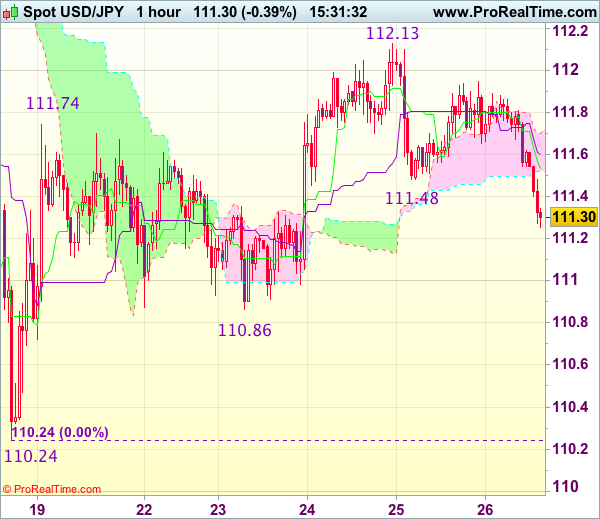

Trade Idea : USD/JPY – Hold long entered at 111.50

USD/JPY - 111.33

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.53

Kijun-Sen level : 111.60

Ichimoku cloud top : 111.70

Ichimoku cloud bottom : 111.52

Original strategy :

Bought at 111.50, Target: 112.50, Stop: 111.15

Position : - Long at 111.50

Target : - 112.50

Stop : - 111.15

New strategy :

Hold long entered at 111.50, Target: 112.50, Stop: 111.15

Position : - Long at 111.50

Target : - 112.50

Stop : - 111.15

As the greenback has dropped again after faltering below 112.00, suggesting caution on our long position entered at 111.50 and 111.15-20 needs to hold to retain prospect of another rebound to 111.70 but break of 112.00 is needed to signal the pullback from 112.13 has ended, bring test of this level, break there would extend the erratic rise from 110.24 low to 112.36 (100% projection of 110.4-11174 measuring from 110.86) and then 112.45-50 (61.8% Fibonacci retracement).

In view of this, we are holding on to our long position entered at 111.50. Below 111.15-20 would abort and risk weakness to indicated support at 110.86 but only break there would confirm top has been formed and suggest the rise from 110.24 has ended, then further fall to 110.50-55 would follow.

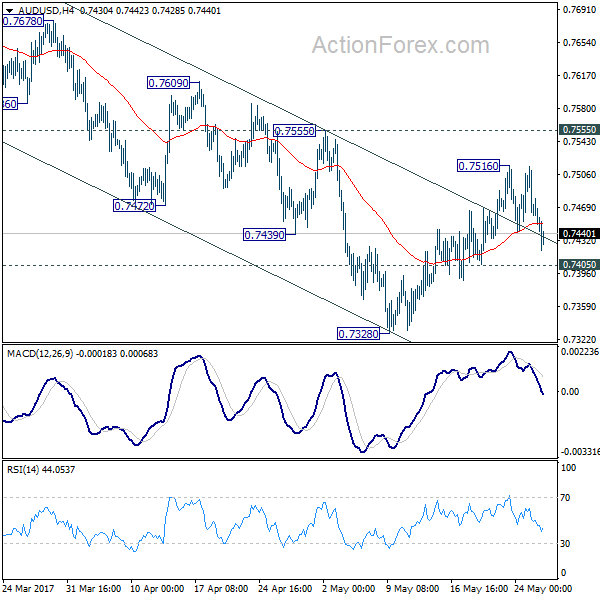

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7430; (P) 0.7473; (R1) 0.7496; More...

Intraday bias in AUD/USD remains neutral for the moment as it's staying below 0.7516 temporary top. With 0.7555 resistance intact, fall from 0.7748 is still expected to continue. Below 0.7405 minor support will turn bias to the downside for 0.7382. Break there will target 0.7144/7158 support zone. However, firm break of 0.7555 will argue that fall from 0.7748 is completed and turn bias back to the upside.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8115) and above.

Oil Slips On OPEC Meeting. US Q2 GDP Expected To Be Revised Higher

The much anticipated OPEC meeting held in Vienna yesterday saw the OIL cartel announce an extension of the oil production cuts until March 2018 as informally reported earlier. Yet, despite the announcement, crude oil prices fell sharply on the day with the NYMEX Crude oil futures falling 4.8% on the day.

The weaker oil prices also pulled down the price of other commodities including gold which slipped to $1256 an ounce. The US dollar managed to post some modest gains but remains largely flat, trading below the 97.50 handle.

In the UK, the Office for national statistics (ONS) revised down the first quarter GDP growth from the initially reported 0.3% QoQ to only 0.2%. The revised numbers came on account of consumers feeling the pinch with rising inflation and weak wage growth.

Looking ahead, the US Commerce department will be releasing the second revision to the first quarter GDP. Economists are expecting a higher revision to 0.9% from first estimates of 0.9%.

EURUSD intraday analysis

EURUSD (1.1197): The EURUSD attempted another go at testing the previous highs above 1.1200, but price action closed with a doji type candlestick pattern which indicates indecision in the markets.

However, for some meaningful correction to be expected, price action will need to follow through with a bearish close today, preferably below 1.1200. This will indicate a move towards the first support level at 1.1100. On the 4-hour chart, supporting the bearish view is the fact that yesterday's gains resulted in a lower high which suggests that some downside may be in store. The economic data today is relatively quiet as far as data from the eurozone is concerned, which will leave most of the heavy-lifting to the U.S. revised GDP numbers.

GBPUSD intraday analysis

GBPUSD (1.2888): The British pound tested the 1.3000 handle briefly yesterday before closing bearish. The price action currently is indicating further declines in GBPUSD. The bearish momentum came on a weaker than expected GDP numbers for the first quarter.

Support at 1.2800 remains as the key support to the downside which will be the initial target. On the 4-hour chart, the breakout validates the rising wedge pattern which will see price action extend the declines to 1.2800. In the event of a retracement, watch for the resistance level at 1.3000 region which is likely to be tested once again. However, in the near term, GBPUSD is expected to test the support at 1.2800.

EURCAD intraday analysis

EURCAD (1.5105): The EURCAD was bullish yesterday as the Canadian dollar was hit by the selling in oil prices. The declines came as crude oil prices fell sharply despite the OPEC announcement to cut oil production.

EURCAD posted a bullish close yesterday back at the resistance level of 1.5102 - 1.5147. The re-adjusted rising wedge pattern suggests that in the short term, price action could be seen moving slightly higher towards 1.5147, reaching the top end of the resistance level. Following this minor push, EURCAD could be seen eventually breaking out from the rising wedge pattern. Initial support at 1.4832 will be tested, followed by a test towards 1.4519.

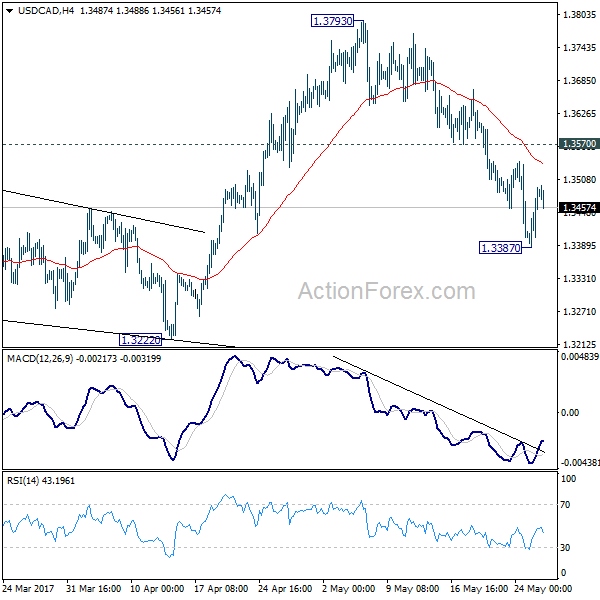

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3417; (P) 1.3455; (R1) 1.3524; More....

A temporary low is in place at 1.3387 as USD/CAD recovered and intraday bias is turned neutral first. Some consolidation would be seen but upside should be limited by 1.3570 resistance and bring another fall. Below 1.3387 will target 1.3222 support first. As noted before, corrective rally from 1.2460 could have finished ahead of 1.3838 fibonacci level. Break of 1.3222 will affirm this case and target 1.2968 key support level for confirmation.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and would end at around 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

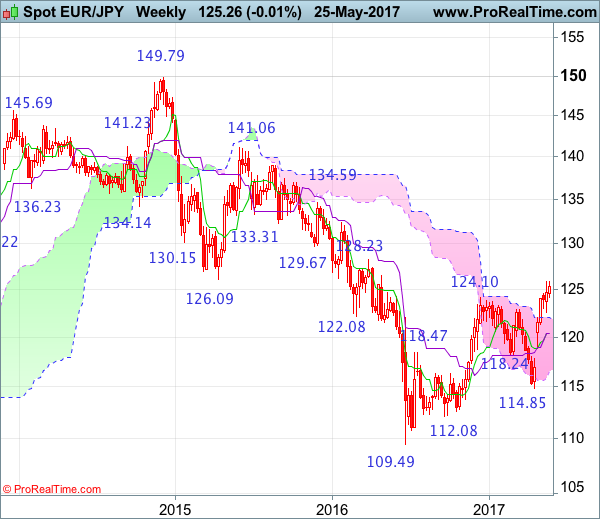

EUR/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Hammer

• Time of formation: 19 Sep 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Doji

• Time of formation: 28 Mar 2017

• Trend bias: Near term up

EUR/JPY – 124.81

Although the single currency has maintained a firm undertone and bullishness remains for recent rise from 114.85 to extend further gain to 125.05-10, however, break of previous chart resistance at 125.82 is needed to signal recent upmove has resumed and extend subsequent headway to 126.50-60, then 127.00-10 but near term overbought condition should limit upside and price should falter well below 128.00-10. If resistance at 125.82 continues to hold, then minor consolidation would take place and risk of another retreat to 123.90-00 and then 122.56 support cannot be ruled out, however, still reckon 121.60-65 (38.2% Fibonacci retracement of 114.85-125.82) would limit downside and bring another rise later.

On the downside, whilst initial pullback to 123.90-00 and then 123.00 cannot be ruled out, reckon downside would be limited to 121.60-65 (38.2% Fibonacci retracement of 114.85-125.82) and bring another upmove later to aforesaid upside targets. Below indicated previous support at 120.60 would abort and signal a temporary top has been formed, bring retracement of recent entire rise to 120.30-35 (50% Fibonacci retracement) and then 120.00 but reckon downside would be limited to 119.40-50 and price should stay above indicated support at 118.92, bring rebound later.

Recommendation: Buy at 121.60 for 124.60 with stop below 120.60.

On the weekly chart, as the single currency has continued trading with a firm undertone, suggesting the erratic rise from 109.49 low is still in progress and bullishness remains for this move to extend gain to 126.45-50, then towards 127.40-50, however, reckon another previous resistance at 128.23 would limit upside and price should falter below 129.60-65 (50% Fibonacci retracement of 149.79-109.49) and price should falter below psychological resistance at 130.00, bring retreat later next month.

On the downside, although initial pullback to 123.90-00 and possibly 123.00 cannot be ruled out, reckon downside would be limited to 122.40-50 and renewed buying interest should emerge around 121.60-65 and bring another rise later. Only below support at 120.60 would defer and risk weakness to the Kijun-Sen (now at 120.34) and then 120.00 which is likely to hold on first testing. Looking ahead, euro needs to penetrate indicated support at118.92 to shift risk to the downside for further fall to 118.00, however, downside should be limited to previous resistance at 117.82 and bring rebound later. A weekly close below 117.82 would suggest first leg of rebound from 114.85 has ended, bring weakness to 117.00 but price should stay above 116.20-25, bring another rebound later.

Market Update – Asian Session: Japan Inflation Recovers, Bullard Talks Down USD

US Session Highlights

(US) Edmunds forecasts May US sales at 1.53M, +7.5% y/y; auto industry seasonally adjusted annual rate (SAAR) at 16.8M

(US) INITIAL JOBLESS CLAIMS: 234K V 238KE; CONTINUING CLAIMS: 1.92M V 1.93ME

(US) APR PRELIMINARY WHOLESALE INVENTORIES M/M: -0.3% V 0.2%E

(US) APR ADVANCE GOODS TRADE BALANCE: -$67.6B V -$64.5BE

Stocks continued to rise as markets were buoyed by strong earnings reports from retailers and positive unemployment data, despite the sharp drop in oil prices. S&P set another all-time intra-day high at 2418.7 before paring a bit to finish the day at its new highest close. The worst-performing S&P sector was Energy, dropping 1.7%, and the two best performing sectors were Consumer Discretionary and Utilities, gaining 1.1% and 0.9% respectively.

US markets on close: Dow +0.3%, S&P500 +0.4%, Nasdaq +0.7%

Best Sector in S&P500: Consumer Discretionary

Worst Sector in S&P500: Energy

Biggest gainers: BBY +21.5%; PVH +4.8%; CSRA +4.6%

Biggest losers: SIG -7.8%; RIG -7.6%; MRO -7.1%

At the close: VIX 10.0 (flat); Treasuries: 2-yr 1.29% (flat), 10-yr 2.26% (-1bps), 30-yr 2.92% (-2bps)

US movers afterhours

NTNX: Reports Q3 -$0.42 v -$0.43e, R$191.8M v $186Me; Guides Q4 -$0.38 v -$0.31e, R$215-220M v $202Me, gross margin ~58% ; +16.3% afterhours

DECK: Reports Q4 +$0.11 v -$0.06e, R$369.5M v $359Me; Guides Q1 -$1.70 to -$1.65 to $ v -$1.73e, Rev up low single digits % y/y; +12.9% afterhours

EGHT: Reports Q4 $0.05 v $0.03e, R$66.5M v $65.7Me; Guides initial FY18 Rev $296-300M v $295Me; income margin 7-9% ; +6.1% afterhours

ULTA: Reports Q1 $2.05 v $1.79e, R$1.31B v $1.28Be; +3.9% afterhours

COST: Reports Q3 $1.59 v $1.31e, R$28.2B v $28.7Be; +1.9% afterhours

MRVL: Reports Q1 $0.24 v $0.21e, R$579M v $570Me; -2.0% afterhours

SPLK: Reports Q1 -$0.01 v -$0.05e, R$242.4M v $233Me; Guides Q2 R$267-269M v $268Me, Non-GAAP op margin ~4% ; -5.7% afterhours

GME: Reports Q1 $0.63 v $0.49e, R$2.05B v $1.89Be; Affirms FY17 $3.10-3.40 v $3.25e, SSS (Ex Tech Brands) -5% to flat ; -6.9% afterhours

ZOES: Reports Q1 $0.01 v $0.01e, R$90.6M v $92.2Me; Cuts FY17 Rev $314-322M v $324Me, SSS -3% to flat; -10.8% afterhours

Politics

(US) White House advisor Jared Kushner said to be under the FBI investigation in Russia probe - US press

(US) Republican candidate Greg Gianforte wins Congressional seat in Montana, defeating Democrat Rob Quist

(UK) According to the latest YouGov/Times poll, Conservatives lead Labour by 43% to 38% ahead of June 8th elections (note: poll was taken after Manchester terror attacks); Smallest lead since Apr 2016

Key economic data

(JP) JAPAN APR NATIONAL CPI Y/Y: 0.4% (3-month high) V 0.4%E ; CPI EX FRESH FOOD (CORE) Y/Y: 0.3% (2-year high) V 0.4%E

(JP) JAPAN MAY TOKYO CPI Y/Y: 0.2% (6-month high) V 0.0%E; CPI EX-FRESH FOOD Y/Y: 0.1% (18-month high) V 0.0%E

(JP) JAPAN APR PPI SERVICES (CGPI) Y/Y: 0.7% V 0.9%E (3-month low)

(KR) South Korea May Consumer Confidence: 108.0 v 101.2 prior

Asia Session Notable Observations, Speakers and Press

Asian markets traded mixed despite continued bullish momentum on Wall St, where 6th consecutive gaining session took US cash indices to new record highs. US gains were particularly impressive given the large sell-off in Energy, as mere extension (rather than expansion) of OPEC supply cut weighed on oil prices to the tune of about 5%. Consumer discretionary has supported markets with a strong beat for big box electronics store Best Buy (up over 20%) as well as more strength in Amazon.

ASX200 is underperforming thanks to a drop in Mining space, with Dalian iron ore futures down 4% while tech-heavy Kospi is adding to its record highs with more gains. In FX, dollar majors are generally rangebound, though USD/JPY is under some notable pressure with a 40pip drop to 111.40. Comments from Fed's Bullard were seen weighing on the greenback as he noted prices deviating noticeably from 2% inflation path and called market expectations of 2 more rate hikes this year as too aggressive. GBP/USD was impacted to the downside as well, with the latest YouGov survey showing Conservative's lead over Labour continue to narrow ahead of next month's elections.

In economic data, rising energy prices last month are finally making a dent in disinflationary forces in Japan, as Headline CPI hit 3-month high while Core CPI (ex food) hit a 2-year high. Recall the latest soft patch of CPI prints, both in Japan and US, have been attributed to price pressure in mobile communications space.

China

(CN) Moody's comments following recent sovereign downgrade of China: China may no longer get A1 rating if there are signs that debt keeps rising and debt exceeds expectations

(CN) China can meet 2017 GDP target of around 6.5% despite slowing economic indicators in Apr - Chinese press

Japan

(JP) Japan PM Abe and US President Trump to hold bilateral meeting at G7 on Friday, May 26th - financial press

Australia/New Zealand

(NZ) Moody's: New Zealand budget shows better debt and growth than AAA rating

(AU) Capital Economics: Australia retail sales growth in April likely weak due to disruptions from Cyclone Debbie - press

Asian Equity Indices/Futures (00:45ET)

Nikkei -0.4%, Hang Seng flat, Shanghai Composite +0.1%, ASX200 -0.6%, Kospi +0.6%

Equity Futures: S&P500 flat; Nasdaq +0.1%, Dax -0.1%, FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (00:45ET)

EUR 1.11.85-1.1215; JPY 111.55-111.85; AUD 0.7420-0.7460; NZD 0.7005-0.7025

June Gold +0.2% at 1,259/oz; July Crude Oil -0.6% at $48.60/brl; July Copper flat at $2.60/lb

(CN) PBOC SETS YUAN MID POINT AT 6.8698 V 6.8695 PRIOR

(CN) PBOC to inject combined CNY40B v CNY70B prior

(AU) Australia MoF (AOFM) sells A$600M in 1.75% 2020 Bonds; avg yield: 1.7612%; bid-to-cover: 4.45x

Asia equities notable movers

Australia

Appen (APN) +4.5%; Guides FY17

Alumina (AWC) -1.6%; CEO sells shares

Ansell (ANN) -6.9%; Cut at UBS

Select Harvests (SHV) -9.7%; Cuts FY17 crop estimate to 13.5K-14K MT, expects material impact on earnings

Japan

Nissan (7201) -0.2%; China's GSR said to be close to $1B deal to purchase Nissan's rechargeable battery unit - financial press

Toshiba (6502) -0.2%; Western Digital said to secure large amount of financing and emerging as a frontrunner for Toshiba chip unit - Japan press

Hong Kong

Oriental Watch Holdings (398) +1.7%; Positive profit alert

China Agri-Industries Holding (606) +1%.6%; To acquire COFCO Fortune Foods for CNY1.05B in cash

GOME Electrical Appliances (493) +1.0; Reports Q1