Sample Category Title

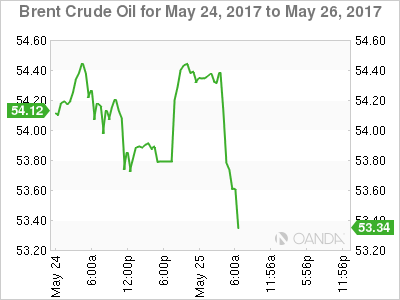

Oil Whacked As OPEC Discusses Cut Extension

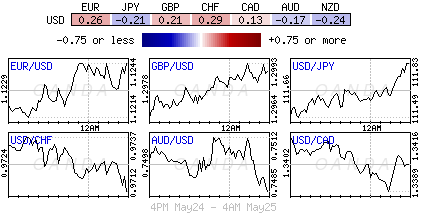

US equity markets look likely to test their all-time highs on Thursday, with the S&P 500 on course to open at record levels and the Dow not far behind. The focus this morning has been on oil and UK markets, with OPEC making statements on the proposed oil cut extension and UK growth figures disappointing in the first quarter.

Buy the Rumour, Sell the Fact – Oil Hit on Cut Extension Comments

Brent and WTI got crushed earlier as energy ministers from within OPEC suggested that an extension will be agreed and will likely be at the same levels for six or nine months. It's been a classic case of markets buying the rumours and selling the facts. It would appear a nine month extension with the potential for deeper cuts was almost fully priced in so when the statements were made, there was nowhere left for prices to go but lower.

We've seen this kind of action time and time again. Traders buy on anticipation of the deal and when its delivered as expected, they take their profits and run. The unwinding of the positions, probably combined with some speculative selling, is what creates this sudden plunge. Prices have rebounded a little following the initial sell-off but remain below the pre-statement levels. With the Saudi Energy Minister confident that stocks can now fall back to their five year average by the first quarter of next year but open to another extension if needed, it will be interesting to see whether prices stabilise at these levels and remain supported – and if so how long for – or if they'll drift lower again as they did following the previous cut. He did suggest that he doesn't see US shale derailing their plans or believe forecasts that output will rise by one million barrels per day but OPEC has been wrong on this in the past.

EUR/USD – Euro Drifting Continues in Thinned Holiday Trade, Fed Minutes Disappoint

GBP Tumbles on Weakest Quarterly UK growth in More Than Four Years

Sterling has come under pressure this morning after the ONS confirmed that the UK grew by only 0.2% in the first quarter – 2% from a year earlier – which is the slowest rate of quarterly growth in more than four years.

It would appear the economic reliance on the consumer is finally taking its toll with higher prices seen as contributing to the softer activity in the first quarter. With wages now falling in real terms, this doesn't bode well for the coming quarters and while the Brexit vote may have taken a little longer than many expected to harm the economy, it would appear that the initial pain is starting to be felt.

Dollar Cannot Catch a Break

It's also worth noting that the pound was already looking a little unsettled at its highs against the dollar. It would appear we've been seeing something of a reluctant rally over the last month and perhaps the sell-off that we've seen in the pair this morning is a reflection of that. Should the pair break below 1.29, it could signal a sharper downturn in the coming weeks. The weakness in the dollar – with another downturn over the last couple of weeks – is certainly helping to support the pair but with a rate hike likely at the June meeting, I wonder whether this will continue.

Still to come today we've got jobless claims data being released from the US and we'll hear from Lael Brainard and James Bullard from the Federal Reserve.

Euro Drifting Continues In Thinned Holiday Trade, Fed Minutes Disappoint

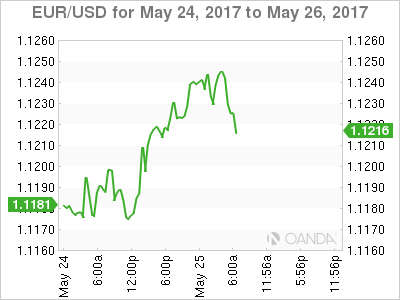

The euro is showing little movement in the Thursday session, and with German and French banks closed for a holiday, this trend will likely continue throughout the day. Currently, EUR/USD is trading just above the 1.12 level. On the release front, OPEC members are meeting in Vienna, and the US releases unemployment claims, with the indicator expected to rise to 238 thousand.

The much-anticipated Fed minutes were released on Wednesday, but traders hoping for confirmation of a June rate hike came away disappointed, as the minutes conveyed a less hawkish tone than the markets had expected. Policymakers were careful in their message, saying that a rate hike was coming “soon”. Does that mean a move at the June policy meeting? The markets believe so, as Fed funds futures for a June hike remained at 78% after the minutes were released. At the same time, the Fed has given itself some wiggle room, and could opt to delay a hike until the second quarter if inflation or consumer indicators take an unexpected nosedive. The minutes stated that policymakers wanted to see additional evidence that the recent slowdown in the economy was temporary before raising rates. As for additional hikes in 2017, the markets remain skeptical. The odds for a September rate stand at just 37%. This pessimism is a result of a weak performance from the US economy in Q1, as well as doubts that President Trump, who is facing congressional investigations over his connections with the Russian government, will be able to pass his agenda of cutting taxes and government spending. Gone are the heady days at the end of 2016, when a red-hot US economy had analysts predicting four rate hikes in 2017. At the same time, a strong improvement in economic data could quickly change the cautious tone of the Fed and revive discussion of four rate hikes this year.

Earlier in the week, the White House presented President Trump’s 2018 budget proposal to lawmakers in Congress. Trump has promised to slash government spending, and much of the funds for the budget would come from huge cuts to the Medicaid health program and food stamps. The budget proposes slashing more than $600 billion from Medicaid and over $192 billion from food stamps over a decade. Trump has promised to balance the budget within 10 years, claiming this can be achieved through tax cuts and annual growth of 3 percent. However, experts are at odds as to whether the economy can reach and maintain such levels of growth, which is much higher than current economic expansion. The budget proposal is unlikely to remain in its present form for very long on Capitol; Hill. Democrats will want nothing to do with it, and Republicans will not want to make drastic cuts to federal programs that will incur the wrath of voters. Still, the Trump administration, which has been in damage-control mode for weeks over the firing of FBI director James Comey, can point to the budget as a step forward in trying to implement Trump’s pro-business agenda.

Dollar Cannot Catch A Break

There were no surprises from the Fed yesterday, but the tone, it was a tad more 'dovish' than the neutrals were expecting.

The FOMC minutes release received a muted reaction in the bond market, despite most Fed members saying that they felt 'weaker data would be temporary and that another rate hike is coming soon.'

Expectations are for a rise as soon as next month (June 13-14). The committee also talked about tapering their balance sheet 'gradually with caps and increasing the cap every three- months.'

Net result, U.S equity markets ended on their highs, with S&P rallying to a record close, the dollar losing some support on yield differentials as investors took note of increased caution about lower inflation data in. And while the case for June rate hike remained above +80% (prior +83%), the Fed funds odds of two-more rate hikes this year have now slid below 50%.

Their next meeting is June 13-14, which will be followed by a press conference.

The markets focus now shifts to Vienna to see if OPEC and non-OPEC members officially extend last November's production cut deal to support global prices.

1. Mixed reaction from regional bourses

The Fed's 'dovish' tone has helped U.S and Asian stocks to post yet more record highs. But that equity bullishness has failed to transfer to Europe, where some stock exchanges are closed today for the Ascension holiday.

In Japan, stocks rose overnight as the strong-yen (¥111.78) trend paused. The Nikkei share average ended +0.4% higher, while the broader Topix gained +0.2%.

In Hong Kong shares followed regional markets higher, even after Moody's downgraded Hong Kong's local and foreign currency issuer ratings shortly after cutting China's ratings yesterday. The Hang Seng index rose +0.8%, while the China Enterprises Index gained +1.7%, a fresh 22-month high.

In China, equities have rebounded sharply, as the blue-chip CSI300 index posted its best day in 21-months amid growing hopes that global index provider MSCI Inc. will add mainland shares to its benchmark next-month.

Korea's Kospi was the best performing regional index, rallying +2.1%, supported by the Bank of Korea (BoK) leaving rates on hold (+1.25%) overnight in a unanimous decision, but signaled a bullish view, stating growth was now seen above last months forecast as household debt increase subsided.

In Europe, most indices have reversed their earlier gains to trade largely lower across the board. Ahead of the U.S open, the DAX trades lower by over -0.5%.

U.S indices are set to open in the black (+0.2%).

Indices: Stoxx50 -0.2% at 3579, FTSE -0.1% at 7507, DAX -0.5% at 12578, CAC-40 -0.2% at 5332, IBEX-35 +0.2% at 10931, FTSE MIB -0.6% at 21233, SMI -0.3% at 9035, S&P 500 Futures +0.2%.

2. Oil steady before expected extension of OPEC output cut

Oil prices are steady ahead of today's OPEC meeting expected to extend production cuts into 2018 in an attempt to drain a global-glut.

Brent crude oil is unchanged at +$53.96, while U.S light crude (WTI) is -10c lower at +$51.26. Both benchmarks are up more than +15% from this months lows.

OPEC and various non-OPEC members, including Russia, are widely expected to agree to extend Novembers cut in oil supplies by -1.8m bpd. The current deal only covers the H1 of 2017.

Note: Market observers believe that a nine-month extension would have little impact on the 'average' price forecast for 2017, which is +$55 per barrel for Brent. However, the bulls believe that if producers can agree in a cut extension to cover all of 2018, the tighter market could push average 2018 Brent prices up towards +$63 per barrel.

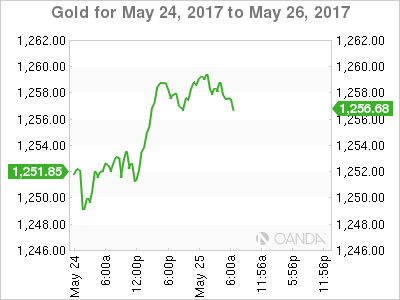

Gold (+$1,257.90 an ounce) is holding steady ahead of the U.S open, supported by the USD slipping after yesterday's FOMC minutes downplayed the chance of more aggressive interest rate hikes.

3. U.S yields fall on Feds 'gradual' approach to reduce balance sheet

Treasury yields fell after the Fed outlined a plan to unwind its balance sheet by 'gradually' allowing increasing amounts of the securities to mature without reinvesting them.

Investors have expected the Fed to reduce its balance sheet carefully, but a more concrete plan to do so is still a positive for bonds, which could be hurt if the Fed took a more aggressive approach.

The plan is expected to involve introducing a series of 'caps' that would determine the maximum amount of the Fed's maturing debt that would be reinvested in new securities – the caps could increase over time to accelerate the shrinking of its balance sheet.

The yield on U.S 10's fell less than -1 bps to +2.24%, after losing -3 bps to +2.25% yesterday.

Elsewhere, French (OAT's) 10-year yields fell -3 bps, while German Bunds dropped -4 bps to +0.36%.

4. Dollar loses its shine

The 'mighty' USD remains on the defensive as the Fed dialed down market's 'hawkish' policy expectations.

The EUR/USD (€1.1227) continues to hover atop of the psychological €1.12 handle. Many expect the 'single' unit pullbacks to be brief and shallow. The 'bulls' believe the EUR is in the process of going higher – the prospect of the ECB announcing a path to more tapering of its asset-purchase program at the June ECB meeting, improving eurozone economic activity, and rising eurozone capital inflows is expected to support the currency towards €1.1275 -1.13.

The pound briefly traded above £1.3000 this morning ahead of this morning's Q1 GDP reading and has since drifted lower (£1.2960) after the data was revised lower in its second reading (see below). Nevertheless, GBP is still within striking distance of testing the alleged option barriers at £1.3050. To many, £1.3000 is considered the key pivot and with any momentum through theses levels expect the structural shorts out there post-Brexit will be looking to wind back. Short-term sterling bulls are now targeting £1.3350/1.3400.

USD/JPY (¥111.88) has resisted the trend and is trading higher after Japan's Upper House approved government's two nominees for the BoJ board. The nominees would replace current dissenters of Kuroda's QQE policy.

5.U.K's Q1 growth revised down

Data this morning showed the U.K. economy slowed more sharply than first thought in Q1 – a warning sign on domestic growth ahead of next months General Election (June 8) and the start of Brexit talks with the EU.

The ONS said its latest data suggests the economy expanded at a quarterly rate of +0.2% in Q1, a weaker pace of growth than the +0.3% preliminary estimate published in April and much weaker than the +0.7% pace for Q4, 2016. It suggests that U.K households are feeling the pinch from rising prices and inadequate wage growth.

Trade also weighed on growth as imports outpaced exports, despite a weakened pound.

Note: there was one bright spot and it was business investment, which rose a steady +0.6% on the quarter

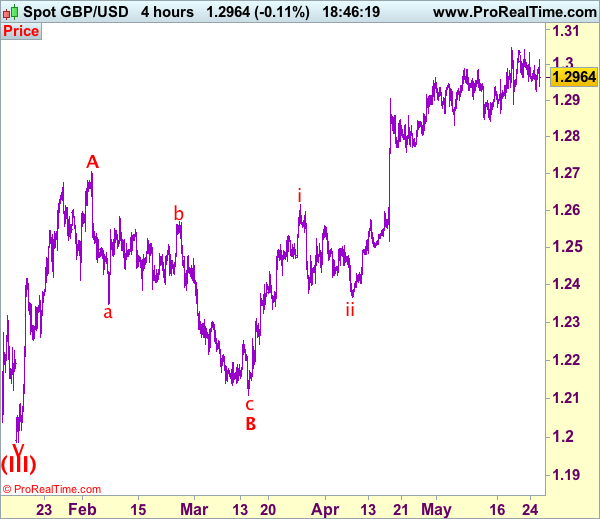

Trade Idea: GBP/USD – Look to buy lower

GBP/USD – 1.2960

Recent wave: Wave V of larger degree wave (III) has ended at 1.1986 and major correction has commenced from there for gain to 1.3000 and 1.3140-50

Trend: Near term up

New strategy :

Look to buy lower

Position: -

Target: -

Stop:-

Despite intra-day brief bounce to 1.3015, as price has retreated again, retaining our view that further consolidation below indicated resistance at 1.3048 would be seen before recent upmove resumes, above said resistance would extend recent rise for further gain to 1.3075-80, then 1.3100-10 but near term overbought condition should limit upside to 1.3150-60 and price should falter well below 1.3200-10.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

On the downside, whilst pullback to 1.2940 is likely, reckon 1.2920-25 would limit downside and bring further consolidation. Only below said support at 1.2889 would signal top has been formed at 1.3048 and bring retracement of recent upmove to 1.2866, then towards previous support at 1.2844 which is likely to hold from here.

Trade Idea: GBP/JPY – Stand aside

GBP/JPY - 145.10

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Despite intra-day brief breach of 145.40, lack of follow through buying and current retreat suggest further consolidation would take place and weakness to 144.70-75 cannot be ruled out, however, break of support at 144.50-55 is needed to signal top is formed, bring further fall to 144.00, then test of support at 143.80 but reckon 143.40 support would hold from here.

On the upside, above resistance at 145.45 would extend the erratic rise from 143.40 low for a stronger retracement of the fall from 148.10 to resistance at 145.90-95, having said that, break there is needed to confirm the decline from 148.10 has ended, bring further subsequent gain to 146.30-35 but resistance at 147.10 should remain intact.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

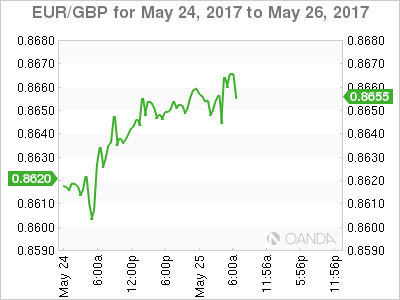

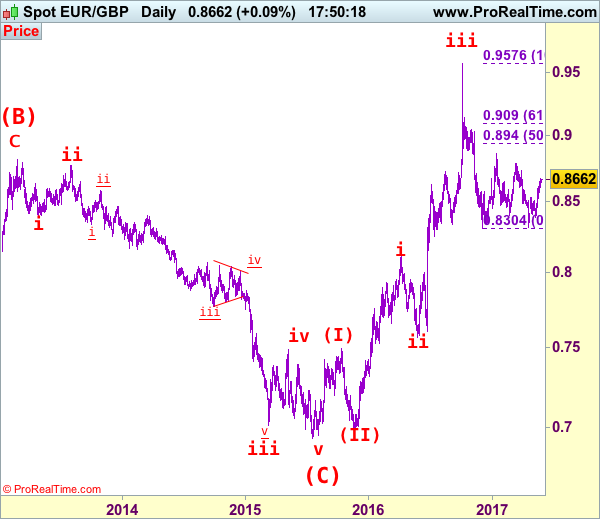

EUR/GBP Elliott Wave Analysis

EUR/GBP – 0.8657

EUR/GBP – The major (A)(B)(C)-(X)-(A)(B)(C) correction from 0.9805 is unfolding and 2nd (A) has possibly ended at 0.6936.

As the single currency has maintained a firm undertone after recent rally above indicated previous resistance at 0.8615, adding credence to our view that another leg of corrective rise from 0.8312 is underway and bullishness remains for this move to extend further gain to 0.8700 and possibly towards resistance at 0.8735, however, as broad outlook remains consolidative, reckon upside would be limited to another previous resistance at 0.87688, bring further choppy trading later.

Our latest preferred count is that the wave V of a 5-wave series from 0.5682 ended at 0.9805 earlier and major from there has possibly ended at 0.8067 as A-B-C-X-A-B-C. We are keeping our view that the entire correction from 0.9805 has possibly ended at 0.7756 and as labeled as the attached daily chart and impulsive move from 0.9084 has ended at 0.7756 as a 5-waver which marked either the (C) wave or the A leg of (C), a daily close above resistance at 0.8831 would suggest (C) leg has ended and headway towards 0.9084.

On the downside, whilst initial pullback to 0.8600-05 cannot be rule out, reckon 0.8565-70 would limit downside and bring another rise later. Below support at 0.8524 would suggest top is possibly formed instead, risk weakness to 0.8500-05 but only break of 0.8455-60 would confirm and suggest the rebound from 0.8312 has ended, bring further fall towards indicated key support at 0.8384.

Recommendation: Buy at 0.8570 for 0.8720 with stop below 0.8500

Euro's long term uptrend started in Feb 1981 at 0.5039 and is unfolding as a (A)-(B)-(C) move with (A): 0.8433 (Feb 1993), (B): 0.5682 (May 2000) and impulsive wave (C) should have ended at 0.9805 with wave III ended at 0.7254 (May 2003), triangle wave IV at 0.6536 (23 Jan 2007) and wave V as well as wave (C) has ended at 0.9805.

We are keeping an alternate count that only wave III ended at 0.9805 and the correction from there is the wave IV and may extend weakness to 0.7700, however, it is necessary to see a daily close above resistance at 0.9143 would change this to be the preferred count.

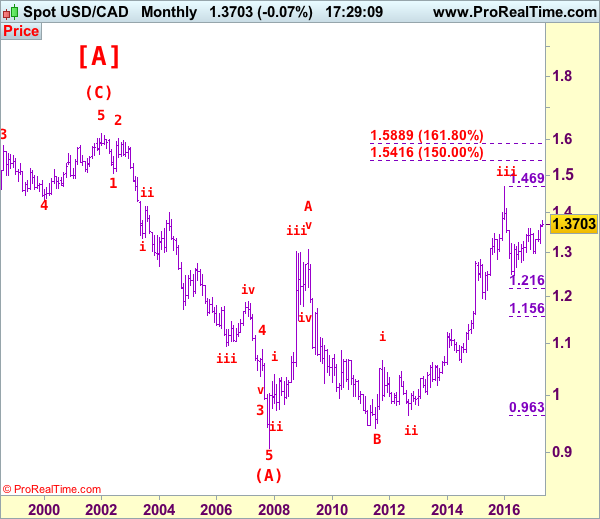

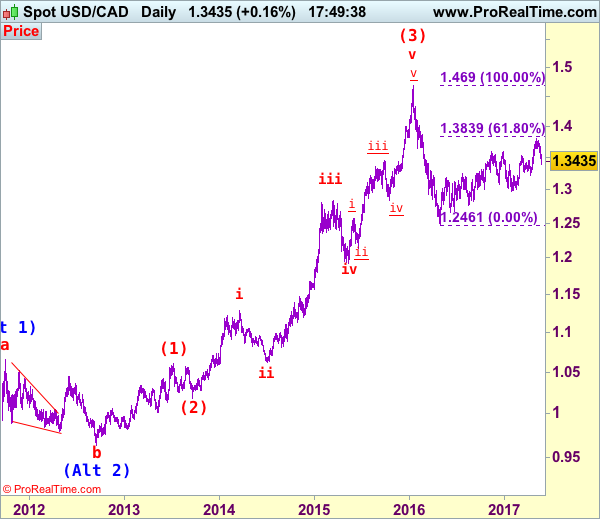

USD/CAD Elliott Wave Analysis

USD/CAD – 1.3433

USD/CAD – Wave v ended at 0.9407 and a-b-c correction may extend gain to 1.4700

As the greenback has dropped again after brief recovery, suggesting top has been formed at 1.3794 and consolidation with downside bias is seen for this fall from there to extend weakness to 1.3320-30, then towards support at 1.3262 but reckon key support at 1.3223 would hold from here, bring rebound later. Looking ahead, only a daily close below this level would provide confirmation that recent upmove has ended at 1.3794, bring further subsequent decline to 1.3140-50 and then 1.3090-00.

We are keeping our view that the wave b from 1.0657 (a leg top) has possibly ended at 0.9633 with (a): 0.9800, wave (b): 1.0447 and wave c at 0.9633, the subsequent rise from there is now treated as wave c exceeded indicated upside target at 1.3770-80 and 1.4000 and wave (3) has possibly ended at 1.4690 and wave (4) correction has commenced for retracement back to 1.2832 support, then 1.2410-20.

On the daily chart, our latest preferred count remains that the A of (B) rally from 0.9059 low (7 Nov 2007) unfolded into an impulsive wave with i: 0.9059-1.0380, ii ended at 0.9819, iii at 1.3019 followed by triangle wave iv at 1.2026 , then wave v formed a top at 1.3066 and also ended the wave A. The wave B is unfolding as an double three a-b-c-x-a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c at 1.0784, followed by wave x at 1.1725, another set of a-b-c unfolded with 2nd a at 0.9931, 2nd b at 1.0674. the 2nd c has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3900 had been met and gain to 1.4700 would follow.

On the upside, whilst initial recovery to 1.3490-00 cannot be ruled out, reckon upside would be limited to 1.3525-30 and bring another decline later. Above previous support at 1.3571 would suggest the first leg of decline from 1.3794 has ended, bring a stronger rebound to 1.3610-15 and possibly towards resistance at 1.3670, price should falter well below said resistance at 1.3794, bring another decline later.

Recommendation: Sell at 1.3530 for 1.3330 with stop above 1.3630.

Longer term - The selloff from 1.6194 (21 Jan 2002) to 0.9059 (07 Nov 2007) is viewed as (A) wave which is a 5-waver as labeled on the monthly chart as below, the subsequently rally is labeled as (B) with impulsive A leg of (B) ended at 1.3066, wave B of (B) is unfolding which has either ended at 0.9407 or would extend one more fall but downside should be limited to 0.9200 and 0.9000 should hold.

Market Update – European Session: OPEC Poised For 9-Month Extension Of Production Cuts At Current Levels, UK Q1 GDP...

Notes/Observations

OPEC, non-OPEC set for new oil cut, eye longer duration with 9-months likely

UK Q1 GDP (2nd reading) revised lower (QoQ: 0.2% v 0.3% advance reading)

Fed dialed down market's hawkish policy expectations

Overnight:

Asia:

Bank of Korea (BOK) left its Repo Rate unchanged at 1.25% (as expected) for its 11th consecutive hold in the current easing cycle; turns optimistic on growth outlook

BOJ's Deputy Gov Iwata: BoJ will manage exit from QE so there is no sudden spike in yields

Bank of Japan (BOJ) Sakurai: underlying inflation remains moderate, crucial for BoJ to maintain monetary easing. Won't be able to achieve 2% inflation sustainable if policymakers try to forcefully stimulate short term demand-

China Securities Regulatory Commission (CSRC): Considering allowing foreign investors into futures market; Will not allow innovation in futures to bypass regulation

Fitch Analyst Fennell: China's finance and track record underpin A+ sovereign rating

US Navy destroyer conducted navigation operation in the South China Sea, within 12 nautical miles of Mischief Reef, which is claimed by China

Europe:

UK PM May plans to cut short her visit to the G7 meeting in Sicily after the terror threat level was raise din Britain to critical following a suicide bombing in Manchester

UK political parties will resume campaigning on Friday following a 3 day suspension after Manchester Arena bombing earlier in week

Americas:

FOMC May 3rd Minutes: Most participants viewed March soft inflation as transitory; Staff presented phased in balance sheet run-off plan. Agreed details on balance sheet plan should be announced soon; operations should get underway this year. Prudent to wait for more evidence that recent weak economic data were transient to raise rates again

Fed's Kaplan (moderate, voter): Expect rate hikes to be more gradual than once per quarter; Fed should not be in a rush and remove accommodation gradually.

Fed's Evans (dove, voter): Reiterates it's key to try harder to hit inflation goal sooner

Treasury Sec Mnuchin:Urged Congress to pass a clean debt ceiling before the August break; Preference is for congress to pass a clean debt ceiling increase

OMB Director Mulvaney: Tax revenues are coming in slower than expected; may have to move up debt limit date

Economic Data

(ES) Spain Q1 Final GDP Q/Q: 0.8% v 0.8%e; Y/Y: 3.0% v 3.0%e

(PL) Poland Apr Unemployment Rate: 7.7% v 7.7%e v 8.1% prior

(UK) Q1 Preliminary GDP Q/Q: 0.2% v 0.3%e; Y/Y: 2.0% v 2.1%e

(UK) Q1 Preliminary Private Consumption Q/Q: 0.3% v 0.3%e; Government Spending Q/Q: 0.8% v 0.4%e; Gross Fixed Capital Formation Q/Q: +1.2% v -0.2%e; Exports Q/Q: -1.6% v +0.5%e; Imports Q/Q: +2.7% v +0.9%e

(UK) Q1 Preliminary Total Business Investment Q/Q: 0.6% v 0.3%e; Y/Y: +0.8% v -0.9% prior

(UK) Apr BBA Loans for House Purchase: 40.8K v 40.8Ke

(HK) Hong Kong Apr Trade Balance (HKD): -34.1B v -39.2Be; Exports Y/Y: +7.1% v +12.5%e; Imports Y/Y: +7.3% v +13.5%e

Fixed Income Issuance:

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.2% at 3579, FTSE -0.1% at 7507, DAX -0.5% at 12578, CAC-40 -0.2% at 5332, IBEX-35 +0.2% at 10931, FTSE MIB -0.6% at 21233, SMI -0.3% at 9035, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes European indices have reversed earlier gains to trade largely lower across the board, led bu the FTSE MIB and Dax which trade lower by over 0.5%. US indices did close at new record highs with futures continuing course this morning after the FOMC minutes yesterday. In the corporate front Petrofac trades lower by over 25% following a probe by the SFO, and the suspension of its COO. Elsewhere WizzAir is outperforming after strong 2018 guidance, whilst Daily Mail Group trades shapely lower after a decline in earnings. Looking ahead notable US earnings scheduled this morning from Medtronics, Genesco, Dollar Tree

Equities

Consumer discretionary [WizzAir [WIZZ.UK] +8.5% (Earnings, FY18 outlook), Daily Mail & General TST [DMGT.UK] -8.7% (Earnings), Halfords [HFD.UK] +2.2% (Earnings), Henry Boot [BOOT.UK] +5% (Trading update)

Consumer Staples [Tate and Lyle [TATE.UK] -1.7% (earnings)

Industrials: [Qinetiq Grp [QQ.UK] +1.3% (Earnings), Vedanta [VED.UK] +1.9% (Chairman: No tie up with Anglo American)

Financials: [Intermediate Capital Grp [ICP.UK] +9.5% (Earnings)

Energy: [Petrofac [PFC.UK] -33% (SFO investigation, COO suspension), Amec Foster Wheeler [AMFW.UK] -4% (With Petrofac)]

Speakers

Russia Central Bank (CBR) Gov Nabiullina: Russia was in no hurry to replenish FX reserves

China Academy of Social Sciences (CASS) researcher Jin Bei: China GDP growth to slow until 2020 as potential economic growth rate will be lower than 6%

China Defense Ministry urged US to correct wrong behavior regarding disturbing peace and stability in South China Sea (**Note: comments made after a US Navy destroyer conducted navigation operation in the South China Sea, within 12 nautical miles of Mischief Reef, which is claimed by China)

Various OPEC ministers comment ahead of its bi-annual meeting in Vienna:

Saudi Arabia Energy Min Al Falih: OPEC likely to extend cuts for 9-months; could be prolonged further if needed; likely to rule on same level. Many countries had indicated flexibility on cuts. Saw oil inventories at 5-year average in Q1 2018; re-balancing would happen sooner rather than later. Nigeria, Libya exempt from production deal (were exempt at Nov OPEC meeting). US Shale oil production would not derail what OPEC was doing. Saudi Arabia has no plans to expand capacity beyond 12.5M bpd

Kuwait Oil Min Almarzooq: Expected 9-month extension of OPEC/Non-OPEC oil cuts.Did not expect meeting to discuss deeper cuts . Market had already absorbed rise in shale oil production

Iran Oil Min Zanganeh: No objection to 12-month extension; will respect and comply with OPEC decision of either 3,6, 9 or 12 months. Wanted oil prices between $55-60/barrel. Did not have oil in floating storage and was currently exporting 2.1-2.2M bpd

Iraq Oil Min Min Al-Luaibi: Supported all options on output agreement. Supported 9 month extension with same level of cuts; there was a proposal for an extension with deeper cuts. Country's oil production at 4.465M bpd; exports at 3.79M bpd (includes Kirkuk)

UAE Oil Min Mazrouei: Sought a 6-month production cut and not concerned about US shale oil production

Venezuela Oil Min Del Pino: Deal most likely to be extended by 9-months but 6-months is also an option

Ecuador Energy Min Perez: Supported 9-month extension of OPEC deal

Nigeria Oil Min Kachikwu stated that he supported 9-month extension of oil production cuts; OPEC members largely on-board with this view

Currencies

USD remained on the defensive as the Fed dialed down market's hawkish policy expectations. Fed members noted that it was prudent to wait for more evidence that recent weak economic data were transient before raising rates again.

EUR/USD was higher and nearing the mid-1.12 area (just off recent 6-month high) while GBP/USD continue to probe the 1.30 level.

GBP/USD was above the 1.30 level just ahead of Q1 GDP reading and drifted lower afetr the data was revised lower in its 2nd reading.

USD/JPY bucked the trend and was higher as several BOJ officials

Price action in oil was choppy as various OPEC ministers spoke ahead of the bi-annual meeting. WTI crude drops to session lows near $51/barrel after Saudi Oil Min Al-Falih noted that deeper production cuts not needed at this time. WTI was above $52/barrel at 5-week highs before the numerous OPEC ministers spoke

Fixed Income

Bund futures trade at 161.37 up 31 ticks, surging as stocks slide. Gains took out the 161.32 (May 23rd high) resistance level. Further resistance lies near the April 27th high of 162.01 level followed by 163.68. A break of 160.01 support level could see lows target 159.01 followed by 157.50.

Gilt futures trade at 128.82 higher by 29 ticks and approaching last week's high of 128.95 following disappointing UK GDP and BBA loans data. Last week's rally respected both the 129.00 handle and the 129.14 April 18th high. Price is now tentatively above the 128.51 level and finds key support at the 127.52 support level. An acceleration lower could test the 126.74 region. Resistance stands at 129.14 followed by 132.80.

Thursday's liquidity report showed Wednesday's excess liquidity rose to €1.628T a slight gain of €0.8B from €1.6272T prior. Use of the marginal lending facility rose to €186M from €130M prior.

Corporate issuance saw over $2.75B come to market via 2 issues headlined by Home Depot $2B in an 3-part senior unsecured offering and High Grade Pipeline $750M in 7-year notes

Looking Ahead

OPEC bi-annual meeting in Vienna (currently underway)

(EU) NATO Leaders Meet in Brussels

(EU) EU President Tusk and EU's Juncker meet with US President Trump in Brussels

05:30 (ZA) South Africa Apr PPI M/M: 0.5%e v 0.3% prior; Y/Y: 4.9%e v 5.2% prior

05:30 (HU) Hungary Debt Agency (AKK) to sell Bonds (3 tranches)

05:45 (IT) Italy Fin Min Podoan at conference

06:00 (IL) Israel Mar Manufacturing Production M/M: No est v -2.3% prior

06:00 (CZ) Czech Republic to sell 3-month Bills; Avg Yield: % v -1.25% prior

06:00 (RO) Romania to sell 5.95% Mar 2021 Bonds; Yield: % v 2.46% prior; bid-to-cover: x v2.9x prior

06:30 (AU) RBA's Debelle participates on panel in London

07:00 (UR) Ukraine Central Bank Interest Rate Decision: Expected to cut Key Rate by 50bps to 12.50%

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Apr Advance Goods Trade Balance: -$64.5Be v -$64.2B prior (revised from 64.8B)

08:30 (US) Initial Jobless Claims: 238Ke v 232K prior; Continuing Claims: 1.93Me v 1.898M prior

08:30 (US) Apr Preliminary Wholesale Inventories M/M: 0.2%e v 0.2% prior; Retail Inventories M/M: No est v 0.4% prior

08:30 (US) Weekly USDA Net Export Sales

09:00 (RU) Russia Gold and Forex Reserve w/e May 19th: No est v $399.7B prior

09:00 (MX) Mexico Apr Trade Balance: -$1.6Be v -$0.2B prior

09:00 (ZA) South Africa Central Bank (SARB) Interest Rate Decision: Expected to leave Interest Rates unchanged 7.00%

09:30 (BZ) Brazil Apr Total Outstanding Loans (BRL): No est v 3.077T prior; M/M: No est v 0.2% prior; Personal Loan Default Rate: No est v 5.9% prior

10:00 (US) Fed's Brainard (voter, dove) participates on panel

10:00 (MX) Mexico Q1 Current Account Balance: -$6.5Be v -$3.4B prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) May Kansas City Fed Manufacturing Activity: 10e v 7 prior

11:00 (BR) Brazil to sell Fixed Rate 2023 and 2027 Bonds

11:00 (BR) Brazil to sell 2017, 2019 and 2020 LTN Bills

12:00 (CA) Canada to sell 5-Year Bonds

13:00 (US) Treasury to sell 7-Year Notes

13:30 (BR) Brazil Apr Central Govt Budget Balance (BRL): +7.3Be v -11.1B prior

Oil Whacked As OPEC Discusses Cut Extension

- Buy the rumour, sell the fact – Oil hit on cut extension comments;

- GBP tumbles on weakest quarterly UK growth in more than four years;

- US jobless claims and Fed speeches still to come.

US equity markets look likely to test their all-time highs on Thursday, with the S&P 500 on course to open at record levels and the Dow not far behind. The focus this morning has been on oil and UK markets, with OPEC making statements on the proposed oil cut extension and UK growth figures disappointing in the first quarter.

Brent and WTI got crushed earlier as energy ministers from within OPEC suggested that an extension will be agreed and will likely be at the same levels for six or nine months. It's been a classic case of markets buying the rumours and selling the facts. It would appear a nine month extension with the potential for deeper cuts was almost fully priced in so when the statements were made, there was nowhere left for prices to go but lower.

We've seen this kind of action time and time again. Traders buy on anticipation of the deal and when its delivered as expected, they take their profits and run. The unwinding of the positions, probably combined with some speculative selling, is what creates this sudden plunge. Prices have rebounded a little following the initial sell-off but remain below the pre-statement levels. With the Saudi Energy Minister confident that stocks can now fall back to their five year average by the first quarter of next year but open to another extension if needed, it will be interesting to see whether prices stabilise at these levels and remain supported – and if so how long for – or if they'll drift lower again as they did following the previous cut. He did suggest that he doesn't see US shale derailing their plans or believe forecasts that output will rise by one million barrels per day but OPEC has been wrong on this in the past.

Sterling has come under pressure this morning after the ONS confirmed that the UK grew by only 0.2% in the first quarter – 2% from a year earlier – which is the slowest rate of quarterly growth in more than four years. It would appear the economic reliance on the consumer is finally taking its toll with higher prices seen as contributing to the softer activity in the first quarter. With wages now falling in real terms, this doesn't bode well for the coming quarters and while the Brexit vote may have taken a little longer than many expected to harm the economy, it would appear that the initial pain is starting to be felt.

It's also worth noting that the pound was already looking a little unsettled at its highs against the dollar. It would appear we've been seeing something of a reluctant rally over the last month and perhaps the sell-off that we've seen in the pair this morning is a reflection of that. Should the pair break below 1.29, it could signal a sharper downturn in the coming weeks. The weakness in the dollar – with another downturn over the last couple of weeks – is certainly helping to support the pair but with a rate hike likely at the June meeting, I wonder whether this will continue.

Still to come today we've got jobless claims data being released from the US and we'll hear from Lael Brainard and James Bullard from the Federal Reserve.

OPEC And Non-OPEC Meeting: Extension, Deeper Cuts, Or Both?

Today, the highly anticipated meeting between major OPEC and non-OPEC oil producers will take place in Vienna. Recent comments from the oil ministers of Saudi Arabia and Russia suggest they have agreed to extend the November oil-output cut deal until March 2018, an extension of 9 months at the current volume of 1.8 mbpd. Ever since those remarks, many other OPEC oil ministers have expressed their support for a 9-month extension as well. Bearing this in mind, we think that most, if not all, of the good news are probably already priced into oil, evident by the recent surge in prices. As a result, if we only get a 9-month extension, we see further upside in oil as likely being limited. In order for oil prices to rally significantly from current levels, we believe that producers have to deliver something over and above what the market currently expects, namely an extension of a full year and/or deeper cuts in production.

WTI traded somewhat higher yesterday, after it hit support near 50.60 (S1) on Tuesday. During the European morning Thursday, the price looks to be headed for a test of the 52.60 (R1) resistance hurdle. In case the producers deliver a full-year extension or deeper cuts, WTI could surge above 52.60 (R1) and initially aim for the 54.00 (R2) territory. A clear break above that zone could pave the way for the next resistance of 54.80 (R3). On the other hand, a potential disappointment, like an extension of only 6 months, could trigger a pullback in oil prices. In such a case, we expect the bears to seize control and push the price lower towards 50.60 (S1), where a decisive break could set the stage for the next support at 49.90 (S2).

Bank of Canada stands pat, maintains a neutral tone

The BoC kept its policy unchanged yesterday, as was widely expected. The tone of the meeting statement was neutral overall, indicating that although uncertainties continue to cloud the Canadian outlook, the economy's adjustment to lower oil prices is almost complete and recent economic data such as business investment have been encouraging. Perhaps due to the absence of any really concerned comments by policymakers, the Canadian dollar gained on the decision. In case the OPEC and non-OPEC producers deliver something more than the market expects, the currency could come under renewed buying interest.

USD/CAD dipped yesterday from near 1.3540 (R3) following the BoC decision, and then declined even further after the FOMC minutes, to break below the support (now turned into resistance) barrier of 1.3410 (R1). Considering the BoC's neutral outlook, the battered US dollar, and the prospect of a deal that boosts oil prices, we think that this decline could continue. An initial break of the 1.3360 (S1) zone could trigger further downside extensions towards the 1.3310 (S2) support territory.

FOMC minutes: Prudent to wait for evidence that GDP slowdown is transitory

The FOMC minutes from the May policy meeting had a neutral tone overall in our opinion, with every hawkish comment being balanced with a cautious remark. For instance, most participants judged that if economic data came in more or less in line with their expectations, then another rate hike “would soon be appropriate”. However, they also judged it would be prudent to wait for evidence that the recent slowdown in GDP was transitory before taking any further action. The US dollar declined alongside US treasury yields, but interestingly enough, the probability for a June rate hike remained elevated at 83% according to the Fed funds futures. Moving forward, we expect the market to shift its attention to incoming US data as well as Fed speakers. In that respect, Fed Board Governor Brainard's remarks today may be closely followed, for any hints as to whether she will support a hike at the coming meeting.

As for the rest of today's highlights:

During the European day, the UK will release its 2nd estimate of GDP for Q1. The forecast is for the 2nd reading to be in line with the preliminary figure and confirm that economic growth slowed notably from Q4. In such a case, we expect market participants to turn their focus to the other important aspect of the 2nd estimate: business investment. Investment surprisingly declined in Q4, generating concerns that the first real impact of Brexit-related uncertainties had shown up, as firms appeared hesitant to invest in the UK ahead of the impending Brexit negotiations. We expect investors to look at the Q1 print in order to determine whether this was a one-off, or if Brexit jitters have already began to weigh on GDP growth. The consensus is for the investment rate to have rebounded, but only marginally so. Another soft print could enhance the aforementioned concerns and thereby, prove negative for sterling.

Besides Fed Board Governor Lael Brainard, we will also hear from ECB Vice President Vitor Constancio today.

WTI

Support: 50.60 (S1), 49.90 (S2), 48.40 (S3)

Resistance: 52.60 (R1), 54.00 (R2), 55.00 (R3)

USD/CAD

Support: 1.3360 (S1), 1.3310 (S2), 1.3260 (S3)

Resistance: 1.3410 (R1), 1.3460 (R2), 1.3540 (R3)