Sample Category Title

Trade Idea: USD/CAD – Stand aside

USD/CAD - 1.3464

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

The greenback has fallen again after brief recovery, suggesting the decline from 1.3794 top is still in progress and downside risk remains for this move to bring a stronger retracement of recent rise, hence weakness to 1.3411 support cannot be ruled out, however, near term oversold condition should prevent sharp fall below there and reckon 1.3350-60 would hold, bring rebound later.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Above 1.3505-10 would bring recovery to 1.3540-45 but only break of previous support at 1.3571 would signal low is formed, bring a stronger rebound to 1.3630-35 but resistance at 1.3670 should remain intact.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

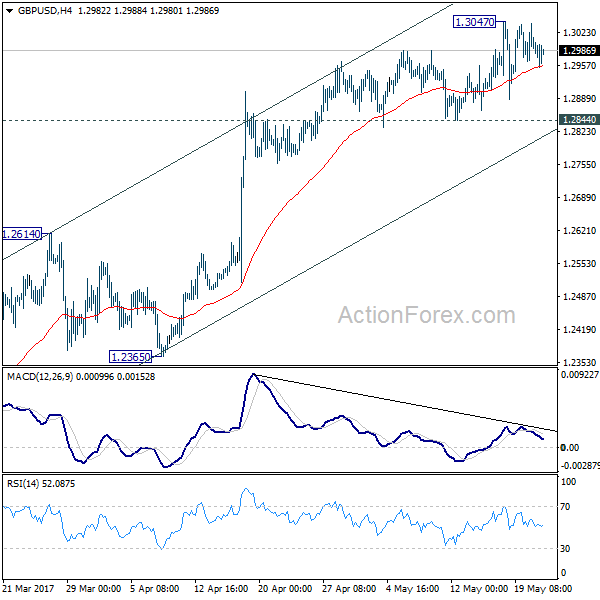

GBP/USD Bears Test Uptrend Line Support Post Manchester Terror Attack

GBP/USD has been trading above the downside uptrend line support since mid-March.

Cable rallied around 3.5% since Theresa May announced a snap general election on April 18 as markets have largely priced in a Tory victory.

GBP/USD hit a high of 1.3047 on May 18, last seen on September 29, breaking a significant resistance level at 1.3000.

However, the bullish momentum has waned since Monday, because of the drop in the approval rating for the Conservative Party caused by Theresa May's plans to cancel free school lunches and reduce free healthcare services for wealthy senior citizens.

The terror attack last night in Manchester further weighed on GBP/USD resulting in Cable falling below the significant level at 1.3000.

Currently, GBP/USD still holds above the downside uptrend line support.

However, on the 4-hourly chart, the 10 SMA is crossing over the 20 SMA, indicating bearish sentiment is increasing.

If the downside uptrend line support is broken, we will likely see a further fall in GBP/USD.

The resistance level is at 1.3000, followed by 1.3020 and 1.3050.

The support line is at 1.2950, followed by 1.2920 and 1.2900.

We will see a set of US economic data to be released between 14:45 - 15:00 BST this afternoon. It will likely affect GBP/USD.

Technical Outlook: USDJPY Trading in Directionless Mode

The pair is trading in directionless mode for the fourth day, after bounce from fresh one-month low at 110.23 was capped by descending 55SMA which continued to limit upside attempts. Today's action is capped by daily Kijun-sen line (111.34) with lower pivot at 110.74 (daily cloud base) being under pressure, on overall weaker greenback. Bearish tone prevails on near-term studies while daily MA's are in bearish setup and maintain downside pressure. A probe below daily cloud and attempts towards strong supports at 110.23/00 (18 May low/psychological support) and 200SMA at 109.87 could be anticipated while 55SMA caps, as last week's long bearish daily candle continues to weigh. Descending 55SMA offers solid resistance (currently at 111.65), followed by daily cloud top at 111.80, which are expected to limit upticks and keep focus shifted lower. Alternative scenario requires break above daily cloud to neutralize bearish pressure and open way for recovery extension towards next strong barrier at 112.30 (daily Tenkan-sen).

Res: 111.34; 111.65; 111.80; 112.30

Sup: 110.74; 110.50; 110.23; 110.00

USDX Forecasting the Decline after Flat

Hello fellow traders. In this technical blog we're going to take a quick look at the past Elliott Wave charts of Dollar Index published in members area of www.elliottwave-forecast.com. We're going to take a look at the price structures of USDX , count the swings and explain the forecast.

USDX 4 hour update 05.09.2017

As our members know, we were pointing out that USDX is having incomplete bearish swings sequnces within the cycle from the 03/02 peak. From the chart below, we can see that USDX has a clear 5 swing from the peak, when we're about to complete 6th swing as Irregular Flat. Consequently, we're calling further weakness once proposed Flat is complete. Dollar index is targeting 97.92-96.91 area ideally.

Now let's take a look at the short term structures...

USDX 1 Hour Asia Chart 05.11.2017

Dollar Index is about to complete wave ((x)) recovery as expanded flat structure. We got clear 5 waves from the lows that is part of wave (c) of flat. Although, the extreme area is reached at 99.64 -99.92, and we have minimum requirements for correction to complete soon, we see possibility of marginal extension higher within the blue box still.

USDX 1 Hour NY Midday Chart 05.11.2017

We got expected marginal extension and reaction from the blue box. Now we're calling wave ((x)) recovery completed at 99.88 peak as expanded flat. While the price stays below 99.88 peak further weakness should ideally follow.

USDX 1 Hour London Chart 05.16.2017

99.88 peak held nicely and USDX is now breaking lower, suggesting more downside in 7th swing towards proposed 97.92-96.91 area.

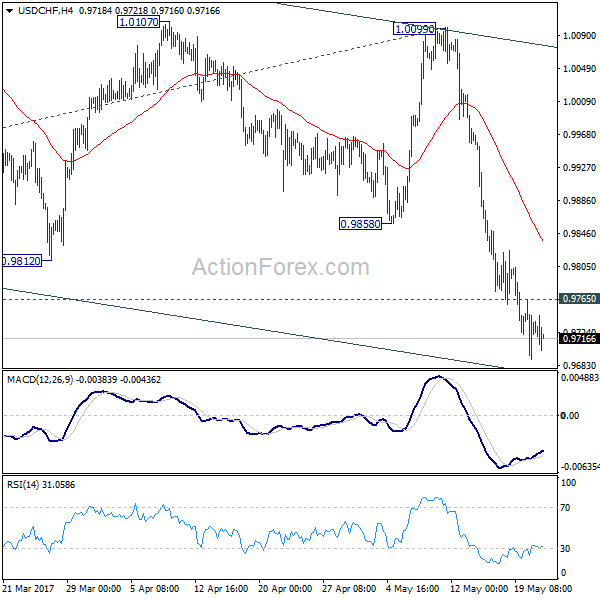

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9694; (P) 0.9730; (R1) 0.9768; More.....

USD/CHF continues to lose some downside momentum. But with 0.9765 minor resistance intact, intraday bias remains on the downside. Current fall from 1.0342 should target 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. We'll start to look for bottoming signal again below there. On the upside, above 0.9765 minor resistance will turn intraday bias neutral again and bring consolidations first, before staging another fall.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.94; (P) 111.27; (R1) 111.62; More...

Intraday bias in USD/JPY remains neutral for the moment. Consolidation from 110.23 is still progress and could extend. Overall, recent development suggests that whole corrective decline from 118.65 is going to extend lower. Below 110.23 turn bias back to the downside and send USD/JPY through 108.12 low. In that case, we'll look for bottoming signal again at 61.8% retracement of 98.97 to 118.65 at 106.48.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

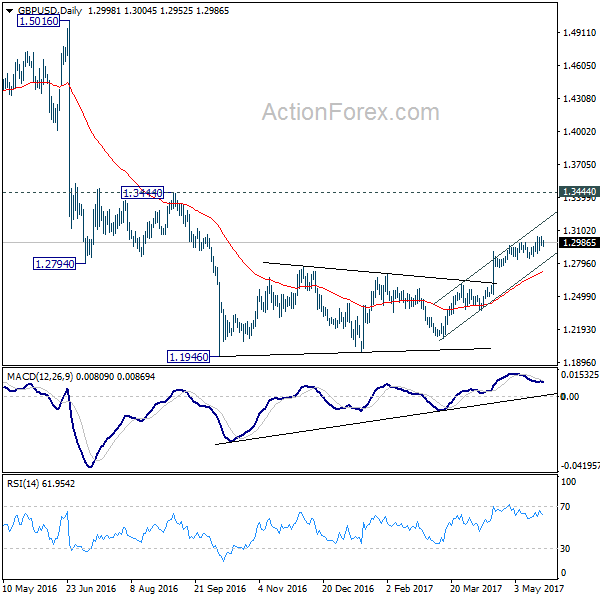

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2961; (P) 1.3002; (R1) 1.3039; More...

GBP/USD continues to be bounded in range of 1.2844/3047 and intraday bias remains neutral first. As long as 1.2844 minor support holds, further rise remains mildly in favor. Nonetheless, as we are still viewing price actions from 1.1946 as a corrective move, we'd expect upside to be limited below 1.3444 resistance to bring near term reversal. On the downside, break of 1.2844 will indicate short term topping and turn bias back to the downside for 1.2614 resistance turned support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There are signs of reversal, like breaking of 55 week EMA, weekly MACD turned positive, and monthly MACD crossed above signal line. But still, break of 1.3444 resistance is need to confirm medium term bottoming. Otherwise, outlook will remains bearish for extend the down trend through 1.1946 low.

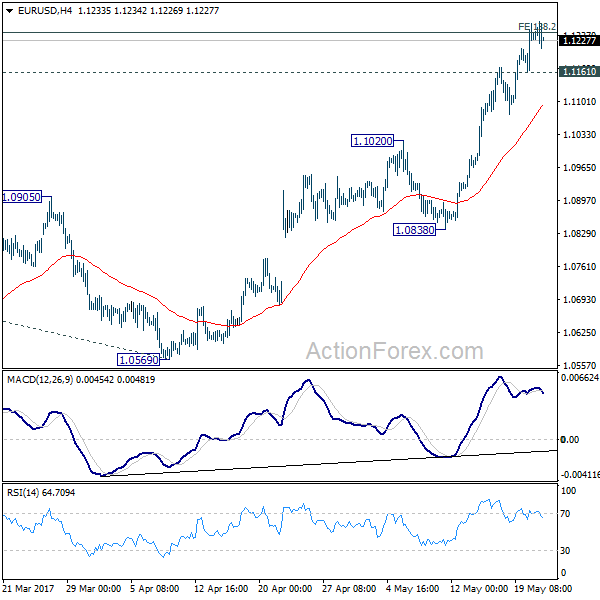

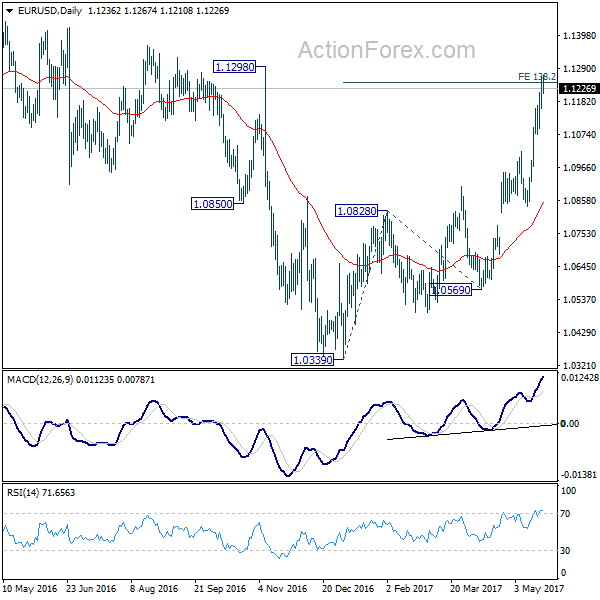

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1178; (P) 1.1220 (R1) 1.1280; More....

Intraday bias in EUR/USD remains on the upside as 1.1161 minor support holds. We stay cautious on strong resistance from 1.1245/98 (138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245) resistance zone to limit upside and bring reversal. However, decisive break of 1.1298 will carry larger bullish implication and target 1.1615 resistance next. On the downside, below 1.1161 minor support will turn bias neutral first.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD now far above 55 week EMA. Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

Euro Firm after Solid PMIs and German Ifo, But Outshone by Commodity Currencies

Euro remains firm against most major currencies but is outshone by commodity currencies today. Solid economic data from Eurozone lifts sentiments with major European indices trading higher at the time of writing. US futures also point to higher open. Meanwhile, Dollar and Sterling remain the weakest major currencies for the week. The Greenback will need something drastic from either US President Donald Trump or FOMC minutes to halt it's decline against Euro and Swiss Franc. In other markets, gold is trading flat in tight range around 1260. WTI crude oil is losing some upside momentum but stays firm around 51.

Eurozone PMI hits six year high

Eurozone PMI manufacturing rose to 57.0 in May, up from 56.7, beat expectation of 56.5. That's the highest level in more than six years. Eurozone PMI services dropped to 56.2, down from 56.4 and missed expectation of 56.4. Markit chief business economist Chris Williamson noted that "the consensus forecast of 0.4 percent second quarter growth could well prove overly pessimistic if the PMI holds its elevated level in June." Meanwhile, "although the pace of economic growth signalled by the PMI is historically consistent with the ECB taking a hawkish stance, the dip in cost pressures will add weight to arguments that there's no rush to taper policy."

Germany PMI manufacturing rose to 59.4 in May, up from 58.2, beat expectation of 58.0. Germany PMI services dropped to 55.2, down from 55.4, missed expectation of 55.5. Markit noted that the data point to at least 0.6% growth in Q2, same as Q1. France PMI manufacturing dropped to 54.0, down from 55.1, missed expectation of 55.2. France PMI services rose to 58.0, up from 56.7, beat expectation of 56.7.

German Ifo hits record high

German Ifo business climate rose to 114.6 in May, up from 112.9, beat expectation of 113.1. That's the highest level on record since the series began back in 1991. Expectation gauge rose to 106.5, up from 105.2 and beat expectation of 105.4. Current assessment gauge rose to 123.2, up from 121.1, beat expectation of 121.0. Ifo head Clemens Fuest noted in the statement that "economic activity in Germany remains very brisk" and businesses were feeling "euphoric". Ifo economist Klaus Wohlrabe said that French President Emmanuel Macron's win has provided a tailwind." And "it is a signal that the European Union is not under acute pressure, as it was a year ago." Also from Germany Q1 GDP growth was finalized at 06% qoq, unrevised.

Eurogroup Chairman Jeroen Dijsselbloem said in a press conference after the Eurogroup meeting Eurozone finance ministers, IMF and Greek government failed to reach an "overall agreement" on debt relief for Greece. Nonetheless, the "formal conclusion of the second review is very close" and he holed to complete it in June. EU Economics Commissioner Pierre Moscovici is also hopeful for a deal at the next Eurogroup meeting in Luxembourg on June 15.

Sterling softens after Manchester terrorist attack

Sterling remains the weakest major currency for the week so far. At least 22 people were reported killed by the terrorist suicidal bomb attack in Manchester in UK. Another 59 people were injured. UK Prime Minister Theresa May condemned the attack and said it stands out for "its appalling, sickening cowardice, deliberately targeting innocent, defenseless children." Meanwhile, she pledged that "significant resources have been deployed to the police investigation, and there continues to be visible patrols around Manchester, which include the deployment of armed officers."

May halted her election campaign after the attack. But pressure on her and the Conservatives is piling up as recent poll showed that their lead over Labour halved. May would need to have a landslide win in the election on June 8 to give her a strong position for Brexit negotiation.

Also released today

Canada wholesales sales rose 0.9% mom in March. UK public sector net borrowing rose to GBP 9.6b in April. CBI reported sales dropped sharply to 2 in May. Swiss trade surplus narrowed to CHF 1.97b in April. Japan all industry activity index dropped -0.6% mom in March.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1178; (P) 1.1220 (R1) 1.1280; More....

Intraday bias in EUR/USD remains on the upside as 1.1161 minor support holds. We stay cautious on strong resistance from 1.1245/98 (138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245) resistance zone to limit upside and bring reversal. However, decisive break of 1.1298 will carry larger bullish implication and target 1.1615 resistance next. On the downside, below 1.1161 minor support will turn bias neutral first.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD now far above 55 week EMA. Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 4:30 | JPY | All Industry Activity Index M/M Mar | -0.60% | -0.50% | 0.70% | |

| 6:00 | CHF | Trade Balance (CHF) Apr | 1.97B | 2.87B | 3.10B | 3.04B |

| 6:00 | EUR | German GDP Q/Q Q1 F | 0.60% | 0.60% | 0.60% | |

| 7:00 | EUR | France Manufacturing PMI May P | 54 | 55.2 | 55.1 | |

| 7:00 | EUR | France Services PMI May P | 58 | 56.7 | 56.7 | |

| 7:30 | EUR | Germany Manufacturing PMI May P | 59.4 | 58 | 58.2 | |

| 7:30 | EUR | Germany Services PMI May P | 55.2 | 55.5 | 55.4 | |

| 8:00 | EUR | Eurozone Manufacturing PMI May P | 57 | 56.5 | 56.7 | |

| 8:00 | EUR | Eurozone Services PMI May P | 56.2 | 56.4 | 56.4 | |

| 8:00 | EUR | German IFO - Business Climate May | 114.6 | 113.1 | 112.9 | |

| 8:00 | EUR | German IFO - Expectations May | 106.5 | 105.4 | 105.2 | |

| 8:00 | EUR | German IFO - Current Assessment May | 123.2 | 121 | 121.1 | |

| 8:30 | GBP | Public Sector Net Borrowing (GBP) Apr | 9.6b | 8.0b | 4.4b | 2.3b |

| 10:00 | GBP | CBI Realized Sales May | 2 | 10 | 38 | |

| 12:30 | CAD | Wholesale Sales M/M Mar | 0.90% | 1.00% | -0.20% | 0.30% |

| 13:45 | USD | US Manufacturing PMI May P | 53.1 | 52.8 | ||

| 13:45 | USD | US Services PMI May P | 53.2 | 53.1 | ||

| 14:00 | USD | New Home Sales Apr | 610K | 621K |

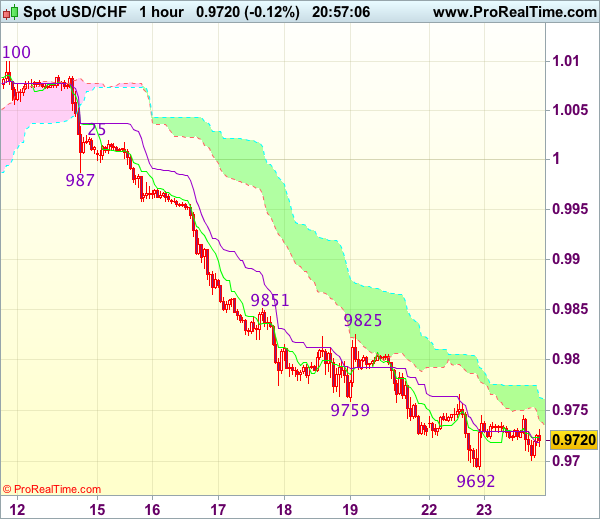

Trade Idea Update: USD/CHF – Hold long entered at 0.9700

USD/CHF - 0.9720

Original strategy :

Bought at 0.9700, Target: 0.9800, Stop: 0.9690

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9690

New strategy :

Hold long entered at 0.9700, Target: 0.9800, Stop: 0.9690

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9690

Although dollar has remained under pressure and marginal weakness from here cannot be ruled out, as long as yesterday’s low at 0.9692 holds, prospect of another rebound remains, above 0.9765-70 would suggest low is possibly formed, bring subsequent bounce to 0.9800 but reckon upside would be limited to 0.9825 and previous resistance at 0.9851 should remain intact, bring another decline later.

In view of this, we are holding on to our long position entered at 0.9700. Below 0.9670-75 would risk weakness to 0.9650 but still reckon downside would be limited to 0.9620-25 and bring another rebound later.