Sample Category Title

Fed Focus To Sharpen

With Trump overseas the focus on politics is fading at the same time as the June 14 FOMC meeting comes into focus. The New Zealand dollar was the top performer while the euro lagged as it finally gave up some ground. Kuroda and Australian construction work are up next.

The US dollar caught a bid late in New York trade on Tuesday as Treasury yields moved higher. Yesterday's speech from Brainard generally avoided monetary policy except for a nod towards soft core inflation in the Q&A. The thinking was that she would have said something more if she was planning to argue against a June hike. The same could be said about another dove in Kashkari. He said he wants to see more economic data before making up his mind.

The thinking in the market is as follows: If the dovish contingent at the Fed hasn't been swayed yet, there's no hope of swinging the moderates and hawks in time for June 14.

There is still time for a shift before the June 3 blackout period starts. A full slate of top-tier data is due before then and one to watch will be the FOMC minutes on Wednesday. They will likely skew hawkishly because they're from May 3, when officials had more confidence about inflation and growth. But if the Fed wants to sneak in a hint about patience, it's an opportunity.

Before that, the BOJ's Kuroda speaks at 0000 GMT in Tokyo. Expectations are low for any kind of shift from the BOJ at the moment so any hint might enliven JPY trading.

For AUD traders, the Q1 construction work report is due at 0130 GMT. The consensus is for a 0.5% decline to compound a 0.2% drop in Q4 2016. Any miss is likely to move AUD as the RBA keeps a close eye on data.s

EUR/USD Extends Gains, But Rally to Slow?

- European equities opened little changed as uncertainty after the Manchester terrorist attack weighed on sentiment. However, European markets soon returned to risk-on modus as EMU eco data were very strong. Gains eased slightly in afternoon trading but most European indices still show gains of about 0.5%.

- US equities futures traded in positive territory for most of the day, but open only with marginal gains of 0.1%/0.2% as a big part of the post-Trump losses are reversed and as key technical levels are again coming within reach.

- European PMI confidence indicators indicated that European growth will stay strong in the second quarter. The May EMU composite PMI remained at the highest level in more than six years (56.8). According to IHS Markit the PMI pointed to 0.7% Q/Q in the quarter of 2017.

- German business morale as measures by Ifo brightened more than expected in May to hit its highest level on record since 1991. Both current conditions index (123.2 from 121.4) and the expectations component (106.5 from 105.2) improved further, indicating that Europe's biggest economy is firing on all cylinders.

- President Donald Trump is set to propose a raft of politically sensitive cuts in his first full budget, for the fiscal year that starts in October, a proposal that some analysts expected would be put aside by lawmakers. Trump wants lawmakers to cut $3.6 trillion in government spending over 10 years according to a preview given to reporters.

- The Brexit squeeze on British consumers has hurt the government's finances as well as retailers, data showed on Tuesday. A stalling of sales tax revenues, a barometer of the economy, helped to widen Britain's budget deficit by more than expected. A separate survey showed business confidence among retailers declined at the fastest pace since 2012.

- The Hungarian central bank left its benchmark rate unchanged at 0.90% for the 12th month. Recent strong economic data failed to convince policy makers to change tactics. Rate-setters remain ready to use targeted instruments to ease conditions further if inflation remains persistently below target.

Core bonds little changed; Schatz auction fails.

Core bonds trade flat (Germany) to slightly higher (US Treasuries) in an uneventful session. Strong EMU data weighted in the morning session on the Bund and helped equities higher. From noon onwards, the Bund struggled higher, but without much conviction, but limiting the losses. The Schatz auction went poorly (see below) while the Belgium new 20-year syndicated OLO attracted strong demand and was priced sharply (see below). There was a lot of talk about the US budget proposals, but ultimately it was considered as a non-starter and thus left US Treasuries untouched. At the time of writing, US yields decline modestly between 0.8 bp (2-yr) to 1.8 bps (5-yr). The German 2-yield rises by 2.7 bp while yields at the remainder of the German curve are almost flat.

In EMU bond markets 10-yr yield spreads narrowed slightly for semi-core and Ireland (-2 bp), while Italy outperformed (-4 bps). Greece trades 15 bps wider as a result of the inability of the Greek creditors to cling a deal on debt relief. That means there is still no certainty Greece will receive the next tranche of its bailout loan. That is needed to repay €7B of maturing bonds and coupons.

Belgium sold successfully €3B of its 20 yr benchmark (June 2037) at mid-swaps +8. The debt agency allocated less than investors expected after the book totalled more the €15B. As a consequence, Belgium outperformed at the 20-yr sector. The German Schatz auction (€5B 0% June 2019)) was again very poor. The bid/cover amounted to only 0.9 (€3.965B). The Bundesbank retained more than €1B for its market regulation which brought the official bid/cover at 1.2. There was an unusual tail of 2 cents. The Schatz 2-yr underperformed the German curve.

EUR/USD extends gains, but rally to slow?

Today, the trends of the previous days persisted. USD/JPY (111.10) struggled to make any further gains even as sentiment on risk remained constructive for most of the session. The euro remained well bid supported by very strong EMU confidence data. The EUR/USD touched a new intraday top but trades currently again in the 1.1235 area. The jury is still out, but the pace of the Euro rally shows tentative signs of slowing.

Overnight, the terrorist attack in Manchester dominated the press headlines, but the impact on global markets was modest. The yen traded marginally stronger (USD/JPY 111.00). EUR/USD (1.1250 area) held near the recent highs even as negotiations on a solution for the Greek debt involving the IMF again didn't reach a conclusion.

European equities opened mixed to slightly lower. EUR/USD dropped temporary to the 1.1225 area before the start of European equity trading. However, a series of impressive EMU eco data reactivated a European risk trade. The EMU PMI remained at the highest level in more than six years. German IFO confidence even printed the best level since the early 90's. That data suggest ongoing strong growth in the second quarter and question the need for an extremely accommodative ECB policy stance. Core bond yields rose gradually further. Especially short-term interest rate differentials narrowed in favour of the euro. EUR/USD touched a new correction top in the 1.1268 area. As was the case of late, USD/JPY again hardly profited from the risk-on sentiment. The pair held a tight range mostly in the low 111-area.

There were no important early morning data in the US. US investors debated the new budget plan of the Trump administration. However, the plan contained aggressive spending cuts and it is unclear how the budget gap will be solved. All this makes it very unlikely a similar plan will pass in Congress. If anything, the plan might be a negative for the dollar. The US PMI report was mixed with manufacturing (52.5) printing slightly softer than expected, but services was stronger than expected (54.00). Even so, the report doesn't help risky assets or the dollar. EUR/USD trades in the 1.1235/40 area. USD/JPY still struggles not the fall below the 111 big figure.

EUR/GBP sets a new ST correction top

Today, the news flow on the UK and the UK economy remained sterling negative. The terrorist attack in Manchester yesterday evening weighed on sterling overnight, but the losses were limited. During the morning session, the April budget deficit was reported wider than expected. VAT revenues disappointed indicating a loss of dynamics in consumer spending. The CBI May reported sales were also softer than expected. At the same time, the euro remained in good shape as EMU eco data indicating ongoing strong growth in Q2. EUR/GBP touched a new correction top in the 0.8675 area around noon. Afterwards, the euro rally shifted into lower gear. EUR/GBP trades currently in the 0.8650 area. The intraday picture of cable was more diffuse. The pair hovered sideways in the upper half of the 1.29 big figure. The pair still fails to sustain north of 1.30 even as USD sentiment remains fragile.

Yen Unchanged Despite Disappointing Japanese Data

USD/JPY continues to have a quiet week. In Tuesday's North American session, the pair is trading just above the 111 line. On the release front, Japanese Flash Manufacturing PMI dropped to 52.2, short of the forecast of 52.9 points. Japanese All Industries Activity declined 0.6%, weaker than the forecast of -0.4%. US data also stumbled on Tuesday. New Home Sales dropped to 569 thousand, well short of the forecast of 611 thousand. As well, the Richmond Manufacturing Index dropped to just 1 point, compared to a forecast of 15 points. On Wednesday the Federal Reserve will release the minutes of its policy meeting earlier this month.

The Fed is likely to raise rates at the June policy meeting, but the odds of a rate hike have been showing an unusual amount of movement. In late April, a rate hike was priced in at just 50%. The odds have jumped higher in May, and currently the markets have priced in a hike at 78%. Leaving a June hike aside, a key question is how many more hikes does the Fed have in mind for 2017? On Monday, FOMC member Robert Kaplan stated that three interest increases in 2017 was "appropriate". Earlier in the year, there was speculation that the Fed might raise rates four times in 2017, but with inflation still below the Fed target of 2.0%, three moves is a more likely scenario. The Fed minutes are expected to underscore support for a June move, but many not shed much light on what happens after that.

With President Trump overseas for his first trip abroad, the White House presented Trump's 21018 budget to lawmakers in Congress on Tuesday. Trump campaigned on slashing government spending, and the budget lives up to that promise, with major cuts to the Medicaid and the food stamp programs. Trump has outlined an ambitious program to cut government spending by $3.6 trillion in the next 10 years and achieving a balanced budget by 2020. The budget includes $25 billion for paid leave after childbirth and some $200 billion for infrastructure programs. Trump's budget will face a tough sale on Capitol Hill, with both Democrats and Republicans likely to demand changes. Still, with the cloud of scandals around dismissed FBI director James Comey lingering in the air, Trump can point to the budget as a step forward in his agenda to rein in government spending.

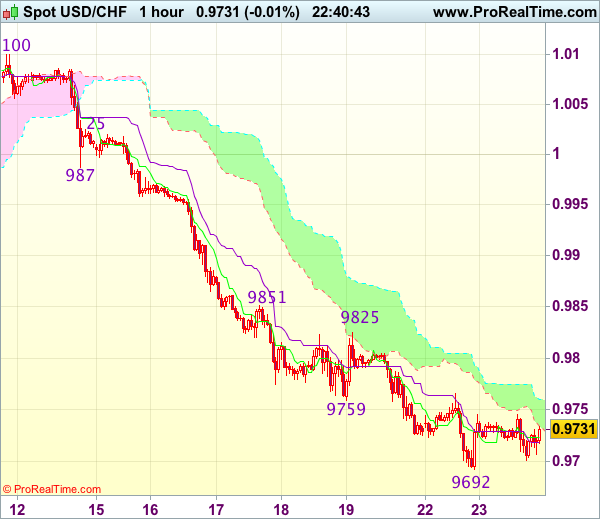

Trade Idea Wrap-up: USD/CHF – Hold long entered at 0.9700

USD/CHF - 0.9721

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9723

Kijun-Sen level : 0.9719

Ichimoku cloud top : 0.9760

Ichimoku cloud bottom : 0.9734

Original strategy :

Bought at 0.9700, Target: 0.9800, Stop: 0.9690

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9690

New strategy :

Hold long entered at 0.9700, Target: 0.9800, Stop: 0.9690

Position : - Long at 0.9700

Target : - 0.9800

Stop : - 0.9690

Although dollar has remained under pressure and marginal weakness from here cannot be ruled out, as long as yesterday’s low at 0.9692 holds, prospect of another rebound remains, above 0.9765-70 would suggest low is possibly formed, bring subsequent bounce to 0.9800 but reckon upside would be limited to 0.9825 and previous resistance at 0.9851 should remain intact, bring another decline later.

In view of this, we are holding on to our long position entered at 0.9700. Below 0.9670-75 would risk weakness to 0.9650 but still reckon downside would be limited to 0.9620-25 and bring another rebound later.

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.2977

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2977

Kijun-Sen level : 1.2998

Ichimoku cloud top : 1.2999

Ichimoku cloud bottom : 1.2969

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s rise to 1.3043, as cable has retreated after faltering below indicated resistance at 1.3048 (last week’s high), retaining our view that further choppy trading below this level would be seen and pullback to 1.2950 cannot be ruled out, however, reckon downside would be limited to 1.2920-25 and said support at 1.2889 should remain intact, bring another rebound later.

On the upside, only a break of said resistance at 1.3048 would confirm recent upmove has resumed an extend further gain to 1.3075-80 and possibly towards 1.3100-10 later. As near term outlook is mixed, would be prudent to stand aside in the meantime.

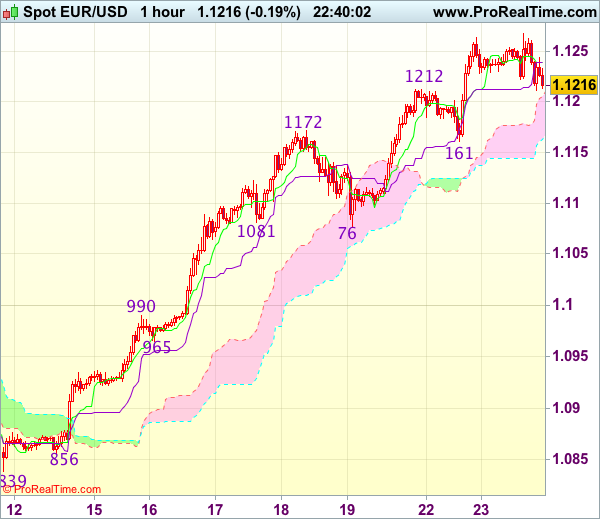

Trade Idea Wrap-up: EUR/USD – Stand aside

EUR/USD - 1.1222

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1240

Kijun-Sen level : 1.1240

Ichimoku cloud top : 1.1206

Ichimoku cloud bottom : 1.1163

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the single currency has maintained a firm undertone after recent rally and near term bullishness remains for recent upmove to extend gain to 1.1260-65, reckon upside would be limited to 1.1280-85 (61.8% projection of 1.0839-1.1172 measuring from 1.1076) and loss of near term upward momentum should prevent sharp move beyond 1.1300-10, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below 1.1185-90 would bring pullback towards support at 1.1161 but break there is needed to signal top is formed, bring retracement of recent rise to 1.1125-30 first.

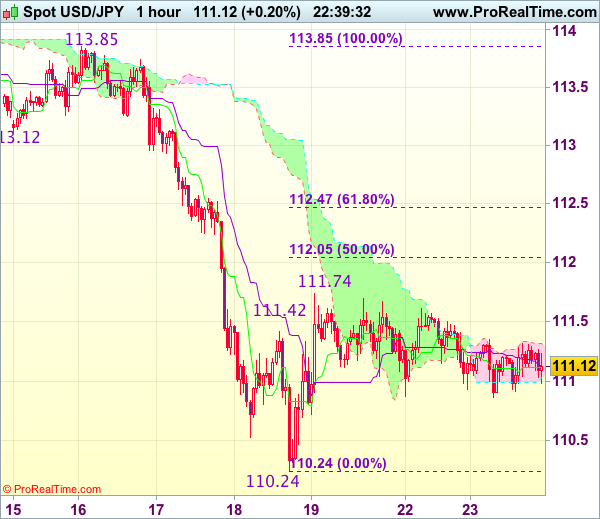

Trade Idea Wrap-up: USD/JPY – Sell at 112.05

USD/JPY - 111.07

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.12

Kijun-Sen level : 111.14

Ichimoku cloud top : 111.32

Ichimoku cloud bottom : 111.03

Original strategy :

Sell at 112.05, Target: 110.85, Stop: 112.40

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.05, Target: 110.85, Stop: 112.40

Position : -

Target : -

Stop : -

The greenback has remained confined within near term established range and further sideways trading within this familiar range would be seen and another corrective bounce to resistance at 111.74 is likely, however, reckon upside would be limited to 112.00-05 (50% Fibonacci retracement of 113.85-110.24) and bring another decline later, below 110.70-75 would suggest the rebound from 110.24 has ended, bring retest of this level first.

In view of this, would be prudent to sell dollar on further subsequent recovery as 112.05-10 should limit upside and bring another decline. Above 112.35-40 would defer and signal low is formed instead, risk a stronger rebound to 112.65-70.

Technical Outlook: Aussie Resumes Uptrend from 0.7328

The Aussie resumes uptrend from 0.7328 (09 May low) and probes above 0.7500 barrier, after strong barrier at 0.7469 (daily Kijun-sen/Fibo 61.8% of 0.7555/0.7328) has been eventually taken out.

Bull-leg from 0.7406 (19 May trough) extends into third consecutive day, boosted by weaker US dollar and bullish signal on break above 0.7469 pivot.

The pair eyes a cluster of strong barriers between 0.7436 (converged 200/55SMA's) and 0.7555 (02 May high/100SMA), break of which would generate another strong bullish signal.

Meantime, the rally may show signs of stall on approach to these barriers, as slow stochastic is entering overbought territory. Strong bullish structure suggests mild correction, with broken daily Kijun-sen offering initial support and 20SMA at 0.7434, expected to contain.

Res: 0.7517; 0.7536; 0.7555; 0.7584

Sup: 0.7485; 0.7462; 0.7434; 0.7423

Trade Idea: EUR/GBP – Buy at 0.8575

EUR/GBP - 0.8645

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

New strategy :

Buy at 0.8575, Target: 0.8675, Stop: 0.8535

Position : -

Target : -

Stop : -

Euro’s anticipated rally adds credence to our bullish view that the rise from 0.8312 low is still in progress and bullishness remains for this move to extend further gain to 0.8675-80 and then toward s0.8700, however, loss of upward momentum should prevent sharp move beyond latter level and price should falter below resistance at 0.8735, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy euro again on pullback as 0.8575-85 should limit downside. Below 0.8550 would defer and suggest top is possibly formed, bring subsequent test of said support at 0.8524, once this level is penetrated, this would provide confirmation.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Elliott Wave Analysis: USDJPY Trading In A Corrective Recovery

On the intra-day chart of USDJPY we are observing a corrective three-wave recovery in the making. Recently price completed a five wave impulse to the downside within blue wave a, which means some slow and choppy movement was expected to follow. At the moment we see price trading in late stages of sub-wave b), so we expect final push to follow in the near-term into red wave c) of b. Resistance for wave c) may later be found around Fibonacci ratio of 50.0 or 61.8.

USDJPY, 1H