Sample Category Title

Dollar Held to Ransom

Monday May 15: Five things the markets are talking about

Global equities start the week better bid, shrugging off cyber attack threats, a missile test in North Korea, and weak U.S data.

Friday's U.S retail sales and inflation data may suggest that expectations for global growth have run too high.

Nevertheless, investor optimism over China's international infrastructure plans (an alternative to TPP) is offsetting concerns over the strength of the global economy.

Oil and commodity currencies are surging on expectations for a supply cut.

In Germany, Chancellor Merkel party won an election in the country's most populous state yesterday, solidify her lead ahead of Germany national election in September.

The Fed remains on track to hike rates next month with jobless claims at a 28-year low and the unemployment rate down to +4.4%, however, the odds have fallen to +70% from +83% on waning U.S inflation outlook.

On the data front this week, in Japan, GDP for Q1 will be the focus, with growth expected to have accelerated. In the U.K, inflation numbers are due tomorrow, followed by a labor market report Wednesday.

In the U.S, it's a slow week, however, tomorrow's industrial production print will provide useful insight into how the factory sector is performing.

1. Despite geopolitical risks, equities supported

Resilient Asian stocks continue to trade atop of their two-year high overnight, shaking off threats from by a ransom ware attack and North Korea saber rattling.

In Japan, regional stocks were small pressured by a stronger yen (¥113.47). The Nikkei share average fell -0.1%, while the broader Topix fell -0.04%.

In Hong Kong, the Hang Seng China Enterprises Index rose +1.5%, climbing for a sixth consecutive session.

In China, the Shanghai Composite Index rose +0.2%, and the Hang Seng Index advanced +0.7%.

In Europe, it's a quiet start to trading despite the event packed weekend. The Eurostoxx 600 has added +0.2%, after touching the highest level in two years last week. The FTSE has got a boost from the uptick in commodities.

U.S stocks are set to open little changed.

Indices: Stoxx50 -0.2% at 3631, FTSE +0.1% at 7444, DAX little changed at 12763, CAC-40 -0.1% at 5400, IBEX-35 +0.2% at 10920, FTSE MIB +0.3% at 21642, SMI -0.3% at 9100, S&P 500 Futures +0.1%

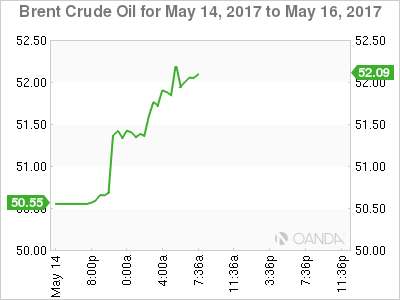

2. Oil jumps as Russia and the Saudi's back longer supply cuts

Oil prices have rallied more than +2% ahead of the U.S open, after Saudi Arabia and Russia said supply cuts need to last into next-year.

The market views this as a step towards keeping an OPEC-led deal to support prices in place longer than originally agreed.

Energy ministers from both countries said that supply cuts should be extended for nine months, until March 2018.

Note: That is longer than the optional six-month extension specified in the November 2017 deal.

Brent crude has rallied +$1.20 to +$52.04 a barrel, while U.S light crude (WTI) is up +$1.18 at +$49.02 a barrel.

Note: Global inventories remain high, and the output from other producers, especially the U.S is rising, which is keeping prices below the psychological +$60 some OPEC members would like to see.

OPEC and non-OPEC countries meet to decide policy on May 25 in Vienna

Data on Friday showed that U.S energy firms added oil rig's for a 17th consecutive week, extending a 12-month drilling recovery.

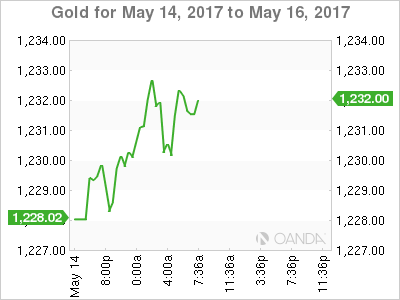

Gold prices have edged higher on weaker-than-expected U.S data and a missile test by North Korea over the weekend pressured the dollar. Spot gold is up + 0.3% at +$1,232.45 per ounce. The yellow metal rose +0.3% on Friday.

3. Global yields on the move

Friday's disappointing U.S data (Retail Sales and CPI) has fixed income dealers trimming the odds for a Fed hike next month. Fed fund futures currently see a +70% chance of a hike, down from +83% Friday morning.

The yield on 10-year Treasury notes has backed +1 bps to +2.34%, after dropping -6 bps Friday when the weaker-than-expected CPI report buoyed bond prices.

Elsewhere, yields on Aussie 10's lost -5 bps to +2.59%. Benchmark yields in France and Germany rose +1 bps.

A rise in German yields above the psychological +0.5% mark is expected to meet with strong resistance, however, the strengthening economic development in the eurozone and the robust outlook may make ECB monetary policy normalization conceivable and even sooner than later.

4. "Big" dollar losing some love

Last weekend's G7 Finance Ministers and central bank meeting did not provide any surprises.

G7 reiterated its pledge on FX - "that excess volatility was bad for growth" and declared their commitment against "competitive devaluation."

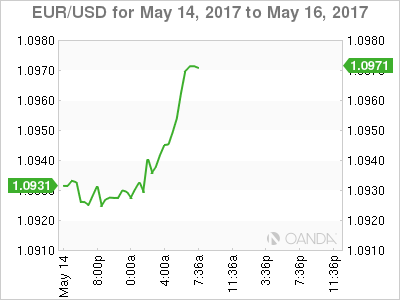

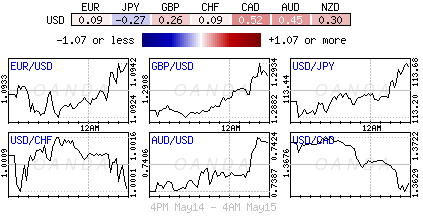

Ahead of the U.S open, the FX markets are somewhat subdued with the USD facing resistance from further underwhelming data. The EUR remains steady trading atop of €1.0940, while USD/CHF has dipped below parity to $0.9989. The pound continues to flounder below £1.2950, while USD/JPY is little changed at €113.42.

Petro-currencies (NOK, CAD, MXN) have all got a boost from higher crude oil prices overnight.

Note: Turkish markets will watch President Erodgan's meeting with U.S President Trump tomorrow. It's considered crucial for geopolitical developments in the region- USD/TRY is last down -0.3% at $3.5618.

5. China's Xi and data

China President Xi said on Sunday that China would "strike a balance between financial stability, gradual deleveraging, and steady economic growth, noting that China was capable of maintaining stability in its financial markets."

Such market-friendly language helped offset economic concerns triggered by news that China's factory output and fixed asset investment growth cooled more than expected last month.

China April Industrial Production: y/y - +6.5% vs. +7.0%e, while Retail Sales: y/y - +10.7% vs. +10.8%e.

China National Bureau of Statistics (NBS) said that economic growth was still within a "reasonable range," yet; overcapacity remained a serious problem in some sectors.

Daily Technical Analysis: GBP/NZD Uptrend Intact

The GBP/NZD has almost closed the retail gap with a slow grind towards D L3 that stands in a confluence with the gap. At this point the price is getting close to the POC zone 1.8685-1.8705 (D L3, Retail gap close, 78.6, bullish order blocks, ATR pivot). As long as 1.8608 support holds we might see a rejection towards 1.8870 ATR/D H4 confluence. Only above 1.8880 the price might go for a full retest of 1.8969.

Technical Outlook: AUDUSD – Break Of Key Barriers At 0.7461/67 Needed To Extend Recovery

The Aussie extended recovery from 0.7329 double-bottom where weekly cloud base contained broader bearish action.

The pair tested daily Tenkan-sen barrier at 0.7435 after strong bullish acceleration on Monday took out pivotal barriers at 0.7406/13 (falling 10SMA / Fibo 38.2% of 0.7554/0.7372 downleg).

Recovery needs to extend above daily Tenkan-sen and also break above next pivots at 0.7461/67 (falling 20SMA / Fibo 38.2% of 0.7554/0.7372 downleg / daily Kijun-sen) to generate stronger bullish signal and sideline risk of limited correction and fresh downside, as overall structure is bearish.

Close above those barriers would signal stronger recovery towards 0.7500+ zone.

Otherwise, risk of lower top and fresh bear-leg would remain in play while recovery stays limited under 0.7461/67 pivots.

Res: 0.7440, 0.7467, 0.7500, 0.7554

Sup: 0.7406, 0.7383, 0.7364, 0.7329

GOLD Golden Cross, SILVER Short-Term Bounce Above $16.00, CRUDE OIL Strong Upside Pressures.

GOLD Golden cross.

Gold seems on its way back up. Hourly support is now located at 1195 (10/03/2017 low). Expected to show further upside pressures.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Short-term bounce above $16.00.

Silver's bearish pressures are still lively despite short-term consolidation. Strong support is given at 15.63 (20/12/2017 low). Closest support is given at 16.20 (04/05/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high). Expected to see continued bearish pressures.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Strong upside pressures.

Crude oil continues to bounce on shortsqueeze move. Support is given at a distance 43.76 (05/05/2017 low). Demand is very strong and crude oil is set to be monitor again the $50 mark.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

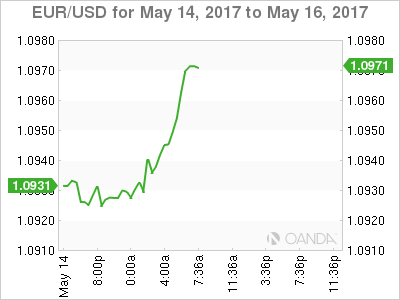

EUR/USD – Euro Under Pressure As Euro Closing In On 1.10

The euro has edged lower in the Monday session, as EUR/USD trades at 1.0970. On the release front, there are no eurozone indicators on Monday. In the US, today’s highlight is the Empire State Manufacturing Index. On Tuesday, we’ll get a look at Eurozone Flash GDP and German ZEW Economic Sentiment. The US will release Building Permits and Housing Starts.

The first quarter of 2017 has seen improved numbers in the euro area, largely due to strong numbers from Germany, the locomotive of the eurozone. Germany’s economy expanded 0.6% in the first quarter, compared to a 0.4% gain in Q4 of 2016. What was particularly encouraging was that the expansion was broadly based, with strong consumer and state spending, and an upsurge in the construction and manufacturing and export sectors. However, inflation levels continues to recede, after some strong numbers in the first quarter. In April, German Final CPI dropped to 0.0%, marking a 3-month low. This trend has also characterized inflation in the eurozone, as weaker inflation levels has lessened pressure on the ECB to tighten monetary policy.

The EU released its Spring 2017 Economic Forecast, and the report gave the eurozone a passing grade. The report noted that the European economy is in its fifth year of recovery, and forecast eurozone GDP growth of 1.7% in 2017 and 1.8% in 2018. On the inflation front, the report stated that inflation had risen in recent months, but this was mainly due to an increase in oil prices. Still, inflation was expected to reach 1.6% in 2017 and 1.3% in 2018, compared to just 0.2% in 2016. Stronger growth has led to lower unemployment, and the report projected that eurozone unemployment rate would drop to 9.4% in 2017 and 8.9% in 2018. At the same time, economic risks remain tilted to the downside, including US economic and trade policy under President Trump, the European banking sector and Brexit. This forecast was considerably more optimistic than the Winter 2017 forecast, as is apparent from the captions in the press releases for these two reports: The Winter forecast was entitled “Navigating through choppy waters”, while the caption for the Spring forecast reads “Steady growth ahead”.

US consumer spending and inflation numbers improved in April, but still fell short of estimates. CPI came in at 0.2%, short of the estimate of 0.3%. Core CPI, which excludes the most volatile items, posted a small gain of 0.1, shy of the estimate of 0.2%. Retail Sales came in at 0.3%, compared to the forecast of 0.5%. Retail Sales rose 0.4%, short of the estimate of 0.6%. Consumer confidence remained strong, as the reading of 97.7 beat the forecast of 97.0 points. These numbers underscored a troubling trend where strong consumer confidence has failed to translate into increased consumer spending.

Donald Trump has been embroiled in a number of controversies in his short presidency, but the political earthquake he has now stirred could become political quicksand for the new president. Trump abruptly fired FBI director James Comey last week, stunning lawmakers on both sides of the aisle in Congress. Comey, who has been conducting an investigation into possible collusion between Trump and Russia during the presidential campaign, clearly has been a thorn in Trump’s side. The White House has claimed that it fired Comey over his handling of an email scandal involving Hillary Clinton, but the move has been roundly condemned by the Democrats, and some key Republicans have also voiced opposition as well. The firestorm could heat up further, with calls in Congress to appoint a special prosecutor into Trump’s connections with Russia. Has Trump gone one step to far? This latest controversy could cause some jitters among investors and hurt the US dollar.

EUR/JPY Sideways Price Action, EUR/GBP Ready For Further Decline, EUR/CHF Fading Below 1.1000.

EUR/JPY Sideways price action.

EUR/JPY's bullish run has stalled below range resistance at 124.59 (07/05/2017 high), Hourly support is given at 122.93 (05/05/2017 low). Major support is given at 114.90 (18/04/2017low). Expected to see further renewed buying pressures towards 125.00.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Ready for further decline.

EUR/GBP is trading lower. The technical structure remains negative as long as the resistance at 0.8530 (25/04/2017 low) holds. Expected to show continued weakness until support given at 0.8304 (05/12/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level

EUR/CHF Fading below 1.1000.

EUR/CHF's volatility is getting stronger. Resistance given is given at 1.0978 (09/05/2017 high). Despite the sharp increase and the recent bullish breakout which is very likely psychological, we believe that the medium-term pattern suggests us to see at some point renewed bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

USD/CHF Bouncing Back Lower, USD/CAD Weakening, AUD/USD Bouncing Within Symmetrical Triangle.

USD/CHF Bouncing back lower.

USD/CHF has paused after sharp reversal off 1.0107 high (10/04/2017 high). Support located at 1.0049 (10/05/2017 low) has been broken. Expected to consolidate around parity.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Weakening.

USD/CAD has declined after failing to reach 1.3800 before bouncing back. Hourly support can be found at 1.3411 (24/04/2017 high) then 1.3353 (20/01/2017 high). Expected to show bearish pressures as the pair remains broke support at 1.3530 (27/04/2017 low).

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Bouncing within symmetrical triangle.

AUD/USD has paused above key support at 0.7339 (intraday low). As long as prices remain below the resistance at 0.7608 (17/04/2017 high), the short-term technical structure is negative. Key resistance stands at 0.7681 (30/03/2017 high). Expected to show further weakness.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Medium-Term Bullish, GBP/USD Sideways Price Action, USD/JPY Consolidation Phase.

EUR/USD Medium-term bullish.

EUR/USD is trading higher towards resistance at 1.1023 (07/05/2017 high). Stronger support is now given at 1.0682 (21/04/2017 base) and key support can be found at 1.0494 (22/02/2017 low). Expected to reach 1.10.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Sideways price action.

GBP/USD is trading mixed. Hourly resistance is given at 1.2989 (07/05/2017 high). Hourly support can be found at 1.2757 (21/04/2017 low). An unlikely break of this support would indicate further weakness. Expected to push higher.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Consolidation phase.

USD/JPY is pushing higher since the pair broke resistance given at 112.20 (31/03/2017 high). Hourly support can be found at 113.86 (11/05/2017 low). Stronger support is located at 108.13 (17/04/2017 low). Other key supports lie at a distant 106.04 (11/11/2016 low). Expected to show continued bullish pressures after this consolidation phase.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

Greenback Slides As US Data Disappoints

Lacklustre US data puts investors on their toes

The last batch of US data came on the soft side and called into question the actual Fed’s rate path. Indeed, inflationary pressures eased for a third month a row in April with headline CPI printing at 2.2% and the core one, which excludes the most volatile components, moving below the 2% threshold to 1.9%.

April’s retail sales were also weaker than expected as the main measure missed the median forecast of 0.6%m/m to print at 0.4%. Core retail sales rose 0.3% m/m versus 0.5% expected and 0.3% in the previous.Even though the data may just signal a temporary slowdown of the US economy, it definitely ruled out a strong economic rebound in economic activity.

With President Trump’s reforms failing to materialise and weaker than expected inflation, the market is readjusting expectations for the pace of monetary tightening. The entire US treasury yield curve shifted lower on Friday and dragged the greenback down. The dollar index is down 0.66% since Friday and continued to move south on Monday morning.

The single currency and the Swiss franc partially erased last week’s losses and rose 0.75% and 0.83% respectively over the last two trading days. With the June rate hike already priced-in and assuming that Trump’s fiscal plan gets delayed further, we believe that the risk is mostly on the downside for the dollar for now.

SNB’s massive intervention continues

During the French Presidential elections, it was clear that the Swiss National Bank was selling franc to prevent any safe haven effect. Uncertainties regarding the outcome (at least before the first round) drove the Swiss institution to intervene massively.

The Swiss currency is now back on the US Treasury watch of currency manipulators and the Finance Ministry declared that the Central Bank is only trying to limit the overvaluation from the franc and not gain a competitive advantage, which is - in the end - the same thing. It is becoming tougher for the SNB to convince markets about the exact nature of its intervention.

The Swiss foreign exchanges are now larger than the Swiss GBP and today’s total sight deposits have largely increased by 2 billion CHF. We continue to be bullish on the CHF as upside pressures on the currency should continue. Datawise, the trade balance is still largely positive and is even increasing.

Next week, export data for April will be released and they are expected to print at a great + 2.5% m/m (out of inflation) while imports should continue to decline. It is clear that the Swiss economy resists well, which leaves some room for the SNB to intervene.

China see marginal data weakness

Data from China came in on the softer side but after a significantly strong 1Q print. However, there are further indications that growth in China will continue to moderate. Chinese retail sales rose to 10.7% y/y against 10.8% expected, indicating that consumption remains solid. Fixed asset investment increased 8.9% y/y against 9.1% expected while industrial production slipped to 6.5% y/y against 7.0% expected.

Overall, these reads are consistent weaker trade data and softer April manufacturing PMI. While fixed asset growth fell marginally due to weak manufacturing investment, the number remains supportive.

Clearly efforts by China's central regulatory agencies and local governments to tighten policy are working. We view the current slowdown as managed decelerations to combat worries in shadow banking, real estate and local debt financing rather than the start of a broader fall in economic condition. China's Premier Li has continued to state that China will further put into place conservative monetary policy to lower financial risk as the highest priority. Interestingly, this is counter to what we are hearing from the US, where the Trump administration is attempting to hyper-accelerate the US economy with pro-growth policy (despite solid growth and full employment).

We remain optimistic on the China story and see key opportunities in Asian assets. On the FX side we are constructive on EM Asia against JPY as lower interest rates, higher growth, less protectionism risk and general positive risk-taking environments will support the currencies. USDJPY might have peaked failing to break 114.38 on three occasions; suggesting marginal downside corrections; however, JPY has further weakness against regional peers (THB, INR, IDR and KRW).

Technical Outlook: USDJPY – Bullish Bias Above 100 SMA/Daily Cloud

Strong two-day pullback from double upside rejection at 114.36 found support at 113.07, being contained by rising daily Tenkan-sen and kept intact key supports at 112.95/78 (100SMA /daily cloud top).

Fresh recovery rally on Monday was so far capped by Fibo barrier at 113.75, but immediate downside risk has been sidelined.

Overall bullish bias is expected to keep focus at the upside while the price holds above 100SMA/daily cloud top supports, with break and close above 113.75 (Fibo 76.4% of 115.49/108.11) seen as supportive factor for renewed attempts above 114.00 barrier and re-test of pivotal barrier at 114.36 (10/11 May peaks).

Conversely, increased risk of stronger correction of 108.11/114.36 rally could be expected on violation of 112.95/79 pivots.

Res: 113.75, 113.93, 114.36, 114.87

Sup: 113.31, 113.07, 112.95, 112.79