Sample Category Title

US Import Prices Surge 0.5% In April

.

'In April, higher prices for nonfuel industrial supplies and materials; foods, feeds, and beverages; and each of the major finished goods categories all contributed to the overall rise in nonfuel prices.' - US Bureau of Labour Statistics

The US Import Price Index managed to post a larger-than-expected gain over the course of April, official data revealed on Wednesday. The US Bureau of Labour Statistics reported that the price index for US imports tacked on 0.5% in April, following the upwardly revised 0.1% uptick registered in the preceding month and beating analysts' expectations for a 0.2% increase. April's surge was mainly driven by higher fuel prices, which rose 1.6% over the month of April, following a 0.9% drop observed in March. A 1.6% hike in prices for petroleum and a 4% advance in natural gas prices appeared to be the main contributors to the increase in fuel prices. In the meantime, the price index for imports excluding fuel rose 0.3% in April, following an increase of 0.2% posted in the previous month. As reported by the US BLS, higher prices for food and beverages, industrial supplies and materials as well as an uptick in feeds managed to bolster the overall acceleration in nonfuel prices. Over the year, prices for US imports soared 4.1% in April, while export prices inched 3% higher over the same period.

RBNZ Holds Benchmark Rate At Record Low Of 1.75%

'…the growth outlook remains positive, supported by on-going accommodative monetary policy, strong population growth, and high levels of household spending and construction activity.' - Reserve Bank of New Zealand

Yet again, the Reserve Bank of New Zealand left its monetary policy unchanged at its May meeting on Wednesday in support of inflation and steady economic growth. The Monetary Policy Committee voted to hold the official cash rate at a record low of 1.75%, where it has stood since November last year, satisfying market analysts who are eyeing a gradual tightening beginning not earlier than at the start of 2018. In the May statement, the RBNZ highlighted that the monetary policy is likely to remain accommodative until late 2019, however, economists worldwide argued that this would be difficult to justify, as inflation continues to spike up. The CPI was up 2.2% in the Q1 of 2017, much higher than the 1.5% projected by the Central Bank. Since 2011, it was the first time when the RBNZ has reached the mid-point if its inflation target range of 1-3%. Meanwhile, data released last week suggested long-run inflation expectations across the business sector also inched higher in the first quarter. Overall, the RBNZ Governor Graeme Wheeler remained upbeat on the country's economic outlook, though still warned that major challenges remain emplace.

EUR/USD Analysis: Stalls Below 1.09

'Traders continue to be wary of the EUR as it approaches the 1.0820 area that was the opening level after the first round of French presidential voting.' – Alexandria Arnold and Dennis Pettit, Bloomberg

Pair's Outlook

On Thursday morning the common European currency traded between the 1.0860 and 1.0880 levels against the US Dollar. From a technical perspective the currency exchange rate was still set to decline down to the support cluster, which surrounds the 1.0830 mark. However, due to recent US Dollar weakness caused by political events in the country the currency pair has remained just below the 1.09 level. Markets are still expecting the Euro to resume its decline, as the European Central bank is set to continue its stimulating monetary policy.

Traders' Sentiment

SWFX traders remain bearish, as 60% of open positions are short. In addition, 65% of trader set up orders are set to sell the Euro.

GBP/USD Analysis: Attempts To Break Away From Weekly PP

'The improved optimism regarding the macro fundamentals are supportive of a stronger US dollar in the current circumstances.' – London Capital Group (based on Investing.com)

Pair's Outlook

The Cable remained completely flat on Wednesday, although some upside volatility was registered. The Pound has been consolidating against the US Dollar for quite some time now, but with the bullish momentum moderately prevailing. According to technical studies, the Sterling should continue outperforming the US Dollar, with demand at 1.2934, represented by the weekly PP, remains sufficient to keep the pair afloat, and no resistance is preventing the exchange rate from climbing over the 1.30 level. The overall ceiling for now is the area sirca 1.3130, where a number of supply levels coincide with the ascending channel's upper boundary.

Traders' Sentiment

Market sentiment remains unchanged, with 51% of all open positions being short for the fifth consecutive time.

USD/JPY Analysis: Set For Another Rally

'With this [expectations of the newly-elected South Korean President to negotiate with North Korea] in the background, as well as the present uncertainty in the U.S., the dollar will trade heavily today below the 114-yen level.' – Daiwa Securities (based on Reuters)

Pair's Outlook

The USD/JPY currency pair surprised with its performance once again, having breached the immediate resistance, thus, stabilizing above 114.00. However, due to the recent almost constant three-week rally, a bearish correction is bound to take place sooner or later, but according to technical indicators—today is no such case. With the weekly and the monthly R2s now providing immediate support, the Buck has the opportunity to even put the 115.00 level to the test, as the upper Bollinger band marks the possible intraday high, as well as the a psychological resistance area, which the given pair failed to pierce back in March.

Traders' Sentiment

There are 66% of traders holding short positions (previously 65%), while 51% of all pending orders are to acquire the US Dollar.

Gold Analysis: Remains Above Resistance

'From a pure technical-fundamental aspect, everybody would be eying $1,200 as the next level of support, but I think $1,215 support here is not out of the question.' – Spencer Campbell, Kaloti Precious Metals (based on Reuters)

Pair's Outlook

Due to fundamental events in the US the price of the yellow metal remained above the 1,220 mark on Thursday morning. The future course of the commodity price is unclear, as both from a technical and fundamental perspective the yellow metal's price is being squeezed. The metal keeps finding support in the support cluster below it, which has forced the bullion into breaking short term descending channel patterns that were reviewed in the Trade Pattern Ideas section of Dukascopy Bank. Due to that reason it is possible that a surge is about to occur up to the 1,242 mark in the medium term.

Traders' Sentiment

Trader open positions remain neutral. However, 66% of trader set up orders are set to buy the bullion.

GBP Holds Ahead of BoE Announcements

Today will see the release of a set of UK economic data for March at 09:30 BST, including manufacturing production, industrial production, and trade balance. This will be followed by the Bank of England's (BoE) interest rate decision and monetary policy minutes at 12:00 BST and the NIESR GDP estimate (Feb to April) at 13:00 BST.

Recent UK economic data has been soft lowering market expectations for a rate hike. The general election will be held on June 8 and, with the Brexit procedure ongoing, the BoE is unlikely to take any actions at least before the election result; therefore, they are likely to keep policies steady until the Brexit negotiation deal has a clear outline.

GBP/USD has rallied approximately 3% since Theresa May's announcement of a snap general election on April 18th. On Monday May 8th GBP/USD hit a 7-month high of 1.2988. The bulls failed to breach the significant psychological level at 1.3000 since then. Markets seem to be taking a cautious stance ahead of the BoE announcements.

The BoE's announcement will likely cause a move to GBP and GBP crosses. With a hawkish comment, it will likely cushion GBP/USD. Conversely, with a dovish comment, we will likely see a correction downward.

ECB Governor Draghi stated on Wednesday that “the Eurozone economy is becoming increasingly solid and downside risks have further diminished”. However, it is too early for the ECB to remove QE as inflation pressure continues to be subdued.

Although the Eurozone recovery is sound, with the expectation ECB is not yet going to remove QE, EUR/USD only rebounded around 20 points during the speech, followed by a retracement due to the strengthening of USD. EUR/USD hit a 2-week low of 1.0852 after Draghi's speech.

German Q1 GDP first reading will be released at 07:00 BST, Friday May 12th. It will be followed by a set of crucial US data for April at 13:30 BST including retail sales, core retail sales, CPI and core CPI.

The German unemployment rate has seen a downtrend since 2009. The global economic recovery helping to boost German exports. German business confidence for April hit a 6-year high indicating German companies regard the economic outlook as optimistic.

German GDP has been oscillating in the range between 1.3% – 3.1% in 2016. The consensus for Q1 GDP is 1.7%, with a better-than-expected reading it will likely provide further support for EUR and the DAX index.

The Dax index hit a record high of 12834.45 on May 5th, lifted by market expectations on Macron's victory. It has seen a 44.2% surge since February 2016.

Sterling Consolidates Ahead Of BoE’s ‘Super Thursday’

Today, it's 'Super Thursday' in the UK. That means that besides the BoE rate decision and the meeting minutes, we will also get the quarterly Inflation Report, which Governor Carney will present at a press conference after the gathering. The BoE added a hawkish touch the last time it met, indicating that 'some members' would consider a reduction in stimulus should there be any further upside news on the prospects for growth or inflation. On top of that, Kristin Forbes dissented the decision to remain on hold, favoring an immediate rate hike instead. Since that gathering, data showed that the core CPI rate rose further, but GDP growth slowed significantly in Q1.

Therefore, we think that the BoE is likely to stand pat, erase the hawkish touch it added the last time, and reiterate that policy can respond in both directions. We believe that policymakers will place more emphasis on supporting economic growth, and repeat that above-target inflation entirely reflects the drop in sterling and is thus transitory. As such, although Forbes is likely to dissent again, the overall tone of the Committee may be somewhat more concerned than previously. In this case, sterling could reverse some of its latest gains. In addition, there is the prospect for the GDP forecasts to be revised lower.

GBP/USD has been trading in a consolidative manner recently, staying between the support of 1.2900 (S1) and the psychological round figure of 1.3000 (R1). A cautious committee today may be an excuse for some profit taking on existing long positions, which could cause the rate to correct lower. We believe that a dip below 1.2900 (S1) may open the way for a test near the key zone of 1.2850 (S2). Nevertheless, we still see an uptrend on the 4-hour chart and as such, we would treat such a slide as a corrective setback.

The key risk to our view for a pullback is the prospect that more than one MPC members vote for a rate hike. Something like that could indicate that there is increasing support among the Committee for such action, thereby raising speculation for a rate hike in coming meetings. In such a case, GBP/USD could surge, break above the psychological level of 1.3000 (R1), and perhaps aim for the next resistance of 1.3050 (R2).

RBNZ keeps the door for further easing open; NZD tumbles

Overnight, the RBNZ kept its policy rate unchanged, but did not communicate a more optimistic bias as many market participants may have anticipated. The statement accompanying the decision made it clear that although domestic economic data are improving, some of the progress is transitory, particularly in the inflation outlook. With regards to the Kiwi, the Bank noted that its 5% decline since February is encouraging, and if sustained will help to rebalance the growth outlook. Perhaps most importantly, policymakers kept the door for further easing wide open, indicating that numerous uncertainties remain and that policy may need to adjust accordingly. Given that this may have come as a surprise to NZD-traders, the Kiwi plunged. We think that the currency could remain under pressure for a while, perhaps until the recent concerns regarding a slowdown in Chinese growth ease a little bit.

NZD/USD traded higher heading into the meeting, to hit resistance marginally above the 0.6940 (R1) barrier just a few hours before the decision. At the time of the decision though, given the disappointing tone of the RBNZ, the pair plunged and broke below the 0.6880 (R2) level. For now, we believe that the pair may correct some of that steep fall, and perhaps test the 0.6880 (R2) territory as a resistance this time. If the bears manage to take advantage of such a corrective rebound, we would expect them to aim for another test near 0.6840 (R1), where a decisive dip may pave the way for the 0.6780 (S1) support area.

As for the rest of today's highlights:

During the European day, Sweden's CPI data for April are due out. The forecast is for both the headline and the underlying inflation rates to have moved higher, which could reverse some of SEK's latest losses.

As for the UK economic data, we get the trade balance and industrial production for March, but these are likely to be overshadowed by the BoE meeting.

From the US, we get PPI data for April and initial jobless claims for the week ended on the 5th of May.

Besides BoE Governor Carney, we have three more speakers on the agenda. From the ECB, we will hear from Vice President Vitor Constancio and Executive Board member Peter Praet. In the US, comments from the influential New York Fed President William Dudley will be in focus.

GBP/USD

Support: 1.2900 (S1), 1.2850 (S2), 1.2770 (S3)

Resistance: 1.3000 (R1), 1.3050 (R2), 1.3125 (R3)

NZD/USD

Support: 0.6780 (S1), 0.6680 (S2), 0.6620 (S3)

Resistance: 0.6840 (R1), 0.6880 (R2), 0.6940 (R3)

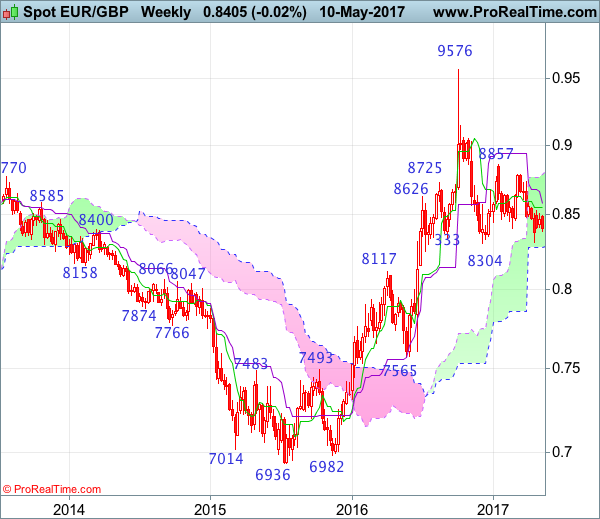

EUR/GBP Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: N/A

• ime of formation: N/A

• Trend bias: Near term up

Daily

• Last Candlesticks pattern: Hammer

• Time of formation: 3 Feb 2016

• Trend bias: Up

EURGBP – 0.8445

The single currency met resistance at 0.8509 late last week and has retreated, suggesting the rebound from 0.8312 has possibly ended at 0.8531 and consolidation with downside bias is seen for further fall to 0.8351 support, however, a daily close below there is needed to add credence to this view and bring resumption of recent decline for retest of 0.8312. Looking ahead, only a drop below 0.8304 support would revive bearishness and signal early downtrend has resumed for weakness to 0.8270-75, then 0.8250 but price should stay well above 0.8200-10.

On the upside, whist recovery to the Tenkan-Sen (now at 0.8447) cannot be ruled out, reckon said resistance at 0.8509 (last week’s high) would hold and bring another decline later. Only a break of said previous resistance at 0.8531 would shift risk back to upside for the rebound from 0.8312 low to bring retracement of recent decline towards 0.8592 resistance but a daily close above there is needed to signal recent decline has ended instead, bring further gain to the upper Kumo (now at 0.8623), then towards 0.8660-65, however, price should falter well below previous resistance at 0.8735, bring retreat later.

Recommendation: Hold long entered at 0.8400 for 0.8600 with stop below 0.8310.

On the weekly chart, as the single currency has retreated again after brief recovery to 0.8509, suggesting initial downside risk remains for weakness to 0.8350-55, however, as long as recent support at 0.8312 holds, consolidation with mild upside bias is seen for another rebound, above said resistance at 0.8509 would bring test of 0.8531, break there would bring test of the Tenkan-Sen (now at 0.8550) but break of resistance at 0.8592 is needed to signal the fall from 0.8857 has ended, then gain to 0.8675-80 would follow, however, as broad outlook remains consolidative, reckon upside would be limited to 0.8788 resistance, bring retreat later.

On the downside, although initial pullback to 0.8351 support cannot be ruled out, as long as minor support at 0.8351 holds, prospect of another rebound remains. A drop below 0.8351 would bring test of indicated support at 0.8304-12, once this level is penetrated, this would signal decline from 0.9576 top has resumed for retest of 0.8304 but only break there would extend the fall from 0.9576 top for retracement of medium term upmove to previous support at 0.8251, then 0.8200.

EURUSD Undergoing A Reversal From The Top, More Weakness May Follow

EUR/USD is undergoing an intraday drop form the high, which could mean that final wave C as part of wave Y) found a top at the start of this week and that the whole fourth wave correction since January of 2017 is completed. If so, then we will see a minimum three wave decline to unfold in the next trading sessions and a break beneath the previous minor wave four swing at 1.0844 level, that may cause the GAP at 1.080 to be filled.

EURUSD, 4H