Sample Category Title

Australia’s Retail Sales Drop For The Second Straight Month In March

For the 24 hours to 23:00 GMT, the AUD declined 0.11% against the USD and closed at 0.7383.

LME Copper prices declined 1.2% or $64.5/MT to $5466.0/MT. Aluminium prices declined 1.5% or $28.0/MT to $1879.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7361, with the AUD trading 0.3% lower against the USD from yesterday's close, on the back of disappointing retail sales data in Australia.

Early morning data showed that Australia's seasonally adjusted retail sales unexpectedly dropped 0.1% on a monthly basis in March, declining for the second consecutive month and confounding market consensus for a rise of 0.3%. In the prior month, retail sales had fallen by a revised 0.2%.

The pair is expected to find support at 0.7334, and a fall through could take it to the next support level of 0.7307. The pair is expected to find its first resistance at 0.7406, and a rise through could take it to the next resistance level of 0.7451.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Investor Confidence Jumped To A Nearly 10-Year High Level In May

For the 24 hours to 23:00 GMT, the EUR declined 0.46% against the USD and closed at 1.0923.

On the data front, the Euro-zone's Sentix investor confidence index rose more-than-expected to a level of 27.4 in May, notching its highest level since July 2007, as investors grew optimistic about the region's current economic outlook and as worries over political populism across the Euro bloc ebbed. The index had registered a reading of 23.9 in the prior month, while investors had envisaged for an advance to a level of 25.2.

Elsewhere, in Germany, the seasonally adjusted factory orders advanced 1.0% MoM in March, rising for second straight month and surpassing market expectations for a gain of 0.7%. Factory orders had registered a revised gain of 3.5% in the previous month.

In the US, data indicated that the labour market conditions index climbed to a level of 3.5 in April, after recording a revised rise of 3.6 in the previous month and compared to market expectations for an advance to a level of 1.0.

In the Asian session, at GMT0300, the pair is trading at 1.0926, with the EUR trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.0895, and a fall through could take it to the next support level of 1.0865. The pair is expected to find its first resistance at 1.0976, and a rise through could take it to the next resistance level of 1.1027.

Moving ahead, market participants focus on Germany's trade balance and industrial production data, both for March, slated to release in a few hours. Moreover, in the US, final wholesale inventories and JOLTS job openings, both for March along with the NFIB small business optimism index for April, will be eyed by investors.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

UK’s House Prices Fell For The First Time In 3 Months In April

For the 24 hours to 23:00 GMT, the GBP declined 0.16% against the USD and closed at 1.2937.

In economic news, UK's Halifax house prices unexpectedly dropped 0.1% in April, compared to market consensus for a rise of 0.1%. In the previous month, house prices had registered a flat reading.

In the Asian session, at GMT0300, the pair is trading at 1.294, with the GBP trading slightly higher against the USD from yesterday's close.

Overnight data revealed that the nation's BRC retail sales across all sectors advanced 5.6% YoY in April, compared to a drop of 1.0% in the prior month, while market participants were anticipating for a gain of 0.5%.

The pair is expected to find support at 1.2916, and a fall through could take it to the next support level of 1.2893. The pair is expected to find its first resistance at 1.2974, and a rise through could take it to the next resistance level of 1.3009.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.39% against the JPY and closed at 113.26.

In the Asian session, at GMT0300, the pair is trading at 113.18, with the USD trading 0.07% lower against the JPY from yesterday’s close.

Early this morning, data showed that Japan’s labour cash earnings surprisingly dropped 0.4% on an annual basis in March, after registering a 0.4% gain in the previous month.

The pair is expected to find support at 112.57, and a fall through could take it to the next support level of 111.95. The pair is expected to find its first resistance at 113.59, and a rise through could take it to the next resistance level of 113.99.

Moving ahead, investors await the Bank of Japan’s (BoJ) summary of opinions report, slated to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading A Tad Higher This Morning, Ahead Of Swiss Unemployment Rate Data

For the 24 hours to 23:00 GMT, the USD rose 0.94% against the CHF and closed at 0.9985.

On the data front, Switzerland's total sight deposits climbed to a level of CHF573.1 billion in the week ended 05 May, from CHF571.4 billion in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9982, with the USD trading marginally lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9912, and a fall through could take it to the next support level of 0.9841. The pair is expected to find its first resistance at 1.0022, and a rise through could take it to the next resistance level of 1.0061.

Ahead in the day, all eyes will be on Switzerland's unemployment rate data for April.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Canada’s Housing Starts Declined In March

For the 24 hours to 23:00 GMT, the USD rose 0.33% against the CAD and closed at 1.3695.

Macroeconomic data indicated that Canada's seasonally adjusted housing starts fell more-than-expected to a level of 214.1K in April, from a revised ten-year high level of 252.3K registered in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.3694, with the USD trading a tad lower against the CAD from yesterday's close.

The pair is expected to find support at 1.3645, and a fall through could take it to the next support level of 1.3596. The pair is expected to find its first resistance at 1.3738, and a rise through could take it to the next resistance level of 1.3782.

Going ahead, Canada's building permits data for March, slated to release later in the day, will garner a lot of market attention.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

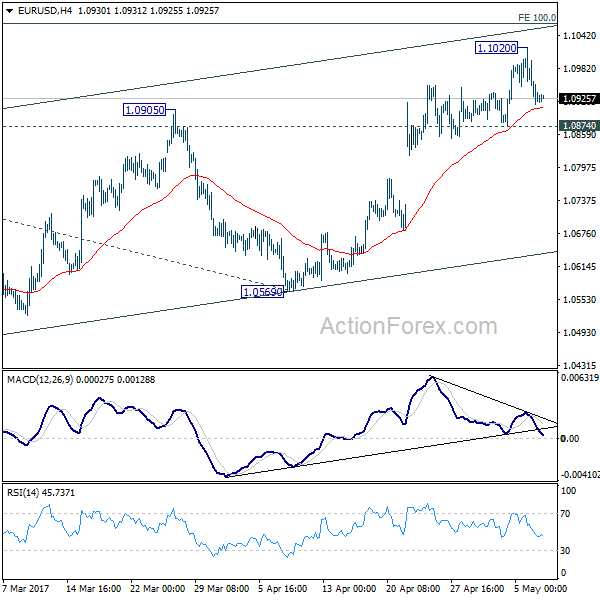

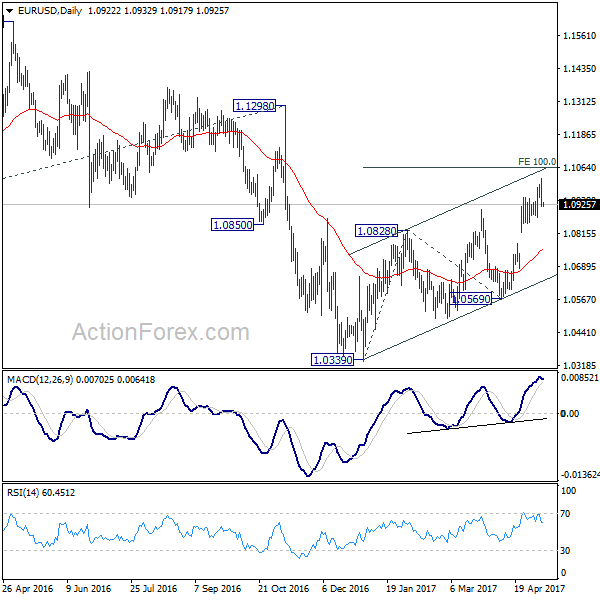

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0885; (P) 1.0953 (R1) 1.0991; More....

Intraday bias in EUR/USD remains neutral for consolidation below 1.1020 temporary top. Another rise will be expected as long as 1.0874 support holds. Above 1.1020 will extend current rally to 100% projection of 1.0339 to 1.0828 from 1.0569 at 1.1058. However, rise from 1.0339 is still seen as a corrective move. Hence we'd expect strong resistance from 1.1058 projection to limit upside and bring near term reversal. On the downside, break of 1.0874 support will turn bias back to the downside for 1.0569 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate long term reversal.

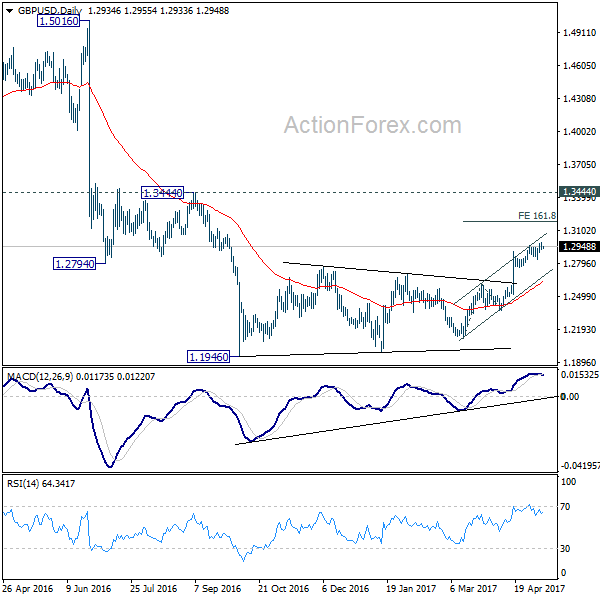

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2917; (P) 1.2952; (R1) 1.2976; More...

With 1.2830 minor support intact, further rise is still expected in GBP/USD. Current rally would target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2830 support will indicate short term topping. In such case, intraday bias will be turned back to the downside for 1.2614 support.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

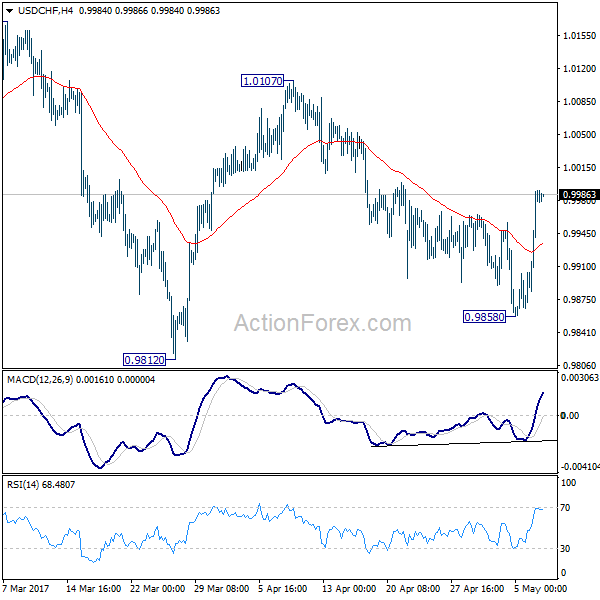

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9905; (P) 0.9948; (R1) 1.0030; More.....

Intraday bias in USD/CHF remains on the upside for 1.0107 resistance. Current development revived the case that correction from 1.0342 is already completed at 0.9812. Break of 1.0107 will bring a retest on 1.0342 high. Nonetheless, on the downside, break of 0.9858 will turn bias to the downside and target 0.9812 and below.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

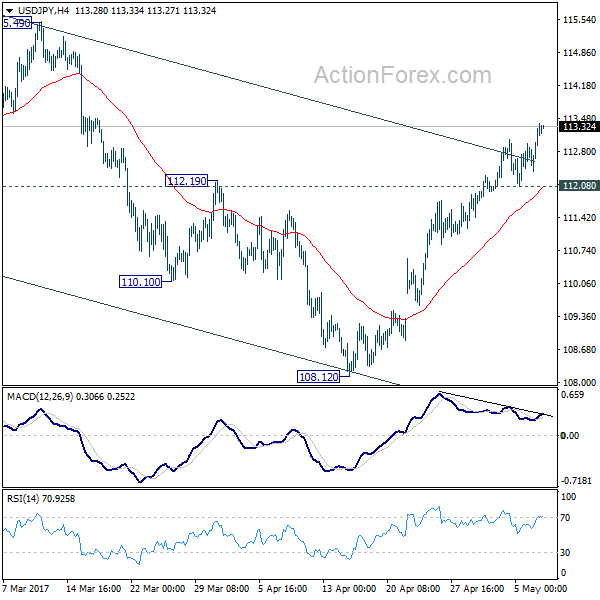

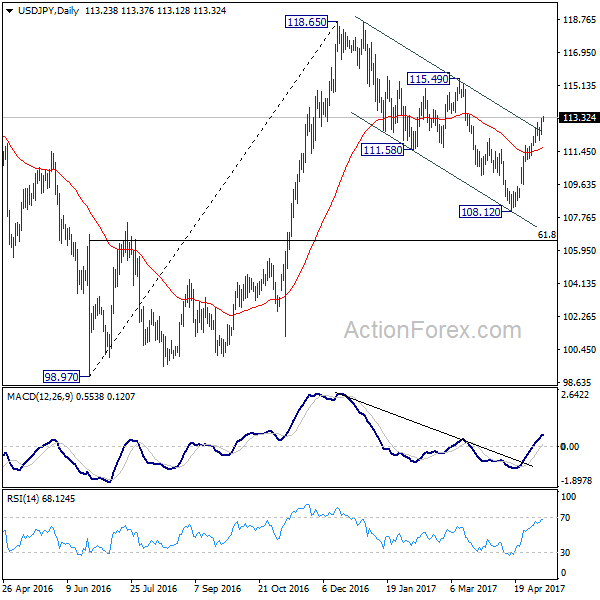

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.66; (P) 112.98; (R1) 113.56; More...

USD/JPY's rally resumed after brief consolidation and reaches as high as 113.37 so far. Intraday bias is back on the upside for 115.49 resistance. We're holding on to the view that corrective fall from 118.65 could be completed with three waves down to 108.12. Break of 115.49 will resume larger rally from 98.97 to 125.85 high. On the downside, break of 112.08 support is needed to indicate near term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.