Sample Category Title

Trade Idea Update: USD/CHF – Buy at 0.9910

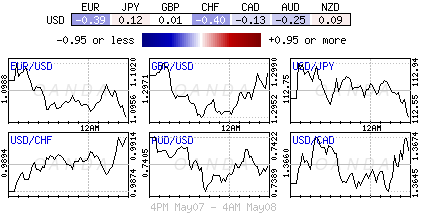

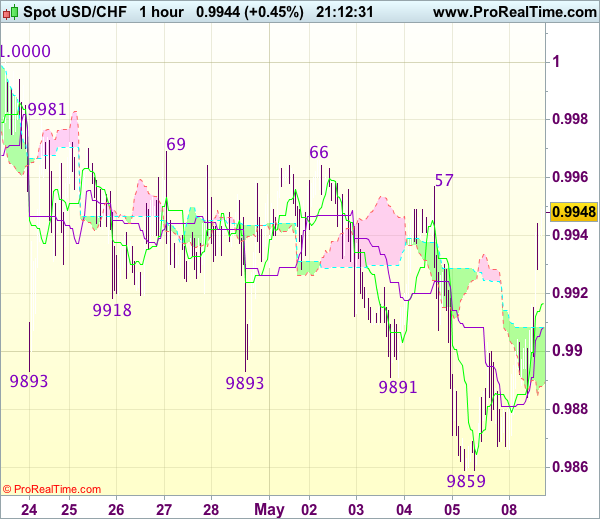

USD/CHF - 0.9952

New strategy :

Buy at 0.9910, Target: 1.0005, Stop: 0.9875

Position : -

Target : -

Stop : -

The greenback has staged another strong rebound in European session, suggesting a temporary low has been formed at 0.9859 and consolidation with mild upside bias remains for test of 0.9966-69 resistance, break there would add credence to this view and extend gain to indicated previous resistance at 1.0000-08 but only break there would signal recent decline from 1.0108 top has ended, then headway to 1.0025-30 would follow.

In view of this, we are looking to buy dollar on dips as 0.9900-05 should limit downside. Below 0.9880 would risk test of 0.9859, however, break there is needed to signal recent decline has resumed and extend weakness to support at 0.9831 and possibly towards 0.9800.

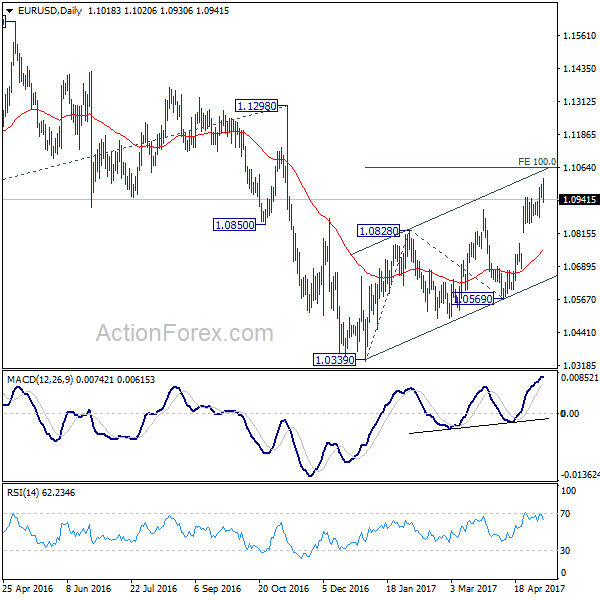

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0962; (P) 1.0981 (R1) 1.1015; More....

A temporary top is in place at 1.1030 with 4 hour MACD crossed below signal line. Intraday bias in EUR/USD is turned neutral for consolidation. Another rise will be expected as long as 1.0874 support holds. Above 1.1020 will extend current rally to 100% projection of 1.0339 to 1.0828 from 1.0569 at 1.1058. However, rise from 1.0339 is still seen as a corrective move. Hence we'd expect strong resistance from 1.1058 projection to limit upside and bring near term reversal. On the downside, break of 1.0874 support will turn bias back to the downside for 1.0569 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate long term reversal.

Euro Retreats after Initial Spike, Turning into Consolidation

After initial spike on news of French presidential election, Euro quickly retreated. While weakness in the common currency is limited so far, the price actions suggest that it's now in a near consolidation phase. And focus will move away from Euro to others. Two major focuses of the week are BoE Super Thursday and RBNZ rate decision. In particular, Sterling could ride on cross buying in EUR/GBP and a hawkish twist in BoE inflation report to extend recent rise. Meanwhile, Loonie and Aussie will look into development in energy and commodity markets. Canadian Dollar rebounds today with the help of recovery in oil price. However, WTI is starting to feel heavy again ahead of 47 handle. Overall, Dollar recovers broadly but the outlook is mixed so far as it's not in focus.

French parliamentary election in June watched

After the landslide victory, French President-elect Emmanuel Macron vowed to "fight with all my energy against the deepening divisions" in France. But now the focus will be quickly turned to parliamentary election in June. His EN Marche! movement basically has no experience with legislative election. And without a solid coalition, it would be very hard for Macron to push through his agenda. And Macron is also expected to push for reform in EU too. Talking about EU, German Chancellor Angela Merkel hailed that Macron "carries the hopes of millions of French people, and of many people in Germany and the whole of Europe". Belgian Prime Minister Charles Michel also failed that Macron's victory represented "a clear rejection of a dangerous project of European withdrawal."

More on French Election in Macron Becomes French President In Landslide Victory.

ECB Mersch: Risks almost back in balance

ECB Executive Board member Yves Mersch delivered an upbeat speech in Tokyo today. Mersch said that "the recovery in the euro area is gaining more and more traction." And, "the confirmation of a broadly balanced risk outlook for growth is within reach." He also noted that "political uncertainties and fragilities have consistently evolved in a positive fashion in Europe since the beginning of the year." And, if conditions continue to improve, "a discussion on policy normalization becomes warranted in the future." But for now, he emphasized that "the Governing Council is convinced of the need to continue an accommodative monetary policy stance without deviation from the announced measures under implementation to be expected."

Eurozone investor sentiment jumped to near 10 year high

Eurozone Sentix investor sentiment rose sharply to 27.4 in May, up from 23.9 and beat expectation of 25.2. That's also the highest level since July 2007. Current condition sub-index jumped to 34.5, up fro 28.8, highest since January 2008. Expectation sub-index rose to 20.5, up from 19.3, best since August 2015. Sentix noted that "before the decisive second round in the French presidential election, investors are once again assessing the economic situation in the euro zone improved. Investors are obviously expecting a decrease in political uncertainties in the euro zone." Separately, Germany factory orders rose 1.0% mom in March.

BoJ Kuroda: Faced challenging situation with inflation close to zero

In Japan, BoJ Governor Haruhiko Kuroda said during the weekend that inflation being close to zero for four years was "certainly a very challenging situation for central bank governors and central bankers in Japan." Nonetheless, he acknowledged that growth and price conditions have "greatly improved" and pledged to continue with "strong" monetary easing. Regarding exchange rate, Kuroda said that "in the case of Japan, exchange rates are affecting not much the trade balance but the corporate profit situation, through which domestic demand will fluctuate.

China exports and imports grew less than expected

China trade surplus widened to USD 38.1b in April, up from USD 23.9b and beat expectation of USD 35.3b. However, exports rose merely 8.0% yoy while imports rose 11.9% yoy. Both fell short of expectation of 10.4% yoy and 18.0% yoy respectively. In Yuan terms, trade surplus widened to CNY 262b, up from CNY 164b and beat expectation of CNY 197b. The data showed softening domestic demand that weighed down imports. There would likely be more downward pressure with the government's tightening policies.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0962; (P) 1.0981 (R1) 1.1015; More....

A temporary top is in place at 1.1030 with 4 hour MACD crossed below signal line. Intraday bias in EUR/USD is turned neutral for consolidation. Another rise will be expected as long as 1.0874 support holds. Above 1.1020 will extend current rally to 100% projection of 1.0339 to 1.0828 from 1.0569 at 1.1058. However, rise from 1.0339 is still seen as a corrective move. Hence we'd expect strong resistance from 1.1058 projection to limit upside and bring near term reversal. On the downside, break of 1.0874 support will turn bias back to the downside for 1.0569 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate long term reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| EUR | Second and Final Round of French Presidential Election | |||||

| 01:30 | AUD | Building Approvals M/M Mar | -13.40% | -4.00% | 8.30% | 8.90% |

| 01:30 | AUD | NAB Business Confidence Apr | 13 | 6 | ||

| 03:25 | CNY | Trade Balance USD Apr | 38.05B | 35.3B | 23.9B | |

| 03:25 | CNY | Trade Balance CNY Apr | 262B | 197B | 164B | |

| 05:00 | JPY | Consumer Confidence Index Apr | 43.2 | 44.3 | 43.9 | |

| 06:00 | EUR | German Factory Orders M/M Mar | 1.00% | 0.70% | 3.40% | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence May | 27.4 | 25.2 | 23.9 | |

| 12:15 | CAD | Housing Starts Apr | 214K | 220.0k | 253.7k | 253K |

| 14:00 | USD | Labor Market Conditions Index Change Apr | 0.4 |

Trade Idea Update: GBP/USD – Buy at 1.2905

GBP/USD - 1.2963

Original strategy :

Buy at 1.2905, Target: 1.3005, Stop: 1.2870

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2905, Target: 1.3005, Stop: 1.2870

Position : -

Target : -

Stop : -

As cable has maintained a firm undertone after last week’s late rally above previous resistance at 1.2965, adding credence to our bullish view that recent upmove is still in progress and may extend further gain to 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance), then towards 1.3040-50 which is likely to hold from here due to near term overbought condition.

In view of this, would not chase this rise here and would be prudent to buy cable on pullback as 1.2900-05 should limit downside and bring another rise later. Below 1.2880 would defer and risk weakness to 1.860-65 but only a break of said support at 1.0831 would signal a temporary top has been formed.

Trade Idea Update: EUR/USD – Sell at 1.0990

EUR/USD - 1.0950

Original strategy :

Sell at 1.0990, Target: 1.0890, Stop: 1.1025

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0990, Target: 1.0890, Stop: 1.1025

Position : -

Target : -

Stop : -

Although the single currency opened higher earlier today, lack of follow through buying and the subsequent retreat from 1.1025 suggest consolidation below this level would be seen and pullback to 1.0920 cannot be ruled out, break there would suggest a temporary top is possibly formed, bring correction to 1.0900 but support at 1.0875 should remain intact and bring rebound later.

In view of this, we are looking to sell euro on recovery as 1.0995-00 should limit upside and bring another retreat. Above said resistance at 1.1025 would abort and signal recent upmove from 1.0340 low has resumed for headway to 1.1050 but reckon upside would be limited to 1.1065-70 (61.8% projection of 1.0602-1.0951 measuring from 1.0851).

New Zealand’s Unemployment Data Unlikely to Change RBNZ’s Tone

Summary:

- In the quarter ending March 2017, New Zealand's unemployment fell to 4.9%

- The decline in the unemployment suggested stronger than expected job growth

- It is estimated that over 29,000 workers entered the workforce in the quarter ending March 2017

- New Zealand's labor participation rate continued to rise to 70.6% marking a record high

New Zealand's quarterly unemployment rate fell to 4.9% in the March 2017 quarter which reversed the increase from the previous quarterly unemployment rate of 5.2%. The drop in the unemployment rate came on firm job growth.

Data released by Statistics New Zealand last week showed that the employment rose by 1.2% over the quarter, with 29k workers entering the workforce. This was a strong jobs growth, higher than what was anticipated.

The labor force increased by 23k during the quarter ending March 2017 which came as the growth in the economy attracted more workers into the labor market. Further adding weight to this was the strong levels of migration as well which continued to attract workers, strengthening the labor force as a result.

New Zealand unemployment rate: 4.9%, Q1 2017

Combined, the above factors led to a consistent increase in the labor participation rate which rose to 70.6% and marked a record increase, up 0.1 percentage points from the previous quarter.

Most of the job gains came from part-time jobs which rose 3.1% on the quarter whereas full time jobs rose only 0.6%. Industry-wise, job gains were seen coming from hospitality and services sectors including accommodation and good services. The construction sector was also seen contributing to the labor market growth.

Despite the strong numbers, surprisingly the average hours worked fell 0.6% in the quarter following a strong increase in the previous quarter. Alongside the decline in average hours worked, wage inflation was also absent.

The prospects of the labor market in New Zealand continued to remain strong, according to the Quarterly Survey of Employment. Data showed that firms expect to see a modest pace of employment growth. Full time employment is expected to rise 0.4% while the filled jobs rose 0.3% on the quarter.

While labour demand continued to strengthen, this has not yet translated into stronger nominal wage growth. The private sector LCI index rose 0.4% in the quarter, leaving annual inflation on this measure at 1.5% (in line with expectations). Similarly, the broader QES measure of average hourly earnings rose 0.3% over the quarter.

RBNZ expected to keep OCR unchanged

The unemployment report was indeed a surprising report especially for policy makers on the stronger than expected jobs growth, but still, there is strong evidence of broad softness in the data especially when it comes to wage growth and unemployment rate.

However, in a separate report, the New Zealand job ads showed a 2.8% jump in April as the monthly growth continued to accelerate. Job ads were up 18% from a year ago in April suggesting that the underlying factors in the labor market continued to build up.

The Reserve Bank of New Zealand will be meeting this week on Wednesday and policymakers are unlikely to make any changes to their statement while also leaving the overnight cash rate unchanged at 1.75%. The markets are expecting the first rate hike from the RBNZ to come only next year, in 2018 currently.

However, that could change should inflation continue to rise in the coming quarters while on the unemployment front; wage inflation will remain a key component in assessing the pace of future rate hikes. While no changes to the OCR is expected this week, the RBNZ could remain neutral which could bode well for the New Zealand dollar in the short term.

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 112.68

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback opened higher earlier today, as dollar has retreated after faltering below last week’s high at 113.05, suggesting further consolidation below this level would be seen and pullback t 112.40 cannot be ruled out, however, reckon support at 112.09 would limit downside and bring another rise later. Above said resistance at 113.05 would confirm recent upmove has resumed and extend gain to 113.10-15 (61.8% projection of 108.13-111.78 measuring from 110.87) and 113.30 but reckon upside would be limited to previous resistance at 113.54 and price should falter well below 113.90-00.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 112.09 support would bring test of 111.96 but break of this level is needed to signal a temporary top has been formed at 113.05, bring correction to 111.73-78 (38.2% Fibonacci retracement of 109.59-113.05 and previous resistance), however, reckon 111.21-32 (previous support and 50% Fibonacci retracement) would contain weakness.

DAX Dips After Brief Bounce From Macron Win

The DAX has edged lower on Monday and is currently trading at 12,684.25. On Sunday, Emmanuel Macron easily defeated Marie Le Pen to win the French presidential election. On the release front, there are no major events out of the eurozone. There was some positive news in the eurozone, as German Factory Orders gained 1.0%, above the forecast of 0.7%. As well, Eurozone Sentix Investor Confidence climbed to 27.4, beating the estimate of 25.3 points. The indicator has now improved over four consecutive months, pointing to stronger confidence among investors and analysts. The improvement in confidence is linked to the stronger eurozone economy, as key numbers such as PMI reports continue to point to expansion in the manufacturing and expansion sectors.

There were no surprises in the French presidential election, as Emmanuel Macron cruised to victory. Macron won 64% of the popular vote, with Marie Le Pen taking 36%. Macron's margin of victory was larger than the polls predicted, and the DAX showed some gains immediately after the vote, but was unable to consolidate these gains. The markets had priced in a decisive Macron victory, so it's not surprising that the Sunday rally did not last. Although Macron certainly "won big", it should be noted that fully one third of French voters either abstained or voted a blank ballot as a protest vote. This means that Macron was viewed by many voters as a default choice, given that his opponent was the leader of the far-right and has been accused of being racist and xenophobic. The French elections now enter a new phase, with parliamentary elections slated for mid-June. Macron's En Marche! party is barely a year old and is unlikely to win a majority, which would mean a power-sharing setup in parliament, likely between Macron's party and the center-right. Similar to the presidential election, the parliamentary election promises to be full of uncertainty, and opinion polls during the election campaign will be important as fundamental releases and should be treated as market-movers.

Time to Focus on OPEC Now that France is Out of Sight?

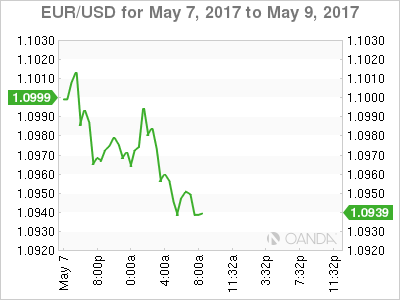

Investors have arrived in full force to exploit the opportunity to sell the Euro at its highest level since November 2016, with the EURUSD now appearing at risk to dropping back below 1.09 after briefly climbing above 1.10 when the markets opened for the week following confirmation of Macron becoming the new President of France.

While the lifeline of the Euro relief rally appears to be short-lived, I would go as far as to say that the Euro is heavily oversold at these levels and this is not linked to the headlines that Europe has defeated populism. Although political headlines are still overshadowing economic news when it comes to the global market theme of 2017, there is an improved economic sentiment around Europe that has been building recently as a result of significantly improved data.

Perhaps the reason for the heavy selling pressure on the Euro at present is due to expectations that the European Central Bank (ECB) will leave monetary policy accommodative, despite the stronger data being seen around Europe.

Time to shift focus to upcoming OPEC meeting?

Now that the French election is out of the way, investors should highlight May 25 in their calendar, because this is when the next OPEC meeting is scheduled in Vienna. Traders should expect and be prepared for shifts in volatility in both directions when it comes to the price of Oil, as the markets speculate over what the outcome of the meeting could possibly be.

I expect for producing nations to publicly talk up the prospects of an extension to the current production cut agreement made late in 2016, but this doesn't impact the underlying factor that the real fight OPEC has to deal with is a battle with US Shale production. There has been an obvious correlation that inventories from Shale production in the US have improved in recent months, which is surely going to be weighing heavily in the minds of all the Oil ministers from both OPEC and non-members when they sit at the table in a couple of weeks.

As always investors should prepare for the unexpected when it comes to OPEC meetings with recent history in mind that there have been unexpected surprises from past meetings. With that in mind there are at least two possible risk scenarios that investors should consider in the lead up to the May 25 event:

- While the organisation is currently committed to reducing output, that agreement expires next month. With the markets believing that the current collaboration will need to be extended, there is a risk that the markets will be caught off-guard with a decision to delay it, in order to prevent further US Shale production from reaching the landscape. Should OPEC and Non-OPEC agree to an increase in production for the second half of the year, a volume war could be on the cards with this providing sellers with heavy encouragement to begin pricing in the resumption of heavy selling momentum and a possible return to the historic lows for Oil.

- The other risk scenario that investors would be mindful to factor into consideration is that there is an agreement to throw in the towel and submit to extending not only the duration of the current agreement, but also cutting further output. Although this would be seen as OPEC declaring Shale victorious in the production war and would also further weaken the credibility of oil producers who, until just a few years ago, were in full control of global oil production, it would most probably achieve a stronger rebound in the price of Oil.

Basically what this could come down to is whether OPEC and Non-OPEC members are willing to lose face by accepting defeat to Shale in return for a further boost in revenue, or are they committed to prolonging their participation in this ongoing production war with Shale?

GBPUSD not ready to touch 1.30 yet?

The Pound is trading in a very narrow range against the Dollar at the beginning of the week as the spotlight shines on the French election result, and it looks like the British Pound is shying away from touching 1.30 for the first time since September 2016.

While the Pound benefitted from some impressive PMI results last week, it is possible that investors will shift their attention to the Bank of England (BoE) and the likelihood of inflation risks being highlighted when the latest inflation report is delivered this Thursday.

Quelle Surprise! Macron Wins, Back to Fundamentals

Monday May 8: Five things the markets are talking about

In yesterday's second round French Presidential vote, Emmanuel Macron convincingly beat National Front leader Marine Le Pen (66% vs. 34%).

Market reaction has been relatively muted with investors now turning their focus to global growth and corporate earnings after last week's robust U.S jobs report and the Fed's comments encouraging optimism in their economy.

Regarding Macron, the market will be looking ahead to next month's French Parliamentary elections and will also be questioning his ability to govern a divided populace.

This week, the Bank of England (BoE) meets Thursday and will issue its Quarterly Inflation Report. For the rest of Europe, most economic data releases center around industrial production and merchandise trade balances.

In Asia, China begins releasing last months merchandise trade balance and consumer and producer price indexes.

In the U.S, the focus will be on Friday's inflations expectations and retail sales.

1. Global equities mixed reaction

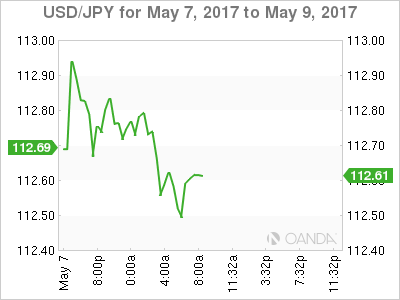

Overnight in Japan, stocks hit 17-month highs as the yen (¥112.64) stayed weak after Macron's win. The Nikkei share average soared +2.3%, while the broader Topix rallied +2.2%, the most since January 4.

In Hong Kong, the market also breather a sigh of relief after Macron's victory, the Hang Seng index ended up +0.4%, while the China Enterprises Index gained +0.6%.

In China, stocks extended their fall with the benchmark Shanghai Composite Index ending at its lowest close since mid-October, as investor fears over tightening regulations deepened. The blue-chip CSI300 index fell -0.7%, while the Shanghai Composite Index lost -0.8%.

In Europe, stocks are trading largely lower on profit taking following Macron's expected victory. The CAC leads the decliners down -0.6%, with the FTSE a tad higher.

In the U.S, stocks are set to open small down (-0.1%).

Indices: Stoxx50 -0.5% at 3642, FTSE flat at 7297, DAX -0.3% at 12676, CAC-40 -0.7% at 5393, IBEX-35 -0.4% at 11096, FTSE MIB -0.5% at 21376, SMI -0.3% at 8994, S&P 500 Futures 0%

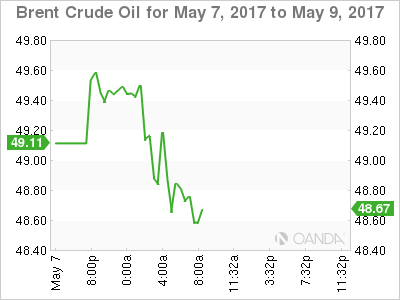

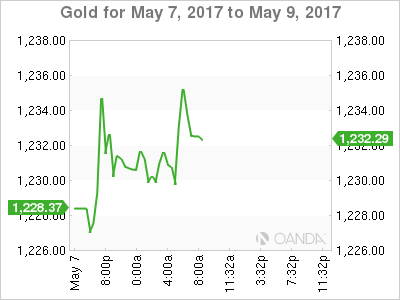

2. Oil prices rise on hope of production cuts, gold stronger

Oil prices are better bid ahead of the U.S open after the Saudi energy minister said an OPEC-led production cut scheduled to end in June would likely be extended to cover all this year, or even into 2018. However, the possibility of another increase in U.S drilling is capping gains.

Brent crude futures are trading at +$49.48 per barrel, up +38c, or +0.75% from Friday's close. U.S West Texas Intermediate (WTI) crude futures are at +$46.52 per barrel, up +30c, or +0.7%.

Note: A decision on whether to continue the production cuts is expected at OPEC's next official meeting on May 25.

U.S drilling continued to pick up last week, with the rig count climbing by +6 to 703.

Gold has climbed +0.2% to +$1,230.49 an ounce, mostly on bargain hunting. The yellow metal last week saw its biggest weekly percentage fall since November, ending -3.2% lower.

Note: Prices have fallen over -5% since hitting a five-month high of +$1,295.42 in mid-April.

3. Global yields see little movement

Macron's convincing win yesterday removes a big part of political risk in Europe, however, contained inflation expectations are expected to prevent a sell-off in Euro government bonds, particularly Bunds. German 10's are trading at +0.41%.

It's no surprise to see French and riskier eurozone assets slightly weaker on profit taking following Macron's victory – both had rallied in the run up to the vote. French government bonds (OAT's) have backed up +1 bps to +0.85%.

Elsewhere, the yield on 10-year Treasury notes are flat at +2.35%, while yields on Aussie debt have climbed +3 bps to +2.67%, extending their two-week slide in prices.

4. Euro gains are 'short-lived'

During the Asia session the markets initial reaction to Macron's Presidential win was "risk-on," this pushed the EUR to test well above the psychological €1.10 handle to €1.1042, its highest reading since early November as the political uncertainties in the eurozone decreased.

However, ahead of the U.S open the single unit has given up those gains on some aggressive profit taking, currently trading €1.0937.

With commodity prices also bouncing back on the potential of an OPEC cut in oil production is helping the AUD (A$0.7408) hold steady ahead of tonight's Aussie retail sales number. The yen is little changed at ¥112.68, near the lowest level in seven-weeks, while sterling (£1.2962) is still having difficulties making an assault on the £1.3000 handle.

5. German Manufacturing Orders Rise

Orders for Germany's important manufacturing sector rose by more than expected in March, +1.0% vs. +0.7%e m/m. The data adds to the evidence that growth in Europe's largest economy picked up speed in Q1.

Digging deeper, the increase in orders was led by strong foreign demand for German manufacturing goods, particularly from other eurozone countries – foreign orders jumped +4.8% in March from a month earlier. Domestic orders, however, dropped by -3.8%.