Sample Category Title

EUR/USD Analysis: Retreats After Election Jump

'Macron is a new face and that's exactly what France and Europe need: a fresh start.' – Andre Sapir, Bruegel (based on Bloomberg)

Pair's Outlook

On Monday morning the common European currency was in a retreat against the US Dollar, as it touched the support provided by the weekly PP, which is located at the 1.0958 level. It is most likely that the currency exchange rate will continue to surge, as it could be pushed higher by minor support levels. It could reach next the combined resistance of the weekly and monthly R1s at 1.1040. Meanwhile, market participants should be careful with technical analysis, as the yesterday's election was a large fundamental change for the basis of the Euro.

Traders' Sentiment

SWFX traders remain bearish, as 62% of open positions are short, and 54% of trader set up orders are to sell.

GBP/USD Analysis: Leaves 1.30 Unchallenged

'The rapid deterioration in the UK's economic momentum has largely gone unnoticed by an FX market preoccupied with political distractions.' – GJanes Rossiter (Based on Pound Sterling Live)

Pair's Outlook

Having outperformed the US Dollar, the British Pound approached the 1.30 major level on Friday, but with supply around this area remaining relatively strong. Consequently, another bullish development is not expected to occur, as the Cable is likely to keep weakening until the 1.28 major level is reached—that is where demand is sufficient to trigger a solid rebound. However, technical indicators in the daily timeframe are unable to confirm the pair is to edge lower today, thus, the immediate support, namely the weekly pivot point, at 1.2934 should limit any possible losses today.

Traders' Sentiment

Traders retain a neutral sentiment, as 51% of all open positions are currently short and the remaining 49% are long. At the same time, there are only 54% of orders to acquire the Sterling (previously 57%).

USD/JPY Analysis: To Preserve The Channel Pattern

'The dollar fell 0.3 percent against the yen to 112.19, pulling away from a seven-week high of 113.045 yen set on Thursday.' – Masayuki Kitano (Based on Reuters)

Pair's Outlook

Strong US fundamentals helped the USD/JPY pair to completely recover from its intraday low on Friday and even edge 29 pips higher, retesting the descending channel's resistance line. Today the pair opened with a small bullish gap, but those gains are not expected to hold, with the channel's upper boundary still prevailing. The Greenback should now keep declining against the Yen until the 108.00 mark is reached. However, first the Buck is required to pierce the 55-day SMA, where demand could be sufficient and trigger another rally, eventually leading to the end of the channel pattern.

Traders' Sentiment

Today 61% of traders are short the US Dollar, compared to 58% on Friday. Meanwhile, 52% of all pending orders are to sell the Buck (previously 58%).

Gold Analysis: Recovers On Monday

'Spot gold still targets $1,209 per ounce, as suggested by a Fibonacci retracement analysis.' – Wang Tao, Reuters

Pair's Outlook

After a low opening and touching the 1,221.50 level on Monday morning the yellow metal regained its losses in the early hours of the day's trading session. However, the bullion is still likely to continue the retreat, as the Macron victory in the French Presidential Election is seen as a sign of minor changes in the fundamentals in the financial markets, which could affect the price of the yellow metal. Due to that reason the commodity price might retreat down to the next support cluster, which begins just below the 1,220 mark.

Traders' Sentiment

Traders are neutral bearish, as 51% of open positions are short. However, 68% of trader set up orders are to buy the metal.

Macron Wins French Election With Landslide Victory

Macron won the final battle of the French presidential election which was in line with market expectations. He has become the youngest president in the French history.

Notably, Macron got 66.06% of the votes, largely surpassing his opponent Le Pen's 33.94% outperforming the 20% lead poll projections.

The voting ratio was 65.3%, which was lowest compared to the past three presidential elections; 71.96% in 2012, 75.11% in 2007 and 67.62% in 2002. Macron received a higher share of votes in big cities such as Paris and Marseille whilst Le Pen received a higher share of votes in the suburbs.

Le Pen's extreme stance and policies, such as anti-globalization, anti-immigrants, trade protectionism and making France leave the EU, will likely lead France's direction back toward conservativism and enclosure.

Conversely, Macron's policies aim to change the country's long-standing bureaucracy and excessive government control to revive the sluggish French economic performance. The outright victory of the independent centrist Macron indicates that French citizens aspire for change and variety.

Macron's victory has eased market concerns over France's leaving the EU and the collapse of the EU, pushing EUR and Europeans stocks further up.

During the early Asian session on Monday, EUR/USD hit a 6-month high of 1.1021. EUR/JPY hit a high of 124.49, last seen May 12 of 2016. Spot gold hit a low of 1220.77, last seen March 17. However, EUR and European stocks saw a retracement during the early European session due to profit taking pressure and the rebound of USD.

Macon now must face severe challenges such as high unemployment rate, low economic growth and immigration issue. In addition, as Macron is independent, he has little control of the parliament, which will likely be a hurdle after he taking office.

Technical Outlook: CAC 40 – Corrective Easing On Overbought Studies To Precede Fresh Upside

The index eased in early Monday trading and stays below Friday's fresh multi-year high at 5443 (session high in Asia was 5442). The move could be seen as correction ahead of fresh upside as the price rallied strongly last week, gaining 4.3% for the week. Strong bullish signal was generated on last week's break above former peak at 5284 (26 Apr 2015 high/Fibo 76.4% of 6168/2396, May 2007/Feb 2009 fall) that would extend bull-leg from 3922 (June 2016 trough) towards next targets at 5660 zone. Meantime, the price is expected to correct recent strong gains, as daily studies are overbought. Rising daily Tenkan-sen offers good support at 5323, ahead of broken former peak at 5284 (also rising 10SMA) and last week's low at 5213 (reinforced by weekly Tenkan-sen and near daily higher base at 5205). Only break here would weaken the structure and signal deeper correction towards 5119 (24 Apr post first election round gap-higher low).

Res: 5443, 5500, 5550, 5660

Sup: 5367, 5323, 5284, 5205

Technical Outlook: EURUSD Eases From Fresh 6-Month High On Buy Rumor Sell Fact Scenario After Macron’s Victory

The Euro pulled back to 1.0950 support zone in early Monday's trading after hitting fresh six-month high at 1.1020 on opening.

Brief probe above psychological 1.1000 barrier on relief after Emmanuel Macron won French presidential election was so far short-lived, as trader took profits on larger Euro longs, on buy rumor sell fact scenario.

However, overall sentiment remains firmly bullish and additionally supported by comments from ECB official who said that recovery in the Eurozone is gaining traction.

Technical studies are bullish and supportive for further upside, with current pullback seen as positioning for fresh longs.

Initial support at 1.0950 (former two-week congestion top, reinforced by rising daily Tenkan-sen) is holding for now, followed by rising 10SMA at 1.0923, with strong support at 1.0900 zone where top of thick 4-hr cloud (1.0900/1.0815) is expected to contain pullback.

Only extended dips below 1.0850/30 (former congestion floor / 200SMA) would generate stronger bearish signal for deeper correction.

Res: 1.0995, 1.1020, 1.1067, 1.1100

Sup: 1.0950, 1.0923, 1.0900, 1.0874

Daily Technical Analysis: EUR/USD 1.0930-1.0950 Is Point Of Confluence

The expected win of newly elected president Emmanuel Macron seem to be priced in the market after a successful rally as we shown in the previous EUR/USD analysis. At this point the pair is heading towards the POC zone 1.0930-50 where we could see a possible bounce. As the ATR of EUR/USD is low - only 77 pips, levels to watch for are 1.0990 and 1.1020. However the loss of 1.0930 is a possible signal for a deeper retracement towards 1.0870. Retail gap could only be closed if the pair broke below 1.0820.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

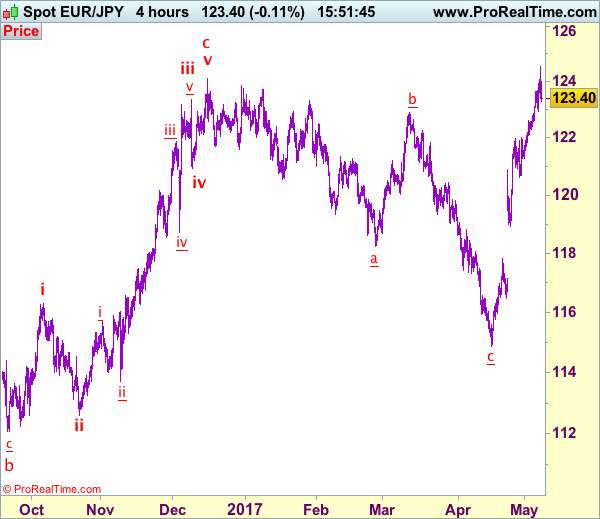

Trade Idea: EUR/JPY – Sell at 124.00

EUR/JPY - 123.31

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

Original strategy:

Buy at 122.10, Target: 124.10, Stop: 121.50

Position: -

Target: -

Stop: -

New strategy :

Sell at 124.00, Target: 122.20, Stop: 124.60

Position: -

Target: -

Stop:-

Although the single currency jumped initially above 124.10 resistance and rose to as high as 124.55, the subsequent retreat suggests consolidation below this level would be seen and as long as this level holds, mild downside bias is seen for another retreat to 122.92 support, below there would suggest a temporary top is possibly formed, bring further fall to 122.60 but break of 122.00-10 is needed to add credence to this view, bring retracement of recent upmove to 11.50 first.

In view of this, we are looking to turn short on recovery. Above said resistance at 124.55 would abort and signal recent upmove is still in progress and may extend further gain towards 125.00 level but loss of upward momentum should prevent sharp move beyond 125.40-50, risk from there is seen for another retreat later.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Canadian Job Creation Slows Markedly In April

'All in all, a fairly weak jobs report'. - David Madani, Capital Economics

Canadian employment growth fell unexpectedly last month, whereas the unemployment rate hit its lowest level in nearly nine years. Statistics Canada reported on Friday that the Canadian economy created 3.2K jobs in April, following the preceding month's climb of 19.4K and falling behind analysts' expectations for a 20.0K job gain. Meanwhile, the unemployment rate dropped to 6.5%, while analysts expected an unchanged reading of 6.7%. Statistics Canada attributed the decline in the jobless rate to 45.5K people leaving the labour force. It also noted that the youth jobless rate fell 1.1% to 11.7%. Average hourly earnings rose 0.7% on an annual basis in April, the slowest since October 1997. In regional terms, the largest job gain of 11.3K was registered in British Columbia, where the unemployment rate climbed slightly to 5.5%. Analysts suggested that the economy lost positive momentum after showing strong economic growth in the final quarter of 2016. The Bank of England said at its recent meeting that it was concerned with weak pay growth and noted that there was still room for improvement.