Sample Category Title

US Unemployment Rate Drops To 4.4% As Job Creation Rebounds Sharply

'A stable oil market and a rebound in nonfarms will likely set the stage for a narrow to mixed trading session.' - Peter Cardillo, First Standard Financial

The US unemployment rate dropped unexpectedly last month, as companies created more jobs than expected. The Department of Labour reported that US firms added 211K jobs to the economy in April, following the preceding month's revised down increase of 79K jobs and surpassing analysts' expectations for a 194K gain. Data also showed that the unemployment rate fell to 4.4%, down from March's 4.5%, whereas markets anticipated an acceleration to 4.6%. Meanwhile, average hourly earnings rose 0.3% last month, up from March's climb of 0.1% and in line with forecasts. According to analysts' projections, if job creation remains strong, the US labour market will likely hit full employment already this year. Friday's better-than-expected employment report combined with low initial jobless claims and the strong services PMI pushed up the odds of a June hike by the Federal Reserve. Furthermore, some analysts said that the economy regained positive momentum in the Q1, suggesting that the Fed will likely be forced to raise rates at a quicker than initially expected pace this year.

Trade Idea: AUD/USD – Sell at 0.7470

AUD/USD – 0.7404

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term down

Original strategy :

Sell at 0.7470, Target: 0.7300, Stop: 0.7530

Position: -

Target: -

Stop: -

New strategy :

Sell at 0.7470, Target: 0.7300, Stop: 0.7530

Position: -

Target: -

Stop:-

As aussie has recovered after falling to 0.7368 on Friday, suggesting consolidation above this level would be seen and another bounce to 0.7425-30 is likely, however, reckon upside would be limited to 0.7470-75 and bring another decline later, below said support at 0.7368 would extend recent decline from 0.7750 top for at least a retracement of early upmove to 0.7330-35 (100% projection of 0.7750-0.7473 measuring from 0.7611), then 0.7295-00 (76.4% retracement of 0.7158-0.7750) but oversold condition should prevent sharp fall below 0.7245-50, bring rebound later.

In view of this, we are looking to sell aussie on recovery as 0.7465-70 should limit upside, bring another decline. Above 0.7500-10 would defer and risk rebound to said resistance at 0.7556 but break there is needed to signal low is formed instead, bring further gain to 0.7580-85 but resistance at 0.7611 should hold from here.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

EUR/GBP: Downside Better Protected After Recent Rebound

French say 'no' to populism and 'yes' to a united Europe following a similar trend in Austria and The Netherlands over the past six months. Macron's decisive victory on Sunday is a clear sign of a resistance to populism after Trump’s election and the Brexit vote. The Euro hit a seven-month high, to trade above 1.10 against the dollar as an initial reaction, but pulled away in a classic 'buy the rumor, sell the fact' style given that traders were already positioned for a Macron win. The Euro appreciated by 2.5% since the first round of voting, suggesting that the good news was already priced in, and now it requires a fresh catalyst to determine the next move.

The next challenge for Macron is going to be the parliamentary elections in June, and given that there’s a lack of significant support, it remains highly uncertain whether the President can build a parliamentary majority. However, I don’t think this is going to be a major concern to the Euro.

The next political risk event in the EU is the Italian general election, due to be held in March 2018. As there are ten months until this key event, investors and traders should shift their attention from politics to macro fundamental drivers.

The key macroeconomic indicator from the Eurozone, along with fewer political risks, will likely lead to inflows of capital to European markets, especially as valuations look more attractive than the US. But the Euro’s direction will be more influenced by the actions of the European Central Bank. If the ECB is thinking of starting the tapering process, the next meeting on June 8 could be a time to announce the beginning of the exit. Therefore, I see more upside risk than the downside to EURUSD.

Moving into the US, the economy added 211,000 jobs in April and unemployment rate fell to 4.4%. The better than expected data validates the Federal Reserve’s statement that recent weakness in some economic data would prove transitory. However, not all chunks of the jobs report were robust enough. The labor participation rate fell to 62.9% from 63%, and annual wages dipped by 0.2% to 2.5%. While this will not stop the Fed from raising interest rates in June, Friday’s US retail sales and inflation figures will provide a better indication of whether a rate hike is a done deal or not.

Oil prices inched 1% higher early Monday after a steep decline last week, sending both benchmarks to their lowest levels since December, and many traders were left wondering whether further downside risk lies ahead. The factors moving oil prices haven’t changed much recently; it’s all about inventories and US Shale vs. OPEC. The latest negative factor was weaker import figures from China. At this stage, OPEC members have no choice but to talk up prices by signaling an extension to the production cuts agreement, but the ability of Shale to keep pumping at relatively low prices remains the largest threat. I still believe that markets will eventually rebalance at a later stage in H2, and prices will recover, but the recovery won’t be a straight line.

Currencies: EUR/USD Tests 1.10. Post-Macron Consolidation Might Be On The Cards

Sunrise Market Commentary

- Rates: Macron's victory discounted?

Macron's presidential election victory was largely discounted in markets and could trigger some buy-the-rumour, sell-the-fact reaction amid today's uneventful eco calendar. Afterwards, bond markets might start positioning towards key, hawkish (?) June ECB and Fed policy meetings, which is negative for the Bund and the US Note future. - Currencies: EUR/USD tests 1.10. Post-Macron consolidation might be on the cards

This morning, EUR/USD and USD/JPY jumped temporary higher on the Macron victory in the French Presidential election. However, European markets already largely anticipated this victory last week. So, if the risk-on rally takes a breather, the recent rebound of USD/JPY and EUR/USD might also shift into a lower gear.

The Sunrise Headlines

- US equity markets ended 0.25% to 0.5% higher with the S&P setting an all-time closing high. Overnight, Asian bourses gain as well with China underperforming (-1%) and Japan outperforming (+2%), catching up after last week's holidays.

- Macron has swept to emphatic victory in France's presidential election, beating Le Pen and clinching 65% of the vote. Mr Macron has never before held elected office and his political movement En Marche! was set up barely a year ago.

- China's exports and imports rose in April, but missed analysts' expectations, as domestic and foreign demand faltered and commodity prices fell. China's FX reserves rose in April for a third straight month as capital controls and a pause in the dollar's rally helped staunch capital outflows.

- SF Fed Williams said his outlook for three or four rate increases in 2017 hasn't shifted, as the labour market shows signs of expanding beyond its sustainable rate.

- German Chancellor Merkel's Christian Democrats gained a surprise victory in the north German region of Schleswig-Holstein, giving them a boost ahead of September's national Bundestag vote.

- British consumer spending growth slowed to one of its weakest rates in the past three years last month, credit and debit card company Visa reported, as higher inflation and weak wage growth squeeze households' disposable income.

- Today's eco calendar contains only second tier data. Fed governors Bullard and Mester are scheduled to speak.

Currencies: EUR/USD Tests 1.10. Post-Macron Consolidation Might Be On The Cards

EUR/USD tests 1.10. Post-Macron consolidation ahead?

On Friday, the dollar was in the defensive in Asia, but found a bottom later on as European markets were only modestly affected by the decline of commodities and Asian equities. The US payrolls were solid, but not strong enough to inspire a genuine USD rebound. USD/JPY and EUR/USD remained well bid going into the second round of the French election. USD/JPY finished the session at 112.71. EUR/USD closed at 1.0998.

In Asia, risk sentiment is constructive after the victory of Emmanuel Macron in the French Presidential election. Japanese equities show solid gains (2% +) as investors return from the Golden holiday week. The gains elsewhere in the region are more modest. Chinese equities underperform again. Chinese foreign trade data trailed census expectations, but the trade surplus was solid. USD/JPY opened north of 113 on the Macron victory but trades currently again in the 112.75 area. EUR/USD developed a similar pattern. The pair opened north of 1.10, but returned to the 1.0975 area. A Macron victory was largely discounted. The Aussie dollar stabilizes in the 0.74 area, close to recent lows, as industrial commodities including iron ore and copper, struggle to prevent further losses.

Today, there are only second tier data in Europe and the US. EMU Sentix investor confidence may rise further as European bourses have done well recently, but the report will have limited impact on trading. Markets already prepositioned for a Macron victory last week with European (French) equities outperforming. On the FX market this translated in a combined rise of EUR/USD, USD/JPY and EUR/JPY. Sentiment on risk will probably remain constructive at the start of trading in Europe. Even so, the risk-rally of EUR/USD and USD/JPY might run into resistance as investors will gradually turn their focus to the French Parliamentary election and how that will shape the outlook for France.

In a day-to-day perspective, USD/JPY and EUR/USD might probably hold near the recent highs. However, the upside momentum might slow. For EUR/USD, some (cautious) profit take on the recent euro rally might be on the cards. For USD/JPY, we keep an eye at global risk sentiment. US equities/equity futures will probably profit only slightly from the French election result. Commodities and China might are a wildcard, but might be a source of uncertainty. On the interest rate markets, a June rate hike is almost completely discounted. So, probably USD/JPY won't get additional interest rate support. So, Last week's combined rebound of USD/JPY and EUR/USD might see some modest profit taking. LT the ECB strategy/communication will be important for the fate of the euro. However, as we don't expect a clear message before the June meeting, further euro gains might be less evident ST.

From a technical point of view, USD/JPY bottomed out in April and regained the 112.20 resistance last week. This improved the technical picture. However, followthrough gains were modest. Next intermediate resistance comes in at 115.51, but it might be too early for a retest of this level. EUR/USD extensively tested the topside of the MT range (1.0874/1.0906 area) late March. The pair returned to the range top after the first round of the French election and broke above the 1.09/1.0950 resistance at the end of last week. If confirmed, this break would improve the ST picture. Next resistance stands at 1.1129 (62% retracement) and at 1.1366 (correction top). A decline below 1.0821 would suggest that the dollar is regaining traction against the euro. A ST EUR/USD correction might occur as the pair is moving into overbought territory.

EUR/USD breaks above the recent highs in the 1.0950 area. However, some post-Macro consolidation might be on the cards

EUR/GBP

EUR/GBP fails to regain the 0.85 barrier for now

On Friday, there was no important UK news to guide sterling. The conservative party made good progress in local elections, indicating that PM May might secure a comfortable majority at next month's Parliamentary. Cable held strong and drifted to the high 1.29 area. This suggests a slightly positive impact on sterling. The soft reaction of the dollar after the payrolls also supported cable. EUR/GBP traded with a slightly negative intraday bias. The pair closed the session at 0.8473.

Today; only the Halifax house prices are on the UK agenda. A rather soft report (0.1% M/M and 36% Y/Y) is expected. So, sterling trading will probably again be driven by the global trends in the euro and the dollar after the French election. Cable has been very strong of late, so there might be room for some consolidation to digest recent gains.

Two weeks ago, EUR/GBP dropped below EUR/GBP 0.84 support, (temporary) improving the sterling picture. The pair came within reach of the key 0.8305 support (Dec low), but no real test occurred. After a late April EUR/GBP rebound, the range bottom is better protected. Longer term, Brexit-complications remain potentially negative for sterling. On technical considerations we slightly prefer a EUR/GBP buy-on-dips approach.

EUR/GBP: downside better protected after recent rebound

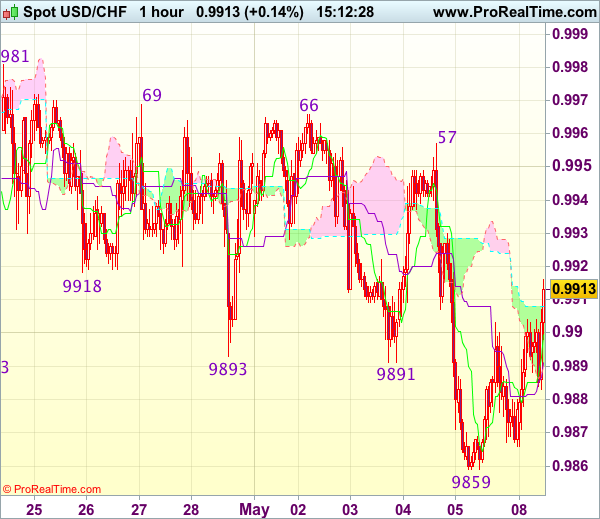

Trade Idea : USD/CHF – Stand aside

USD/CHF - 0.9905

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9900

Kijun-Sen level : 0.9891

Ichimoku cloud top : 0.9908

Ichimoku cloud bottom : 0.9890

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback extended recent decline to as low as 0.9859 late last week, the subsequent rebound suggests consolidation above this level would be seen and recovery to 0.9925-30 cannot bye ruled out, however, reckon resistance at 0.9957 would limit upside and bring further consolidation. Below said support at 0.9859 would signal recent decline from 1.0108 top has resumed and bring further weakness to support at 0.9831 and possibly towards 0.9800.

In view of this, would be prudent to stand aside in the meantime. Only a break of 0.9966-69 resistance would signal low is formed instead, bring subsequent bounce to 1.0000-08 and later towards 1.1030 but resistance at 1.1067 should hold from here.

Trade Idea : GBP/USD – Buy at 1.2905

GBP/USD - 1.2975

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2966

Kijun-Sen level : 1.2957

Ichimoku cloud top : 1.2904

Ichimoku cloud bottom : 1.2889

Original strategy :

Buy at 1.2885, Target: 1.2985, Stop: 1.2850

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2905, Target: 1.3005, Stop: 1.2870

Position : -

Target : -

Stop : -

As cable has maintained a firm undertone after last week’s late rally above previous resistance at 1.2965, adding credence to our bullish view that recent upmove is still in progress and may extend further gain to 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance), then towards 1.3040-50 which is likely to hold from here due to near term overbought condition.

In view of this, would not chase this rise here and would be prudent to buy cable on pullback as 1.2900-05 should limit downside and bring another rise later. Below 1.2880 would defer and risk weakness to 1.860-65 but only a break of said support at 1.0831 would signal a temporary top has been formed.

Trade Idea : EUR/USD – Sell at 1.0990

EUR/USD - 1.0968

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0977

Kijun-Sen level : 1.0987

Ichimoku cloud top : 1.0956

Ichimoku cloud bottom : 1.0933

Original strategy :

Buy at 1.0920, Target: 1.1020, Stop: 1.0885

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0990, Target: 1.0890, Stop: 1.1025

Position : -

Target : -

Stop : -

Although the single currency opened higher earlier today, lack of follow through buying and the subsequent retreat from 1.1025 suggest consolidation below this level would be seen and pullback to 1.0949 cannot be ruled out, break there would suggest a temporary top is possibly formed, bring correction to 1.0900-10 but support at 1.0875 should remain intact and bring rebound later.

In view of this, we are looking to sell euro on recovery as 1.0995-00 should limit upside and bring another retreat. Above said resistance at 1.1025 would abort and signal recent upmove from 1.0340 low has resumed for headway to 1.1050 but reckon upside would be limited to 1.1065-70 (61.8% projection of 1.0602-1.0951 measuring from 1.0851).

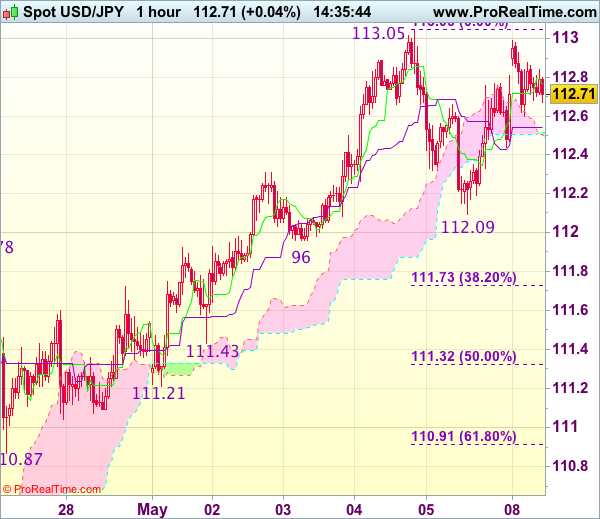

Trade Idea : USD/JPY – Stand aside

USD/JPY - 112.63

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.74

Kijun-Sen level : 112.58

Ichimoku cloud top : 112.52

Ichimoku cloud bottom : 112.47

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback opened higher earlier today, as dollar has retreated after faltering below last week’s high at 113.05, suggesting further consolidation below this level would be seen and pullback t 112.40 cannot be ruled out, however, reckon support at 112.09 would limit downside and bring another rise later. Above said resistance at 113.05 would confirm recent upmove has resumed and extend gain to 113.10-15 (61.8% projection of 108.13-111.78 measuring from 110.87) and 113.30 but reckon upside would be limited to previous resistance at 113.54 and price should falter well below 113.90-00.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 112.09 support would bring test of 111.96 but break of this level is needed to signal a temporary top has been formed at 113.05, bring correction to 111.73-78 (38.2% Fibonacci retracement of 109.59-113.05 and previous resistance), however, reckon 111.21-32 (previous support and 50% Fibonacci retracement) would contain weakness.

US CPI Inflation After The Sharp Fall In March

Market movers today

This morning market focus will be on the out come of yesterday's French president ial election in which independent Macron defeat ed the Front Nat ional's Le Pen with 66.1% against 33.9%. This was a greater margin of victory than opinion polls had projected.

In terms of data releases focus will be on euro area Sentix investor confidence which we expect to climb further as markets seemed relieved by the outcome of the first round of the French election.

The German factory orders are also released today. The figure reported a 3.4% monthly increase in February, following the 6.8% fall in January. We estimate a monthly decline of 2.3% for March but note that the volatility in the figure since October 2016 has been higher than usual, meaning a 2.3% decrease is of less significance than previously

The Fed's Bullard (non-voter, dove) and Mester (non-voter, hawkish) are both scheduled to speak in the afternoon. Here, we hope to get some more colour on the different views within the commit tee after the relatively dull FOMC statement released on Wednesday last week.

During the rest of the week focus will be on US CPI inflation after the sharp fall in March, German GDP growth for Q1 and the BoE which we expect to keep rates unchanged.

Selected market news

In the final run-off of France 's president ial election, independent Emmanuel Macron defeated the Front National's Marine Le Pen with an even greater margin of vict ory (66.1% against 33.9%) than opinion polls project ed. Market s will now wat ch out for Macron's choice of prime minister and cabinet , which he has promised to announce once sworn into office on 14 May. The next key event in the election t imeline will be the parliamentary elections for the National Assembly to be held from 11-18 June under a similar two-round voting system as in the presidential election. The National Assembly is the main legislative body, as it takes prominence over the Senate in law making, and has the power to take down the government in a noconfidence vote. How much of his policy proposals Emmanuel Macron can actually implement will therefore depend on how many seats his movement En Marche! (EM) can secure in the election.

'On Friday, the US jobs report for April was released, and showed solid jobs growth of 211,000. While the FOMC members will welcome the solid jobs growth and the lower unemployment rate, as it supports their view that monetary policy should be tightened gradually, we think they are concerned about the subdued wage growth, as it part ly reflects lower inflat ion expectations. For more details see Flash Comment US: Subdued wage growth a concern for the Fed, 5 May.

Saudi Arabia's oil minister has said thathe expect s OPEC to extend the oil cut deal int o the second half of the year and possibly beyond.

Market Update – Asian Session: Macron Victorious In France

Asia Mid-Session Market Update: Macron victorious in France; Nikkei returns with a 2% rise to 18-month highs; China Trade internals underwhelm while Reserves extend rebound

Friday US Session Highlights

Apr CBIZ Small Business Employment Index: -0.3% v +1.6% m/m; first negative reading for the April period since the SBEI's inception

(US) APR UNEMPLOYMENT RATE: 4.4% V 4.6%E (lowest since May 2007); Underemployment Rate: 8.6% v 8.9% prior; participation Rate: 62.9% v 63.0% prior

(US) APR CHANGE IN NONFARM PAYROLLS: +211K V+190KE; Mar revised lower

(US) APR AVERAGE HOURLY EARNINGS M/M: 0.3% V 0.3%E; Y/Y: 2.5% V 2.7%E; AVERAGE WEEKLY HOURS: 34.4 V 34.4E; prior earnings revised lower

(US) New York Fed Nowcast: cuts Q2 GDP forecast to 1.8% from 2.3% from 4/28

Politics

(FR) France's Macron defeats Le Pen in French Presidential Elections; Turnout was the lowest since 1969 – French Interior Ministry

(FR) According to Kantar survey, Macron's party would get 26% in upcoming French parliamentary elections, followed by Republicans' 21% and Le Pen's FN party at 21% - press

(GE) Chancellor Merkel's Christian Democrats (CDU) defeated the Social Democrats in the Schleswig-Holstein state elections; margin 33% to 26% - ARD

(US) Republicans in the Senate said to plan a version of healthcare bill that is radically different from that of the House, including keeping some of the Obamacare provisions - press

(UK) Opposition Labour Party finance chief McDonnell says he can guarantee that low and middle class wage earners would not see any tax increase to fund the party's spending plans if it wins elections next month - press

Weekend US/EU Corporate Headlines

CCP: To merge with Sabra Health Care REIT for combined equity value of $4.3B in all-stock deal, implies $29.96/share* (implies ~11.8% premium)

DHT: Board Unanimously Rejects Unimproved Proposal from Frontline

TRCO: Sinclair Broadcast expected to make a $45/shr offer for Tribune (implies a $3.9B deal) - financial press

Key economic data:

(CN) CHINA APR FOREIGN RESERVES: $3.030T V $3.020TE (UPDATE); 5-month high; 3rd straight increase (first 3-month streak since mid-2014)

(CN) CHINA APR TRADE BALANCE: $38.1B V $35.2BE

(CN) CHINA APR TRADE BALANCE (CNY): 262.3B V 197.2BE ; 3-month high

(AU) AUSTRALIA MAR BUILDING APPROVALS M/M: -13.4% (biggest decline since mid-2012) V -4.0%E; Y/Y: -19.9% (biggest decline in 5 months) V -10.0%E

(AU) AUSTRALIA APR ANZ JOB ADVERTISEMENTS M/M: +1.4% V +0.8% PRIOR

(AU) AUSTRALIA MAR NAB BUSINESS CONFIDENCE: 13 (highest level since early 2010) V 6 PRIOR; CONDITIONS: 14 V 12 PRIOR

Asia Session Notable Observations, Speakers and Press

Macron defeats Le Pen in French presidential elections by over 20pts as implied by polls, though market reaction is muted as investors look ahead to Parliamentary elections and also question his ability to govern a divided populace used to mainstream politics. Euro initially rises to 1.1020 but quickly reverses initial gains, while US equity futures markets turn marginally lower.

Chinal FX reserves rise for the 3rd straight time to a 5-month high as regulatory actions stem the tide of outflows. China Trade data also mixed, with CNY and USD denominated surplus beating estimates but Exports and Imports growth undershoot projections on both counts. CNY-denominated import growth slows to 4-month lows, and China Customs also notes Iron Ore imports were at lowest since Oct 2016.

Nikkei225 returns from 3-day break to reach its best levels since Dec-2015, tracking USD strength against the Yen following lowest US unemployment rate levels since mid-2007. Australia also firms as miners rally on a bounce in iron ore prices. Recall iron ore fell over 10% late last week, weighing on AUD currency. AUD/USD is tracking higher late in the day, up some 50pips from last week's lows despite a much bigger than expected decline in Australia building approvals.

Australia's 2nd biggest lender Westpac is little changed on mixed H1 results. Earnings were in line and bank said the level of delinquent borrowers remains historically “low” despite a modest uptick in overdue home loans.

China

(CN) Moody's: China shadow banking sector impacted by increasingly tight systemic liquidity - press

(CN) China said to focus on improving the auditing of SOE's overseas investment - Chinese press

(CN) China Customs: Apr iron ore imports were lowest since Oct - press

Japan

(JP) Japan Bankers Association Chairman Hirano: Japan does not need more monetary or fiscal stimulus, needs structural reforms

(JP) Japan Vice Fin Min of International Affairs (currency chief) Asakawa: Slowdown of China economy is a major global risk - press

(JP) Japan PM Abe: China's role is important in dealing with North Korea

Australia/New Zealand

(NZ) BNZ (private bank): Believes RBNZ will raise cash rate in Feb 2018 (prior view was May 2018)

Korea

(KR) South Korea govt think tank (KDI) monthly report: Economy is on modest recovery track - Korean press

(KR) North Korea detains another US citizen, bringing the number of total US detainees to 4 - press

Asian Equity Indices/Futures (00:30ET)

Nikkei +2.4%, Hang Seng +0.6%, Shanghai -0.7%, ASX200 +0.5%, Kospi +1.3%

Equity Futures: S&P500 flat; Nasdaq -0.1%, Dax flat, FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.0960-1.1020; JPY 112.60-112.95; AUD 0.7385-0.7420; NZD 0.6890-0.6930; GBP 1.2950-1.2990

June Gold +0.3% at 1,231/oz; June Crude Oil +1.3% at $46.80/brl; July Copper -1.2% at $2.51/lb

(US) Weekly Baker Hughes US Rig Count: 877 v 870 w/w (+0.8%) (16th straight weekly rise)

(SA) Saudi Oil Min Al-Falih: OPEC cuts could extend beyond H2 of 2017; Not concerned with oil demand peaking any time soon - press

(CN) PBOC SETS YUAN MID POINT AT 6.8947 V 6.8884 PRIOR

(CN) PBOC skips open market operations (2nd straight skip)

Asia equities / Notables / movers

Australia

Westpac (WBC) +0.2%; Reports H1 cash earnings A$4.02B v A$4.02Be; Rev A$10.77B v A$10.48B y/y

Fairfax (FXJ) +2.6%; Received indicative proposal for certain assets from TPG consortium at A$0.95/shr in cash and shares

Myer (MYR) -8.9%; Credit Suisse Cuts MYR.AU to Underperform from Neutral, price target: A$0.82

Origin Energy (ORG) +3.1%; Announces agreement to sell Stockyard Hill Wind for A$110M

Hong Kong

Geely (175) +2.1%; Apr sales

ePrint (1884) -2.2%; Guides FY16

Japan

Olympus (7733) -4.7%; FY16/17 results

Subaru (7270) -0.3%; FY18 results speculation

Toshiba (6502) -1.0%; KKR said to be in talks over a preemptive bid for Toshiba's chip unit - press

Mitsubishi Motor (7211); FY16/17 results speculation