Sample Category Title

GOLD Consolidating Around $1230, SILVER Starting A Consolidation Phase, CRUDE OIL Short-Squeeze.

GOLD Consolidating around $1230.

Gold continues its decline after the yellow metal has faded near the hourly resistance at 1295 (18/04/2017 high). Hourly support is now located at 1195 (10/03/2017 low). The road is wide-open for further decline.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Starting a consolidation phase.

Silver is consolidating after the strong decline. Hourly support is given at 16.20 (04/05/2017 low). Strong resistance is given at a distance at 19.00 (09/11/2017 high). Expected to see continued bearish pressures until at least $16.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Short-squeeze.

Crude oil is bouncing back on short-squeeze move. The commodity has reached a level below $44. Strong support is given at 42.20 (14/11/2017 low). Expected to see renewed bearish pressures.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

EUR/JPY Consolidating Around 5-Month High, EUR/GBP Trading Sideways, EUR/CHF Strong Bullish Pressures.

EUR/JPY Consolidating around 5-month high.

EUR/JPY's buying pressures are there. Strong resistance standing at 124.10 (15/12/2016 low) has been broken. Major support is given at 114.90 (18/04/2017low). Expected to see further renewed buying pressures towards 125.00.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Trading sideways.

EUR/GBP is trading mixed. The technical structure remains negative as long as the resistance at 0.8530 (25/04/2017 low) holds. Expected to show continued weakness until support given at 0.8304 (05/12/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

EUR/CHF Strong bullish pressures.

EUR/CHF's volatility is getting stronger and is now targeting resistance given at 1.0898 (08/12/2017 high). Despite the sharp increase and the recent bullish breakout which is very likely psychological, we believe that the medium-term pattern suggests us to see at some point renewed bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

USD/CHF Towards Support At 0.9814, USD/CAD Profit-Taking, AUD/USD Wide-Open For Further Decline.

USD/CHF Towards support at 0.9814.

USD/CHF is weakening. The positive shortterm technical structure has been invalidated. Expected to target support given at 0.9814 (27/03/2017 high).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Profit-taking.

USD/CAD has declined after failing to reach 1.3800. Hourly support can be found at 1.3411 (24/04/2017 high) then 1.3353 (20/01/2017 high). Expected to show renewed bullish pressures as long as the pair remains above 1.3530 (27/04/2017 low).

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Wide-open for further decline.

AUD/USD is trading below 0.7500. As long as prices remain below the resistance at 0.7608 (17/04/2017 high), the short-term technical structure is negative. Key resistance stands at 0.7681 (30/03/2017 high). Expected to show further weakness.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Trading Sideways, GBP/USD Slight Increase, USD/JPY Consolidating Above Former Resistance.

EUR/USD Trading sideways.

EUR/USD is trading higher. Hourly support is given at 1.0875 (04/05/2017 low) then 1.0682 (21/04/2017 base). Stronger support can be found at 1.0494 (22/02/2017 low). Expected to show another leg higher towards 1.10.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Slight increase.

GBP/USD is trading mixed. Hourly resistance given at 1.2966 (30/04/2017 high) has been broken. Hourly support can be found at 1.2757 (21/04/2017 low). An unlikely break of this support would indicate further weakness.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Consolidating above former resistance.

USD/JPY is now slowing down since the pair reached resistance given at 112.20 (31/03/2017 high). Hourly support can be found at 110.88 (26/04/2017 low). Stronger support is located at 108.13 (17/04/2017 low). Other key supports lie at a distant 106.04 (11/11/2016 low). Expected to show continued bullish pressures.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

Euro Steady As Macron Wins Landslide Victory In French Election

The euro has edged lower in the Monday session, as the pair is currently trading at 1.0940. On Sunday, Emmanuel Macron easily defeated Marie Le Pen to win the French presidential election. It's a quiet start to the week, with no major events out of the eurozone or the US. Still there was some positive news in the eurozone, as German Factory Orders gained 1.0%, above the forecast of 0.7%. As well, Eurozone Sentix Investor Confidence climbed to 27.4, beating the estimate of 25.3 points. The indicator has now improved over four consecutive months, pointing to stronger confidence among investors and analysts.

Emmanuel Macron has become France's youngest president at age 39, and he rode to victory in convincing style. Macron won 64% of the popular vote, with Marie Le Pen taking 36%. Macron's margin of victory was larger than the polls predicted, but the markets had priced in a decisive win, so the euro has showed little response to the election results. Although Macron certainly “won big”, it should be noted that fully one third of French voters either abstained or voted a blank ballot as a protest vote. This means that Macron was viewed by many voters as a default choice, given that his opponent was the leader of the far-right and has been accused of being racist and xenophobic. The French elections now enter a new phase, with parliamentary elections slated for mid-June. Macron's En Marche! party is barely a year old and is unlikely to win a majority, which would mean a power-sharing setup in parliament, likely between Macron's party and the center-right. Similar to the presidential election, the parliamentary election is full of uncertainty, and opinion polls during the election campaign will be important as fundamental releases and should be treated as market-movers.

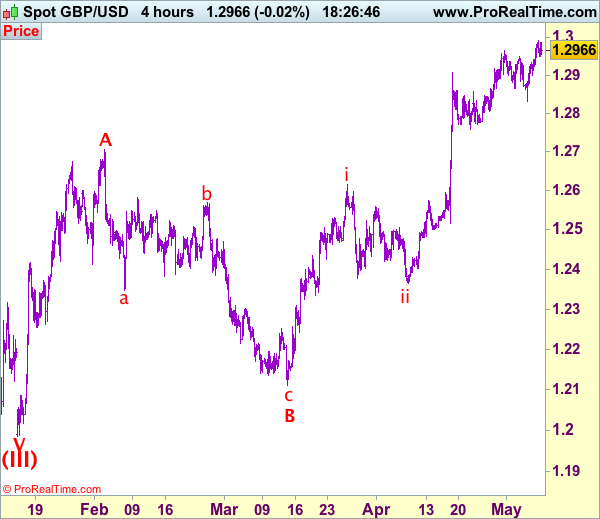

Trade Idea: GBP/USD – Buy at 1.2845

GBP/USD – 1.2963

Recent wave: Wave V of larger degree wave (III) has ended at 1.1986 and major correction has commenced from there for gain to 1.3000 and 1.3140-50

Trend: Near term up

Original strategy :

Buy at 1.2775, Target: 1.2965, Stop: 1.2715

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.2845, Target: 1.3025, Stop: 1.2785

Position: -

Target: -

Stop:-

As cable has maintained a firm undertone after rallying indicated previous resistance at 1.2965, adding credence to our bullish view that recent upmove is still in progress and upside bias remains for test of psychological resistance at 1.3000 but overbought condition should limit upside to 1.3050 and price should falter below 1.3100. We are keeping our view that the wave c as well as larger degree wave B has ended at 1.2109, hence impulsive wave C has commenced from there with wave i of C ended at 1.2616, follow by a correction to 1.2365 (end of wave ii) and wave iii rally is unfolding, hence further gain to indicated upside targets would be seen.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

On the downside, whilst initial pullback to 1.2900-10 cannot be ruled out, price should stay above indicated support at 1.2831 and bring another rise later, Only below support at 1.2757 would abort and signal a temporary top is formed instead, risk correction of recent upmove to 1.2700-10 later.

Trade Idea: GBP/JPY – Buy at 144.50

GBP/JPY - 145.80

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

Original strategy:

Buy at 142.55, Target: 145.00, Stop: 141.95

Position: -

Target: -

Stop: -

New strategy :

Buy at 144.50, Target: 146.50, Stop: 143.90

Position: -

Target: -

Stop:-

As sterling has retreated after rising to 146.70 earlier today, suggesting minor consolidation below this level would be seen and pullback to 144.90-00 cannot be ruled out, however, reckon 144.40-50 would limit downside and bring another upmove later, break of said resistance at 146.70 would extend recent rise from 135.60 to 147.00-10, however, near term overbought condition should limit upside to 147.50-60 and price should falter well below previous chart resistance at 148.45, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy sterling on pullback as 144.40-50 should limit downside. Below 143.80-90 would defer and suggest top is possibly formed, bring correction to support at 143.15, however, reckon downside would be limited to 142.50-55 and price should stay well above previous resistance at 142.10-15, bring another upmove later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

Elliott Wave View: NZDUSD Extended Correction

Revised Elliott Wave view in NZDUSD suggests the decline from 3/21 high (0.709) is unfolding as a leading diagonal Elliott Wave structure where Minute wave ((i)) ended at 0.6905, Minute wave ((ii)) ended at 0.7053, Minute wave ((iii)) ended at 0.6844, Minute wave ((iv)) ended at 0.6968. and Minute wave ((v)) of A ended at 0.6835. Pair is bouncing within Minor wave B to correct cycle from 3/21 high before the decline resumes. We don’t like buying the proposed bounce and expect sellers to appear once wave X bounce is complete in 3, 7, or 11 swing provided that pivot at 3/21 high (0.709) remains intact.

NZDUSD 1 Hour Elliott Wave Chart

Relief Rally Short-Lived As Macron Secures Presidency

It's been a lively start to trading on Monday, with the initial relief rally following Emmanuel Macron's victory in the French election quickly fizzling out as the euro and European stock markets reversed gains to trade lower on the day.

What we're seeing this morning is a classic case of the rumour – or the expected result in this case - being bought and the fact being sold. The gains over the last couple of weeks since Macron's first round victory have been substantial and it would appear the trade has exhausted itself. There were clear signs that Le Pen risk was no longer being priced in after her first round performance, with the spread between French and German 10-year yields having halved since the middle of February, back to the kind of levels we we've been seeing for the last three years.

Still, an initial relief rally on the open came as no surprise, given the potential downside in the event of an upset, but the fact that it was so short-lived shows just how priced in it was. With the euro failing to hold above a major technical resistance level against the dollar and above 1.10 – a big psychological level – questions will now be asked about the sustainability of the recent rally. A break back below 1.0850 in the coming days could trigger a much broader correction to the downside.

Oil has also been very active this morning with the opposing forces of rising US output and oil rigs, and a Saudi led push to extend the production cut beyond the middle of the year creating plenty of volatility. Brent crude rebounded strongly off its lows on Friday following a strong sell-off after breaking below $50, the very level that has capped gains this morning following an early rally. If gains continue to be capped here, it could point to further downside for Brent, possibly towards the $45 levels that we were seeing late last year.

US futures are pointing at a slightly negative start on the week, with the S&P and Dow both struggling to build on Friday's gains as they trade at the highs of the range they've been contained within since March. The S&P failed to break above 2,400 at the third time of asking on Friday and a break below 2,380 now could signal some weakness to follow for the index. The next couple of days is looking quiet from an economic event perspective, leaving traders to focus on Friday's jobs data and the French election result, while eyeing retail sales and inflation data later in the week.

Market Update – European Session: European Sentix Confidence At Highest Level Since July 2007 Aided By Decrease In Political...

Notes/Observations

Macron handily wins the French Presidential election as its European allies' breathe sigh of relief

European Sentix Confidence at highest level since July 2007 aided by decrease in political uncertainties in the euro zone

China's forex reserves rose for the third month in a row in April, signaling eased capital flight pressure.

Overnight:

Asia:

China Apr Trade Balance registers a slightly bigger surplus ($38.1B v $35.2Be) as both exports and imports underwhelm

China Apr Foreign Reserves climb to a 5-month high as its registered its 3rd straight monthly increase ($3.030T V $3.020Te (**Note: Data saw its 1st three-month rising streak since mid-2014)

Japan/China said to have agreed on need to deepen cooperation in finance and collaboration on trade and investment

sidelines of Asian Development Bank's annual meeting

Europe:

France's Macron defeats Le Pen in French Presidential Elections (66% to 34%); Turnout was the lowest since 1969

Chancellor Merkel's Christian Democrats (CDU) defeated the Social Democrats in the Schleswig-Holstein state elections; margin 33% to 26%

German Emnid Poll: Merkel's Conservative coalition extends lead in upcoming Sept elections (- CDU/CSU 36% ; SPD 28%

German Chancellor Merkel said to have expressed her dissatisfaction with EU Commission President Juncker over his Apr 26th dinner with UK PM May and Brexit-related talks

Germany said to consider proposing giving Britain access to single market in return for a fee

PM May said to accuse Juncker of hardening stance on Brexit . Must end threats designed to influence outcome of upcoming snap elections. PM said to consider publishing hard Brexit plans in event EU talks break down

UK Home Sec Rudd: EU President Tusk held very hostile briefings against PM May after April 26th dinner in deliberate attempt to influence voters Sovereign rating (Friday)

Fitch affirmed United Kingdom sovereign rating at AA; outlook Negative

S&P affirmed Italy BBB- sovereign ratings; outlook stable

S&P affirmed Turkey BB sovereign ratings; outlook negative

Canadian rating agency DBRS affirmed Norway sovereign rating at AAA, stable trend

Americas:

Fed's Bullard (non-voter, dovish): wants Fed to start trimming balance sheet in H2 this year; Fed has waited too long to reduce balance sheet

Fed's Williams (moderate, non-voter): We'll be normalizing the balance sheet sometime in the future; it makes sense to start unwinding the balance sheet later

Fed's Rosengren (moderate, non-voter): Fed will hit zero rates more often in the future; it's inevitable the Fed will need to expand balance sheet again in future. Reiterated preference is to cut balance sheet gradually and relatively soon

Energy:

Saudi Oil Min Al-Falih: OPEC cuts could extend beyond H2 of 2017; Not concerned with oil demand peaking any time soon

Economic Data

(JP) Japan Apr Consumer Confidence: 43.2 v 43.2

(DE) Germany Mar Factory Orders M/M: 1.0% v 0.7%e; Y/Y: 2.4% v 2.1%e

(NO) Norway Mar Industrial Production M/M: -0.1% v -0.6% prior; Y/Y: 1.0% v 1.2% prior

(NO) Norway Mar Manufacturing Production M/M: -1.1% v 0.5%e; Y/Y: -3.3% v -1.4% prior

(SE) Sweden May Housing Price Indicator: 69 v 67 prior

(TR) Turkey Mar Industrial Production M/M: 1.3% v 0.8%e; Y/Y: 2.8% v 2.5%e

(CN) China Q1 Preliminary Current Account: $19.0B v $11.8B prior

(UK) Apr Halifax House Prices M/M: -0.1% v +0.1%e; 3M/Y: 3.6%e v 3.8% prior

(SE) Sweden Apr Budget Balance (SEK): +4.3B v -9.1B prior

(TW) Taiwan Apr Trade Balance: $2.8B v $4.0Be, Exports Y/Y: +9.4% v +10.9%e, Imports Y/Y: +23.5% v +18.0%e

(EU) Euro Zone Apr Sentix Investor Confidence: 27.4 v 25.2e (highest since July 2007)

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.5% at 3642, FTSE flat at 7297, DAX -0.3% at 12676, CAC-40 -0.7% at 5393, IBEX-35 -0.4% at 11096, FTSE MIB -0.5% at 21376, SMI -0.3% at 8994, S&P 500 Futures %]

Market Focal Points/Key Themes European Equities trade largely lower on profit taking following the expected victory for Macron in the French election. The CAC leads the decliners down 0.6%, with the FTSE slightly higher. Shares of Centrica and Akzo Nobel down in early trade, with Akzo Nobel rejecting the 3rd increased offer from PPG, and Centrica said its on course to hit 2017 targets. French Banks are giving back some ground following the strong run up to the elections with shares of SocGen a notable decliner. Earnings will continue to dominate the corporate calender in the US today with notable earners including AES Corp, Mallinckrodt and Tyson Foods.

Equities

Consumer discretionary [Premier Foods [PFD.UK] +1.7% (Renews relationship with Mondelez)]

Materials: [Akzo Nobel [AKZA.NL] -2.2% (Rejects PPG offer),]

Industrials: [Hamburger Hafen Und Logistik [HHFA.DE] +6.1% (Raises outlook), Volkswagen [VOW3.DE] +0.1% (Royal Enfield approach for Ducati), Post NL [POST.NL] -8.2% (Earnings)]

Financials: [SocGen [GLE.FR] -2.9% (Profit taking)]

Telecom: [QSC [QSC.DE} +9.7% (Earnings)]

Energy: [Centrica [CNA.UK] -0.3% (Trading update)]

Speakers

ECB's Mersch (Luxembourg) reiterated Euro-area recovery was gathering momentum with confirmation of a broadly balanced risk outlook for growth was within reach. Saw timid signs of early pipeline inflation pressure

Moody's: President's Macron policy platform is credit positive for France. Outcome of France's legislative elections in June would be crucial in determining whether the new president was able to achieve his policy plans

China FX Regulator SAFE noted that the current account surplus was within a reasonable range and the balance of payments basically balanced in Q1 back by sound economy. Economic growth is more stable

China govt reportedly considering merging 8 companies into 3 larger power companies

FX Regulator SAFE's Pan: Reiterated view that govt to keep CNY currency (Yuan) value basically stable at a reasonable level. To further increase Yuan rate flexibility

Russia Energy Ministry: Extension of OPEC deal would accelerate market rebalancing; would support extending OPEC cuts beyond 2017. Reiterated Russian/OPEC efforts have been very effective

Currencies

The session in Asia initially saw risk-on appetite as EUR/USD tested above 1.10 level for its highest reading since early Nov as the political uncertainties in the euro zone decreased.

The European morning saw the Euro give up gains after centrist Emmanuel Macron's victory over the far-right Marine Le Pen in France's presidential elections.

South Korean KRW currency (won) was firmer ahead of presidential elections on Tuesday as leading liberal candidate Moon Jae-in seen likely to emerge victorious

Commodity prices also bounced back on the potential OPEC cut in oil production helping the AUD hold steady.

Fixed Income

Bund futurestrade at 160.63 up 25 ticks but off the highs following the cash open. A break of 160.40 support level could see lows target 159.60 followed by 159.01. Resistance remains near the 161.88 level followed by 163.54.

Gilt futurestrade at 127.81 lower by 9 ticks, after initially bouncing higher on the open. A continuation of the pullback from the 129.14 April 18th high has price eyeing the 127.50 support level. An acceleration lower could test the 126.62 region. Resistance stands at 128.49 then 128.81 followed by 129.14.

Monday's liquidity report showed Friday's excess liquidity rose to €1.650T a gain of €1B from €1.649T prior. Use of the marginal lending facility dropped to €296M from €340M prior.

Corporate issuance saw $39.0B issued last week, well ahead of last week's forecast of $25B. For the week ahead, analysts eye issuance to come in around $35B.

In Euro denominated issuance €9.7B came to market last week via 20 issuers and 21 tranches.

Looking Ahead

(MX) Mexico Apr Vehicle Production: No est v 363.7K prior; Vehicle Exports: No est v 297.6K prior

05:30 (DE) Germany to sell €2.0B in 6-month BuBills - 06:45 (US) Daily Libor Fixing

07:00 (IN) India announces details of upcoming bond sale (held on Fridays)

07:00 (CL) Chile Apr CPI M/M: 0.2%e v 0.4% prior; Y/Y: 2.7%e v 2.7% prior

07:00 (CL) Chile Apr CPI Ex Food and Energy M/M: 0.3%e v 0.4% prior; Y/Y: No est v 2.2% prior

07:25 (BR) Brazil Central Bank Weekly Economists Survey

07:30 (CL) Chile Apr Trade Balance: $0.5Be v $0.3B prior; Total Exports: $4.8Be v $5.5B prior; Total Imports: $4.4Be v $5.2B prior; Copper Exports: No est v $2.3B prior

07:30 (CL) Chile Apr International Reserves: No est v $39.0B prior

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions in week

08:15 (CA) Canada Apr Annualized Housing Starts: 215.0Ke v 253.7K prior

08:15 (UK) Baltic Dry Bulk Index - 08:30 (US) Fed's Bullard (non-voter, dovish)

08:45 (US) Fed's Mester (hawkish, non-voter)

08:50 (FR) France Debt Agency (AFT) to sell combined €5.2-6.4B in 3-month, 6-month and 12-month BTF Bills

09:00 (MX) Mexico Apr Consumer Confidence: 82.5e v 81.0 prior

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:00 (US) Apr Labor Market Conditions Index Change: 1.0e v 0.4 prior

11:30 (US) Treasury to sell 3-Month and 6-month Bills

16:00 (US) Weekly Crop Progress Report