Sample Category Title

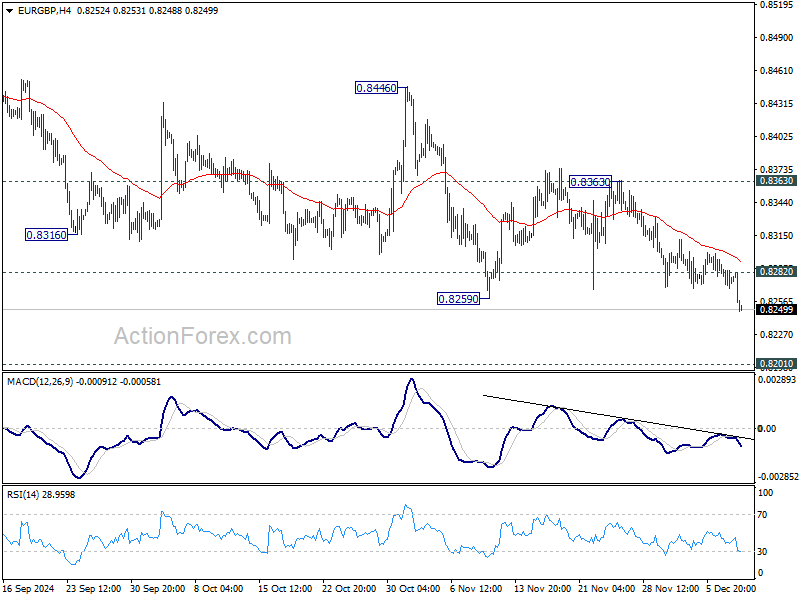

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8267; (P) 0.8279; (R1) 0.8290; More...

EUR/GBP's down trend resumed by breaking through 0.8259 low. Intraday bias is back on the downside for 0.8201 key support level next. Strong support could be seen there to bring rebound. On the downside, above 0.8282 minor resistance will turn intraday bias neutral first. Further break of 0.8363 resistance will be the first signal of bullish trend reversal. However, sustained break of 0.8201 will carry larger bearish implications.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

Euro Hits 2024 Low vs Sterling as ECB Dovish Expectations Build

Euro's selloff accelerated today, breaking to a new 2024 low against Sterling. The common currency also weakened notably against the Swiss Franc, even as it remained relatively steady against other peers. Market sentiment appears to be pricing in dovish guidance from ECB at its upcoming meeting, where a standard 25bps rate cut is expected over a more aggressive 50bps reduction.

Economic struggles in Germany and France, the bloc’s largest economies, remain at the heart of the Eurozone’s troubles. Growth momentum has faltered since mid-year, with the temporary boost from the Paris Olympics fading quickly. Political uncertainty is adding to the strain, with Germany facing policy gridlock and France grappling with ongoing governance challenges. Sentix Investor Confidence data released yesterday highlighted the extent of this economic malaise, further dampening market sentiment. Externally, the prospect of renewed US tariffs under President-elect Donald Trump looms large, posing additional threats to the Eurozone's export-reliant economies.

ECB is under pressure to support the faltering economy while balancing inflation risks. Markets are now pricing in a cumulative 152bps reduction in the deposit rate by the end of 2025, bringing it down from 3.25% to approximately 1.75%.

This anticipated pace of easing of ECB contrasts sharply with BoE's more measured approach. Despite wide dissatisfaction with the Autumn Budget, the UK government under Prime Minister Keir Starmer appears politically stable for now. BoE has signaled a cautious path forward, likely implementing only four rate cuts next year, leaving Sterling better positioned relative to the Euro.

Across the Atlantic, Fed is expected to deliver another 25bps rate cut in December. However, a pause in January seems increasingly likely as the Fed assesses the economic implications of incoming policies from the Trump administration. Expected inflationary pressures from fiscal stimulus and trade measures are likely to temper Fed’s pace of easing, supporting a relatively firmer Dollar.

Overall in the currency markets, Aussie and Kiwi remain the weakest performers of the day, driven by RBA’s dovish shift and fading optimism over China’s latest economic stimulus pledges. In contrast, Loonie leads the pack, followed by Sterling and Dollar while Yen and Swiss Franc are positioning in the middle.

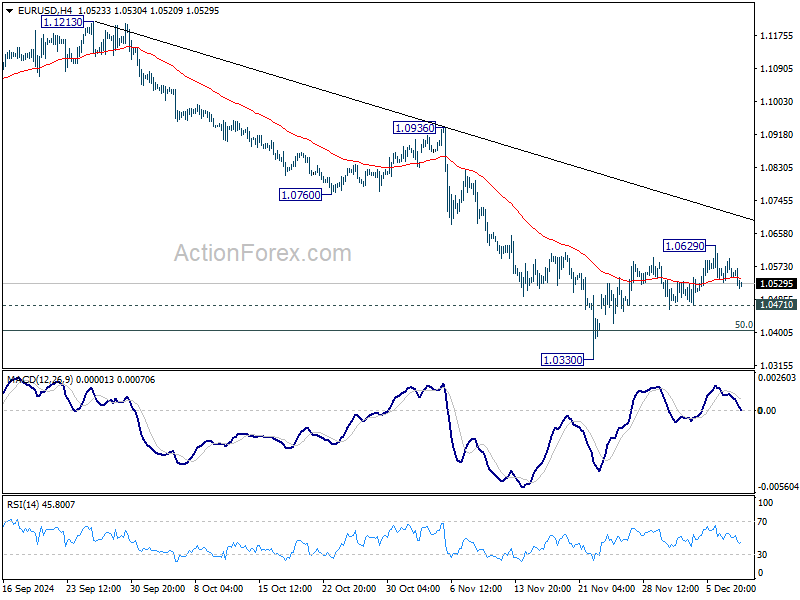

Technically, EUR/USD would be a focus in the next two days, with US CPI and ECB rate decision on agenda. Price actions from 1.0330 are so far corrective looking which suggests that fall from 1.1213 is still in progress. Break of 1.0471 minor support will argue that the corrective recovery has completed, and target 1.0330 and below.

In Europe, at the time of writing, FTSE is down -0.64%. DAX is up 0.08%. CAC is down -0.70%. UK 10-year yield is up 0.035 at 4.315. Germany 10-year yield is down -0.001 at 2.216. Earlier in Asia, Nikkei rose 0.53%. Hong Kong HSI fell -0.50%. China Shanghai SSE rose 0.59%. Singapore Strait Times rose 0.49%. Japan 10-year JGB yield rose 0.024 to 1.066.

RBA holds rates steady, dovish shift raises odds of Feb cut

RBA held its cash rate steady at 4.35% as widely expected, but the accompanying statement marked a clear pivot towards a more dovish stance. While May remains the more likely timing for the first rate cut, February is now emerging as a real possibility, depending on upcoming Q4 jobs and inflation data from Australia.

The most striking change in the RBA's statement was its removal of the phrase "not ruling anything in or out" regarding future monetary policy decisions. This change aligns with the board's growing "confidence that inflationary pressures are declining." RBA acknowledged that some upside risks to inflation have eased and noted the gap between aggregate demand and supply capacity is continuing to narrow.

Recent activity data, according to the RBA, has been “on balance softer than expected,” with the central bank pointing out risks of a slower-than-anticipated recovery in consumer spending. These factors collectively suggest a step away from inflation vigilance and a move closer to easing policy.

Governor Michele Bullock later emphasized that the wording adjustments in the statement were deliberate. While she clarified that a rate cut was not discussed during today's meeting, she acknowledged uncertainty over whether one could occur as early as February.

Markets responded swiftly, with swaps traders raising the probability of a February rate cut to over 60%, up from 50% the previous day. Market expectations now fully price in two rate reductions by May.

Australia’s NAB confidence turns negative to -3 as business conditions deteriorate

Australia’s NAB Business Confidence index slid sharply to -3 in November, down from 5 in October, returning to below average levels. Business conditions also weakened notably, dropping from 7 to 2, marking declines across trading, profitability, and employment metrics. Trading conditions fell to 5 from 13, profitability shifted into negative territory at -1 from 5, and employment conditions edged down to 2 from 3.

Cost pressures showed little relief, with input costs largely unchanged. Labor cost growth held steady at 1.4% in quarterly terms, while purchase cost growth edged slightly higher by 0.2 percentage points to 1.1%. On the pricing side, output price growth remained unchanged at 0.6% in quarterly terms, with retail price growth retreating to 0.6% and recreation and personal services easing slightly to 0.7%.

China's trade data highlights persistent import weakness amid export slowdown

China's trade data for November showed weak signals as exports grew 6.7% yoy to USD 312.3B, down sharply from October's 12.7% yoy expansion and missing expectations of 8.5% growth.

Export performance varied across key regions, with shipments to the US rising 8% yoy, to the EU up 7.2% yoy, and to ASEAN growing by 14.9% yoy. However, exports to Russia declined by -2.5% yoy.

On the import side, the picture was decidedly more negative. Imports fell by -3.9% yoy, marking the steepest decline since September 2023, and missing expectations of a slight 0.3% yoy increase.

Weakness was broad-based, with imports from ASEAN dropping -3% yoy, the US contracting by -11% yoy, and the EU and Russia both registering declines of -6.5% yoy. These numbers underscore persistent weak domestic demand, consistent with recent data showing subdued consumer inflation.

Trade balance widened from USD 95.7B to 97.4B, above expectation of USD 92.0B.

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8267; (P) 0.8279; (R1) 0.8290; More...

EUR/GBP's down trend resumed by breaking through 0.8259 low. Intraday bias is back on the downside for 0.8201 key support level next. Strong support could be seen there to bring rebound. On the downside, above 0.8282 minor resistance will turn intraday bias neutral first. Further break of 0.8363 resistance will be the first signal of bullish trend reversal. However, sustained break of 0.8201 will carry larger bearish implications.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

German Inflation Rises, Euro Edges Higher

The euro is slightly higher on Tuesday. In the European session, EUR/USD is trading at 1.0528, down 0.23% at the time of writing.

German inflation climbs to 2.2%

Germany, the largest economy in the eurozone, remains a shadow of what was once the undisputed locomotive of Europe. Economic growth has sputtered and there is political instability, with an election called in February 2025 after the coalition government collapsed in November.

German inflation rose to 2.2% y/y in November, up from 2% in October and matched the preliminary estimate. This was the highest level in four months. Service inflation was unchanged at 4%, double the European Central Bank’s target of 2%. Core inflation, which excludes volatile food and energy prices, rose to 3%, a six-month high. The inflation data raises hopes that the German economy may be showing signs of stronger activity.

Today’s inflation report comes just two days before the ECB rate announcement. The markets have fully priced in a rate cut, with around an 85% probability of a 25-basis point cut. There is around a 15% possibility of a jumbo 50-bp cut, although hawkish members such as Isabel Schnabel favor a gradual approach of 25-bp increments.

If the ECB lowers rates on Thursday, as expected, it will mark the fourth rate cut this year. The ECB has shown that it is willing to cut rates but there are some dark clouds that may force the ECB to be even more aggressive. France is in political turmoil after the government fell last week and there is the burning question of whether President-elect Trump will make good on his promise to slap US trading partners with tariffs. The fragile eurozone economy runs a real risk of tipping into a recession and ECB policymakers will have to balance the weak economy against the upside risk of inflation in determining how fast to cut interest rates.

EUR/USD Technical

- EUR/USD is testing support at 1.0526. Below, there is support at 1.0497

- There is resistance at 1.0560 and 1.0589

Gold (XAU/USD) Eyes $2,700 as Fed Rate Cut Looms, Geopolitics in Focus

- Gold prices are being supported by a shift in Chinese monetary policy, and geopolitical developments.

- China has resumed gold purchases after a six-month pause.

- From a technical perspective, gold is currently caught between support at $2650 and resistance at $2700. A break above $2700 could signal further upside potential.

Gold has started the week on the offensive as the stars have somewhat realigned for the precious metal. The regime change and geopolitical developments in Syria coupled with a Chinese monetary policy shift and a weaker US Dollar has reignited the appeal of the precious metal.

There was also the announcement by China that they would be starting a probe in AI leader Nvidia, over alleged anti-monopoly law. This could be seen as a sign of what is to come from a trade war moving forward between the US and China and has added to the haven demand narrative.

Together with Friday’s US jobs data, markets have also come to terms with another 25 bps rate cut by the Fed in December. This is also underpinning Gold prices and is likely to limit downside potential.

China Resumes Gold Purchases

China, who had been a major buyer of Gold this year but remained on the sidelines since May, has resumed Gold purchases. The People’s Bank of China said on Saturday that it bought 160,000 troy ounces of gold in November. This ends a six-month break in purchases.

What followed was the announcement yesterday regarding the loosening of monetary policy by the Politburo. This comes as Chinese inflation data remained weak, highlighting slow demand. Markets will no doubt be hoping that stimulus will lead to an uptick in demand and keep the Chinese Central Bank buying the precious metal.

US Dollar to Continue Poor December Performance?

The US Dollar has had a mixed December so far as it looks to buck its historic trend of poor performance in December. The index is advancing this week and this could also be down to its haven appeal.

It may be that the rate cut in December has largely been priced in and thus the US Dollar is experiencing a rally. I think the closer we get to the Christmas break is when the US Dollar will really be tested. As institutions begin to close shop for the festive break, many will look to reposition themselves and their portfolios ahead of 2025.

The US Dollar is primed to enjoy a positive 2025 but we may still see some volatility the closer we get to Christmas.

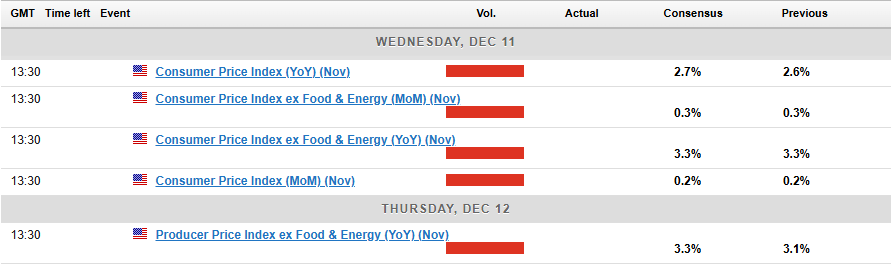

Looking ahead and the biggest impact on Gold this week from a data perspective is likely to come from US CPI numbers out on Wednesday.

The print is unlikely to alter the Fed decision on December 18, but it could stoke some short-term price swings and volatility.

Technical Analysis Gold (XAU/USD)

From a technical analysis standpoint, Gold on a daily timeframe is trading above the range it held last week but below a key resistance area around the 2675 handle.

Immediate support from the range break rests at 2656-2660 which for now appears to be holding firm and thus supporting a bullish narrative.

I would say caution will be key as the precious metals may face a host of challenges gaining acceptance above the 2700 handle once more.

Immediate resistance rests at 2675 and 2685 before the 2700 handle grabs the attention.

Are we going to see more choppy price action like last week, or will the geopolitical risk drive the bullish rally beyond the 2700 handle?

Gold (XAU/USD) Daily Chart, December 10, 2024

Source: TradingView (click to enlarge)

Support

- 2656

- 2639

- 2624

Resistance

- 2675

- 2685

- 2700

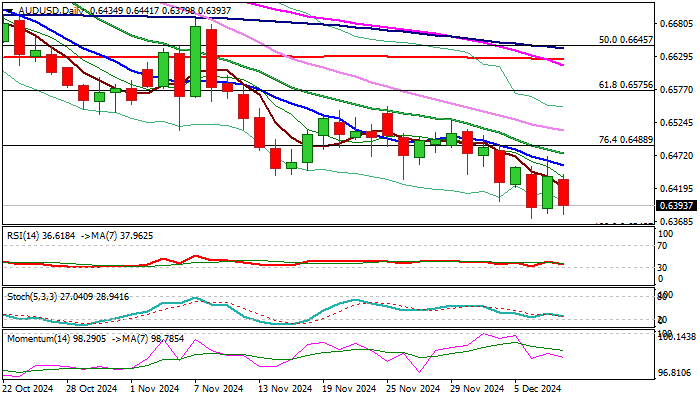

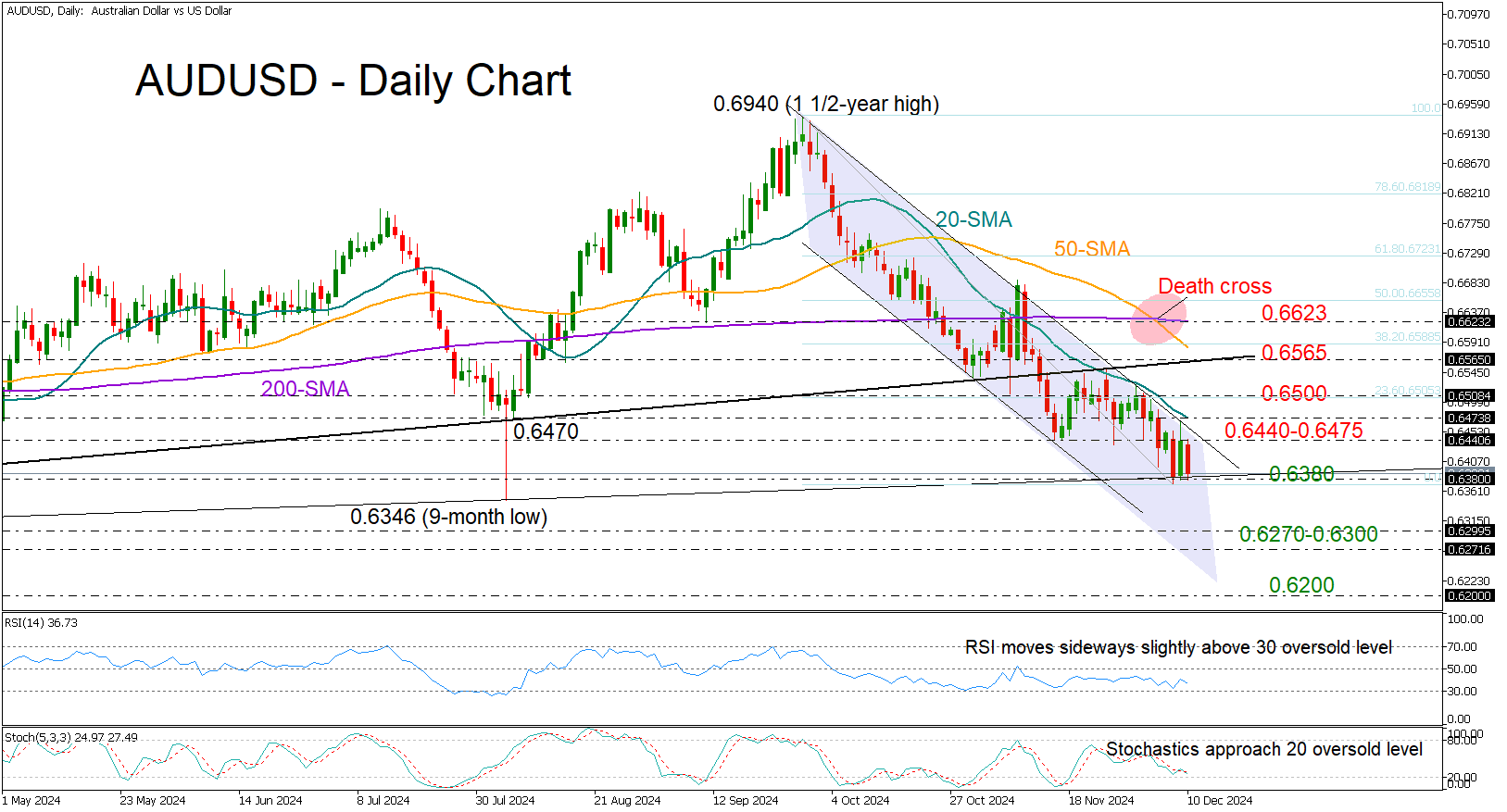

AUD/USD Outlook: Dips on Signals of RBA’s Dovish Shift

AUDUSD fell on Tuesday morning after RBA kept interest rates unchanged at 4.35% but softened it hawkish tone ( on not ruling anything in or out) from the previous meeting that revived expectations for possible rate cut in February.

Recent economic data showed surprisingly weak economic growth in the third quarter, while the central bank showed some confidence that inflation remains on a steady path towards the target, contributing to the latest dovish shift in monetary policy outlook and subsequently add pressure on Aussie dollar.

Markets turn focus on Wednesday’s release of US CPI data, which would also contribute to AUD’s near term action.

Daily chart structure remains in firmly bearish, after Monday’s recovery attempts were capped by falling 10DMA (bull trap), 14-d momentum holds in the negative territory for two months, MA’s are in full bearish setup, with the latest formation of 55/200DMA death cross, adding pressure.

Bears eye targets at 0.6362 (Apr 19 low) and 0.6348 (2024 low, posted on Aug 5), violation of which would open way towards 0.6300 (psychological) and 0.6270 (2023 low).

Near-term bias remains firmly with bears while the price action stays below falling 10DMA (0.6456).

Res: 0.6440; 0.6456;0.6488; 0.6530.

Sup: 0.6372; 0.6362; 0.6348; 0.6300.

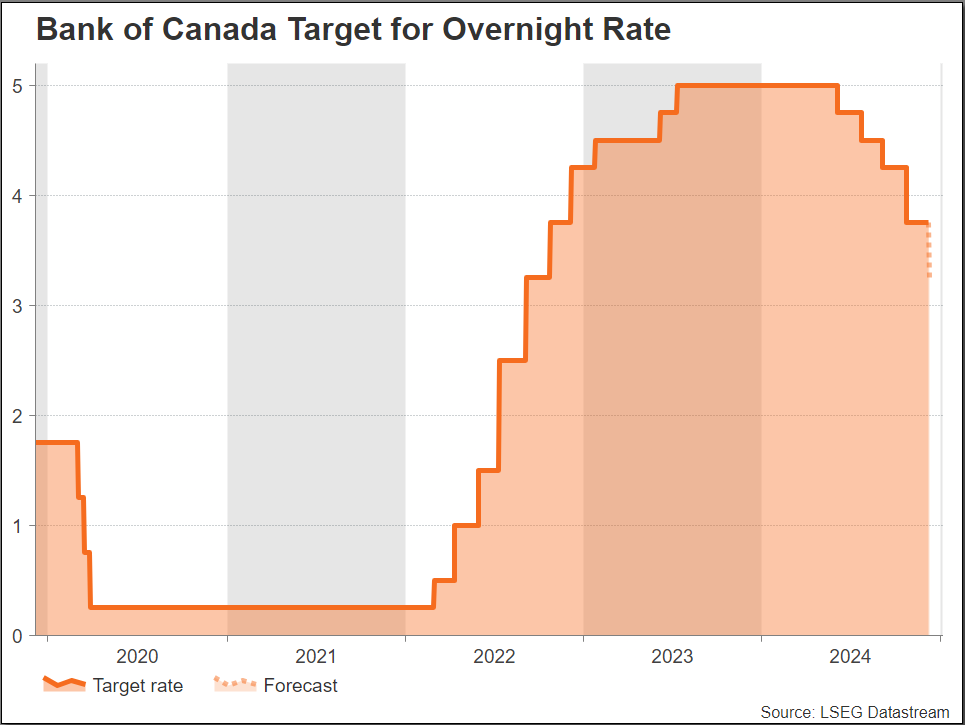

BoC Decision: Another Rate Cut for the Final Policy Meeting of 2024

- Will the BoC deliver a single or double rate cut?

- BoC announces on Wednesday, at 14:45 GMT

- Loonie could probably be affected

One more rate cut before the year-end

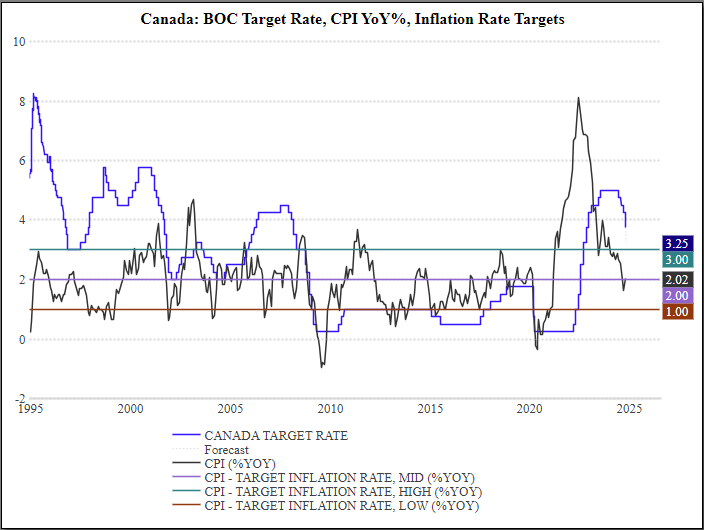

On Wednesday, the Bank of Canada (BoC) will make its final interest rate decision for 2024. Financial markets and economists are widely anticipating another rate cut, with the consensus leaning toward a reduction of 50 basis points, bringing the policy rate down from 3.75% to 3.25%.

The BoC has already made significant cuts this year, including a 50-basis-point reduction in October. Several factors, including the latest job report that revealed weaker-than-expected employment growth, influence the decision to further cut rates. This has increased the likelihood of a more aggressive rate cut to support the economy.

Economic Outlook for 2024

Looking ahead to 2024, the BoC projects a gradual improvement in economic growth. The central bank's October Monetary Policy Report forecasts GDP growth to pick up slowly, with inflation expected to remain around the 2% target. Core inflation is anticipated to decline gradually, reflecting easing price pressures in various sectors. The BoC's outlook suggests that further rate cuts may be necessary to sustain economic momentum and achieve the BoC’s inflation target.

Several key factors are influencing the BoC's decision-making process. Recent data shows that inflation has been relatively stable, but the Bank remains cautious about potential upward pressures. The labor market has shown signs of weakness, prompting concerns about economic growth. Policymakers are also considering the broader global economic environment, including the policies of other central banks like the Federal Reserve and the European Central Bank (ECB). Additionally, housing market trends, consumer spending, and business investment are all critical factors that the BoC monitors closely.

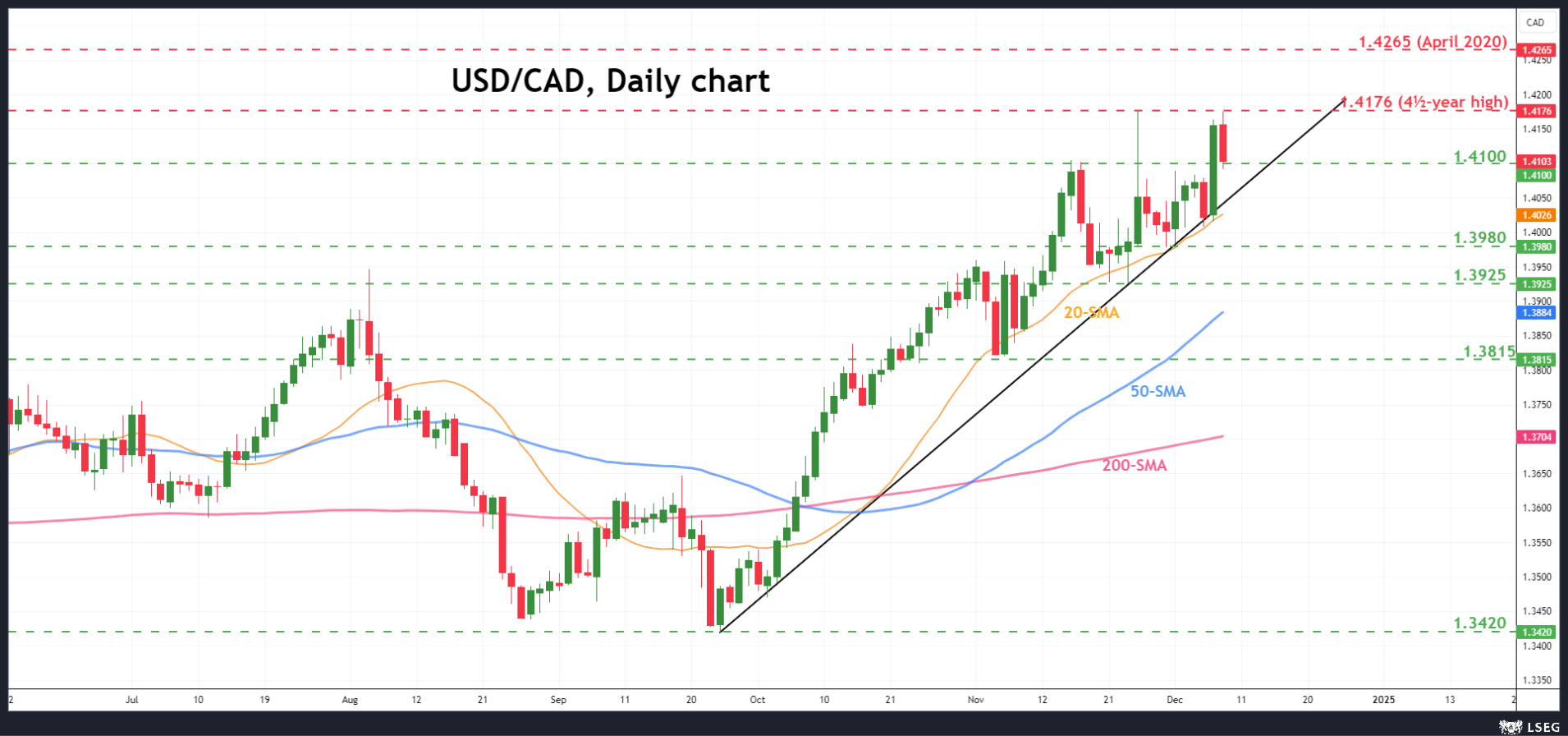

Impact on USD/CAD

The rate cut is likely to affect the dollar/loonie, potentially leading to a depreciation of the loonie. The pair reached the four-and-a-half-year high of 1.4176 early on Monday, endorsing the bullish outlook, with the next resistance coming from the April 2020 peak at 1.4265. Otherwise, a drop below the significant support line of the 20-day simple moving average (SMA) may show signs of a negative retracement until the 1.3980 and 1.3925 support levels.

AUDUSD Flips Back to Recent Lows After RBA’s Decision

- AUDUSD gives up gains after RBA’s inflation comments

- Trend signals remain negative, support is nearby at 0.6380

AUDUSD erased Monday’s rebound following the Reserve Bank of Australia’s (RBA) well anticipated decision to keep interest rates unchanged at 4.35%. The central bank’s comments on easing inflation pressures led investors to bet on a rate cut as early as February, adding pressure on the aussie.

The pair pulled below the 0.6440 barrier to trade again near the 0.6380 area, where the familiar support trendline from 2022 is sitting. The RSI and the stochastic oscillator are approaching their oversold levels, suggesting selling interest could soon fade out. However, if that floor cracks, the next pivot point could be found within the critical 0.6270-0.6300 territory last seen in October 2023. A continuation lower could pause within the 0.6170-0.6200 zone taken from October 2022.

For the bulls to regain control, the pair may have to run sustainably above the bearish channel and the 20-day simple moving average (SMA) at 0.6470. If such efforts prove successful, the door could open for the 0.6500 round mark and then for the 0.6565 constraining zone, where the broken support trendline from October 2023 is located. Additional gains from there would officially declare a bullish trend reversal in the short-term picture, bringing the 200-day SMA next into view at 0.6620. However, with the 50-day SMA crossing recently below the 200-day SMA for the first time since April 2023, hopes for a trend reversal could stay muted.

All in all, AUDUSD continues to face a bearish outlook in the short-term picture, though another recovery attempt or a consolidation phase cannot be ruled out as the price seems to be approaching oversold territory.

Japanese Yen Weakens as USD/JPY Climbs Amid BoJ Rate Hike Uncertainty

The USD/JPY pair reached a high of 151.07 on Tuesday, marking its highest level in a week. This movement is largely attributed to ongoing uncertainty regarding the timing of the next interest rate hike by the Bank of Japan (BoJ). The market remains split on whether the BoJ will implement a rate increase in December or delay it until January.

Recent statements from BoJ Governor Kazuo Ueda highlighted that a rate hike is imminent, based on stable economic indicators aligning with expectations. Contrarily, BoJ policymaker Toyoaki Nakamura expressed concerns over the sustainability of wage growth and signs of economic weakening in Japan, adding layers of uncertainty that are influencing market dynamics.

Recent GDP data for Japan showed a growth of 0.3% quarter-on-quarter in Q3, surpassing the expected 0.2% increase. This stronger-than-anticipated economic performance supports a more aggressive stance on future monetary policy adjustments by the BoJ.

Looking ahead, the full scope of the BoJ's monetary policy for 2025 remains unclear, but increased pressure is expected as the Federal Reserve's fiscal adjustments set a significant pace for change.

Technical analysis of USD/JPY

H4 chart: USD/JPY found support at 149.35 and has since been on an upward trajectory. The pair recently breached the 151.00 level, indicating potential for further gains towards 152.50. Currently, a narrow consolidation range has formed around 151.00. Should there be a downward exit from this range, a corrective move to 149.90 might follow. Conversely, an upward break could see the continuation of the upward wave to 152.50, potentially extending to 153.30. The MACD indicator supports this bullish outlook, with its signal line below zero but ascending sharply.

H1 chart: the market has established a consolidation range around 151.00. A downward exit from this range could lead to a correction towards 149.90. If the pair breaks upwards, it is expected to continue the upward wave towards 152.50. Upon reaching this target, a possible correction back to 149.90 may occur. The Stochastic oscillator aligns with this analysis, showing the signal line below 50 and heading towards 20, indicating potential downward movement before resuming upward momentum.

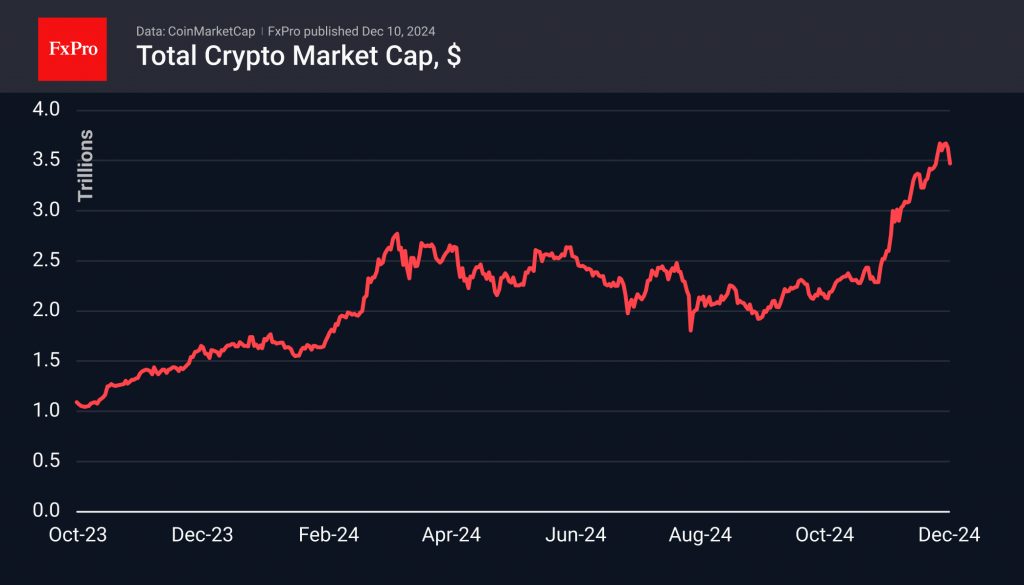

Crypto Market Spooked by Another Bitcoin Pullback Below 100K

Market Picture

Crypto market capitalisation has fallen 4% in the last 24 hours to 3.4 trillion, taking a hit from another failed attempt by Bitcoin to break above 100k. As one would expect, the failure of the leading coin to grow is sparking hesitation among supporters of smaller and more volatile coins.

The Cryptocurrency Fear and Greed Index is at 78 (extreme greed), as it was the day before, but it now looks like a lagging indicator that doesn’t account for the latest dip.

The bulls in Bitcoin once again failed to consolidate above 100K on Monday, which was followed by an impressive sell-off, bringing the price to 94K at the lowest point. There is still a wall of orders clearly visible intraday, keeping the price below 95K for a long time, but the interest in selling above 100K remains unsatisfied until the end.

We still see the potential for the first cryptocurrency to rise into the 120K area once it overcomes resistance at 100k.

News Background

According to CoinShares, global investment in crypto funds rose to an all-time high of $3.851bn last week, renewing the record set two weeks ago. The positive trend continued for the ninth consecutive week. Bitcoin investments rose by $2.546 billion; Ethereum rose to an all-time high of $1.16 billion; XRP rose by a record $134 million; and Solana fell by $14 million.

MicroStrategy bought an additional 21,550 BTC for $2.1 billion at an average price of $98,783, founder Michael Saylor said. MicroStrategy now owns 423,650 BTC, purchased for $25.6 billion at an average price of $60,324 per coin.

Since 8 November, long-term investors have reduced their positions by 827,783 BTC (~$81.2 billion), which was only 30% offset by MicroStrategy and spot ETF purchases. The rest was bought up by short-term holders who are actively leveraged and vulnerable to falling quotes.

BlackRock highlighted Bitcoin’s potential as a new diversification tool alongside gold in its Global Outlook 2025. The limited supply of coins and growing investor demand drive BTC’s potential.

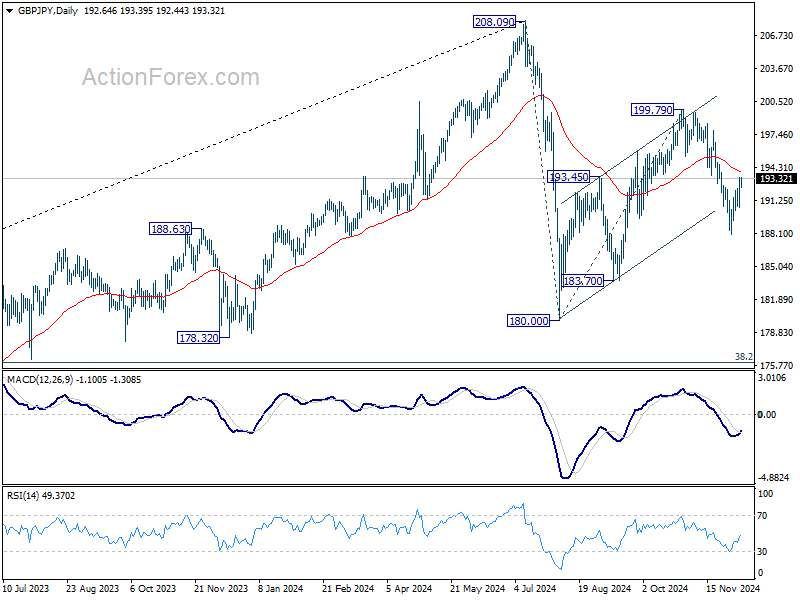

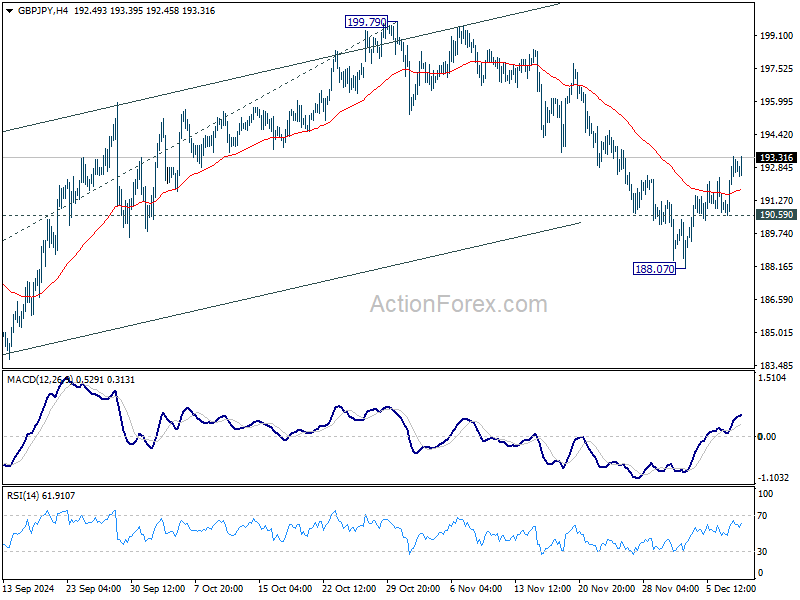

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.15; (P) 192.28; (R1) 193.96; More...

Intraday bias in GBP/JPY stays neutral for the moment. Recovery from 188.07 might extend higher. But outlook will stay bearish as long as 55 D EMA (now at 193.97) holds. On the downside, below 190.59 minor support will bring retest of 188.07 first. Break there will target 183.70 support next.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.