Sample Category Title

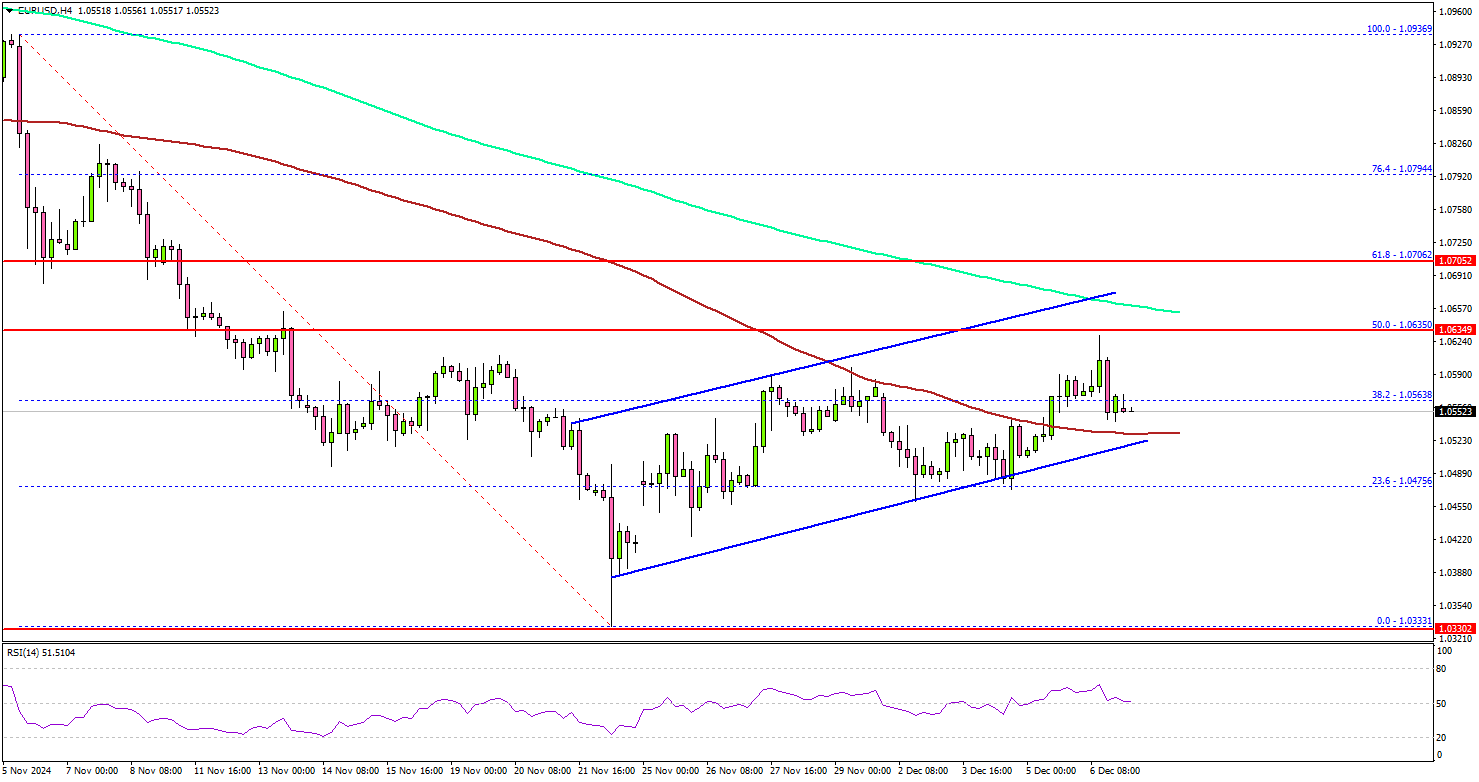

EUR/USD Under Pressure: Resistance Levels Hold Firm

Key Highlights

- EUR/USD started a recovery wave above the 1.0520 resistance zone.

- A key rising channel is forming with support near 1.0500 on the 4-hour chart.

- GBP/USD is attempting to recover above the 1.2750 resistance zone.

- Crude Oil prices are again moving lower and might decline below $66.50.

EUR/USD Technical Analysis

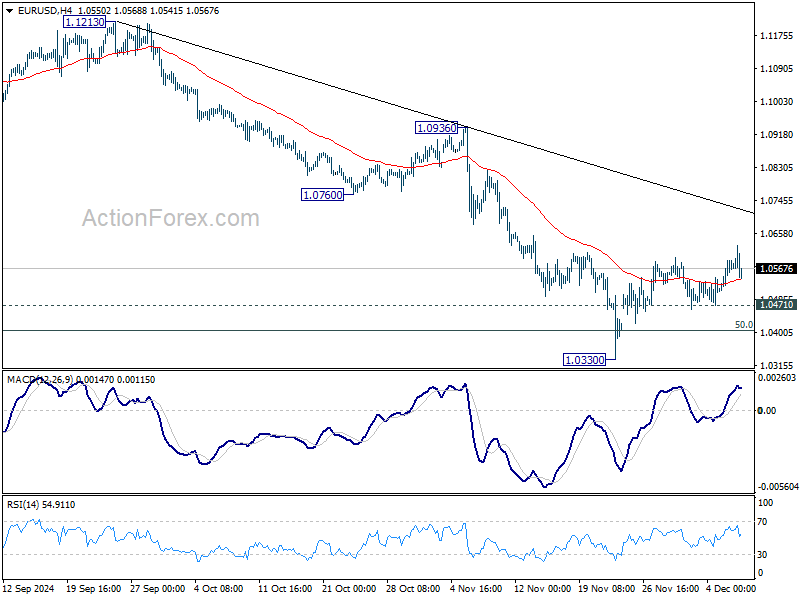

The Euro started a recovery wave above the 1.0450 and 1.0500 levels against the US Dollar. EUR/USD climbed above 1.0520 to move into a short-term positive zone.

Looking at the 4-hour chart, the pair surpassed the 38.2% Fib retracement level of the downward move from the 1.0936 swing high to the 1.0333 low. The pair recovered above the 1.0600 resistance level and the 100 simple moving average (red, 4-hour).

On the upside, the pair could face resistance near the 1.0635 level. It is close to the 50% Fib retracement level of the downward move from the 1.0936 swing high to the 1.0333 low.

The first major resistance is near the 1.0665 level and the 200 simple moving average (green, 4-hour). A close above the 1.0665 level could set the tone for another increase. The next major resistance could be the 1.0800 level, above which the price could climb higher toward the 1.0880 resistance.

On the downside, immediate support sits near the 1.0520 level. The next key support sits near the 1.0450 level. Any more losses could send the pair toward the 1.0420 level.

Looking at Oil, the bears remained in action below the $72.50 resistance, and they might aim for a drop below $65.00 in the near term.

Upcoming Economic Events:

- US Wholesale Inventories for Feb 2024 (preliminary) – Forecast +0.2%, versus +0.2% previous.

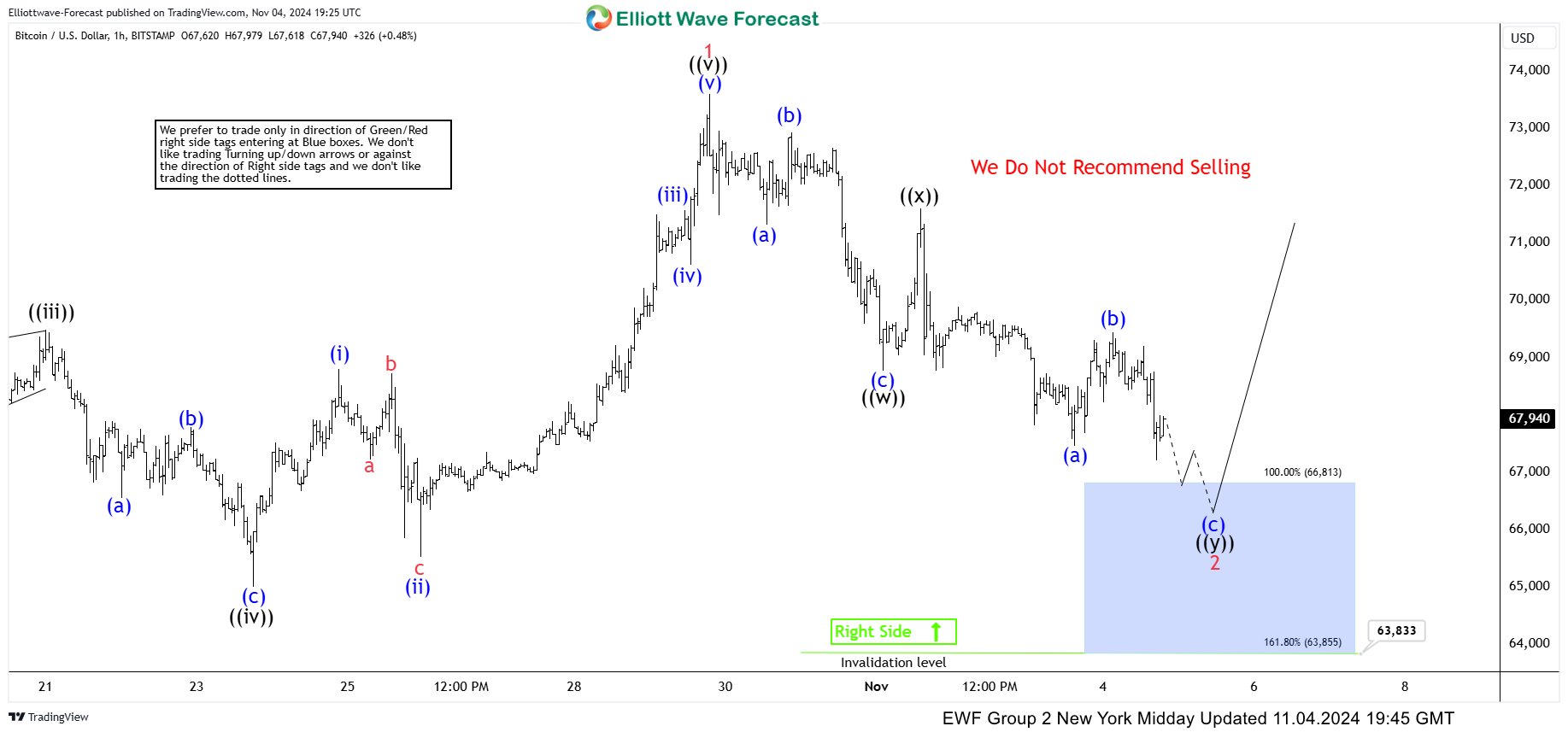

Bitcoin BTCUSD Gained 50% from Our Buying Zone – Here’s How We Did It

In this article we’re going to take a quick look at the Elliott Wave charts of Bitcoin BTCUSD published in members area of the website. As our members know BTCUSD is showing impulsive bullish sequences in the cycle from the 52598 low , that are calling for a further strength. Recently we got a pull back that has ended at the Blue Box zone,our buying area. In the further text we are going to explain the Elliott Wave Forecast and trading setup.

BTCUSD Elliott Wave 1 Hour Chart 11.04.2024

BTCUSD is giving us correction that is unfolding as a Elliott Wave Double Three pattern. At the moment structure is still incomplete. Pull back shows lower low sequences. Bitcoin can see more downside toward 66813-63855 blue box ( buying zone). We don’t recommend selling Bitcoin and prefer the long side. From the marked zone, BTCUSD should ideally make either rally toward new highs or in 3 waves bounce alternatively. Once bounce reaches 50 Fibs against the ((x)) black high , we will make long position risk free ( put SL at BE) and take partial profits.

Quick reminder on how to trade our charts :

Red bearish stamp+ blue box = Selling Setup

Green bullish stamp+ blue box = Buying Setup

Charts with Black stamps are not tradable. 🚫

Bitcoin ( BTCUSD ) Elliott Wave 1 Hour Chart 11.06.2024

BTCUSD made an extension toward our buying zone: 66,813–63,855. The crypto found buyers at the Blue Box as expected, and we got a good reaction from there. Bitcoin made an impulsive rally that broke to new highs. As a result, traders who entered long positions are now enjoying risk-free profits. With the price holding above the 66,797 low, we expect further strength to follow.

Dear traders, before you sign up, reach out to our sales department at vlada@elliottwave-forecast.com. We’ll make sure you’re getting the best deal possible with exclusive discounts and offers. Don’t hesitate—send us an email and let’s get you some savings

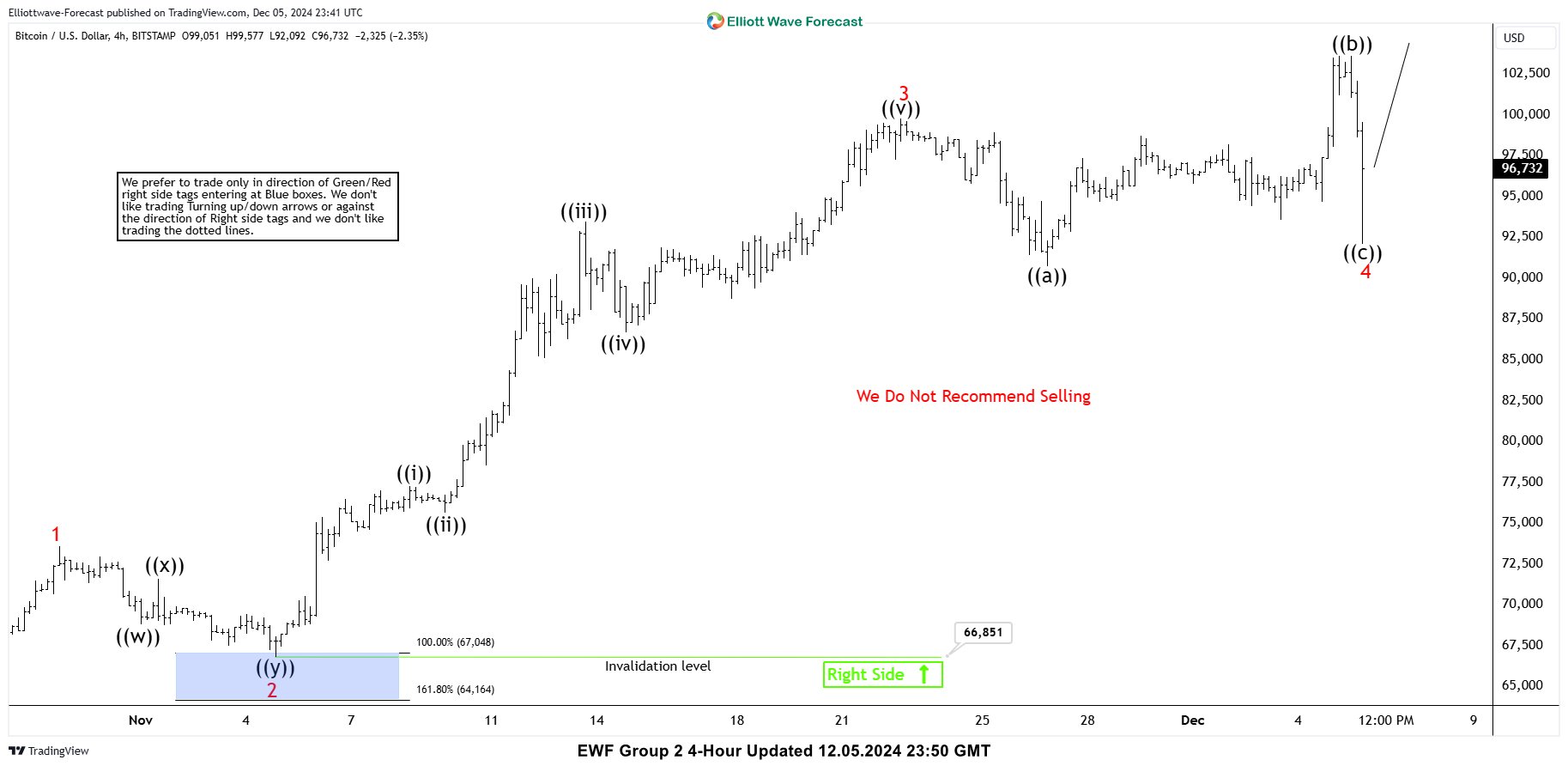

Bitcoin ( BTCUSD ) Elliott Wave 1 Hour Chart 12.05.2024

One month later, we can see that Bitcoin made further gains, just like we expected. The price kept pushing higher, breaking through key resistance levels and reaching new highs. Traders who stuck with their long positions are now enjoying solid profits. The strength we’re seeing now suggests that there could be even more upside ahead.

WTI Crude Oil Wave Analysis

- WTI crude oil broke support zone

- Likely to fall to support levels 66.6 and 66.00

WTI crude oil today broke the support zone lying at the intersection of the support level 67.60 and the support trendline of the daily Triangle from September.

The breakout of this support zone should add to the bearish pressure on WTI crude oil in the coming trading sessions.

Given the strong multi-month downtrend, WTI crude oil can be expected to fall toward the next support levels 66.6 and 66.00.

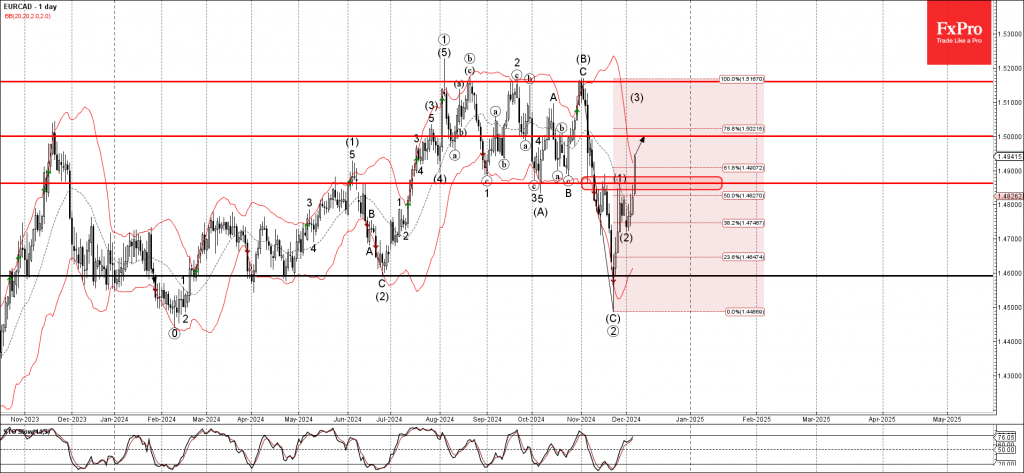

EURCAD Wave Analysis

- EURCAD broke resistance zone

- Likely to rise to resistance level 1.5000

EURCAD currency pair recently broke the resistance zone located between the resistance level 1.4865 (which has been reversing the pair from the middle of November) and the 50% Fibonacci correction of the downward impulse wave C.

The breakout of this resistance zone accelerated the active intermediate impulse wave (C).

Given the clear daily uptrend and the strongly bearish CAD sentiment seen today, EURCAD currency pair can be expected to rise toward the next round resistance level 1.5000.

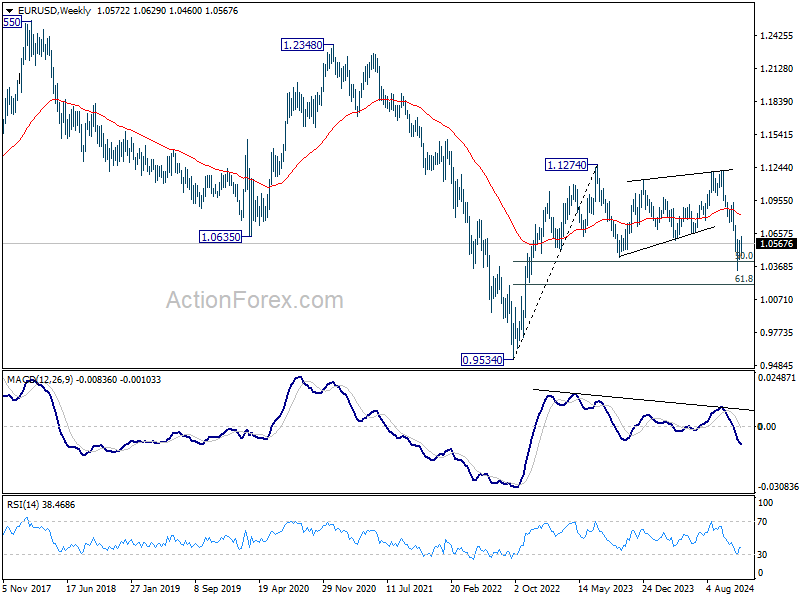

EUR/USD Weekly Outlook

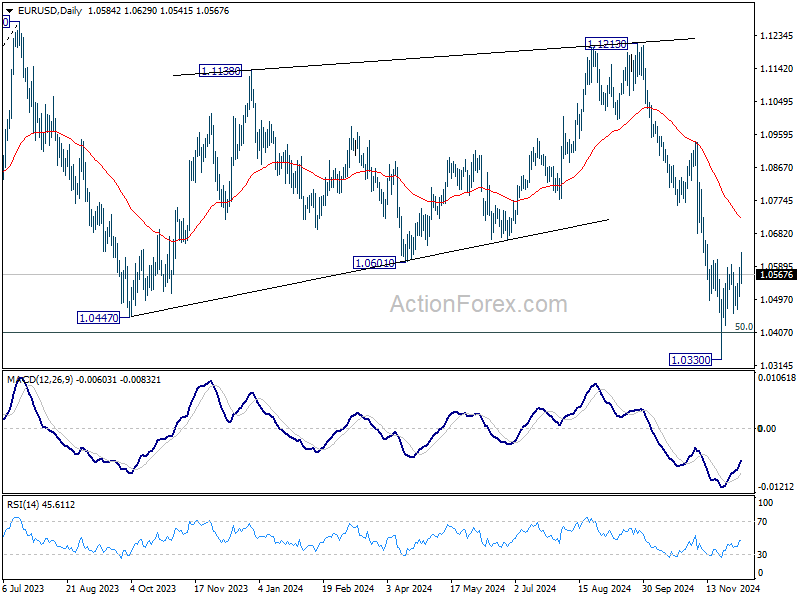

EUR/USD's rebound from 1.0330 short term bottom extended higher last week. Initial bias is mildly on the upside this week for further rise to 55 D EMA (now at 1.0729). But strong resistance could be seen there to limit upside. On the downside, break of 1.0471 minor support will turn bias to the downside for retesting 1.0330 low. Firm break of 1.0330 will resumed the decline from 1.1213, and sustained trading below 1.0404 key fibonacci level will carry larger bearish implication.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

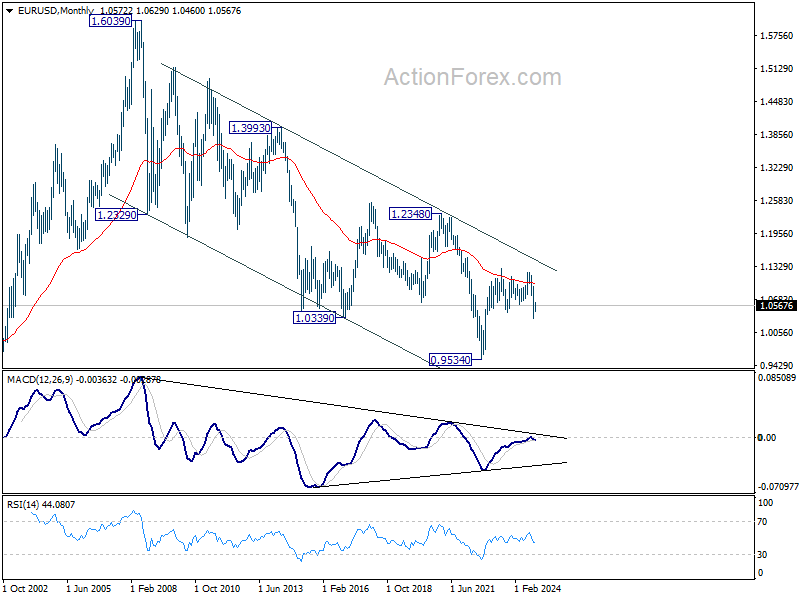

In the long term picture, down trend from 1.6039 remains in force with EUR/USD staying well inside falling channel, and upside of rebound capped by 55 M EMA (now at 1.0981). Consolidation from 0.9534 could extend further and another rising leg might be seem. But as long as 1.1274 resistance holds, downside breakout would be mildly in favor.

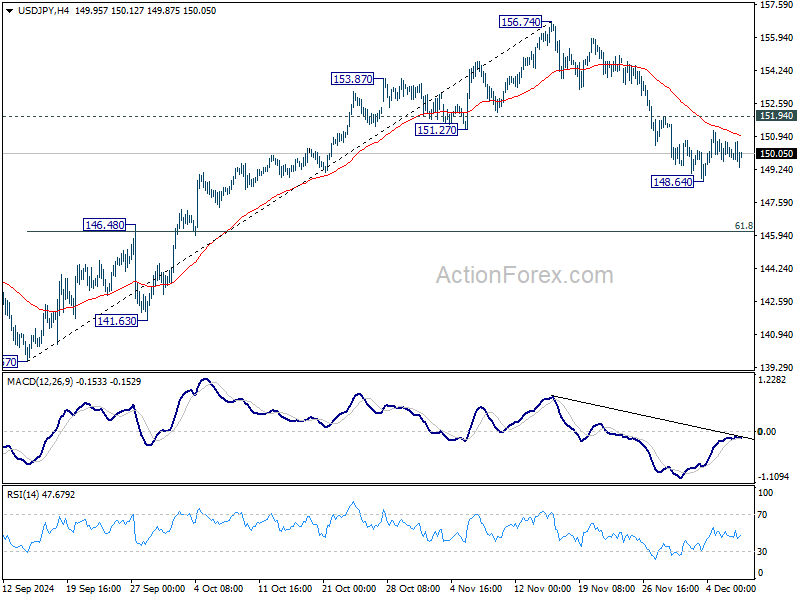

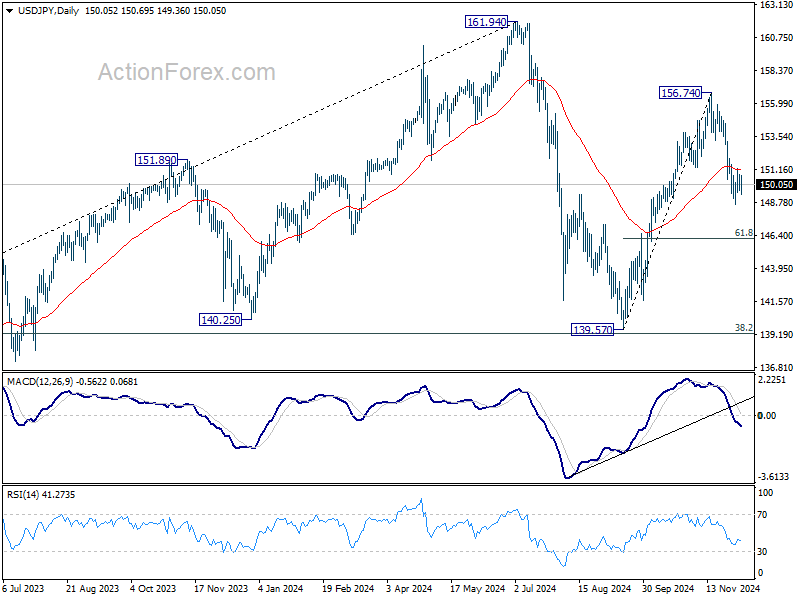

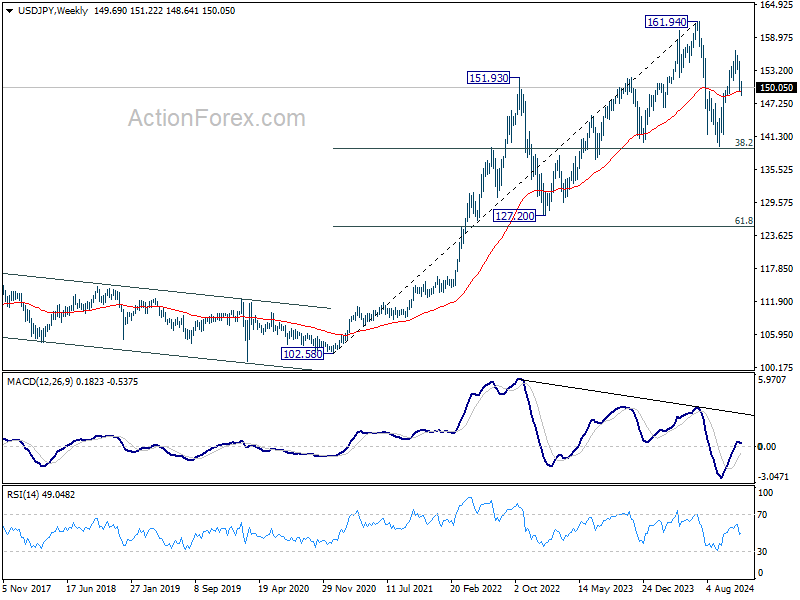

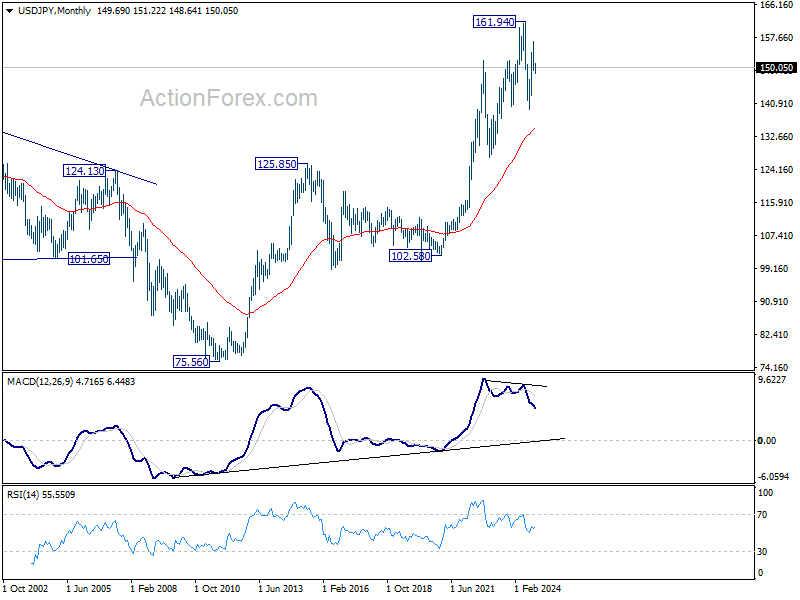

USD/JPY Weekly Outlook

USD/JPY edged lower to 148.64 last week but turned sideway since then. Initial bias stays neutral this week first, and further fall is in favor as long as 151.94 resistance holds. On the downside, below 148.64 will strengthen the case that rise from 139.57 has already completed at 156.754. Deeper fall should then be seen to 61.8% retracement of 139.57 to 156.74 at 146.12 next. Nevertheless, firm break of 151.94 resistance will revive near term bullishness and bring retest of 156.74 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

In the long term picture, it's still early to conclude that up trend from 75.56 (2011 low) has completed. However, a medium term corrective phase should have commenced, with risk of deep correction towards 55 M EMA (now at 134.98).

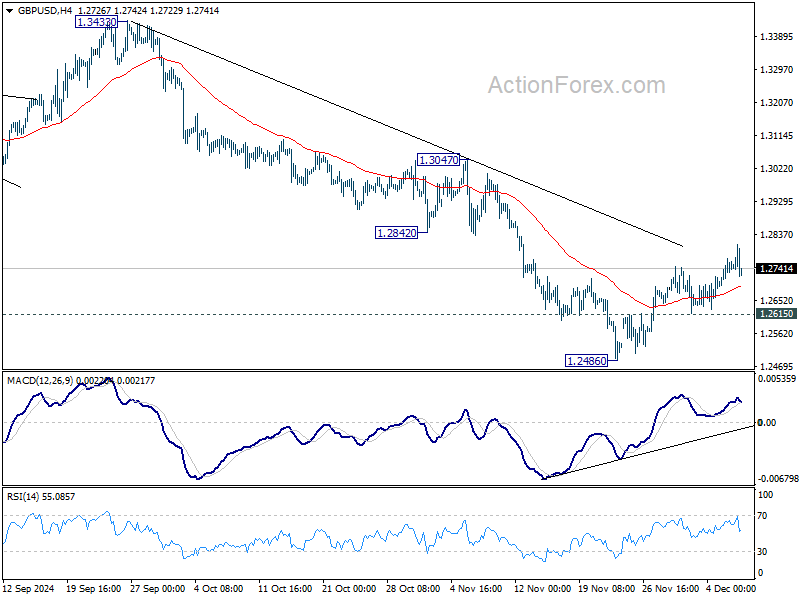

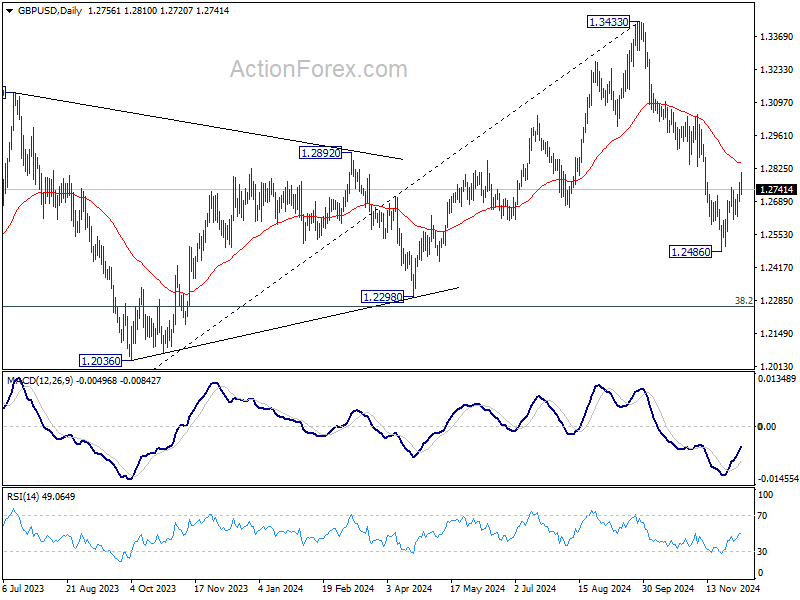

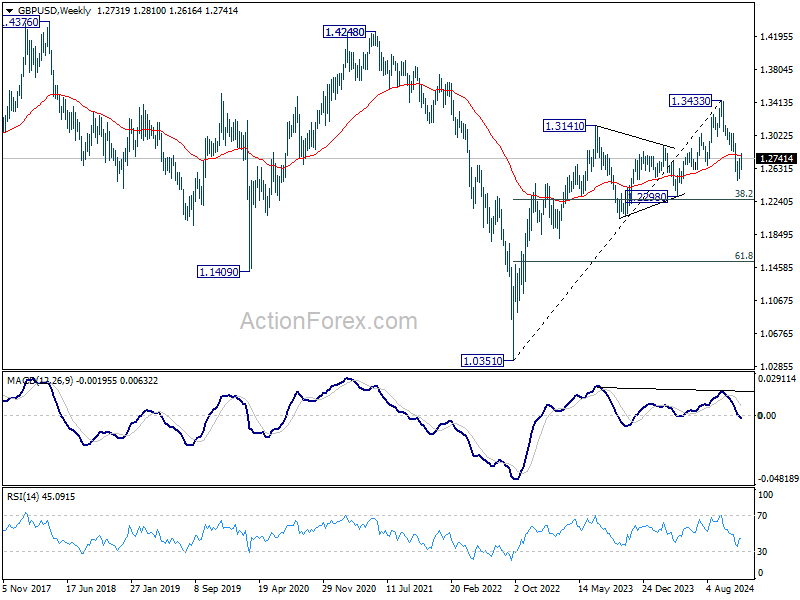

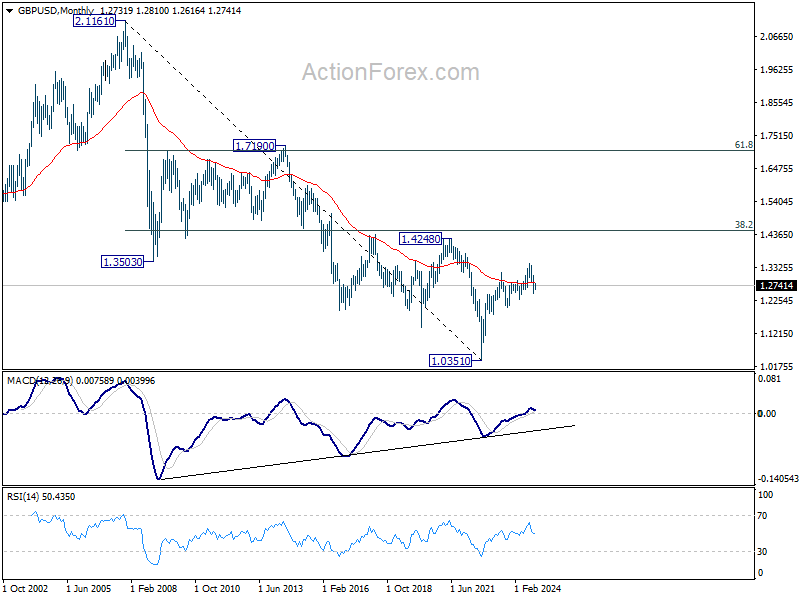

GBP/USD Weekly Outlook

GBP/USD's rebound from 1.2486 extended higher last week but overall outlook is unchanged. While further rise cannot be ruled out, fall from 1.3433 is still expected to continue as long as 55 D EMA (now at 1.2846) holds. On the downside, below 1.2615 minor support will bring retest of 1.2486 first. Firm break there will target 1.2298 cluster support zone. However, sustained break of 55 D EMA will argue that the near term trend has reversed, and targets 1.3047 resistance for confirmation.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

In the long term picture, as long as 1.2298 support holds, rise from 1.0351 long term bottom is expected to continue. But in any case, outlook is neutral at best as long as 1.4248 structural resistance holds.

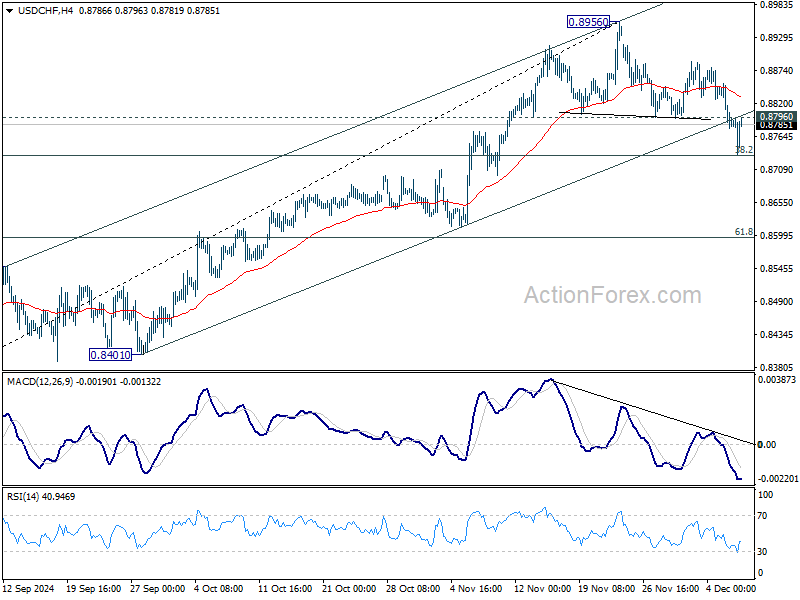

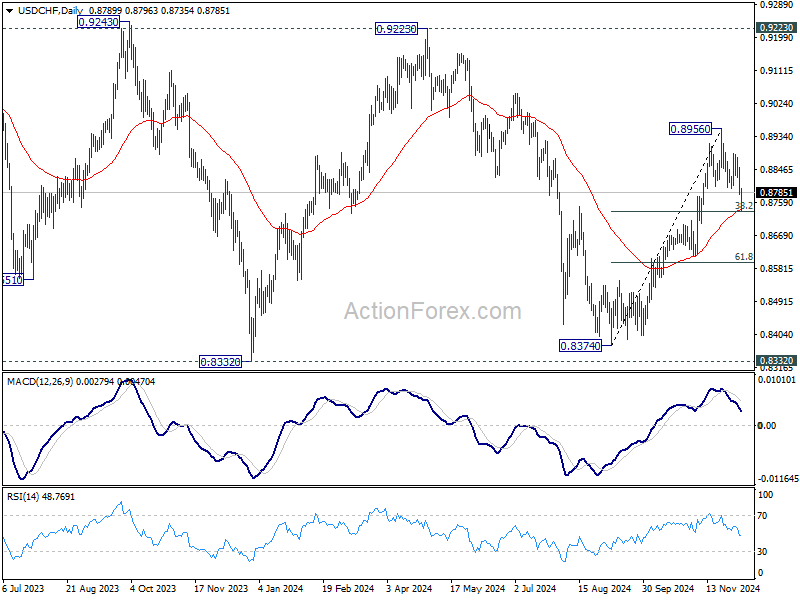

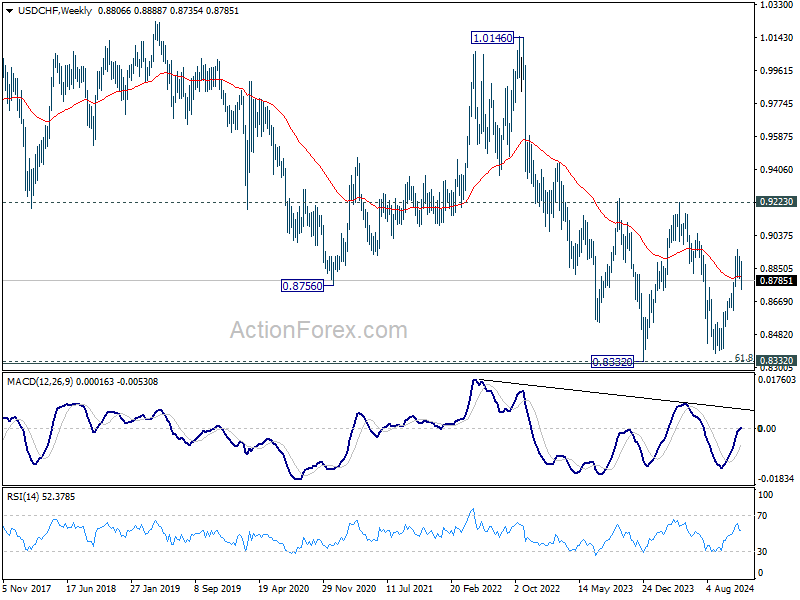

USD/CHF Weekly Outlook

USD/CHF's pullback from 0.8956 extended lower last week but recovered after touching 55 D EMA (now at 0.8738). Initial bias is turned neutral this week first. Strong rebound from current level will retain near term bullishness. Break of 0.8796 minor resistance will bring retest of 0.8956 high first. However, considering head and shoulder top pattern, firm break of the EMA will argue that whole rise from 0.8401 might have completed, and bring deeper decline to 61.8% retracement of 0.8401 to 0.8956 at 0.8613 next.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

In the long term picture, price action from 0.7065 (2011 low ) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Fall from 1.0342 (2016 high) is seen as the second leg. Rejection by 55 M EMA suggest that this fall is in progress. Break of 61.8% retracement of 0.7065 to 1.0342 at 0.8317 will pave the way back to 0.7065.

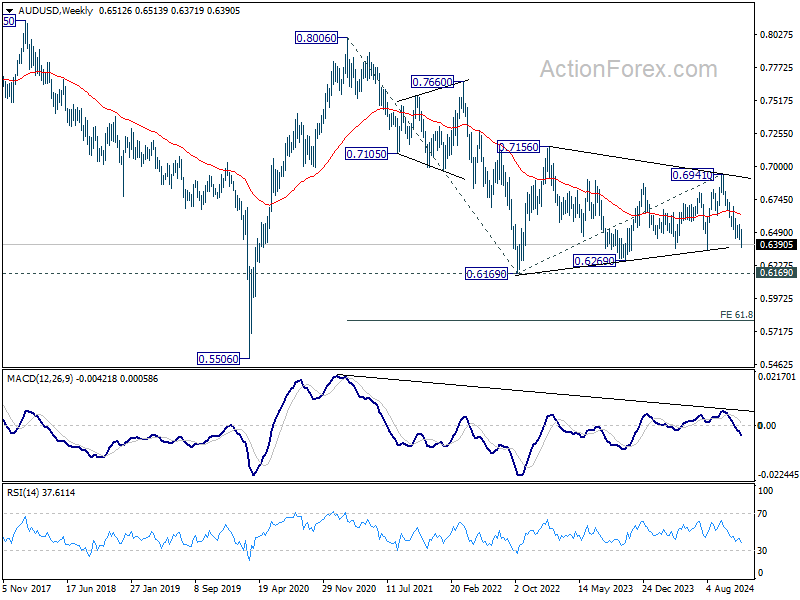

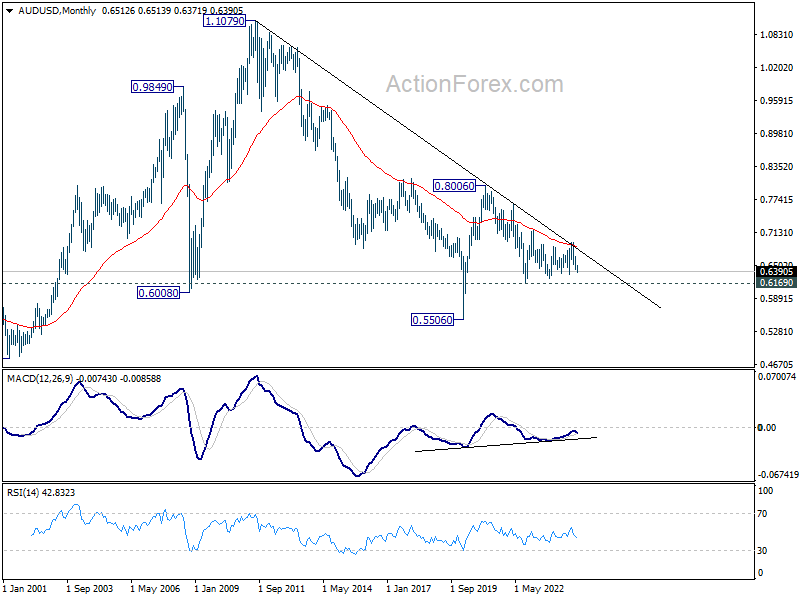

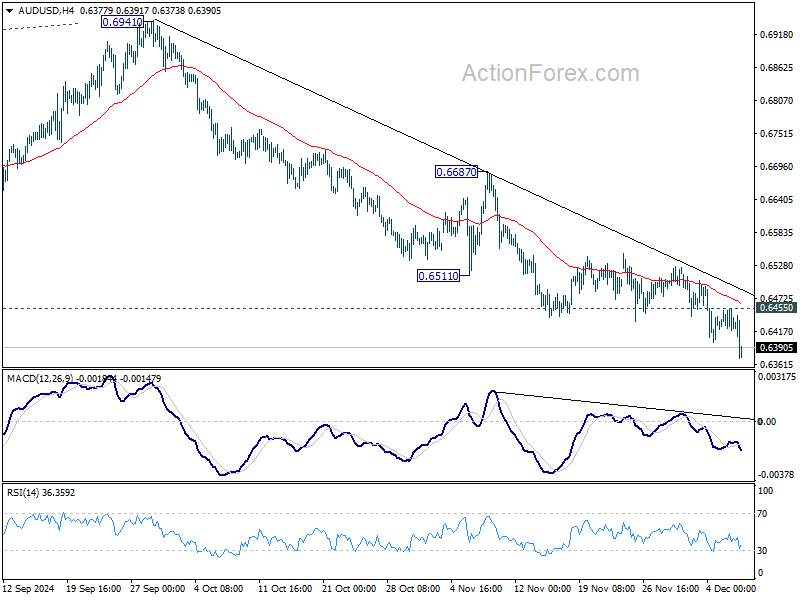

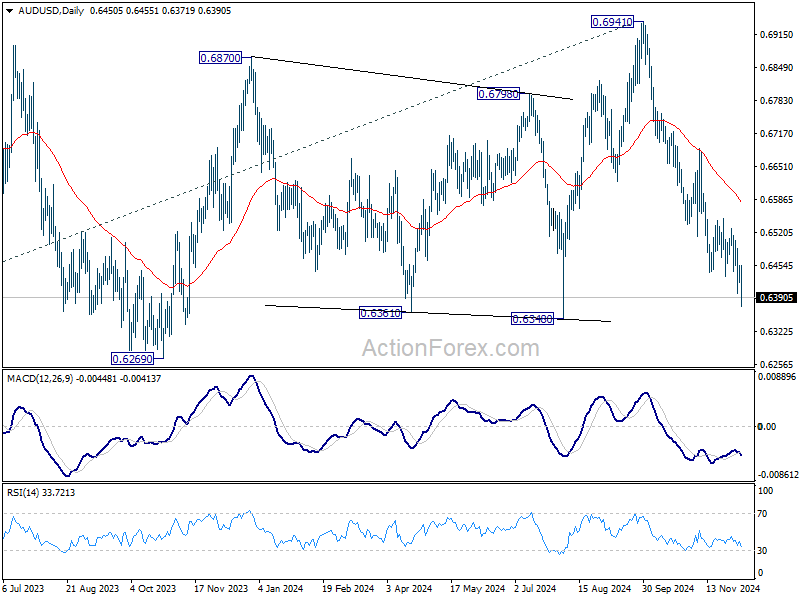

AUD/USD Weekly Report

AUD/USD's decline from 0.6941 resumed last week and dived to as low as 0.6371. Initial bias stays on the downside this week for 0.6348 support first. Firm break there will target 0.6269 support next. On the upside, above 0.6455 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen as the second leg of the pattern. Hence, even in case of deeper fall, strong support should emerge above 0.5506 to contain downside to bring reversal.