Sample Category Title

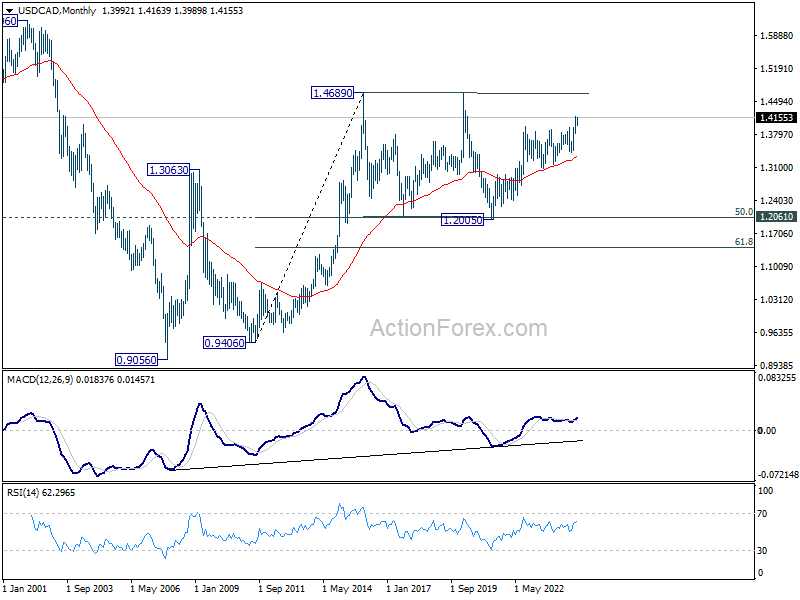

USD/CAD Weekly Outlook

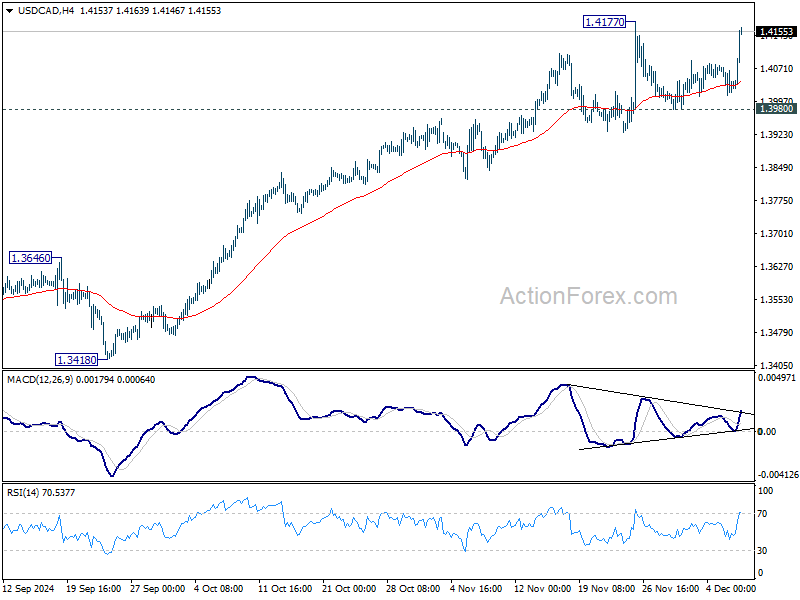

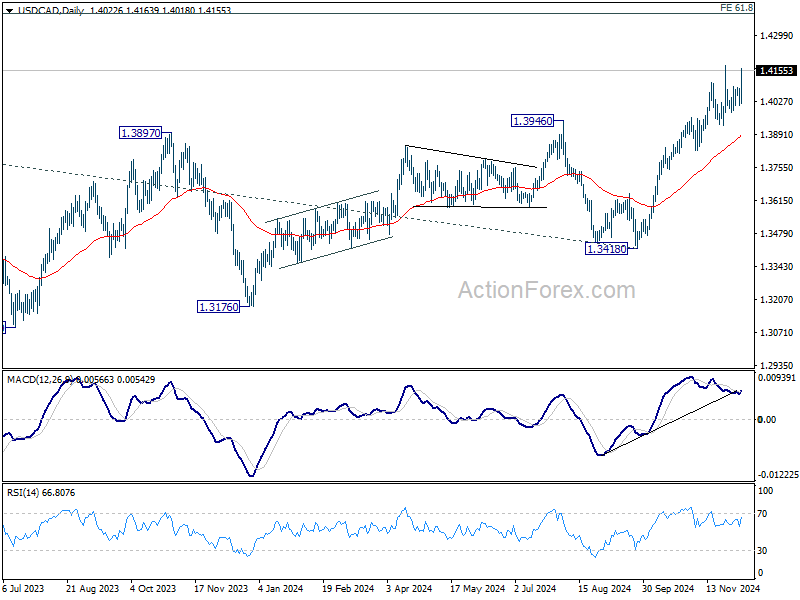

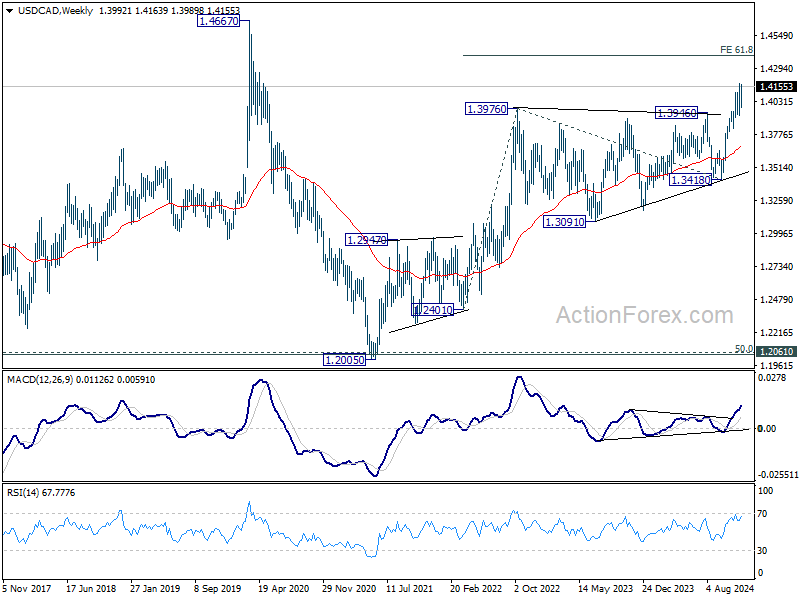

While USD/CAD extended the consolidations from 1.4177 last week, the late surge argues that larger up trend might be ready to resume. Immediate focus is now on 1.4177 resistance this week. Decisive break there will confirm this bullish case and target 1.4391 projection level next. Rejection by 1.4177 will delay the bullish case and bring more consolidations. But outlook will continue to stay bullish as long as 1.3980 support holds.

In the bigger picture, up trend from 1.2005 (2021) is in progress. Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.3418 support holds.

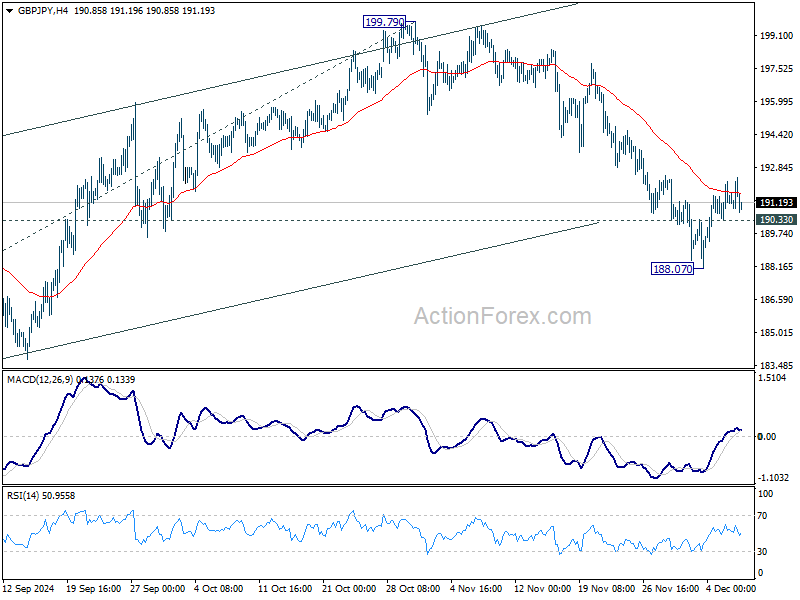

GBP/JPY Weekly Outlook

GBP/JPY edged lower to 188.07 last week as fall from 199.71 extended, but recovered since then. Initial bias remains neutral this week first. While further recovery cannot be ruled out, outlook will stay bearish as long as 55 D EMA (now at 194.04) holds. On the downside, below 190.33 minor support will bring retest of 188.07 first. Break there will target 183.70 support next.

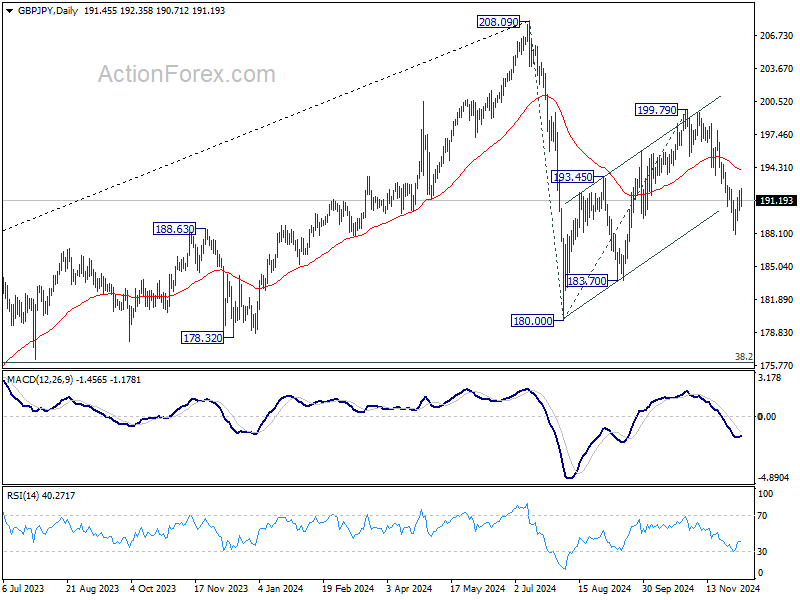

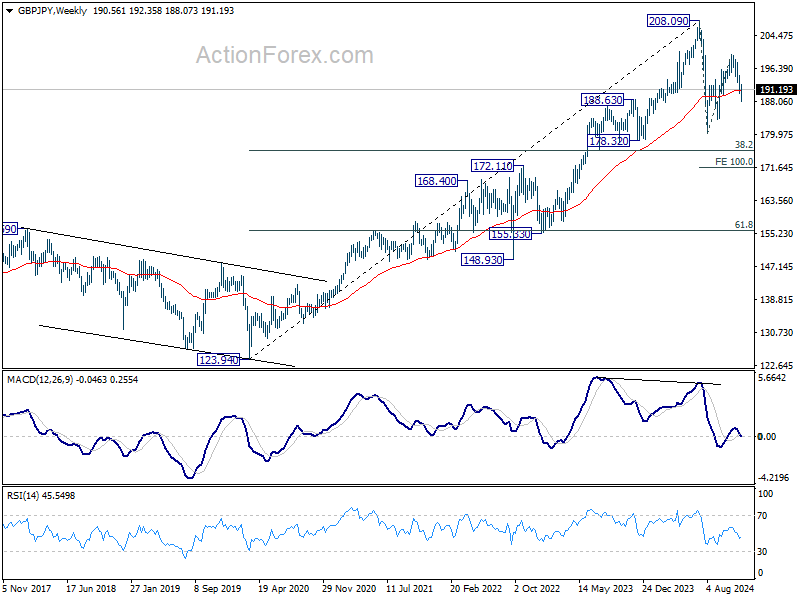

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

In the longer term picture, considering bearish divergence condition in W MACD, 208.09 is at least a medium term top. It's still early to conclude that the up trend from 122.75 (2016 low) has completed. But it's at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 172.51).

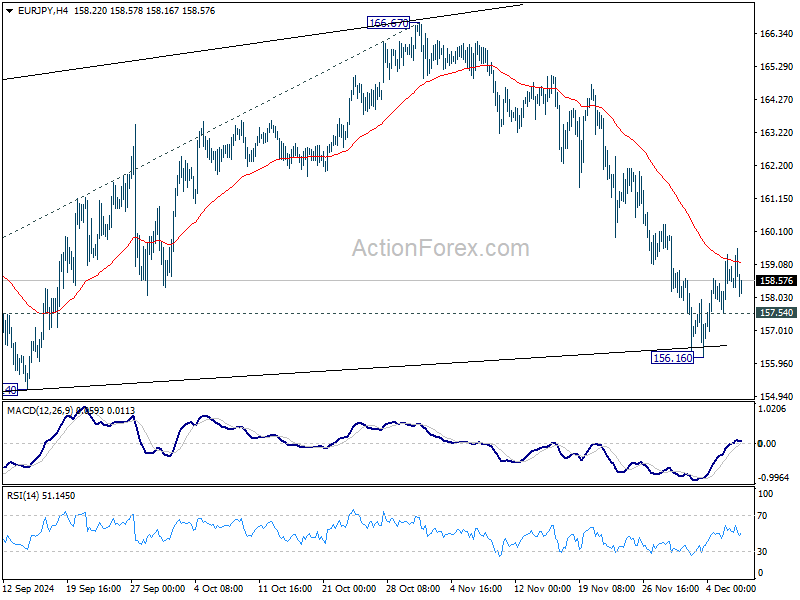

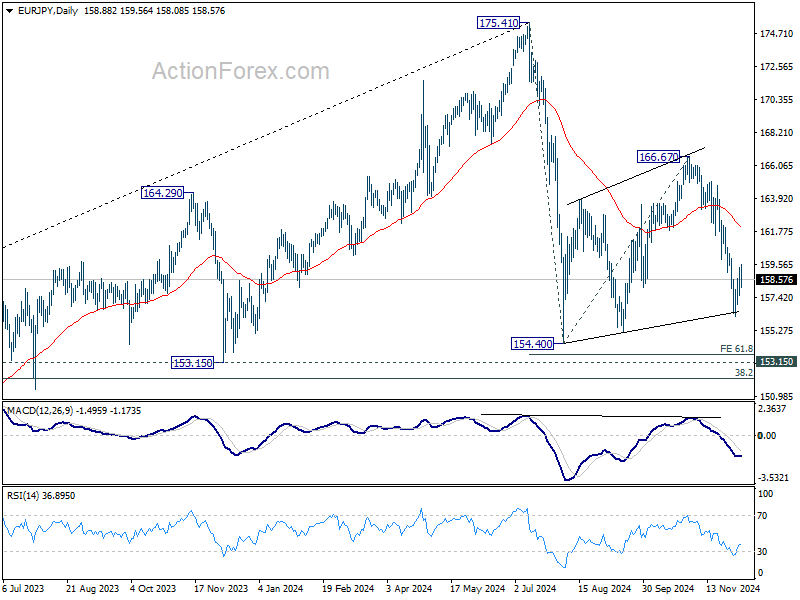

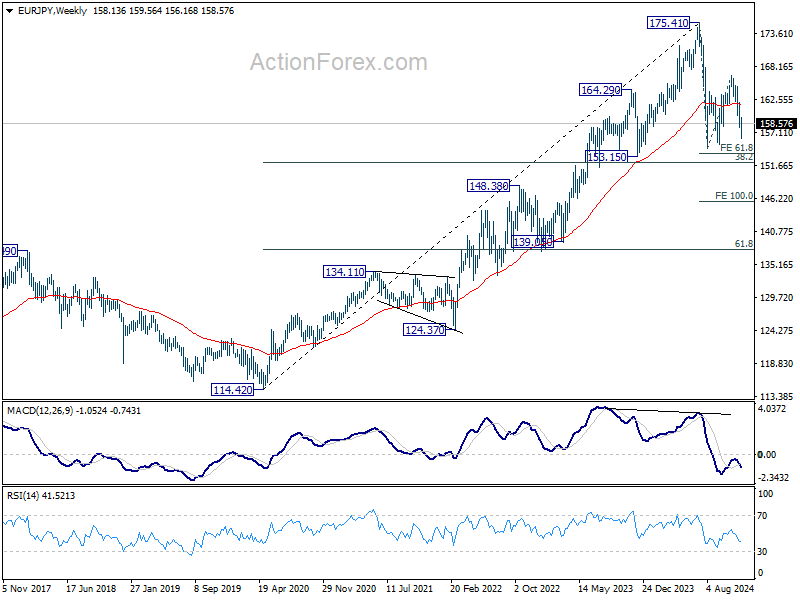

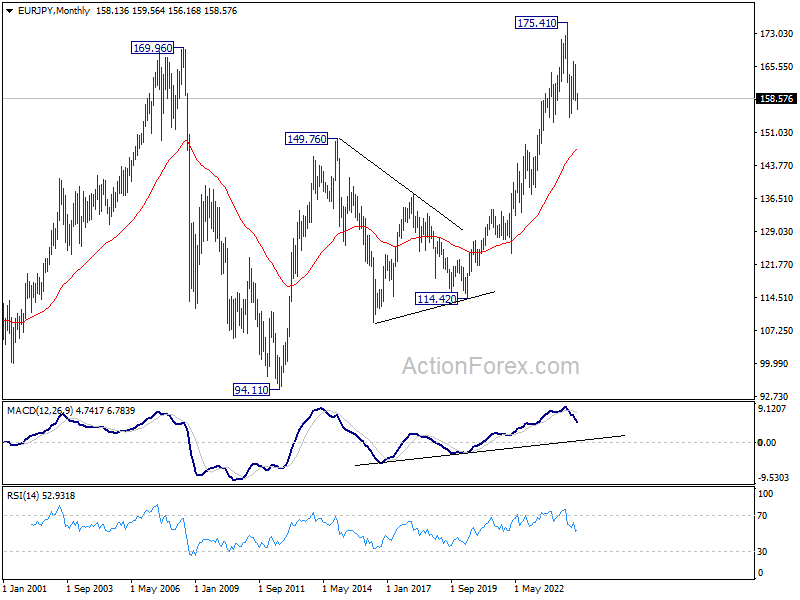

EUR/JPY Weekly Outlook

EUR/JPY edged lower to 156.16 last week as fall from 166.67 extended, but recovered since then. Initial bias remains neutral this week first. While further recovery cannot be ruled out, outlook will stay bearish as long as 55 D EMA (now at 162.11) holds. On the downside, below 157.54 minor support will bring retest of 156.16 first. Break there will target 154.40 low next.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

In the long term picture, considering bearish divergence condition in W MACD, 175.41 is at least a medium term top. It's still early to conclude that up trend from 94.11 (2012 low) has completed. But a medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 147.55).

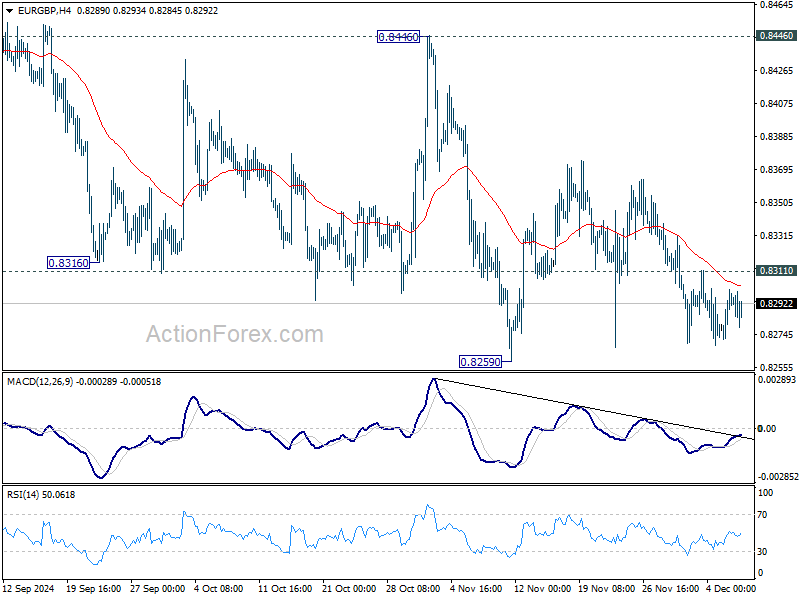

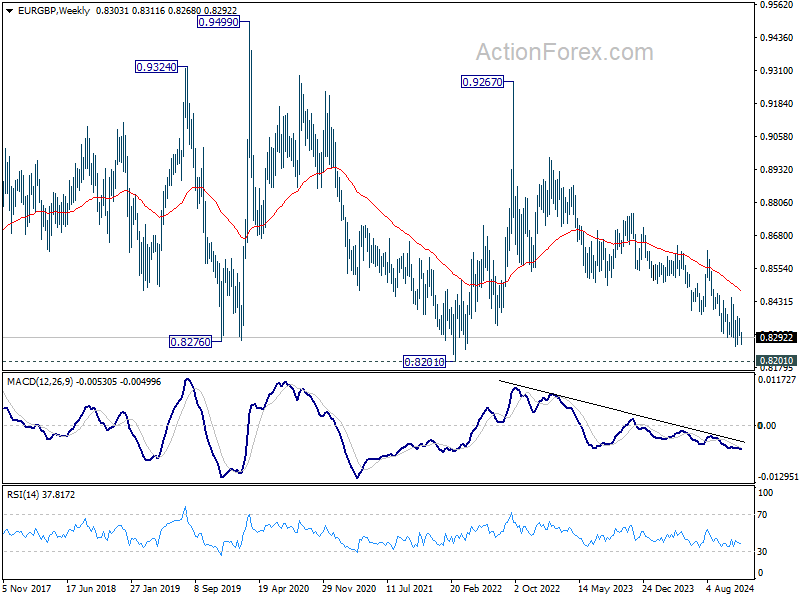

EUR/GBP Weekly Outlook

While EUR/GBP decline last week, downside was still contained above 0.8259 support. Initial bias stays neutral this week first. On the downside, decisive break of 0.8259 will resume larger down trend to 0.8201 key support. On the upside, break of 0.8311 minor resistance will turn bias back to the upside for recovery. But still, outlook will stay bearish as long a 0.8446 resistance holds, and downside breakout is expected at a later stage.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 08.446 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

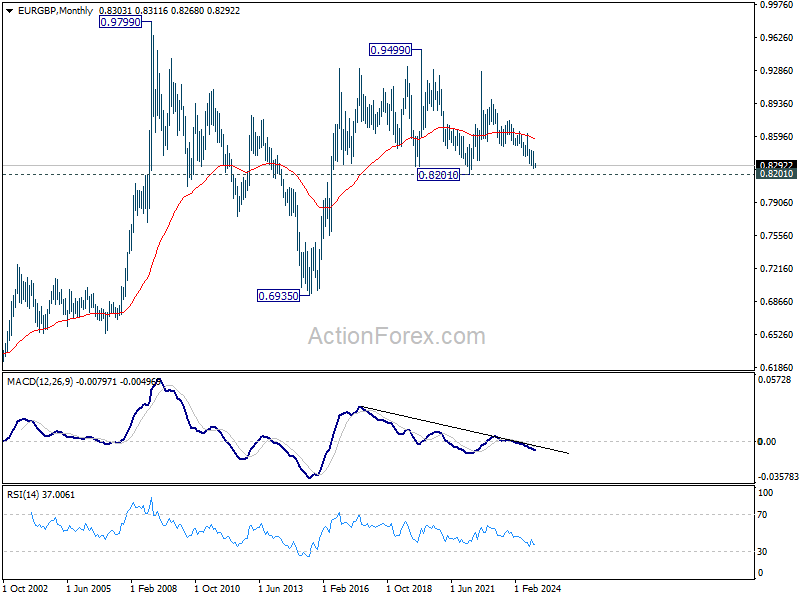

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

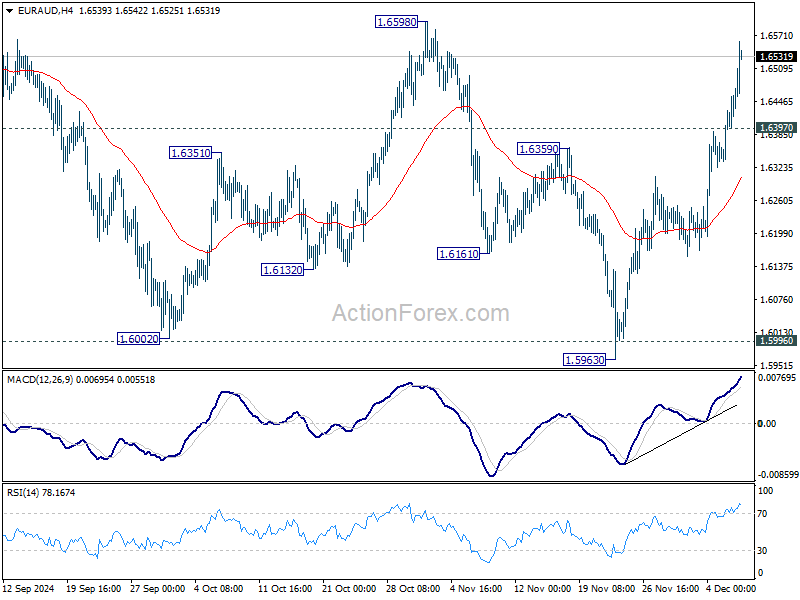

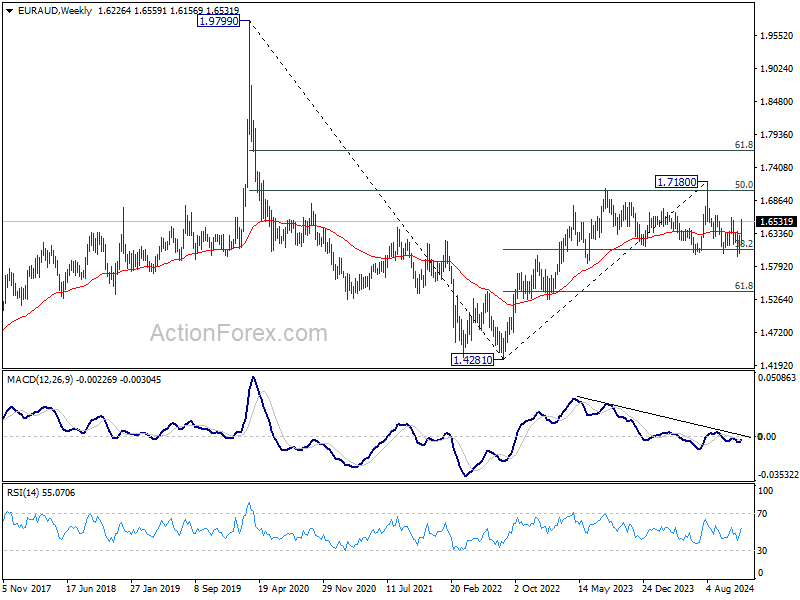

EUR/AUD Weekly Outlook

EUR/AUD's strong rally last week argues that the near term trend might be reversing. Initial bias stays on the upside this week for 1.6598 resistance first. Decisive break there will confirm that whole fall from 1.7180 has complete with three waves down to 1.5963, and target a test on 1.7180 next. On the downside, break of 1.6397 minor support will turn intraday bias neutral again first.

In the bigger picture, EUR/AUD is still holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6047) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

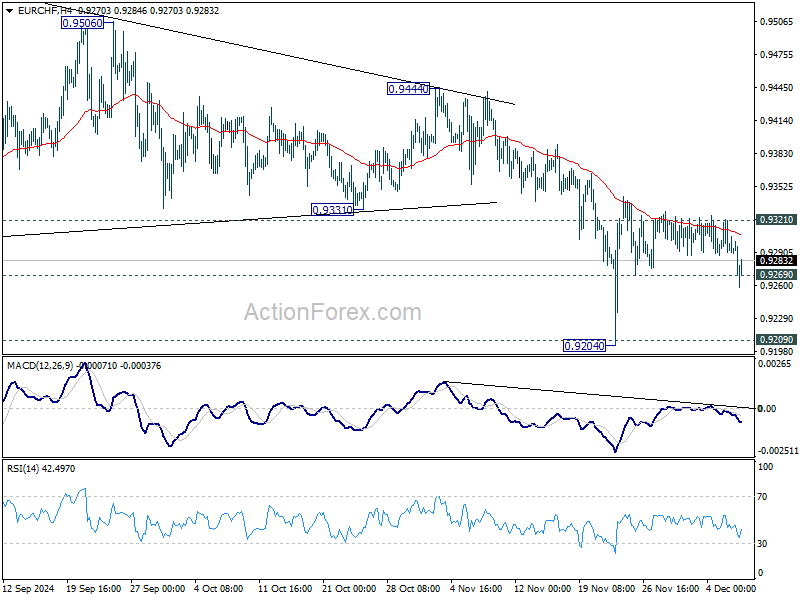

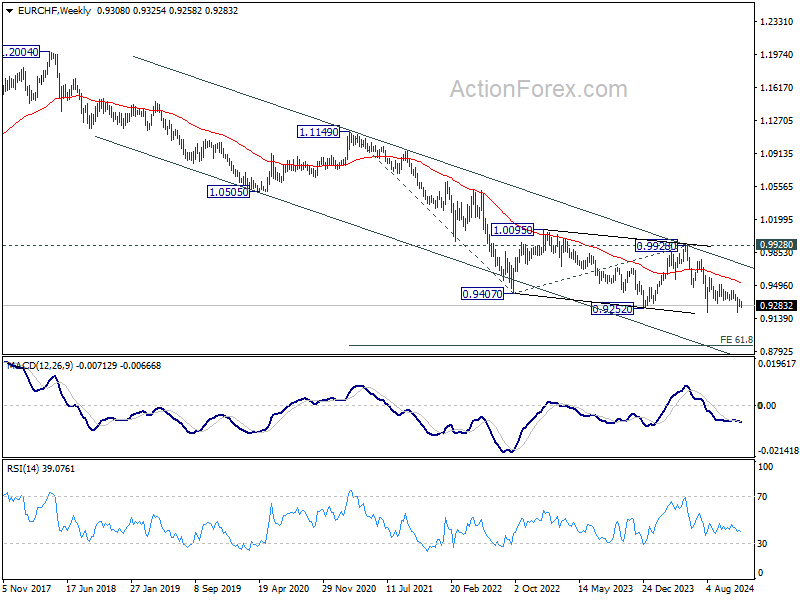

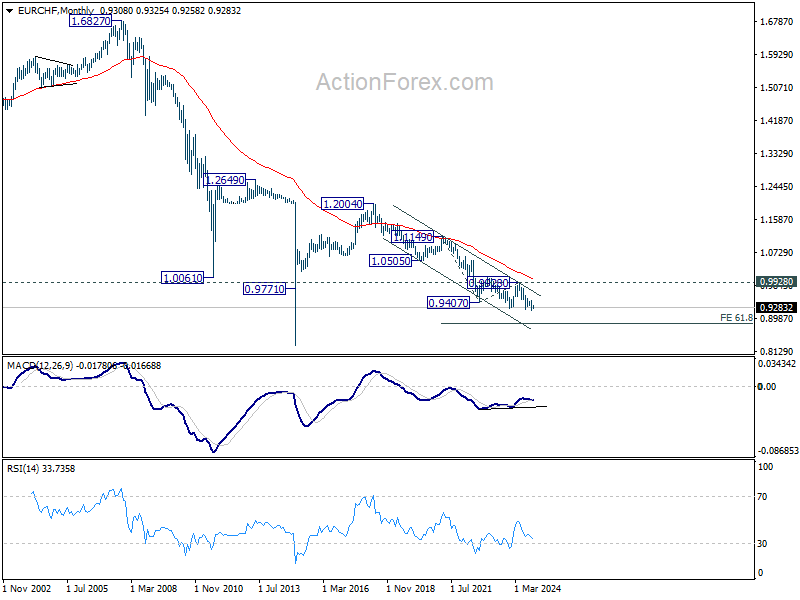

EUR/CHF Weekly Outlook

EUR/CHF's late breach of 0.9269 support last week argues that rebound from 0.9204 has completed already, after repeated rejection by falling 55 4H EMA. Initial bias is cautiously on the downside this week. Deeper fall would be seen to retest 0.9204 low. Firm break of 0.9204/9 will indicate larger down trend resumption. Nevertheless, break of 0.9321 resistance will turn bias back to the upside to resume the rebound from 0.9204 instead, and that would be an early sign of bullish reversal for the near term.

In the bigger picture, outlook will now stay bearish as long as 0.9444 resistance holds. Decisive break of 0.9209 low will resume long term down trend to 61.8% projection of 0.9772 to 0.9209 from 0.9444 at 0.9096 next.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption to 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Trump Trade Roars Back, Dollar in Correction, Commodity Currencies Tumble

The resurgence of "Trump Trade" last week reignited optimism across financial markets, driving US stocks to fresh record highs and propelling Bitcoin past the critical 100k psychological level. Investors appeared largely unfazed by a slew of top-tier US economic data and the solidification of expectations for a 25bps Fed rate cut this month. Instead, the market focused on the longer-term implications of President-elect Donald Trump’s pro-business policies, including reduced regulation and a reinvigorated push for US economic dominance.

Dollar saw mixed performance as it extended its correction against European majors but gained strength against commodity-linked currencies. While Fed is widely expected to deliver a 25bs rate cut this month, markets are bracing for a markedly slower pace of easing in 2025. Dollar's underlying strength could resurface soon, bolstered by expectations of policies under Trump that are perceived as supportive of the greenback.

The tariff-related risks, particularly with China, are amplifying uncertainties for commodity-linked currencies. Aussie has emerged as the worst performer among them, plagued by concerns of renewed US-China trade tensions and a lackluster domestic economic outlook. Market chatter about potential material depreciation next year has gained traction, especially as analysts eye a possible acceleration in RBA’s easing cycle.

Meanwhile, European majors have benefited from the Dollar’s correction, but their resilience may be short-lived. Upcoming ECB and SNB meetings could deliver dovish guidance, adding downside risks for Euro and Swiss Franc. Sterling has stood out among European currencies, supported by expectations that BoE will adopt a gradualist approach to policy easing. However, the British currency faces its own challenges, lacking the decisive momentum to break out of its ranges against Euro and Swiss Franc.

Record-Breaking S&P 500 Gains as Fed's December Cut Looks Certain, Yields and Dollar Ease

After a week rich in critical US data, Fed's next move appears increasingly certain. Market expectations for a 25bps rate cut solidified, with Fed fund futures pricing an 86% probability, up from 66% just a week ago. ISM Manufacturing and Services Indexes reflected further softening in the economy, as non-farm payroll report showed slight signs of labor market loosening. While job growth remained robust, it lacked the strength to dissuade Fed from taking another easing step.

However, attention is pivoting to January, with discussions emerging about a pause in rate reductions, supported by comments from some Fed officials. St. Louis Fed President Alberto Musalem noted the need to "consider slowing the pace of interest rate reductions or pausing," citing the importance of carefully assessing economic conditions and the outlook.

Cleveland Fed President Beth Hammack echoed this cautious approach, suggesting "we are at or near the point where it makes sense to slow the pace of rate reductions", and that "allow us to calibrate policy to the appropriately restrictive level over time given the underlying strength in the economy.”

Reflecting these sentiments, futures markets show only a 27.6% chance of a further 25bps cut in January, compared to a dominant 72.4% expectation for holding rates steady.

The US stock market has embraced the evolving outlook. With the economy demonstrating resilience and Fed pursuing gradual easing, and optimism over the incoming administration’s policies has bolstered sentiment. S&P 500 logged its third consecutive weekly gain, closing at a new record.

Technically, S&P 500 is now entering a resistance zone between 61.8% projection of 4103.78 to 5669.67 from 5119.26 at 6086.98 and medium term rising channel resistance at around 6220. Upside momentum could start to wane in this zone, especially considering that year-end holiday period is approaching.

Nevertheless, outlook will continue to stay bullish as long as 5851.48 support holds. Decisive break of 6080/6220 resistance zone could prompt upside acceleration to 100% projection at 6685.15 in late Q1 or early Q2.

10-year yield extended the decline from 4.505 in reaction to readjusted Fed outlook following NFP. The break of 38.2% retracement of 3.603 to 4.505 at 4.160 suggests that deeper correction is now underway. Further fall is expected as long as 4.281 resistance holds, in case of recovery. TNX would now target 61.8% retracement of 3.603 to 4.505 at 3.947, which is slightly below 4% mark.

The combined environment of risk-on sentiment and falling yields could keep Dollar Index pressured for the near term. Yet, downside would likely be relatively limited considering the slower easing pace of Fed in 2025. Also, the terminal rate of Fed in the current cycle would likely be higher than most of the peers, at least comparing to ECB.

Technically, the structure of the fall from 108.07 is also corrective. So, in case of deeper correction, strong support would likely be seen between 55 D EMA (now at 104.82) and 38.2% retracement of 100.15 to 108.07 at 105.04 to contain downside. Meanwhile, break of 106.72 resistance will indicate that the corrective pattern from 108.07 has already started the second leg back towards this high.

Tech and Crypto Surge as Trump’s Picks Stoke Optimism

The US tech sector and cryptocurrency markets closed the week with significant gains, riding a wave of optimism fueled by the Trump administration’s pro-crypto and tech-focused appointments. Paul Atkins, a well-known advocate for digital innovation, has been nominated to lead the SEC, a move widely interpreted as a green light for regulatory support of the cryptocurrency space. Meanwhile, the naming of former PayPal COO David Sacks as "White House AI & Crypto Czar" added further momentum, energizing both tech and crypto investors. These developments propelled Bitcoin past the 100k milestone and pushed the NASDAQ to new all-time highs.

Technically, NASDAQ's up trend made notable progress by breaking through 61.8% projection of 12543.85 to 18671.06 from 15708.53 at 19366.06. 20k handle is now within reach, but the key hurdle lies in medium term rising channel resistance at around 20300. Decisive break of this level could prompt upside acceleration to 100% projection at 21835.75. In any case, outlook will now stay bullish as long as 18702.37 support holds.

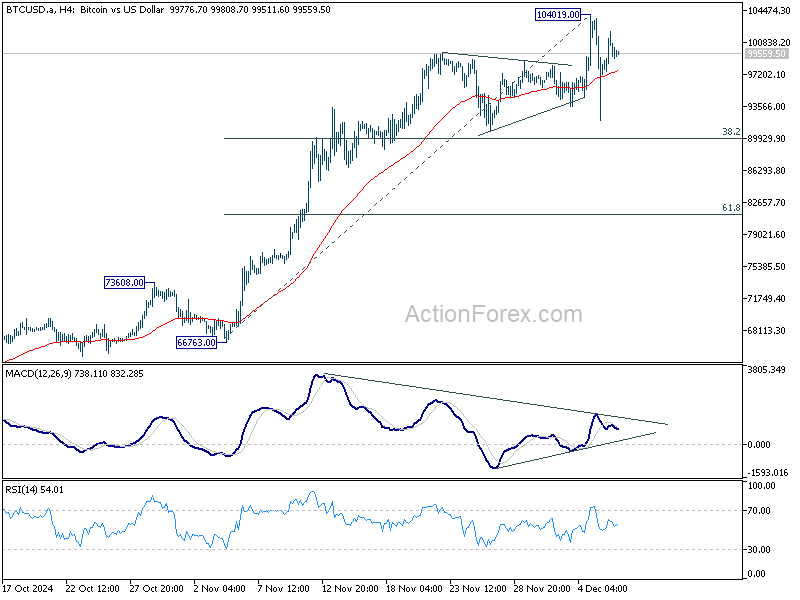

Bitcoin's week was characterized by dramatic volatility. The cryptocurrency achieved a historic high of 104019 before a steep pullback, attributed to a USD 1B liquidation wave within 24 hours of crossing the 100k mark. However, the swift rebound underscored the market's resilience, as bullish sentiment quickly returned.

Technically, while some consolidations could be seen in Bitcoin in the near term, outlook will stay bullish as long as 38.2% retracement of 66763. to 104019 at 89787 holds. Break of 104019 will resume larger up trend towards 138.2% projection of 24896 to 73812 from 52703 at 120304.

The momentum for Bitcoin’s next rally could be significant, particularly if traders who closed long positions during the pullback re-enter the market.

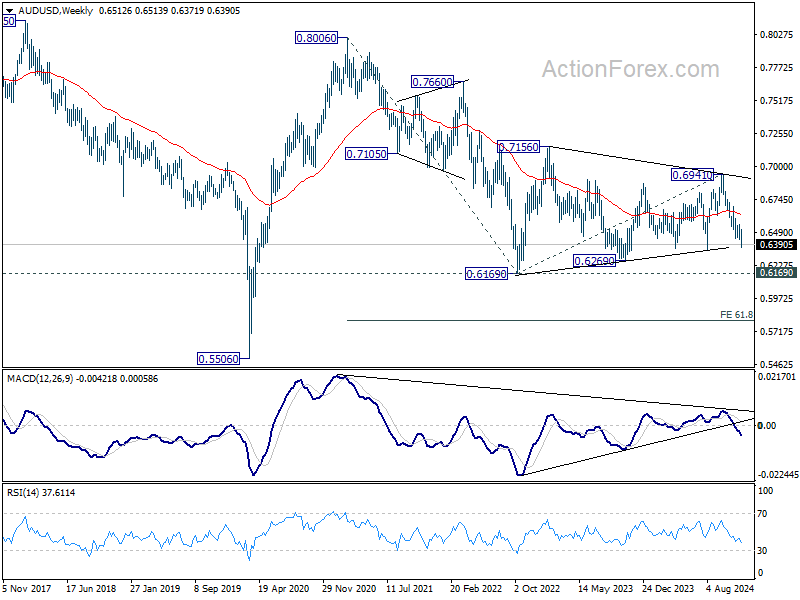

Rapid RBA Policy Shifts Could Trigger Significant Downside for AUD in Coming Year

Commodity-linked currencies were the outliers this week, underperforming despite a broader surge in risk-on sentiment. Persistent fears over a potential tariff war between the U.S., Canada, and China have been a significant drag on currencies like the Australian and Canadian dollars. Adding to the pressure, the U.S. dollar remained resilient as expectations solidified for a slower pace of Fed rate cuts, further weighing on commodity currencies.

Aussie has been particularly vulnerable, with analysts revising their outlooks. The Commonwealth Bank of Australia now anticipates AUD could fall "materially" to as low as 0.60 against USD next year.

RBA remains hesitant to commence monetary easing, with May 2025 still seen as the most likely timing for the first rate cut, not even February. However, weaker-than-expected Q3 GDP data has highlighted the fragility of the Australian economy. The narrative regarding RBA's policy easing could shift if disinflation accelerates significantly in Q1, forcing the central bank to ease faster than originally expected once the cycle commences.

China’s economic sluggishness adds another layer of uncertainty for AUD. Despite stimulus measures, the Chinese economy continues to underperform, compounded by renewed trade tensions with the US. Should these pressures escalate, Australia’s trade-reliant economy could face additional headwinds, amplifying downside risks for its currency.

Technically, one of the various interpretation of the price actions from 0.6169 (2022 low) is that the medium term consolidation pattern from 0.6169 has completed with three waves to 0.6941. That is, the down trend from 0.8006 (2021 high) might be ready to resume. While it's still early to make a conclusion, break of 0.6269 support would support this bearish case. The medium term target could be tentatively set at 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806.

USD/CAD Weekly Outlook

While USD/CAD extended the consolidations from 1.4177 last week, the late surge argues that larger up trend might be ready to resume. Immediate focus is now on 1.4177 resistance this week. Decisive break there will confirm this bullish case and target 1.4391 projection level next. Rejection by 1.4177 will delay the bullish case and bring more consolidations. But outlook will continue to stay bullish as long as 1.3980 support holds.

In the bigger picture, up trend from 1.2005 (2021) is in progress. Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.3418 support holds.

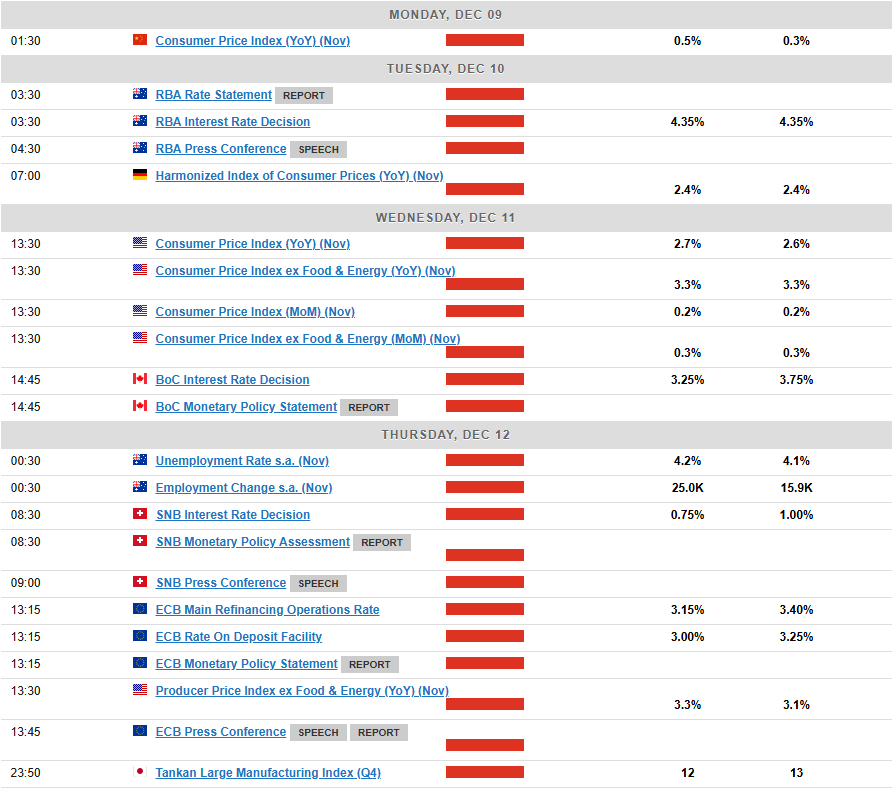

Summary 12/9 – 12/13

Monday, Dec 9, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Nov | 2.60% | 2.70% |

| 23:50 | JPY | GDP Q/Q Q3 F | 0.20% | 0.20% |

| 23:50 | JPY | GDP Deflator Y/Y Q3 F | 2.50% | 2.60% |

| 23:50 | JPY | Current Account (JPY) Oct | 2.28T | 1.27T |

| 01:30 | CNY | CPI Y/Y Nov | 0.50% | 0.30% |

| 01:30 | CNY | PPI Y/Y Nov | -2.90% | -2.90% |

| 05:00 | JPY | Eco Watchers Survey: Current Nov | 47.3 | 47.5 |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Dec | -13.1 | -12.8 |

| 15:00 | USD | Wholesale Inventories Oct F | 0.20% | 0.20% |

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | 1.20% | 1.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Nov | |

| Forecast: 2.60% | Previous: 2.70% | ||

| 23:50 | JPY | GDP Q/Q Q3 F | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q3 F | |

| Forecast: 2.50% | Previous: 2.60% | ||

| 23:50 | JPY | Current Account (JPY) Oct | |

| Forecast: 2.28T | Previous: 1.27T | ||

| 01:30 | CNY | CPI Y/Y Nov | |

| Forecast: 0.50% | Previous: 0.30% | ||

| 01:30 | CNY | PPI Y/Y Nov | |

| Forecast: -2.90% | Previous: -2.90% | ||

| 05:00 | JPY | Eco Watchers Survey: Current Nov | |

| Forecast: 47.3 | Previous: 47.5 | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Dec | |

| Forecast: -13.1 | Previous: -12.8 | ||

| 15:00 | USD | Wholesale Inventories Oct F | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | |

| Forecast: 1.20% | Previous: 1.20% | ||

Tuesday, Dec 10, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Conditions Nov | 7 | |

| 00:30 | AUD | NAB Business Confidence Nov | 5 | |

| 03:00 | CNY | Trade Balance (USD) Nov | 92.0B | 95.7B |

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% |

| 04:30 | AUD | RBA Press Conference | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | 9.30% | |

| 07:00 | EUR | Germany CPI M/M Nov F | -0.20% | -0.20% |

| 07:00 | EUR | Germany CPI Y/Y Nov F | 2.20% | 2.20% |

| 11:00 | USD | NFIB Business Optimism Index Nov | 94.2 | 93.7 |

| 13:30 | USD | Nonfarm Productivity Q3 | 2.30% | 2.20% |

| 13:30 | USD | Unit Labor Costs Q3 | 1.80% | 1.90% |

| 21:45 | NZD | Manufacturing Sales Q3 | 0.10% | |

| 23:50 | JPY | PPI Y/Y Nov | 3.40% | 3.40% |

| 23:50 | JPY | BSI Large Manufacturing Index Q4 | 4.5 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Conditions Nov | |

| Forecast: | Previous: 7 | ||

| 00:30 | AUD | NAB Business Confidence Nov | |

| Forecast: | Previous: 5 | ||

| 03:00 | CNY | Trade Balance (USD) Nov | |

| Forecast: 92.0B | Previous: 95.7B | ||

| 03:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 4.35% | Previous: 4.35% | ||

| 04:30 | AUD | RBA Press Conference | |

| Forecast: | Previous: | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | |

| Forecast: | Previous: 9.30% | ||

| 07:00 | EUR | Germany CPI M/M Nov F | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 07:00 | EUR | Germany CPI Y/Y Nov F | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 11:00 | USD | NFIB Business Optimism Index Nov | |

| Forecast: 94.2 | Previous: 93.7 | ||

| 13:30 | USD | Nonfarm Productivity Q3 | |

| Forecast: 2.30% | Previous: 2.20% | ||

| 13:30 | USD | Unit Labor Costs Q3 | |

| Forecast: 1.80% | Previous: 1.90% | ||

| 21:45 | NZD | Manufacturing Sales Q3 | |

| Forecast: | Previous: 0.10% | ||

| 23:50 | JPY | PPI Y/Y Nov | |

| Forecast: 3.40% | Previous: 3.40% | ||

| 23:50 | JPY | BSI Large Manufacturing Index Q4 | |

| Forecast: | Previous: 4.5 | ||

Wednesday, Dec 11 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 13:30 | USD | CPI M/M Nov | 0.20% | 0.20% |

| 13:30 | USD | CPI Y/Y Nov | 2.70% | 2.60% |

| 13:30 | USD | CPI Core M/M Nov | 0.30% | 0.30% |

| 13:30 | USD | CPI Core Y/Y Nov | 3.30% | 3.30% |

| 14:45 | CAD | BoC Interest Rate Decision | 3.25% | 3.75% |

| 15:30 | USD | Crude Oil Inventories | -5.1M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 13:30 | USD | CPI M/M Nov | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 13:30 | USD | CPI Y/Y Nov | |

| Forecast: 2.70% | Previous: 2.60% | ||

| 13:30 | USD | CPI Core M/M Nov | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 13:30 | USD | CPI Core Y/Y Nov | |

| Forecast: 3.30% | Previous: 3.30% | ||

| 14:45 | CAD | BoC Interest Rate Decision | |

| Forecast: 3.25% | Previous: 3.75% | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -5.1M | ||

Thursday, Dec 12, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Employment Change Nov | 29.6K | 15.9K |

| 00:30 | AUD | Unemployment Rate Nov | 4.20% | 4.10% |

| 08:30 | CHF | SNB Interest Rate Decision | 0.75% | 1.00% |

| 09:00 | CHF | SNB Press Conference | ||

| 13:15 | EUR | ECB Main Refinancing Rate | 3.15% | 3.40% |

| 13:15 | EUR | ECB Deposit Rate | 3.00% | 3.25% |

| 13:30 | USD | PPI M/M Nov | 0.30% | 0.20% |

| 13:30 | USD | PPI Y/Y Nov | 2.50% | 2.40% |

| 13:30 | USD | PPI Core M/M Nov | 0.30% | 0.30% |

| 13:30 | USD | PPI Core Y/Y Nov | 3.30% | 3.10% |

| 13:30 | USD | Initial Jobless Claims (Dec 6) | 221K | 224K |

| 13:30 | CAD | Building Permits M/M Oct | 11.50% | |

| 13:45 | EUR | ECB Press Conference | ||

| 15:30 | USD | Natural Gas Storage | -30B | |

| 21:30 | NZD | Business NZ PMI Nov | 45.8 | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | 13 | 13 |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q4 | 11 | 14 |

| 23:50 | JPY | Tankan Non - Manufacturing Index Q4 | 33 | 34 |

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q4 | 28 | 28 |

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | 9.60% | 10.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Employment Change Nov | |

| Forecast: 29.6K | Previous: 15.9K | ||

| 00:30 | AUD | Unemployment Rate Nov | |

| Forecast: 4.20% | Previous: 4.10% | ||

| 08:30 | CHF | SNB Interest Rate Decision | |

| Forecast: 0.75% | Previous: 1.00% | ||

| 09:00 | CHF | SNB Press Conference | |

| Forecast: | Previous: | ||

| 13:15 | EUR | ECB Main Refinancing Rate | |

| Forecast: 3.15% | Previous: 3.40% | ||

| 13:15 | EUR | ECB Deposit Rate | |

| Forecast: 3.00% | Previous: 3.25% | ||

| 13:30 | USD | PPI M/M Nov | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 13:30 | USD | PPI Y/Y Nov | |

| Forecast: 2.50% | Previous: 2.40% | ||

| 13:30 | USD | PPI Core M/M Nov | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 13:30 | USD | PPI Core Y/Y Nov | |

| Forecast: 3.30% | Previous: 3.10% | ||

| 13:30 | USD | Initial Jobless Claims (Dec 6) | |

| Forecast: 221K | Previous: 224K | ||

| 13:30 | CAD | Building Permits M/M Oct | |

| Forecast: | Previous: 11.50% | ||

| 13:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -30B | ||

| 21:30 | NZD | Business NZ PMI Nov | |

| Forecast: | Previous: 45.8 | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | |

| Forecast: 13 | Previous: 13 | ||

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q4 | |

| Forecast: 11 | Previous: 14 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Index Q4 | |

| Forecast: 33 | Previous: 34 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q4 | |

| Forecast: 28 | Previous: 28 | ||

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | |

| Forecast: 9.60% | Previous: 10.60% | ||

Friday, Dec 13, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Dec | -18 | |

| 04:30 | JPY | Industrial Production M/M Oct F | 3% | 3% |

| 07:00 | GBP | GDP M/M Oct | -0.10% | |

| 07:00 | GBP | Industrial Production M/M Oct | -0.50% | |

| 07:00 | GBP | Industrial Production Y/Y Oct | -1.80% | |

| 07:00 | GBP | Manufacturing Production M/M Oct | -1% | |

| 07:00 | GBP | Manufacturing Production Y/Y Oct | -0.70% | |

| 07:00 | GBP | Goods Trade Balance (GBP) Oct | -16.3B | |

| 07:00 | EUR | GermanyTrade Balance (EUR) Oct | 15.8B | 17.0B |

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | 0.00% | -2.00% |

| 13:30 | CAD | Manufacturing Sales M/M Oct | -0.50% | |

| 13:30 | CAD | Capacity Utilization Q3 | 79.10% | |

| 13:30 | CAD | Wholesale Sales M/M Oct | 0.80% | |

| 13:30 | USD | Import Price Index M/M Nov | -0.30% | 0.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Dec | |

| Forecast: | Previous: -18 | ||

| 04:30 | JPY | Industrial Production M/M Oct F | |

| Forecast: 3% | Previous: 3% | ||

| 07:00 | GBP | GDP M/M Oct | |

| Forecast: | Previous: -0.10% | ||

| 07:00 | GBP | Industrial Production M/M Oct | |

| Forecast: | Previous: -0.50% | ||

| 07:00 | GBP | Industrial Production Y/Y Oct | |

| Forecast: | Previous: -1.80% | ||

| 07:00 | GBP | Manufacturing Production M/M Oct | |

| Forecast: | Previous: -1% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Oct | |

| Forecast: | Previous: -0.70% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Oct | |

| Forecast: | Previous: -16.3B | ||

| 07:00 | EUR | GermanyTrade Balance (EUR) Oct | |

| Forecast: 15.8B | Previous: 17.0B | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | |

| Forecast: 0.00% | Previous: -2.00% | ||

| 13:30 | CAD | Manufacturing Sales M/M Oct | |

| Forecast: | Previous: -0.50% | ||

| 13:30 | CAD | Capacity Utilization Q3 | |

| Forecast: | Previous: 79.10% | ||

| 13:30 | CAD | Wholesale Sales M/M Oct | |

| Forecast: | Previous: 0.80% | ||

| 13:30 | USD | Import Price Index M/M Nov | |

| Forecast: -0.30% | Previous: 0.30% | ||

Markets Weekly Outlook – Central Bank Focus as US Inflation Looms

- US Jobs report all but confirms a December rate cut, with markets pricing in an 80% probability.

- Nasdaq nears 22,000 as US equities continue their strong performance, with the S&P 500 also hitting record highs.

- Global markets await US CPI and ECB decisions, with expectations of a 25 bps rate cut from the ECB.

- Focus for the week ahead includes US CPI, ECB decision, and Chinese inflation data.

Week in Review: Jobs Data All but Confirms a December Rate Cut

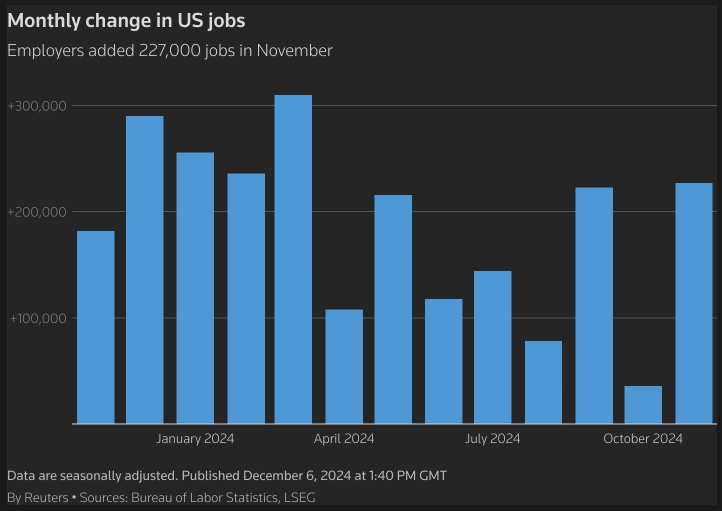

A week that saw a lot of choppy price action as markets awaited the US jobs report on Friday. A stellar jobs print of 227k and a slight uptick in the unemployment rate to 4.2% appear to have sealed a December rate cut.

Source: LSEG

Barring any crazy inflation surprise in the week ahead, markets appear fairly certain that the Fed will deliver a 25 bps cut in December. Federal Reserve policymakers will enter a media blackout that kicks in on Saturday, in the run-up to the central bank’s Dec. 17-18 policy meeting.

US Equities have been the talk of the town once more, as Wall Street Indexes continued their impressive YTD performance. The S&P 500 and the Nasdaq hit intraday record highs on Friday while the Dow struggled following a drop in UnitedHealth shares.

The ‘Santa rally’ appears to be here with the S&P making its way above the 6100 handle and the Nasdaq eyeing consolidation above the 21500 handle. Following the day’s move the S&P and Nasdaq are on course for a third consecutive week of gains with the Dow on course for a minor setback.

Oil prices struggled this week despite OPEC + continuing their current production cut schedule into 2025. The Organization of the Petroleum Exporting Countries (OPEC)+, pushed back the start of oil output rises by three months until April and extended the full unwinding of cuts by a year until the end of 2026

Following a choppy week, Oil was trading down around 1% on Friday and on course to finish the week down around the same. Bank of America forecasts that increasing oil surpluses will drive the price of Brent to average $65 a barrel in 2025, while expecting oil demand growth to rebound to 1 million barrels per day (bpd) next year, the bank said in a note on Friday.

Gold remained rangebound for the majority of the week, as the precious metal coiled in a $40 range between 2612-2660. Not even Friday’s jobs data was enough to shake the precious metal into a breakout.

The DXY had a mixed week with a strong start and end to the week followed by a soft middle leaving the DXY on course for marginal gains of about 0.35%. This was reflected in the choppy price action by major pairs this week with the Euro and the GBP unable to hold onto gains against the Greenback.

The DXY will be worth monitoring given the US Dollar has a track record of poor performance in the Month of December. An uptick in US inflation however could aid the Dollar in its bid to reclaim the 107.00 handle next week.

The Week Ahead: US Jobs Data to Dominate

Asia Pacific Markets

The week ahead in the Asia Pacific region sees some key economic data releases and events.

In China, the big event next week is the annual Central Economic Work Conference. While it won’t focus on exact numerical targets (those are usually set during the Two Sessions), it will give clues about how policymakers are planning for next year. This could have an impact on emerging market currencies and currencies like the Australian Dollar as well.

The better question would be whether there’s any change in their approach to fiscal policy or monetary policy.

China will release its November inflation data on Tuesday and trade numbers on Wednesday. Inflation could very well rise to 0.6%, from the previous 0.3%. Imports are likely to stay weak due to low domestic demand, growing only around 1.2%.

In Australia, the RBA is expected to keep rates on hold this week at 4.35%. The uptick in October core inflation coupled with stronger economic growth in the third quarter suggest the RBA isn’t in a hurry to lower rates.

In Japan, the Tankan Business Survey will be out this week. This comes as speculation continues to grow that the BoJ will deliver a rate hike of 25bps at its upcoming meeting. Something else to pay attention to may be the manufacturing sector, which may face challenges due to growing uncertainty around global trade policies, especially in the auto industry.

Europe + UK + US

In developed markets, the focus moves back to the US and CPI inflation data as speculation grows around a December rate cut.

Core CPI is expected to rise by 0.3% month-on-month again, which could complicate the December decision for the Federal Reserve despite the probability of a rate cut lingering around the 80% mark.

Policymakers agree that policy remains restrictive and the sticking point seems to be over the pace of cuts. I do still think the idea of Trump assuming office will play in the minds of policymakers who will likely cut in December and take a pause in January.

In Europe the ECB decision is due this week with any doubt around the size of a cut seemingly evaporated. A recent bout of data and comments from policymakers have seemingly ruled out the possibility of a 50 bps cut with 25 bps the most likely outcome.

To show they remain committed to managing rates effectively, the ECB is likely to signal that it plans to keep moving rates towards neutral levels and is open to lowering them further into easing territory if needed.

The Bank of Canada has lowered its policy rate by 125 basis points since June, and there’s a strong chance it will cut another 50 bps next week. This would bring the rate down to 3.25%, as the central bank tries to reach a neutral level quickly.

The cuts are needed as Canada struggles with slow economic growth and low inflation. There are other challenges as well while the looming threat of a Trump Presidency and tariffs when he takes office also weighs on the minds of BoC officials.

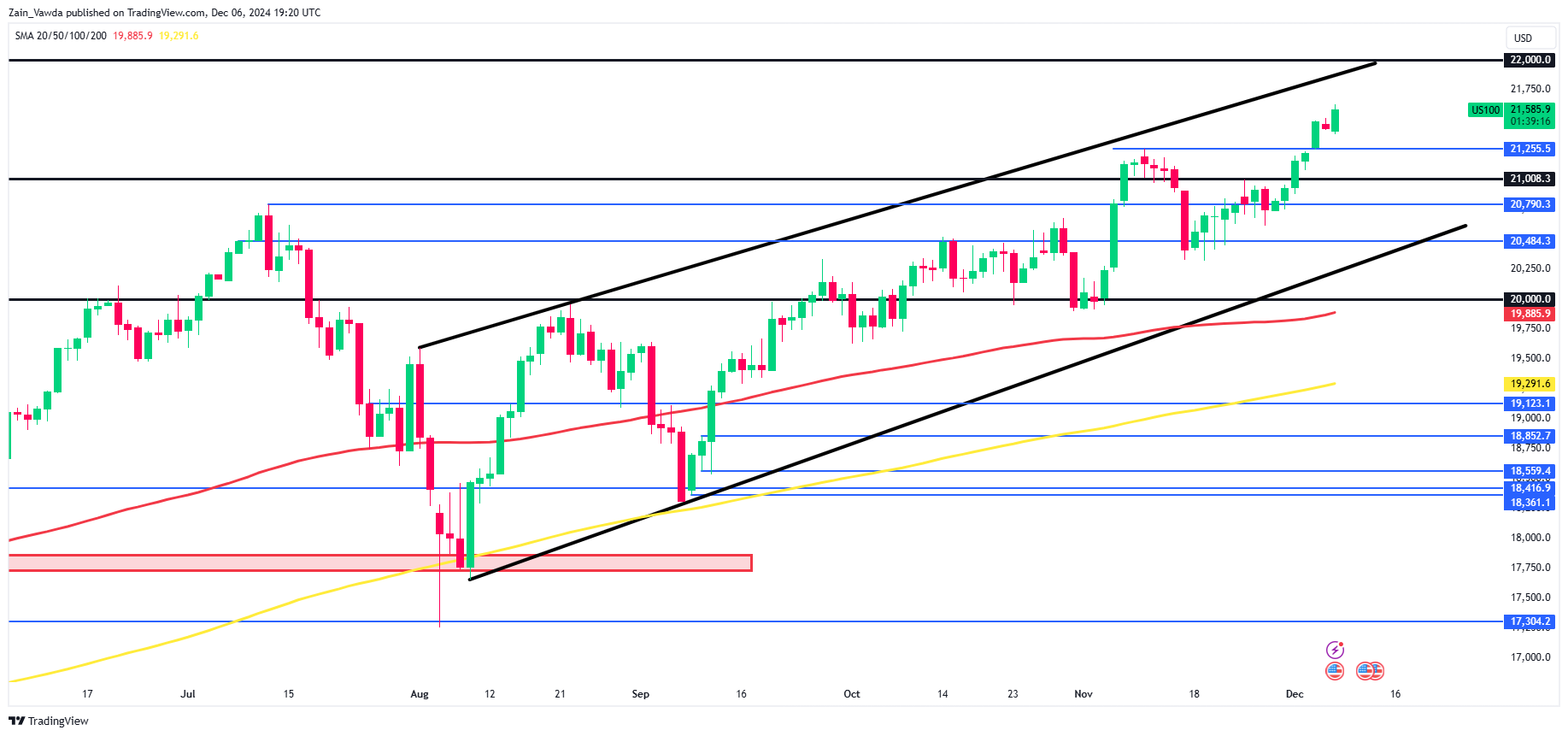

Chart of the Week

This week’s focus is now on the Nasdaq 100, following another stellar showing by US equities. The ‘santa rally they say’, looking good so far.

The Nasdaq 100 is now within 400 points of the 22000 handle following a strong end to the week as US jobs data seemed to confirm a December rate cut.

The Nasdaq is currently in a channel and the top of the channel is around the 22000 handle which would make that a key area of resistance. Before that level however the 21750 handle may also present challenge. The Nasdaq monthly open was around 20930 with the index already rising around 700 points this month.

Any pullback may be viewed as a potential opportunity for buyers to get involved. The historical performance of the index in December coupled with the current fundamentals suggest we may see more upside before the month comes to a close.

My bias remains bullish for the Nasdaq but getting involved now would pose the risk of a correction before the next leg to the upside.

Nasdaq 100 Daily Chart – December 6, 2024

Source: TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 21255

- 21000

- 20790

Resistance

- 21750

- 22000

- 22250

The Weekly Bottom Line: Data Clears the Path for the Rate Cut in December

Canadian Highlights

- The odds of a 50 basis-point rate cut rose to 80% as the unemployment rate ticked up to its highest level since January 2017 (excluding the pandemic).

- There are notable positives in the jobs report. Employment rose by more than twice the consensus forecast, and the employment rate held steady in October, breaking the recent trend of declines.

- With looming tariffs, fiscal spending is poised to rise in 2025. Together with the rebound in consumer spending and real estate, this argues for a more measured 25-basis point rate cut next week. The Bank may still opt for larger cuts if it prioritizes higher unemployment rate and broader economic weakness.

U.S. Highlights

- The embattled ISM Manufacturing Index showed improvement in November, but continued to point to contraction. In contrast to manufacturing, the services sector continued to expand in November, although the pace of growth slowed.

- As was widely expected, hiring rebounded in November, with payrolls adding 227,000 new jobs, as impact of the Boeing strike and hurricanes reversed. However, an uptick in the unemployment rate increased market confidence that a Fed rate cut is in the offing.

- Vehicle sales also posted a sizeable gain in November, reaching the highest level in over three years. It is possible that some of this strength in sales came from replacement demand related to hurricane activity.

Canada – Employment or Unemployment: That is the Question

This week on Bay Street, attention centered on bank earnings, which presented a balanced mix of misses and beats, resulting in modest movement. Investors had plenty to digest with today’s employment report. The unemployment rate climbed to 6.8% - its highest level since January 2017, excluding the pandemic. This nudged the odds of a 50 basis-point rate cut up to 80% (at the time of writing) from what was previously a near coin flip. Consequently, the 10-year bond yield dropped below 3.0% mark for the first time since October, while the S&P/TSX ended the week up 0.5%.

Yet focusing solely on the unemployment rate risks missing the full picture, as the increase was driven by a boost in labour force rather than job losses. There are plenty of bright spots in the overall picture. Employment rose by 51k – more than twice the consensus forecast. Full-time positions accounted for most of the gains, extending the momentum seen in recent months. Previously, employment growth trailed the expansion in the labour force, pushing the employment rate (the share of population that is employed) lower. This time, however, the employment rate held steady, rather than declining (Chart 1).

Taken together, these figures challenge the collective wisdom of the market. We think that today’s labour market data offers little justification for aggressive monetary easing. Moreover, average hourly wage growth of 4.1% year-on-year should still be too discomforting for the Bank of Canada. Strong wage growth without accompanying productivity gains fuels inflationary pressures, strengthening the case for a measured approach to rate cuts.

There are other reasons to tread carefully as 2025 approaches. President-elect Donald Trump’s renewed threats of tariffs loom large, potentially making trade dynamics a critical swing factor. In October, Canada’s merchandise trade balance recorded its eighth consecutive monthly deficit. Although exports rose for the first time in four months, modest import gains outpaced the improvement. Nonetheless, trade with the United States remained a bright spot. Despite declining, the value of exports to the U.S. exceeded the value of imports, contributing positively to Canada’s overall trade balance. This trend has played growing role on economic activity since the USMCA came into effect in mid-2020 (Chart 2).

This trade surplus with the U.S. is precisely what Trump opposes and demands stronger border security in exchange for Canada avoiding tariffs. As a result, any trade deal would likely entail increased spending on border security and defense. This would add to fiscal stimulus initiatives, such as tax holidays and direct payments.

Finally, recent rebounds in consumer and real estate activity argue for the Bank of Canada taking incremental steps to reduce restrictive monetary policy and avoiding steps that could exacerbate inflationary pressures. Still, policymakers may focus on the spike in the unemployment rate and the broader weakness in economic activity, opting to cut rates by another 50 basis points. The wait is almost over – attention now shifts to next Wednesday’s policy decision.

U.S. – Data Clears the Path for the Rate Cut in December

It’s not just the Christmas holidays that are fast approaching. The next Federal Reserve meeting is also just around a corner, and this week featured several important updates for signals on the health of the U.S. economy. This week’s results were broadly positive: contraction eased in manufacturing, activity continued to expand in the services sector, job growth rebounded in November, as did vehicle sales. Vehicle sales registered their highest level in over three years, although it is possible that some of this strength came from replacement demand related to hurricane activity.

The embattled ISM Manufacturing Index showed improvement in November, but still signaled that activity is contracting. Overall, the manufacturing sector has gained some momentum, with the new orders index rising for the third consecutive month, since the Fed began cutting interest rates. However, regulatory and trade policy cloud the outlook. In contrast to manufacturing, the services sector continued to expand in November, although the pace of growth slowed. Still, with 14 out of 18 industries reporting growth, the services sector appears to be in relatively good shape.

As expected, hiring rebounded in November, with payrolls adding 227k new jobs (Chart 1). Revisions also added 56k jobs to the gains seen in the prior two months. Smoothing through the recent volatility, job gains have averaged 173k over the past three-months, or only a modest step down from the 186K averaged over the prior twelve-month period. But this likely overstates the degree of “strength” in the job market. In the household survey, the unemployment rate backed up one tenth to 4.2%, after spending September and October at 4.1%.

Other indicators, such as the Job opening and labor turnover survey (JOLTS), similarly point to a labor market that has come into balance and is no longer a meaningful source of inflationary pressure. JOLTS data, released this week, showed that while job openings increased in October, the uptick was narrowly concentrated in professional and business services and leisure and hospitality. Meanwhile, both the quit rates and the hiring rate are below their pre-pandemic levels. This suggests that the employers are becoming more selective, while workers are less eager to leave job voluntarily. Indeed, with no significant premium for job switching (Chart 2) and given the low hiring rate, landing a new job may be challenging.

Comments from the latest Fed’s Beige book also reflected this trend, stating that “hiring activity was subdued as worker turnover remained low” and that “wage growth softened to a modest pace”. The Beige book, along with the payrolls and especially the next week’s inflation report will help to solidify the Fed’s stance on their next rate move later this month. The cooling labor market should give the policy makers confidence for another quarter point cut. However, with inflation showing some stickiness lately, and in the words of Jerome Powell this week, the Fed could “afford to be a little more cautious”. The market is pricing nearly 90% odds of a December cut, but the path for rate cuts in 2025 is less clear.