Sample Category Title

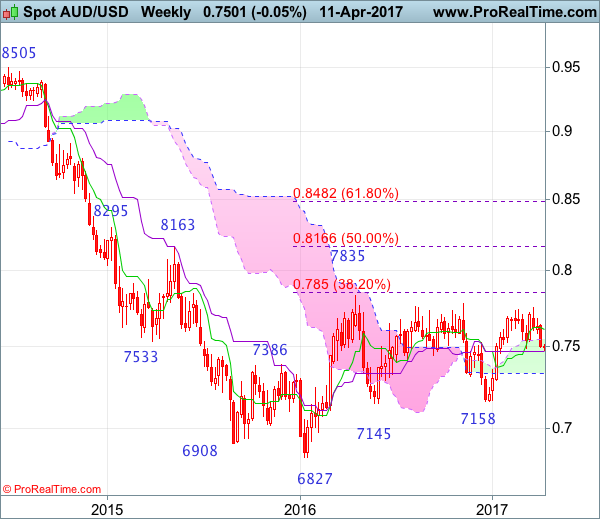

AUD/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting doji

• Time of formation: 20 Feb 2017

• Trend bias: Sideways

Daily

• Last Candlesticks pattern: Bearish engulfing pattern

• Time of formation: 21 Mar 2017

• Trend bias: Near term down

Aussie has dropped quite sharply last week and broke below indicated support at 0.7491, dampening our bullishness and suggesting top has been formed at 0.7750 last month, hence consolidation with downside bias is seen for this fall from 0.7750 to bring at least a strong retracement of the rise from 0.7158 and further decline to 0.7450-55 (50% Fibonacci retracement of 0.7158-0.7750), then towards 0.7380-85 (61.8% Fibonacci retracement), however, reckon downside would be limited to 0.7300-10 and bring rebound later.

On the upside, whilst initial recovery to 0.7540-50 cannot be ruled out, reckon the Tenkan-Sen (now at 0.7569) would limit upside and bring another decline later. Only a daily close above the Kijun-Sen (now at 0.7612) would abort and signal first leg of decline from 0.7750 has ended, bring a stronger rebound to 0,7640-50 but resistance at 0.7680 should cap upside, price should falter below 0.7700-10, bring another decline later.

Recommendation: Sell at 0.7570 for 0.7390 with stop above 0.7670.

On the weekly chart, last week’s selloff below support at 0.7491 formed a black candlestick with price closing near the week’s low, signaling top has been formed at 0.7750 and consolidation with downside bias is seen, a weekly close below the Kijun-Sen (now at 0.7468) would add credence our view that the rebound from 0.7158 has ended at 0.7750, then further choppy trading below previous resistance at 0.7778 would take place with mild downside bias for further fall towards 0.7380-85 (61.8% Fibonacci retracement of 0.7158-0.7750), however, reckon downside would be limited to 0.7290-00, bring recovery later.

On the upside, expect recovery to be limited to 0.7565-70 and the Tenkan-Sen (now at 0.7612) should hold, bring another decline later. Above last week’s high at 0.7641 would risk test of resistance at 0.7680 but only a sustained breach above this level would signal the retreat from 0.7750 has ended instead, bring another bounce towards this level. Looking ahead, only break of 0.7778 resistance would suggest a possible upside break of early established broad range, bring further rise to 2016 high at 0.7835, above there would confirm and encourage for headway to 0.7900 and later towards psychological level at 0.8000.

Technical Outlook: EURUSD – Plethora Of Strong Barriers Likely To Limit Repeated Recovery Attempts

The Euro remains at the front foot on Wednesday and probes again above daily cloud top (1.0613) for renewed attack at next significant barrier at 1.0622 (100SMA), following Wednesday's spike to 1.0628.

Strong upside rejection on Wednesday that left daily candle with long upper shadow is expected to weigh on near-term action, as daily studies remain in bearish setup.

The pair faces a cluster of barriers between 1.0613 and 1.0635 (cloud top/100SMA and daily Tenkan-sen in steep descend) which is seen as strong obstacle for the euro to extend near-term recovery leg from 1.0570 low.

Also, growing fears about the outcome of French elections keeps traders cautious and may limit recovery attempts.

Near-term action is also pressured by falling thick 4-hr Ichimoku cloud (spanned between 1.0664/1.0769), base of which should cap extended upticks.

Res: 1.0622, 1.0635, 1.0650, 1.0664

Sup: 1.0593, 1.0577, 1.0568, 1.0524

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 10612

The intraday bias is slightly positive after 1.0567 low and initial resistance lies at 1.0640. Crucial on the downside is 1.0580 support and a break through that low will challenge 1.0490 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.0640 | 1.0828 | 1.0580 | 1.0490 |

| 1.0700 | 1.0904 | 1.0490 | 1.0340 |

USD/JPY

Current level - 109.52

Yesterday's break through 110.10 lows signals a completion of the prolonged consolidation pattern and the bias is bearish, for a slide towards 108.50 area. Major resistance lies at 110.10.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.50 | 113.50 | 110.10 | 110.10 |

| 112.26 | 115.65 | 110.10 | 107.80 |

GBP/USD

Current level - 1.2487

The intraday bias is positive after the break through 1.2450, as the pair is currently testing 1.2500 resistance area. A violation of the latter will challenge 1.2500 and 1.2620.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2500 | 1.2620 | 1.2450 | 1.2230 |

| 1.2620 | 1.2705 | 1.2364 | 1.2107 |

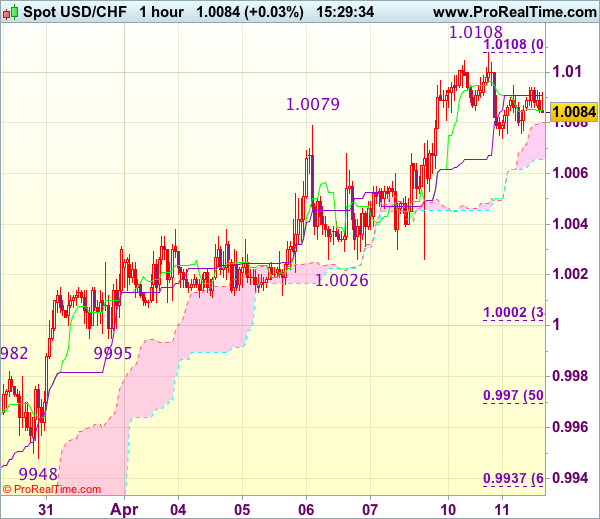

Trade Idea : USD/CHF – Buy at 1.0000

USD/CHF - 1.0072

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0071

Kijun-Sen level : 1.0074

Ichimoku cloud top : 1.0088

Ichimoku cloud bottom : 1.0067

Original strategy :

Buy at 1.0000, Target: 1.0100, Stop: 0.9965

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0000, Target: 1.0100, Stop: 0.9965

Position : -

Target : -

Stop : -

Dollar’s retreat after rising to 1.0108 on Monday has retained our view that consolidation below this level would be seen and initial downside risk is for pullback to 1.0050, then towards support at 1.0026, however, reckon 0.9995 support would contain weakness and bring another rise later, above indicated resistance at 1.0108-09 would extend recent upmove from 0.9813 towards 1.0140-45 but loss of upward momentum should prevent sharp move beyond another previous resistance at 1.0171, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as support at 0.9995 should limit downside. Below 0.9970 (50% Fibonacci retracement of 0.9831-1.0108) would abort and signal top is formed instead, bring correction to support at 0.9948.

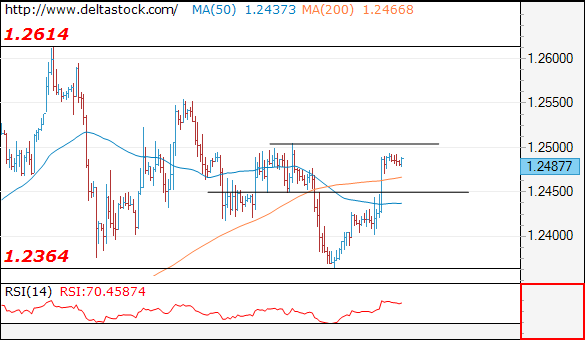

Trade Idea : GBP/USD – Stand aside

GBP/USD - 1.2487

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2488

Kijun-Sen level : 1.2449

Ichimoku cloud top : 1.2422

Ichimoku cloud bottom : 1.2415

Original strategy :

Exit short entered at 1.2475,

Position : - Short at 1.2475

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As cable has maintained a firm undertone after yesterday’s rally, suggesting low has been formed at 1.2365 on Monday and near term upside risk remains for the rebound from there to extend gain to resistance at 1.2506, however, break there is needed to add credence to this view and bring further rise to 1.2525-30 but near term overbought condition should prevent sharp move beyond previous chart resistance at 1.2559, bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 1.2445-50 would suggest an intra-day top is possibly formed, bring weakness to 1.2420, break there would confirm and bring further fall to 1.12400-05 which is likely to hold on first testing.

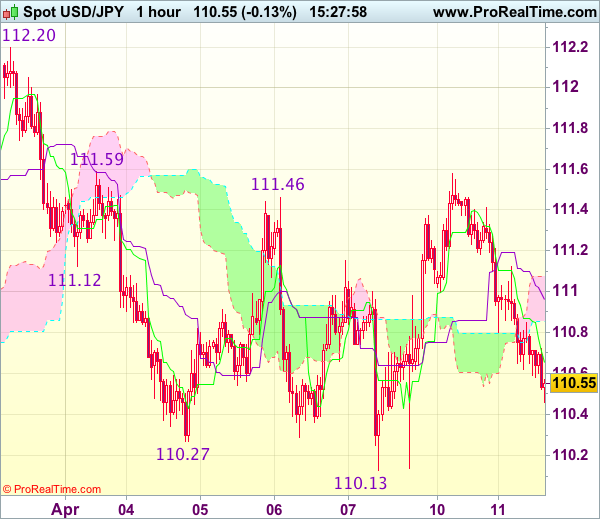

USD/JPY Drops Below 110 Psychological Support

Sunrise Market Commentary

- Rates: Risk aversion erases payrolls

Two days of risk aversion – Monday in Europe on Mélenchon's rise in French presidential election polls and Tuesday in the US on the administration tough stance against North Korea & Syria –erased all of Friday's payrolls-induced losses on US Treasuries. The US 5- and 10-yr yields are testing key support levels again. Will risk sentiment improve and avoid a ST break? - Currencies: USD/JPY drops below 110 psychological support

Geopolitical tensions dominated yesterday's FX trading with the yen the mighty winner. USD/JPY dropped below 110 support. EUR/USD remained nearly unchanged as narrowing rate differentials were no help for the euro. Lingering geopolitical concerns still affect Asian trading overnight, but FX moves peter out. Sentiment-driven trading today?

The Sunrise Headlines

- US equities limited its losses to 0.14% (S&P) after a weak opening dominated by geopolitical concerns. Asian equities are modestly down with Japan underperforming (-1.25%) on yen strength.

- 'We are not going into Syria,' President Trump said. His comments may dilute Rex Tillerson's message in Moscow for Russia to drop its support for Assad. However, he kept up his jawboning against North Korea, saying the US is sending a 'very powerful' armada to deliver a message to Kim Jong Un's regime.

- The yen, gold and Treasuries rose as haven assets extended gains amid lingering concern about the geopolitical tensions. US equity- futures slipped along with Asian equities. Moves are small though and won't necessarily be followed in Europe and US later today

- Saudi Arabia will probably support extending supply cuts for 6 months when OPEC meets. The decision depends on the stance of Iraq, Iran and Russia. In the US, API data showed a decline in inventories. Brent moves up to $56.45/barrel.

- Global reflation got a status check. Chinese PPI slowed to a 7.6% Y/Y advance in March from 7.8% Y/Y in February. Japan's PPI increase accelerated to 1.4% Y/Y in March, from a revised 1.1% Y/Y in February.

- Italy has moved to avoid punishment from Brussels over its public finances as the centre-left government led by Paolo Gentiloni approved €3.4B in extra budget deficit cuts in an effort to meet EU demands.

- Today's market calendar remains very light with only the UK labour data, auctions in US, Germany, Ireland and Italy and a Bank of Canada policy meeting

Currencies: USD/JPY Drops Below 110 Psychological Support

Dollar loses ground, especially versus yen

On Tuesday, the dollar traded with a marginal negative bias going into the US session, but geopolitical tensions (Tough US comments addressed to Russia/Syria & N-Korea) flared up, pushing US yields and equities down. The yen played its traditional safe haven role. USD/JPY approached the psychological 110 level for the third time. Without hesitation, traders pushed the pair this time through the level which accelerated the downfall of the pair, but a pause intervened shortly afterwards simultaneous with US Treasuries peaking and equities bottoming. USD/JPY hovered sideways with a negative bias towards a 109.62 close, ignoring the intraday recovery of US equities.

The price action in EUR/USD was far less spectacular. The euro struggled higher from about 1.0580 to 1.0620 at European noon and stabilized at that level during early US dealings. It only slightly followed later on the steep rise of US Treasuries (narrowing yield spreads), the fall of equities/yen, reaching an 1.0630 intraday high when these other markets peaked/bottomed. It could not even hold on to these slim gains and dropped back to about 1.0605 where it closed. Barely up from the previous 1.0596 finish. So, the euro couldn't profit from dollar weakness and a sharp narrowing of the yield differentials. It was one of the weakest G-10 currencies versus the dollar. We suspect that political risks inside the euro area (France/Italy?) keep the euro weak which matched dollar weakness. The EUR/USD decline in the previous week was stopped this week, but there is no signal yet that the euro could really fight back and conquer the lost ground. Overnight: Dollar stabilizes in calm trading

The overall dollar stabilized near yesterday's lows. There is still a lingering safe haven bid on geopolitical concerns as US Treasuries, gold and yen are, albeit insignificantly, lower (see headline for latest geopolitical news). Oil continues to rise. Chinese PPI slowed in March to a still high 7.6% Y/Y, while Japanese PPI rose to 1.4% Y/Y from 1.1% Y/Y in February. EUR/USD is near yesterday's 1.0605 close having traded in a 1.0595 to 1.0615 range overnight. USD/JPY set a new MT low at 1.0935, but trades currently at 109.55 on lingering geopolitical concerns.

Calendar uneventful, FX trading too?

The market calendar is uneventful (see rates). FX trading will be dominated by risk sentiment and technicals. Will the break in USD/JPY below 110 be confirmed? For EUR/USD we are in no-man's land. The dollar rally petered out, but there are no signs yet of a euro counterattack. The eco calendar heats up tomorrow and the US earnings season starts for real. That may bring more animus, but market closures on Good Friday and thinly staffed desk tomorrow may keep the dollar in a bind till after Easter.

Technicals: USD/JPY picture deteriorates

From a technical point of view, USD/JPY broke through the 110 key support, extending its decline to 109.35, after having failed to regain the 111.36/60 previous range bottom. We downgrade our USD/JPY assessment to bearish, as long as the pair does not break and sustain above 112.20 (neckline ST double bottom). It becomes tactically a sell on upticks environment. USD/JPY has intermediate support at 109.38 (reached today, 50% retracement 100.09/118.66) and 107.18, 62% retracement). EUR/USD extensively tested the topside of the MT range (1.0874/1.0906 area) two weeks ago, but the test was rejected. EUR/USD returned lower in the 1.0875/1.05 trading range with the odds for a test of the downside of the range, but the dollar's advance stopped in past two days, suggesting the dollar rally is a bit tired.

EUR/USD: Dollar cannot prolong its rally and stabilizes ahead of obvious 1.05 support. Too difficult or simply a pause?

EUR/GBP

Sterling: Strong performance versus EUR and USD

At their previous policy meeting, the BoE (MPC) showed they saw little room to let inflation move much higher without tightening policy. However, their concerns proved premature as inflation behaved well in March. There was a knee-jerk reaction pushing sterling stronger versus euro and dollar. However, the absence of follow through sterling buying caught the eye and gains were in no time erased. It looked like it would become a session to forget fast. However, all changed in late European trading. Sterling started to climb against both euro and dollar. It did coincide with the risk-off move in US treasuries, yen and gold. Sterling yields fell less than US ones, which might be an explanation for the cable gains, but that wasn't the case versus German yields. Admittedly, the FTSE 100 outperformed European and US indices. Nevertheless, the advance is difficult to explainan by the fundamentals. There is Brexit and a current account in deficit, which is not the environment to receive safe haven inflows. Whatever, EUR/GBP dropped from about 0.8530 without interruption to a 0.8490 close, which is technically not yet significant with 0.8484 intermediate support before the 0.8409/00 key support. Overnight sterling traded volatile but in a narrow range.

The UK labour market data will be key today. February's labour market figures should highlight that while the jobs market remains tight, wage growth is still subdued. A strong report would help sterling eke out more gains, but did the market front-run yesterday? We have a neutral short-term bias on EUR/GBP. The EUR/GBP 0.88/0.84 range should guide trading for now. Last week, the sterling rally/short-squeeze ran into resistance, but yesterday there was again some fire in sterling. We see no trigger though for a real change in sentiment yet. Longer term, Brexit-complications remain a potential negative for sterling. The BoE won't raise rates anytime soon.

EUR/GBP sterling gained ground yesterday, but without an obvious driver. Anticipation on today's labour market report?

Trade Idea : EUR/USD – Sell at 1.0665

EUR/USD - 1.0615

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.0607

Kijun-Sen level : 1.0604

Ichimoku cloud top : 1.0619

Ichimoku cloud bottom : 1.0590

Original strategy :

Sell at 1.0665, Target: 1.0565, Stop: 1.0700

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0665, Target: 1.0565, Stop: 1.0700

Position : -

Target : -

Stop : -

As the single currency has recovered again after finding support at 1.0595 earlier today, retaining our view that further consolidation would be seen and initial upside risk remains for the rebound from 1.0570 low to extend gain to 1.0630, then 1.0650, however, reckon upside would be limited to 1.0667 resistance (Friday’s high) and bring another decline later, below said support at 1.0595 would bring retest of Monday’s low at 1.0570, break there would extend the decline from 1.0906 to 1.0550-55 (50% projection of 1.0906-1.0635 measuring from 1.0689), then 1.0525-30.

In view of this, would not chase this fall here and would be prudent to sell dollar on further recovery as 1.0667 resistance should limit upside. Only a firm break above said resistance at 1.0667 would abort and suggest low is formed instead, risk a stronger rebound to 1.0689, then 1.0702.

Trade Idea : USD/JPY – Sell at 110.30

USD/JPY - 109.63

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 109.55

Kijun-Sen level : 110.04

Ichimoku cloud top : 110.94

Ichimoku cloud bottom : 110.86

New strategy :

Sell at 110.30, Target: 109.30, Stop: 110.65

Position : -

Target : -

Stop : -

Yesterday’s selloff below support at 110.11 on active cross-buying in yen in part due to risk aversion suggests recent entire decline 118.66 top is still in progress, hence downside bias remains for recent decline to extend weakness to 109.30-35, then towards 109.00-05 (123.6 times projection of 112.20-110.13 measuring from 111.58), however, near term oversold condition should prevent sharp fall below 108.85 (61.8% projection of 115.51-110.11 measuring from 112.20) and reckon 108.40-50 (100% projection of 118.66-111.55 measuring from 115.51) would hold, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 110.30-40 should cap upside and bring another decline. Above 110.70-75 would defer and risk a stronger rebound to 111.00-05 but price should falter well below resistance at 111.58.

Asia Markets Seek Safe Havens

The G-7 Nations acting like the League of Nations seems to have finally opened the floodgates as markets seek safe havens ahead of the Easter break.

As expected, in all honesty, the G-7 officials meeting about a recalcitrant Russia produced nothing new on the sanctions front. Talk of vested interests amongst the G-7 members is perhaps a bit harsh when cool heads should prevail. It did give an overall look of appeasement though, and this seems to have stirred the U.S. markets into action with the theme of the session being seeking safe havens anywhere.

Gold rose 20 USD to 1275, U.S 10-year yields fell below 2.30%, and the USD/JPY dropped 100 points and finally broken the crucial level at 110.00. Elsewhere the U.S. Index (DXY) pushed slightly lower, and the Korean Won fell to just shy of the psychological 1150 level.

The theme continues in Asia with equities generally in the red to start the session. Most notably the Nikkei and Kospi. Precious metals continue to be bid across the board; the U.S 10-year trades at 2.28% and both Brent and WTI have moved higher. Tensions in Europe, the Middle East and the Korean Peninsular have made the geopolitical situation more complicated than re-writing the United Airlines customer service manual.

As Easter approaches Asia, in particular, is focusing on this Easter Friday which is the anniversary of the birthday of the North Korean founder, Kim Il-sung. The North would normally do “something” on this day, as is their want. This year, it’s an almost global holiday, and given the present backdrop, it will have more poignancy. This should ensure that Asia remains solidly in a risk-off mode for the rest of the week, come what may in other centres.

Looking at the markets in Asia today.

FX

USD/JPY

The story of the night as repatriation flows turned to a deluge and USD/JPY finally cracked the 110.00 level. The USD/JPY continues to trade heavily in Asia with the Nikkei. However, those expecting a wholesale collapse may be disappointed as the USD/JPY enters oversold territory on the RSI.

The 110.00 level is now resistance followed by 111.50.

Support appears initially at the 50% Fibonacci at 109.13 and then the 200-day moving average at 108.55.

EUR/JPY

It is reasonable to assume that every cross ending in XXX/JPY didn’t have a great night. EUR/JPY being no exception with its 2nd consecutive close below its 200-day moving average. However, I do note that the cross is now very oversold on it RSI and Stochastic.

Resistance is at the top of its downward parallel channel at 117.80 which is also the area of the 200-day moving average. Initial support is around 80 points away at the bottom of the channel at 115.50. A breakout from here would set the

Initial support is around 80 points away at the bottom of the channel at 115.50. A breakout from here would set the scene technically for a move sub 114.00.

USD/CNH

Quietly appreciated against the USD in the Asian session as the PBOC refrained from open market operations yet again. A slightly softer than expected CPI read of -0.3 % M/M saw a small reversal as the edge was taken of tightening expectations.

With USD/CNH trading at 6.9020 as I write, the key levels continue to be 6.8400 and 6.9300 with the cross continuing to range.

PRECIOUS METALS

GOLD

Precious metals were big movers overnight including gold. The 1.60% move higher to 1275 where we are now trading is significant because we have finally had a close above the 200-day moving average after failures all year.

Apart from being an obvious beneficiary of the delayed safe-haven trade, from a technical perspective, the charts point to a move above 1300 now.

Support is clearly delineated at the 200-day moving average at 1257.50 and 1240.

Resistance is at the Asia session high of 1280 before a triple top from October at 1308. However, traders should keep an eye on the RSI and Stochastics for signs of bearish divergence.

SILVER

Rose 2.40% in overnight trading to 18.3250 following gold as a safe haven darling. Asia has had another look at the upside to 18.4400 before falling back to roughly unchanged at 18.3250.

Silver has key resistance just above here at 18.4500 where it has failed multiple times, most recently last Friday. A close above clearly opens a technical move to 19.0000 on the charts.

Support meanwhile, lies at 18.0725 the 200-day moving average and then yesterday’s lows at 17.9000.

ASIA INDICES

NIKKEI 225

The Nikkei has fallen over 1.0% today as the large move up in the Yen vs. the USD saw exporter stocks sold. The ongoing situation with Toshiba and its non-endorsed accounts continues to weigh as well, with delisting a real possibility. The YEN appreciation on safe haven flows and a compressing of the US/Japan yield spreads will continue to weigh on the index. The Nikkei continues to bump along its four-month lows.

The Nikkei has intraday support at 18.585 with a daily close below suggesting a move to the next support around 18200. We have traded below this level today, but a recent bounce to 18626 means it is the daily close we must watch.

The Nikkei has resistance at 18945, Monday’s high and then the 19145/19225 zone, the 100 and 200-day moving averages.

SUMMARY

Global tensions and a rush to safety ruled the New York session, and this has followed through to Asia. The break of 110 in USD/JPY is extremely significant. With a long weekend globally nearly upon us and further North Korea risk this Friday, the safety first theme is likely to continue.

Geopolitical Tensions Keep Rising

Market movers today

In the UK, the labour market report for March is due. We estimate the unemployment rate (3M average) will be unchanged at 4.7% while we estimate the annual growth rate in average weekly earnings (3M average) declined to 2.0% y/y from 2.3% y/y. The combination of higher inflation and slower wage growth means real wage growth is turning negative, implying less scope for private consumption growth. This is one of the reasons why we expect UK GDP growth to slow this year. Indeed, we have seen the first signs that this is actually happening. In recent months, retail sales have plunged the most since the financial crisis and although it is a weak indicator, it is a sign that private consumption growth has actually slowed.

Otherwise, there is very lit t le happening on the data and macro front ahead of the Easter holiday

Note. Due to the Easter holidays, the next publication of Danske Daily will be Tuesday 18 April.

Selected market news

Geopolitical tensions keep rising as the US Secretary of State Rex Tillerson accused Russia of t rying to shield Syria's government from the blame for a deadly gas at tack (full story Reuters). However, in a Fox interview, Donald Trump stated that he has no plans of 'going into Syria'. Tensions are also rising on the Korean peninsula, where the Japanese navy plans to joins the US navy in deterring the North Korean regime from further missile tests.

Swedish inflation decreased in March (CPI: 1.3% and CPIF: 1.5%) and printed well below both market expectations and t he Riksbank's t arget . While t he t iming of East er holds some of the explanat ion (some rebound can be expected in April), the Riksbank's chances of reaching the 2% inflat ion target over the next couple of years seem slim, given that significant wage drift on top of cent ral wages will be necessary, a t rend not observed in recent years.

The Bank of Japan (BoJ) and Minist ry of Finance have released their balance of payment data (i.e. Japanese investor flows ) for February. While the Japanese investor decreased their holdings of foreign debt generally, the most noteworthy was the fact that Japanese investors accounted for net selling of more than EUR12bn of French government bonds, while increasing t heir purchases of German government bonds. This 'safe haven' flow is likely to be closely related to the polit ical uncertainty stemming from the upcoming French election.

Yesterday's risk-off moves seen in the European and American markets have spilled into the Asian session, with Hang Seng t rading slight ly lower and Nikkei losing some 1.2% at the t ime of writ ing. It should be noted that USD/JPY has moved below the 110 mark for the first time since mid-November last year and has been trading in the 109.40-109.50 range this morning.