Sample Category Title

USD/CHF Remains Weak, USD/CAD Weak Recovery Bounce, AUD/USD Remains Weak.

USD/CHF Remains weak.

USD/CHF is consolidating below new high at 1.0107. Hourly support is given at 1.0039 (07/04/2017 base low) then 0.9814 (27/03/2017 low). Key resistance can be found at a distance at 1.0171 (07/03/2017) then 1.0344 (15/12/2016 high). Expected to show another leg higher.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Weak recovery bounce.

USD/CAD is trying to bounce yet demand is thin. Short-term bullish technical pattern has quickly reversed, indicating further downside pressure. Key support is given at 1.3265 (21/03/2016 low) is in focus then 1.2969 (31/01/2017 low). Resistance can be located at 1.3427 (10/04/2017 high) then 1.3456 (04/04/2017 range high).

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Remains weak.

AUD/USD weak bounce near the support has thus far unimpressive failed to find momentum, confirming persistent selling pressures. Next meaningful support is located at 0.7449 (13/01/2017 low). Resistance can be located at 0.7515 (intraday high and downtrend channel top). • In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

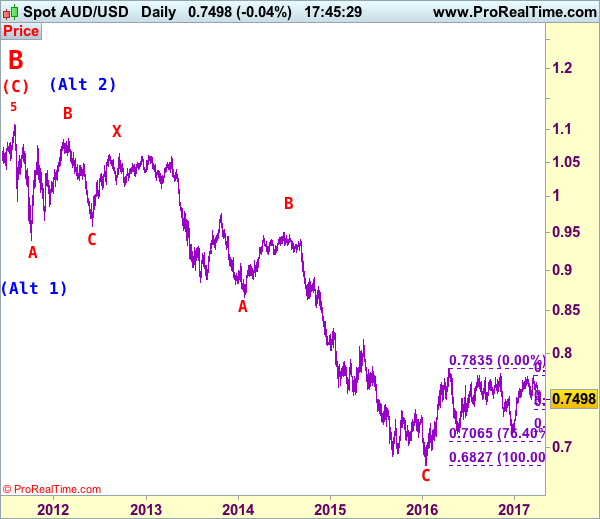

AUD/USD Elliott Wave Analysis

AUD/USD – 0.7574

AUD/USD – Wave 5 of C and (B) has possibly ended at 1.1081

Aussie has dropped sharply last week and finally broke below support at 0.7491, suggesting recent entire rise from 0.7158 has indeed ended at 0.775 last month, hence further choppy trading within early established range would be seen and downside risk remains for the decline from 0.7750 to bring at least a strong correction of the aforesaid rise, initial downside target is seen at 0.7450-55 (50% Fibonacci retracement of 0.7158-0.7750), then towards 0.7380-85 (61.8% Fibonacci retracement), however, near term oversold condition should prevent sharp fall below 0.7300-10 and reckon 0.7280-85 would hold from here, bring rebound later.

We are keeping our count that top has been formed at 1.1081 (wave 5 of V) and major correction (A-B-C-X-A-B-C) has commenced, indicated downside targets at 0.7945 (61.8% Fibonacci retracement of entire rise from 0.6007-1.1081) and 0.7750 had been met and downside bias is seen for further weakness to 0.6800, then 0.6700 but reckon 0.6500 would hold from here.

Our preferred count is that the rally from 0.6007 to 0.7270 (7 Jan 2009) is marked as wave A, the retreat to 0.6248 (2 Feb 2009) is wave B and the subsequent upmove is labeled as wave C with wave (iii) and wave (iv) ended at 0.8265 and 0.7700 respectively and wave (v) as well as 3 ended at 0.9407, then wave 4 ended at 0.8066 (instead of 0.8578). The wave 5 has met our indicated projection target of 1.1060 and could ended at 1.1081, this level is now treated as the peak of wave (C) as well as larger degree wave B, hence major fall in wave C has commenced, our initial downside target at psychological support at 0.7000 has just been met and further weakness to 0.6500 would be seen later.

On the upside, whilst initial recovery to 0.7535-40 is likely, reckon 0.7370-80 would limit upside and bring another decline later to aforesaid downside retracement targets. A daily close above previous support at 0.7587 would defer and risk a stronger rebound to 0.7640-45 but only break of resistance at 0.7680 would abort and suggest the fall from 0.7750 has ended instead,

Recommendation: Sell at 0.7570 for 0.7390 with stop below 0.7670

Our alternate count on the daily chart treated the top formed in 2008 at 0.9851 could be a larger degree wave I and was followed by a deep and sharp correction in wave II to 0.6007 and wave III is unfolding from there.

The long-term uptrend started from 0.4775 (2 Apr 2001) with an impulsive structure. Wave I is labeled as 0.4775 to 0.9851 (15 Jul 2008), wave II has ended at 0.6007 (Oct 2008) and wave III is still in progress which may extend further gain to 1.1265.

EUR/USD Trying To Form A Short-Term Base, GBP/USD Bounce Gains Momentum, USD/JPY Bearish Break Of Horizontal Support.

EUR/USD Trying to form a short-term base.

EUR/USD is trying to bounce. Hourly support can be found at 1.0570 (i11.04.2017 low). Stronger support can be found at 1.0494 (22/02/2017 low). Resistance can be located at a distant 1.0658 (07/07/2017 reaction high). Expected to see further short-term weakness.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Bounce gains momentum.

GBP/USD has bounced near the key support at 1.2334, suggesting a potential short-term base formation. The falling trendline resistances at 1.2500 has been breached. Hourly resistance can be located at 1.2506 and key resistance stands at1.2605 (27/03/2017 high). An hourly support can be found at 1.2405 (11/04/2017 low).

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Bearish break of horizontal support.

USD/JPY has broken to the downside out of the horizontal support at 110.11 confirming a bearish bias. Other key supports lie at a distant 106.04 (11/11/2016 low). An hourly resistance can be found at 110.11, while a key resistance stands at 112.20 (31/03/2017 high).

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

Technical Outlook: Spot Gold At Fresh 2017 Highs On Strong Safe Haven Buying

Spot Gold remains tall on Wednesday and consolidating above $1270 handle, following strong rally on Tuesday (the biggest one-day gains since 15 Mar), inspired by safe haven buying on rising geopolitical tensions.

Fresh extension higher in early Wednesday posted new 2017 high at $1279, which also marks the highest traded since 10 Nov 2016.

Tuesday’s rally also generated strong bullish signal on eventual close above $1255 (Fibo 61.8% of $1337/$1122 descend).

Bulls are now focusing targets at $1286 (Fibo 76.4% retracement) and $1292 (weekly cloud top), as global political uncertainty maintains strong bullish sentiment for gold.

Rally may be interrupted by mild corrections, with last Friday’s spike high at $1270 marking immediate support, followed by former top of 27 Feb at $1263 and rising daily

Tenkan-sen / broken 200SMA at $1259/57, expected to contain extended downticks.

Res: 1279, 1286, 1292, 1295

Sup: 1270, 1263, 1259, 1257

Technical Outlook: AUDUSD – Extended Consolidation Remains Capped By 100SMA And Maintain Bearish Bias

The pair is holding within narrow consolidation for the third day, after denting key short-term support at 0.7489 (09 Mar low), but was so far unable to close below and signal bearish continuation.

Tuesday's long-legged Doji signaled strong indecision, but so far lacking reversal signals, as 100SMA (0.7513) continues to cap.

Slow stochastic is attempting to reverse from oversold r=territory on the daily chart, which would generate initial bullish signal, however, confirmation of reversal would require lift above next pivot, 200SMA at 0.7550, which is reinforced by falling 10SMA that is approaching in attempt to form bear-cross and intensify downside pressure.

Daily studies are in firm bearish mode and suggest further extension of the wave C (on which the pair is currently riding) through its FE 138.2% (current low at 0.7472) towards the base of thick daily cloud at 0.7449 and FE 161.8% at 0.7436.

Extended consolidation ahead of fresh push lower is seen as likely near-term scenario.

Res: 0.7513, 0.7550, 0.7585, 0.7596

Sup: 0.7472, 0.7449, 0.7436, 0.7400

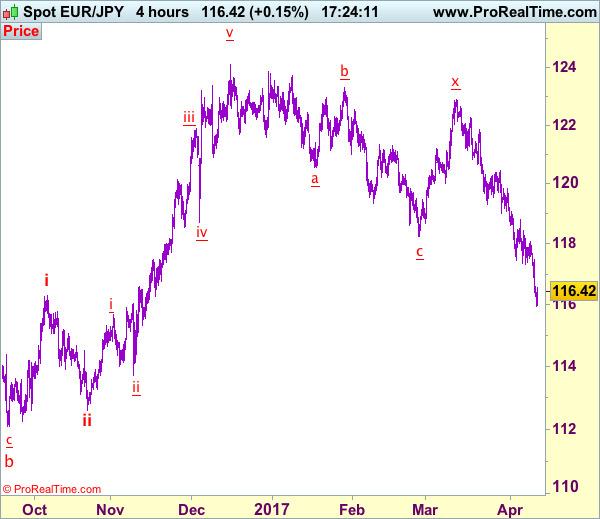

Trade Idea: EUR/JPY – Sell at 118.00

EUR/JPY - 116.41

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term down

Original strategy:

Sell at 119.00, Target: 117.00, Stop: 119.60

Position: -

Target: -

Stop: -

New strategy :

Sell at 118.00, Target: 116.00, Stop: 118.60

Position: -

Target: -

Stop:-

Yesterday’s selloff adds credence to our bearish view that recent entire fall from 124.10 top is still in progress and downside bias remains for further weakness to 115.50-60, then towards 115.00, however, near term oversold condition should prevent sharp fall below latter level and reckon 114.40-50 would hold from here, risk from there is seen for a much-needed rebound to take place later.

In view of this, would not chase this fall here and would be prudent to sell euro on subsequent rebound as 117.90-00 should limit upside. Above 118.40-45 would defer and suggest low is possibly formed, risk test of resistance at 118.80 but break there is needed to add credence to this view, bring retracement of recent decline to 119.06 resistance first.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Trade Idea: AUD/USD – Hold long entered at 0.7525

AUD/USD – 0.7496

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term down

Original strategy :

Bought at 0.7525, Target: 0.7680, Stop: 0.7465

Position: - Long at 0.7525

Target: - 0.7680

Stop: - 0.7465

New strategy :

Hold long entered at 0.7525, Target: 0.7680, Stop: 0.7465

Position: - Long at 0.7525

Target: - 0.7680

Stop:- 0.7465

As aussie has remained under pressure after breaking previous support at 0.7491, marginal weakness from here cannot be ruled out, however, loss of near term downward momentum should prevent sharp fall and bring rebound later, above 0.7550 would bring test of indicated resistance at 0.7588, break there would suggest a temporary low is possibly formed, bring rebound to 0.7625-30 and later towards resistance at 0.7680-85.

In view of this, we are holding on to our long position entered at 0.7525. Below indicated support at 0.7465-70 would signal the fall from 0.7750 is still in progress for further weakness to 0.7450-55 (50% Fibonacci retracement of 0.7158-0.7750), however, oversold condition should limit downside to 0.7380-85 (61.8% Fibonacci retracement), risk from there is seen for a rebound later.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

GBP/USD Bullish Cup With Handle Formation

.

The GBP/USD has formed a cup with handle pattern on H1 timeframe, suggesting further upside. W H4 camarilla is acting as support as the price broke above it, and it forms a clear handle at the brim of a cup. 1.2480 might spike the price to the upside, targeting D H3 H4 and H5 levels respectively, -1.2516, 1.2538, and 1.2580. If the price breaks below the handle, look for possible POC (D L3, double bottom, ATR pivot) 1.2425-45 rejection.

UK Retail Sales Fall On Rising Inflation And Slow Wage Growth

UK labour market data for March will be released at 09:30 BST including claimant count, ILO unemployment rate (from Dec to Feb) and average earnings (from Dec to Feb). The data will likely affect the strength of GBP and GBP crosses. GBP/USD hit a 1-week high of 1.2500 this morning, helped by the weakening of the dollar.

Bank of England Gorvernor Carney will make a speech at 09:30 BST this morning. We will likely get clues about the prospective measures that the BoE will likely take to cope with rising inflation, slowing wage growth and Brexit uncertainty.

The ILO unemployment rate has seen a downtrend since early 2012. UK average earnings, including and excluding bonus (from Dec to Feb), has seen a moderate uptrend in 2016. However, the increase of average earnings, excluding bonus, (from Dec to Feb) has slowed down since the beginning of this year.

UK inflation for February moved above the Bank of England’s 2% target for the first time since 2014. UK CPI (Mar), released yesterday, was 2.3% in line with expectations and the previous figure. Core CPI (Mar) fell to 1.8% in March from 2% in February. Although the latest inflation figures showed a slight slowdown the inflation uptrend is likely to continue. If the pace of wage growth is slower than the pace of inflations rise, resulting in consumers cutting down on their spending on clothing, non-food and non-necessities. It will lead to a slowdown of economic growth.

The British Retail Consortium (BRC) announced on Tuesday that UK retail sales fell by 1% in March (YoY). UK total sales edged up by only 0.1% in the January to March period marking the slowest pace of growth post the financial crisis. Non-food sales fell by 0.8% in the January to March period marking the biggest decline in nearly six years.

The dollar index plunged around 0.31% on Tuesday, falling from the psychological resistance level at 101.00 and hitting a 2-day low of 100.49. This morning the dollar index keeps on weakening thereby pushing gold prices up, spot gold hit a 5-month high of 1279.67. FOMC voting member, Neel Kashkari, was the only member to dissent the Fed’s rate hike decision in March. He stated his view on Tuesday that “there is still slack in the labour market and inflation needs to be higher”.

The Bank of Canada will announce its rate decision this afternoon at 15:00 BST. It will be followed by the BoC’s Gorvernor Poloz’s speech at 21:15 BST. Although Canadian economy is improving, however, the US economic outlook is still uncertain under Trump’s administration. The BoC is likely to keep rates on hold for the near future.

Thursday sees the release of Australian employment change and unemployment rate for March at 02:30 BST. German CPI for March will be released at 07:00 BST; it will likely affect the strength of the Euro and the trend of the DAX index.

Technical Outlook: USDJPY – Yen Hits Five-Month High Vs Dollar On Safe Haven Buying

The pair remains firmly in red following Tuesday's sharp fall (the biggest one-day fall since 15 Mar) and consolidating above fresh five-month low at 109.33, hit on early Wednesday's extension lower.

Long red candle that was formed on Tuesday is expected to heavily weigh on the market, as strong risk-off sentiment on rising geopolitical tensions, keeps yen well supported.

Eventual break below strong 110.00 support has boosted bears to continue larger bear-leg from 115.49, which is also the third wave of five-wave cycle from 118.65, towards its FE100% at 108.23.

Broken 110.00 support zone now acts as initial resistance, ahead of falling daily Tenkan-sen at 110.75.

Res: 109.73, 110.00, 110.75, 110.90

Sup: 109.33, 109.00, 108.50, 108.23