Sample Category Title

Trade Idea Update: EUR/USD – Sell at 1.0665

EUR/USD - 1.0600

Original strategy :

Sell at 1.0665, Target: 1.0565, Stop: 1.0700

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0665, Target: 1.0565, Stop: 1.0700

Position : -

Target : -

Stop : -

As the single currency recovered again after finding support at 1.0595 earlier today, retaining our view that further consolidation would be seen and initial upside risk remains for the rebound from 1.0570 low to extend gain to 1.0630, then 1.0650, however, reckon upside would be limited to 1.0667 resistance (Friday’s high) and bring another decline later, below said support at 1.0595 would bring retest of Monday’s low at 1.0570, break there would extend the decline from 1.0906 to 1.0550-55 (50% projection of 1.0906-1.0635 measuring from 1.0689), then 1.0525-30.

In view of this, would not chase this fall here and would be prudent to sell dollar on further recovery as 1.0667 resistance should limit upside. Only a firm break above said resistance at 1.0667 would abort and suggest low is formed instead, risk a stronger rebound to 1.0689, then 1.0702.

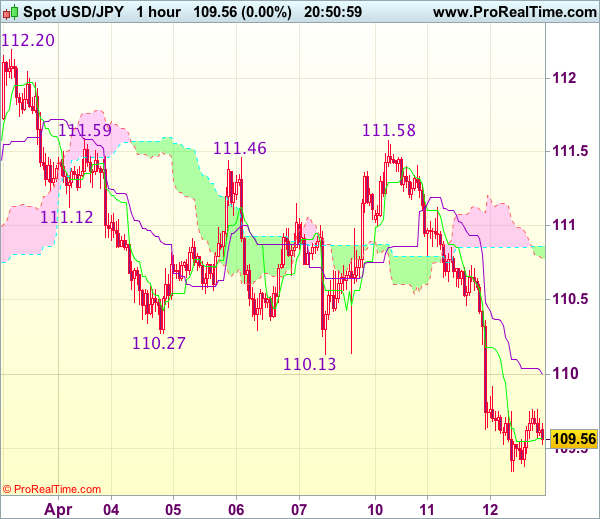

Trade Idea Update: USD/JPY – Sell at 110.30

USD/JPY - 109.55

Original strategy :

Sell at 110.30, Target: 109.30, Stop: 110.65

Position : -

Target : -

Stop : -

New strategy :

Sell at 110.30, Target: 109.30, Stop: 110.65

Position : -

Target : -

Stop : -

Yesterday’s selloff below support at 110.11 on active cross-buying in yen in part due to risk aversion suggests recent entire decline 118.66 top is still in progress, hence downside bias remains for recent decline to extend weakness to 109.30-35, then towards 109.00-05 (123.6 times projection of 112.20-110.13 measuring from 111.58), however, near term oversold condition should prevent sharp fall below 108.85 (61.8% projection of 115.51-110.11 measuring from 112.20) and reckon 108.40-50 (100% projection of 118.66-111.55 measuring from 115.51) would hold, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 110.30-40 should cap upside and bring another decline. Above 110.70-75 would defer and risk a stronger rebound to 111.00-05 but price should falter well below resistance at 111.58.

USD/CAD Tests Major Support at 1.3300 Ahead of BoC

The dollar index plunged around 0.31% on Tuesday, falling from the psychological resistance level at 101.00 and hitting a 2-day low of 100.49. The downtrend was held above the support line at 100.50. This morning during the European session, the dollar index saw a rebound.

USD/CAD has fallen 0.8% in past one week. The bulls failed to gain the significant psychological level at 1.3400.

The USD/CAD downtrend was held above the near term major support line at 1.3300 since Tuesday April 12, as the range between 1.3280 - 1.3300 is the near term major support zone, where there is stronger support.

On the 4-hourly chart, the price has been moving from the lower band to the middle band by the Bollinger Band indicator, suggesting the bearish momentum has been waning.

The Bank of Canada (BoC) will announce its rate decision and monetary policies this afternoon at 15:00 BST. It will be followed by the BoC's press conference at 16:15 BST. Be aware that the data and the press conference will likely affect the strength of CAD and CAD crosses.

Although Canadian economy is improving, however, the US economic outlook is still uncertain under Trump's administration. The BoC is likely to keep rates on hold for the near future.

Keep a close eye on the US retail sales and CPI figures (Mar), to be released at 13:30 BST this Friday April 14. It will likely cause volatility for USD and USD crosses.

The resistance level is at 1.3330, followed by 1.3340 and 1.3355.

The support line is at 1.3315, followed by 1.3300 and 1.3280.

EURUSD: Bearish, Broader Bias Remains Lower

EURUSD: With the pair remaining weak and vulnerable despite its price hesitation on Tuesday, more weakness is envisaged. Resistance comes in at 1.0650 level with a cut through here opening the door for more upside towards the 1.0700 level. Further up, resistance lies at the 1.0750 level where a break will expose the 1.0800 level. Conversely, support lies at the 1.0550 level where a violation will aim at the 1.0500 level. A break of here will aim at the 1.0450 level. All in all, EURUSD faces further bear threats in the days ahead.

Euro Quiet, German Inflation Slips

EUR/USD continues to have a quiet week. Currently, the pair is trading at the 1.06 level. On the release front, German WPI came in at 0.0%, short of the forecast of 0.4%. In the US, there are no major events on the schedule. President Donald Trump will conduct an interview with the Fox Business Network, and will discuss health care, tax reform, and the crisis in Syria. On Thursday, the US releases three key indicators – PPI, unemployment claims and UoM Consumer Sentiment.

The eurozone economy has improved in the first quarter in 2017, and this has been reflected in investor confidence levels, which have moved higher. Eurozone Sentix Investor Confidence climbed to 23.9 points in April, pointing to strong optimism among investors and analysts. German ZEW Economic Sentiment, which surveys the mood of German investors, sparkled in April, jumping to 19.5 points, well above the forecast of 13.2 points. This marked the strongest reading since August 2015.

On Monday, Federal Reserve Chair Janet Yellen said that with the economy close to full employment and 2 percent inflation, Fed policymakers were looking to reduce the support that the central bank was providing the economy. The minutes of the March meeting indicated that the Fed plans to trim the $4.5 trillion balance sheet, which has ballooned as a result of the huge asset-purchase program which started in 2008. The Fed plans to raise rates twice more in 2o17, with the next rate expected in June. Yellen emphasized that the Fed’s policy stance is neutral, as interest rate increases will be gradual, given that the economy is growing at a moderate pace.

US Nonfarm Payrolls was unexpectedly soft in March, as the economy produced just 98 thousand jobs, compared to an estimate of 174 thousand. However, the good news is that the weak reading was not accompanied by higher unemployment numbers. The unemployment rate dropped to 4.5% and jobless claims fell sharply to 234 thousand. This means that the Fed is unlikely to lose any sleep over the weak payrolls report, and will remain on course to raise rates twice more in 2017 (a majority of FOMC voting members favor two more hikes, while some members have called for three more hikes this year). According to the CME Group, the markets have circled June as the next likely date for a hike, which is priced in at 67 percent.

Haven Trades Fade As Yen, Treasuries Erase Gains

Despite safe haven flows remaining the prevalent market theme on geopolitical risks related to conflicts in Syria and saber rattling by North Korea, investors are shifting away from the worst of theses levels as yen, U.S Treasuries and gold erase their gains ahead of the U.S open.

Note: Yesterday, the Vix had spiked to a two-week high, while U.S 10's tested a key long-term support of +2.30%, and the Nikkei was the worst performing major index on Yen strength (both Nikkei and USD/JPY are at lowest levels since mid-Nov).

With limited fundamental data being released in the North American session, the market focus will be on the Bank of Canada's (BoC) monetary policy announcement (10:00 am EST).

Dealer consensus expects the central bank to leave its benchmark interest rate unchanged (+0.5%), with Gov. Poloz expected to keep his focus on downside risks even though signs point to a Canadian economy that “maybe” coming to life.

Note: Many still argue that Canada's economy is not as strong as the data would suggest, citing a recent setback in trade data and a household sector burdened with debt. Others argue that economic indicators, most notably job creation, point to an acceleration in growth.

1. Global equities produce mixed results

In Asia overnight, Japanese stocks fell to their lowest in more than four-months as rising geopolitical tensions in the region curbed risk appetite, with exporters badly hit as the safe-haven yen (¥109.35) spiked to a five-month high. The Nikkei 225 share average dropped -1.0%, while the broader Topix also fell -1%, led by declines in banks, autos and other exporters.

In Korea, the Kospi rose +0.2%, after dropping -2% over the previous six-sessions. Down-under, Australia's S&P/ASX 200 index gained less than +0.1%.

In Hong Kong, the Hang Seng China Enterprises Index climbed +0.3% and the Hang Seng Index jumped +0.6%, wiping out earlier intraday losses.

In China, the Shanghai Composite fell -0.5% as data showed China's producer price gains slowed in March from a peak in February, tempering the global inflation outlook (see below).

In Europe, equity indices are trading higher despite geopolitical tensions and the French Presidential election. Banking stocks are notably higher in the Eurostoxx, while mining stocks are trading lower in the FTSE 100.

U.S stocks are set to open in the black (+0.1%).

Indices: Stoxx50 +0.4% at 3,482, FTSE +0.4% at 7,396, DAX +0.4% at 12,183, CAC-40 +0.5% at 5,126, IBEX-35 +0.2% at 10,440, FTSE MIB +0.3% at 20,172, SMI +0.4% at 8,672, S&P 500 Futures +0.1%.

2. Oil higher on compliance, gold atop five month high

Oil prices have rallied overnight, putting crude futures on track for their longest winning streak in nine month, as Saudi Arabia is reported to be lobbying OPEC and non-OPEC members to extend last Nov. production cut beyond the H1, 2017.

Brent crude futures are up +20c, or +0.36% at +$56.43 per barrel, while U.S West Texas Intermediate (WTI) crude futures are up +18c, or +0.34%, at $53.58 a barrel.

While compliance from some participants has been patchy, the Saudi's have made significant cuts, with production down -4.5% since late 2016, despite a slight increase in March to +9.98m bpd.

The oil ‘bear' remains concerned that markets are bloated and oversupplied. Official U.S production and inventory data will be published later this morning (10:30 am EST).

Political tensions and expectations of a cautious Fed (gradual rate rise) continue to support gold prices. After printing a nine-month high yesterday, the yellow metal has fallen -0.1% to +$1,273.70 an ounce ahead of the U.S open.

3. Global yield curves flatter

Uncertainty surrounding the French presidential election on April 23 continues to drive investors to sell French government bonds (OAT's) and migrate cash into German government bonds and U.S Treasury debt. The yield on French 10's has backed up to +0.947%, while 10-year Bunds trade atop of their technically critical level of +0.2%.

Yesterday's U.S Treasury +$20B 10-year note reopening drew +2.332%. The bid-to-cover ratio was +2.48 vs. +2.66 prior. Indirect took +65.2% of competitive bids, with +26.4% were allotted at the high, while +5.3% go to direct bidders and +29.5% go to dealers.

The yield on U.S 10-year notes backed up +1 bps to +2.31%, erasing earlier declines. The rate dropped -7 bps on Tuesday.

Elsewhere, this morning Germany sold +€2.43B Feb. 2027 Bunds at an average yield of +0.21% vs. +0.41% on March 22. The bid-to-cover was +1.4 vs. +1.5.

4. Dollar pares losses, EUR contained, Yen jumps

With safe haven flows remaining the prevalent FX theme, overnight price action saw Yen (¥109.35) climb to its strongest level since mid-November before consolidating.

The pound (£1.2515) touched a one-week high ahead of this morning's U.K market data (see below). Thus far, GBP has been able to hold onto its gains as average wages (key focus of the BoE) beat expectations and saw higher back-month revisions.

Diminishing chances of a victory for far-right candidate Marine Le Pen in France's presidential election is helping the EUR (€1.0604). However, expect that growing support for leftist candidate Jean-Luc Melenchon keeps alive French political concerns and tempers the ‘single' unit's gains.

Note: Volumes across the various asset classes are down in a week that's shortened in many countries by Easter holidays.

5. China inflation soft, U.K wage growth slows

Data overnight showed China consumer inflation again remained “underwhelming” last month, as m/m CPI (-0.3% vs. -0.2%) fell for the second consecutive month in March and y/y was near its two-year lows below +1%.

Note: China's official CPI target for 2017 is +3%.

Digging deeper, the food CPI component fell again by over -4%, while non-food rose slightly by +2.3% vs. +2.2% prior. Also, rising input costs continue to prop up wholesale inflation, with PPI up for the seventh straight month at +7.6% – close to consensus.

In the U.K, average earnings after inflation in February for the first time in two and a half years, highlighting how rising prices fuelled by a weakened pound (£1.2500) are squeezing households' spending power.

Average weekly earnings growth after inflation and excluding bonuses declined -0.4% on the month. Over the three months through February, earnings growth averaged +0.1%.

Note: Annual U.K inflation is expected to exceed the BoE's +2% target as a fall in the pound since June's Brexit vote pushes up the cost of imports.

Pound Holds Against Major Currencies

- Pound holds against major currencies

- Bank of Canada expected to hold rates at 0.50%

Yesterday saw the Pound put in another day of modest gains across the board. GBP-EUR and GBP-USD both spent the morning hovering around 1.17 and 1.24 respectively. UK March Consumer Price Index results largely met expectations at 2.3% from forecast 2.2% and 0.4% month-on-month.

German ZEW Economic Sentiment then beat forecasts at 19.5 to keep Pound gains in check. The afternoon saw the Pound continue its gains on average of around 0.5% across all major currencies. There was no specific data to justify this; however, there does appear to be some shifting in the global risk environment which suggests that the Pound is responding well to global investor nerves.

Trump's stance on North Korea, Russia and Syria have stressed geopolitical tensions and created some risk aversion. Yesterday, President Trump said that the US is willing to go it alone against North Korea and the decision to move ships into the region could enrage the unpredictable Kim Jong Un into an action that sees things escalate quickly.

And with the Eurozone not being considered a safe-haven ahead of the French elections, the German stock market is in the red; maybe the UK is turning into a safer option. The Pound performed second strongest in the G10 only being outdone by the ultimate safe-haven, Japanese Yen.

Today we have UK Average Earnings, Claimant Count and UK Unemployment Rate data, just after a speech by Mark Carney at the International FinTech Conference in London.

In the afternoon, we have Canada's rate decision; expecting no changes here and to remain at 0.5%. The following press conference will be closely monitored for hints of a potential hike in the future.

English is hard

How can a clam cram in a clean cream can?

The thirty-three thieves thought that they thrilled the throne throughout Thursday.

Seth at Sainsbury's sells thick socks.

Roberta ran rings around the Roman ruins.

Technical Outlook: Oil May Extend Steep Ascend Above $54.00

US CRUDE OIL

US oil remains in strong uptrend and extends rally into fifth consecutive bullish day. Tuesday's close above Fibo 76.4% barrier at $53.13generated fresh bullish signal, as yesterday's long-tailed daily candle underpins fresh extension higher.

Rising geopolitical tensions keep oil price supported, along with weaker dollar. Fresh bullish extension on Wednesday is approaching target at $53.78 (07 Mar high) ahead of psychological $54.00 barrier and $54.41 (01 Mar high).

Firmly bullish daily studies that formed double bull-cross of 10/100 and 10/55 SMA's underpin the action and so far ignore strongly overbought daily slow stochastic, which continues to head north.

Session low at $53.33 and broken Fibo 76.4% barrier at $53.13 mark initial supports, ahead of yesterday's low and strong downside rejection at $52.68.

Res: 53.78, 54.00, 54.41, 55.01

Sup: 53.33, 53.13, 52.68, 52.30

Trump, Gold And Sterling In Focus

Ongoing geopolitical tensions across the globe and heightened political risk in Europe have limited appetite for riskier assets this week, with global stocks now on the back foot. Asian share concluded in the redon Wednesday, as the uncertainty from world events left investors on edge. Although European markets have displayed some resilience by opening higher this morning gains may be capped, especially if anxiety mounts ahead of the French Presidential elections. With the overall trading mood subdued and participants adopting a cautious stance in this tense environment, Wall Street could struggle to venture higher this week.

Sterling boosted by mixed jobs report

Sterling received a slight boost on Wednesday, with short bulls in action after the mixed jobs report showed that the UK’s unemployment rate remained steady at 4.7% in the three months to February. However, the upside was limited, as claimant count increased sharply by 25.5k in March while regular pay rose by a tepid 0.1% after accounting for inflation. With nominal earnings in the United Kingdom slowing to their weakest pace in seven months, consumer spending may be negatively impacted moving forward. A drop in consumer spending power could reignite concerns over the sustainability of the UK’s consumer-driven economic growth, which may in turn create further headaches for the Bank of England.

Focusing on the foreign exchange outlook, the GBPUSD has staged a sharp rebound, with prices breaking above 1.2500 on the back of Dollar weakness. The currency pair still remains in a wide range on the daily timeframe, with weakness back below 1.2450 opening a path towards 1.2370. In an alternative scenario, a decisive breakout above 1.2550 will signal an official breakout with bulls targeting 1.2650.

Trump in the spotlight again

The heightened geopolitical risks around Syria and North Korea have left markets tense this week andinvestors on high alert. Participants are in need of clarity on world events this week and as such, may encourage most to focus on Donald Trump’s aired interview on Fox Business Network. For those who remain somewhat optimistic over Trump's fiscal policies, the pending interview could provide further insight on the market-shaking tax reforms and infrastructure spending. With Syria and North Korea developments likely to be discussed, this could be labelled as a high-risk event that sparks volatility.

The combination of profit taking, geopolitical concerns and overall uncertainty has exposed the Greenback to downside risks this week. With short-term bulls still in control amid the expectations of higher US rates, the current Dollar decline could be treated as a technical correction. From a technical standpoint, the daily bullish outlook remains valid as long as the Dollar Index keeps above 100.25.

Commodity spotlight – Gold

The uncomfortable trading atmosphere created from geopolitical tensions andpolitical risk has boosted Gold’s attraction this week, with prices sprinting to five-week highs. This yellow metal is firmly bullish on the daily charts, and further upside may be expected as anxiety accelerates the flight to safety. From a technical standpoint, prices are trading above the daily 20 SMA, while the MACD has crossed to the upside. Previous resistance at $1260 could transform into a dynamic support that opens a path towards $1280 and potentially higher.

Market Update – European Session: Markets Try To Shrug Off Risk Aversion Sentiment

Notes/Observations

Simmering tensions on the Korean Peninsula and Syria fan demand for safer assets; gold at 5-month highs

UK average wages slightly exceeds expectations with back month revised higher

Overnight:

Asia:

China Mar CPI registered its 2nd straight decline (M/M: -0.3% v -0.2% prior Y/Y: 0.9% v 1.0%e

Trump administration said to be unlikely to label China as a currency manipulator in Treasury Dept foreign currency report out Saturday, Apr 15th

Europe:

Germany Fin Min Schaeuble: German 2017 GDP seen growing by ~1.5%; European authorities would turn to WTO over any trade violations (urges US to scrap plans for border-adjustment tax)

France govt to revise 2017 budget deficit target to 2.8% from 2.7% prior

Italy govt raised its 2017 GDP forecast to +1.1% y/y (up from +1.0% prior forecast)

Americas:

Fitch affirms United States sovereign rating at AAA; outlook Stable

Fed's Williams (moderate, non-voter): reiterates three to four rate increases are appropriate this year; Fed should start to shrink balance sheet by end of 2017

Economic Data

(DE) Germany Mar Wholesale Price Index M/M: 0.0% v 0.5% prior; Y/Y: 4.7% v 5.0% prior

(ES) Spain Mar Final CPI M/M: 0.0% v 0.0%e; Y/Y: 2.3% v 2.3%e

(ES) Bank of Spain (BOS): Mar Spanish Banks ECB borrowings at €149.4B v €145.0B prior

(UK) Mar Jobless Claims Change: +25.5K v -6.1K prior; Claimant Count Rate: 2.2% v 2.1% prior

(UK) Feb Average Weekly Earnings 3M/Y: 2.3% v 2.2%e; Weekly Earnings (Ex Bonus) 3M/Y: 2.2% v 2.1%e

(UK) Feb ILO Unemployment Rate 3M/3M: 4.7% v 4.7%e; Employment Change 3M/3M: K v +70Ke

Fixed Income Issuance:

(IN) India sold total INR140B in 3-month and 12-month Bills (INR80B and INR60B respectively)

(EU) ECB allotted $35M in 7-day USD Liquidity Tender at fixed 1.41% vs $45M prior

(SE) Sweden sold SEK10B vs. SEK10B indicated in 3-month bills; Avg Yield: -0.6714% v -0.6735% prior; bid-to-cover: 2.36x v 1.25x prior

(GR) Greece Debt Agency (PDMA) sold €812.5M vs. €625M indicated in 13-Week Bills; Avg Yield: 2.70% v 2.70% prior; Bid-to-cover: 1.3x v 1.3x prior

(IE) Ireland Debt Agency (NTMA) sold total €1.25B vs. €1.0-1.25B indicated range in IGB 2023 and 2026 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 10:00 GMT)

Indices [Stoxx50 +0.4% at 3,482, FTSE +0.4% at 7,396, DAX +0.4% at 12,183, CAC-40 +0.5% at 5,126, IBEX-35 +0.2% at 10,440, FTSE MIB +0.3% at 20,172, SMI +0.4% at 8,672, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes: European equity indices are trading higher as market participants digest ongoing concerns over geopolitical tensions, ahead of the French Presidential elections; Banking stocks trading generally higher across the board with shares of Deutsche Bank higher on large volume; shares of Daimler also notably higher in the Eurostoxx after they released prelim Q1 results overnight; commodity and mining stocks trading lower in the FTSE 100 as copper prices trade sharply lower intraday; shares of Tesco the notable laggard in the index after releasing their FY results, with shares of other large supermarket chains Morrison and Sainsbury lower in sympathy.

Upcoming scheduled US earnings (pre-market) include Delta Air Lines, Fastenal, ClubCorp Holdings, and Shaw Communications.

Equities (as of 09:50 GMT)

Consumer Discretionary: [Barry Callebaut BARN.CH -0.2% (H1 results), Dunelm DNLM.UK -2.2% (Q3 sales), Norcros NXR.UK +13.2% (trading update), PageGroup PAGE.UK +6.4% (Q1 gross profit), Puma PUM.DE +4.9% (prelim Q1 results), Telegraaf Media Groep TMG.NL +0.8% (Talpa confirms bid of €6.50/shr), Tesco TSCO.UK -3.4% (FY16/17 results)]

Consumer Staples: [Clas Ohlson CLASB.SE +1.7% (Mar sales)] - Energy: [Hunting HTG.UK +1.9% (trading update)]

Financials: [Countryside Properties CSP.UK +1.5% (trading update)]

Industrials: [Daimler DAI.DE +1.0% (prelim Q1 results), Kuehne & Nagel KNIN.CH +0.7% (MoU with BABA)]

Materials: [BHP Billiton BLT.UK -0.4% (Response to Elliott proposal)]

Speakers

German Economic Ministry Monthly Report: Domestic demand remained very robust; saw vigorous expansion in Q1. Euro area growth outlook was brighter

German Leading Economic Institutes (Advisors) spring economic forecasts raises 2017 GDP growth forecast from 1.4% to 1.5%and 2018 from 1.6% to 1.8%(as speculated). Saw German 1Q GDP growth of 0.6% and at 0.5% in Q2. ECB monetary policy could stimulate German economy more than assumed

Eurogroup chief Dijsselbloem: ECB's broad monetary policy could be phased out and did disadvantages to low interest rates

South Africa's Fin Min Gigaba: Treasury committed to fiscal consolidation; top priority is inclusive growth. Fully aware of impact of govt ability to borrow affordably. To undertake an international roadshow soon and meet with foreign investors

Turkey Dep PM Simsek: GDP growth would rise to 6% path following a 'yes' vote in upcoming Constitutional referendum. Easing of fiscal policy was temporary and expected rapid improvement in budget balances in H2

US Sec of State Tillerson stated from Moscow that lines of communication were always open; talks with Russian counterpart come at important moment in relationship

Russia Dep Foreign Min: Upcoming Lavrov/Tillerson meeting to discuss no-fly zone in Syria. US position on Syria remained a mystery to Moscow

China Foreign Ministry commented on potential US actions on Korea said to urge actions should be in accordance with International law. Escalating situation on Korean peninsula would be dangerous

S&P affirmed Singapore sovereign rating at AAA; outlook stable

OPEC secondary output production for March to be 31.928M bpd

Bund futures trade at 163.14 ticks down 7 ticks trading at the lower end of today's range in a relatively quiet morning ahead of the Easter break. Futures traded a high of 163.37, with a break back above targeting 163.57 then 163.99. A reversal continues to target 162.84 followed by 162.25.

Gilt futures trade at 128.44 down 5 ticks trading little changed after a mixed UK jobs report. Support moves to 127.94 then 127.34 followed by 127.05. A move above 128.67 targets 128.96. Short Sterling futures trade flat to up 1bp with Jun17Jun18 remaining at 10.5/11bp

Wednesday's liquidity report showed Tuesday's excess liquidity fell to €1.593T a fall of €27B from €1.620T prior. Use of the marginal lending facility rose to €265M from €185M prior.

Corporate issuance saw $5.4B come to market via 3 issuers comprised Yankee issues. Toyota 3 part $2.25B and JSC NC KazMunayGas $2.75B 3 part deal accounted for the bulk of the issuance as weekly issuance stands just shy of the $10B estimate.

Currencies

Safehaven flows remained the prevalent theme as geopolitical risks related to conflicts in Syria and saber-rattling by North Korea were not abating. Price action saw the JPY currency (Yen) climb to its strongest level since mid-November. USD/JPY tested 109.35 before consolidating. Spot gold hit a 5-month high just under the $1,280 level.

GBP/USD (Sterling) touched a 1-week high ahead of UK labour market data. The GBP was able to hold onto its gains as average wages (key focus of the BOE) did beat expectations and saw higher back-month revisions).

Looking Ahead

(IT) Italy Debt Agency (Tesoro) to sell €8.0-10B in 2020, 2024, 2030 and 2036 BTP Bonds

05:30 (DE) Germany to sell €3.0B in 0.25% Feb 2027 Bunds

05:30 (UK) DMO to sell £1.5B in 2.5% 2065 Gilts

05:30 (PT) Portugal Debt Agency (IGCP) to sell €1.0-1.25B in 2022 and 2025 OT bonds

06:00 (PT) Portugal Mar CPI M/M: No est v -0.2% prior; Y/Y: No est v 1.6% prior

06:00 (PT) Portugal Mar CPI EU Harmonized M/M: No est v -0.2% prior; Y/Y: 1.2%e v 1.6% prior

06:45 (US) Daily Libor Fixing

06:50 OPEC Monthly Report

07:00 (RU) Russia to sell OFZ bonds

07:00 (US) MBA Mortgage Applications w/e Apr 7th: No est v -1.6% prior

07:00 (ZA) South Africa Feb Retail Sales M/M: +0.2%e v -1.2% prior; Y/Y: -1.8%e v -2.3% prior

07:30 (CL) Chile Central Bank's Traders Survey

08:00 (IN) India Mar CPI Y/Y: 4.0%e v 3.7% prior

08:00 (IN) India Feb Industrial Production Y/Y: 1.3%e v 2.7% prior

08:00 (BR) Brazil Feb Retail Sales M/M: +0.3%e v -0.7% prior; Y/Y: -6.9%e v -7.0% prior

08:00 (BR) Brazil Feb Broad Retail Sales M/M: +1.7%e v -0.2% prior; Y/Y: -7.4%e v -4.8% prior

08:00 (PL) Poland Mar CPI Core M/M: 0.2%e v 0.1% prior; Y/Y: 0.5%e v 0.3% prior

08:00 (RO) Romania Central Bank (NBR) Apr Minutes - 08:00 (HU) Hungary Central Bank (NBH) Mar Minutes

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Mar Import Price Index M/M: -0.2%e v +0.2% prior; Y/Y: 4.0%e v 4.6% prior

08:30 (CA) Canada Mar Teranet/National Bank HPI M/M: No est v 1.0% prior; Y/Y: No est v 13.4% prior; House Price Index: No est v 202.25 prior

09:00 (EU) EU's Juncker speaks in Brussels

10:00 (CA) Bank of Canada (BOC) Interest Rate Decision: Expected to leave Interest Rates unchanged at 0.50%

10:00 (CA) Bank of Canada (BOC) April Monetary Policy Report

10:00 (MX) Mexico Central Bank (Banxico) Mar Minutes

10:00 (US) Fed's Kaplan (moderate, voter) speaks in Texas

10:30 (US) Weekly DOE Crude Oil Inventories

11:00 (IS) Iceland Mar International Reserves (ISK): No est v 811B prior

11:15 (CA) Bank of Canada (BoC) Gov Poloz holds post rate decision press conference

13:15 (DE) German Fin Min Schaeuble attends panel discussion in Berlin

13:00 (US) Treasury to sell 30-Year Bonds Reopening

14:00 (US) Mar Monthly Budget Statement: -$169.0Be v -$108.0B prior

(BR) Brazil Central Bank (BCB) Interest Rate Decision: Expected to cut Selic Target Rate by 100bps to 11.25%