Sample Category Title

Trade Idea Wrap-up: GBP/USD – Stand aside

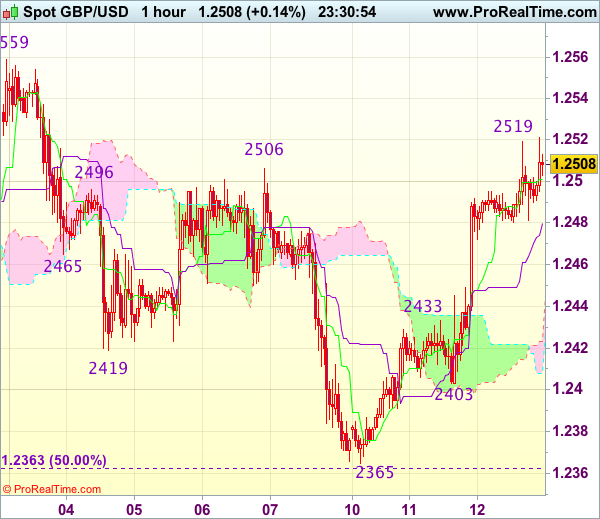

GBP/USD - 1.2509

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2501

Kijun-Sen level : 1.2480

Ichimoku cloud top : 1.2423

Ichimoku cloud bottom : 1.2408

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As cable has maintained a firm undertone after yesterday’s rally, suggesting low has been formed at 1.2365 on Monday and near term upside risk remains for the rebound from there to extend gain to 1.2525-30, however, break there is needed to add credence to this view and bring further rise towards resistance at 1.2559 but near term overbought condition should prevent sharp move beyond 1.2575-80 and price should falter below 1.2600, bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 1.2445-50 would suggest an intra-day top is possibly formed, bring weakness to 1.2420, break there would confirm and bring further fall to 1.12400-05 which is likely to hold on first testing.

Trade Idea Wrap-up: EUR/USD – Sell at 1.0665

EUR/USD - 1.0621

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.0611

Kijun-Sen level : 1.0613

Ichimoku cloud top : 1.0619

Ichimoku cloud bottom : 1.0598

Original strategy :

Sell at 1.0665, Target: 1.0565, Stop: 1.0700

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0665, Target: 1.0565, Stop: 1.0700

Position : -

Target : -

Stop : -

As the single currency recovered again after finding support at 1.0595 earlier today, retaining our view that further consolidation would be seen and initial upside risk remains for the rebound from 1.0570 low to extend gain to 1.0630, then 1.0650, however, reckon upside would be limited to 1.0667 resistance (Friday’s high) and bring another decline later, below said support at 1.0595 would bring retest of Monday’s low at 1.0570, break there would extend the decline from 1.0906 to 1.0550-55 (50% projection of 1.0906-1.0635 measuring from 1.0689), then 1.0525-30.

In view of this, would not chase this fall here and would be prudent to sell dollar on further recovery as 1.0667 resistance should limit upside. Only a firm break above said resistance at 1.0667 would abort and suggest low is formed instead, risk a stronger rebound to 1.0689, then 1.0702.

Trade Idea Wrap-up: USD/JPY – Sell at 110.30

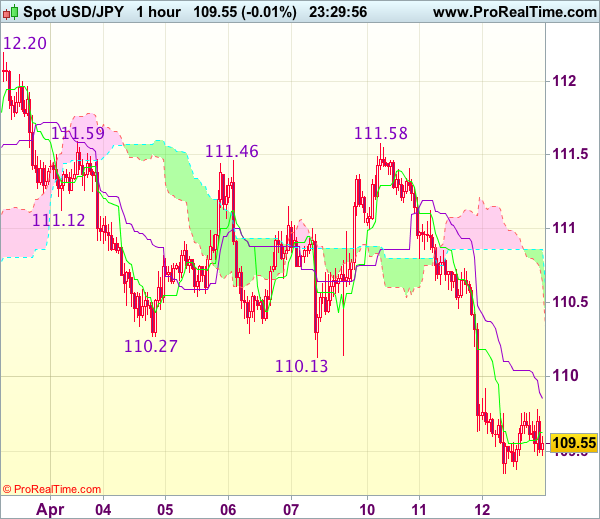

USD/JPY - 109.55

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 109.63

Kijun-Sen level : 109.86

Ichimoku cloud top : 110.86

Ichimoku cloud bottom : 110.64

Original strategy :

Sell at 110.30, Target: 109.30, Stop: 110.65

Position : -

Target : -

Stop : -

New strategy :

Sell at 110.30, Target: 109.30, Stop: 110.65

Position : -

Target : -

Stop : -

Yesterday’s selloff below support at 110.11 on active cross-buying in yen in part due to risk aversion suggests recent entire decline 118.66 top is still in progress, hence downside bias remains for recent decline to extend weakness to 109.30-35, then towards 109.00-05 (123.6 times projection of 112.20-110.13 measuring from 111.58), however, near term oversold condition should prevent sharp fall below 108.85 (61.8% projection of 115.51-110.11 measuring from 112.20) and reckon 108.40-50 (100% projection of 118.66-111.55 measuring from 115.51) would hold, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 110.30-40 should cap upside and bring another decline. Above 110.70-75 would defer and risk a stronger rebound to 111.00-05 but price should falter well below resistance at 111.58.

Geopolitical Tensions Boost Safe-Haven Japanese Yen

USD/JPY has steadied in the Wednesday session, as the pair trades at 109.70 in the North American session. In economic news, Japanese Core Machinery Orders bounced back with a gain of 1.5%, but this was well short of the forecast of 3.9%. On the inflation front, PPI improved to 1.4%, close to the forecast of 1.5%. In the US, there are no major events on the schedule. President Donald Trump will conduct an interview with the Fox Business Network, and will discuss health care, tax reform, and the crisis in Syria. On Thursday, the US releases three key indicators – PPI, unemployment claims and UoM Consumer Sentiment.

The yen has posted strong gains this week, as cautious investors have moved towards the safe-haven currency. USD/JPY has dropped 1.5 percent this week and is at its lowest level since November 2016. Escalating geopolitical concerns, particularly over Syria and North Korea, are weighing on the US dollar. The US bombed a Syrian military base last week, in response to a chemical attack by Syrian warplanes. Russia has strongly condemned the US move, chilling relations even further between the US and Russia. President Trump has also sent warships to the Korea peninsula, in a show of strength against North Korea, which continues to test ballistic missiles in defiance of the international community. If tensions escalate on either of these fronts, the yen rally could resume.

On Monday, Federal Reserve Chair Janet Yellen provided some insights into the Fed mindset. Yellen said that with the economy close to full employment and 2 percent inflation, Fed policymakers were looking to reduce the support that the central bank was providing the economy. The minutes of the March meeting indicated that the Fed plans to trim the $4.5 trillion balance sheet, which has ballooned as a result of the huge asset-purchase program which started in 2008. The Fed plans to raise rates twice more in 2o17, with the next rate expected in June. Yellen emphasized that the Fed's policy stance is neutral, as interest rate increases will be gradual, given that the economy is growing at a moderate pace.

Geopolitical Tensions Ease, Dollar Stabilizes after Disappointing Session Yesterday

Headlines

European equities trade little changed and mixed after a better opening. US equities open with small losses of about 0.15%.

The UK unemployment rate stabilised in the 3 months to February at 4.7%, the lowest level since 2005. Average weekly earnings rose by 2.3% Y/Y (vs 2.2% Y/Y expected). Employment growth was less than forecast though (+39k vs +70k) while jobless claims rose by 25.5k. Sterling hardly reacted to the mixed report.

Opec's oil output fell in March to sit below the level where the cartel estimates demand for its crude this year, as attempts to tighten the market were bolstered by supply disruptions in member countries. Brent crude rose further today, north of $56.5/barrel.

Christine Lagarde, the IMF's managing director, said that eurozone creditors must provide considerably more detail on debt relief for Greece before the fund will take a decision to join the country's bailout programme.

US Secretary of State Tillerson and Russian Foreign Minister Lavrov met in Moscow, amid a confrontation between the Trump administration and Russia over recent US strikes on Syria and the fate of Syrian President al-Assad. In remarks before a closed-door session, Mr. Lavrov appeared to warn Washington not to strike Syria again.

Chinese President Xi Jinping called for a peaceful resolution of rising tension on the Korean peninsula in a telephone conversation with US President Trump, as a US aircraft carrier strike group steamed towards the region.

Rates

Geopolitical tensions ease

Global core bonds traded in a narrow sideways range today amid an empty eco calendar. The geopolitical storm following hostile US comments against Syria and North Korea eased. Equity markets (lower) and oil prices sent a diffuse picture for core bonds. Markets seem to be gearing up for US retail sales and inflation data on Friday. In yield terms, both the German (0.2%) and US 10-yr yield (2.3%) hover close to/slightly below key support levels. At the time of writing, the changes on both the US and German yield curve range between -1 bp and +1 bp. On intra-EMU bond markets, 10-yr yield spread changes versus Germany narrow up to 4 bps with Greece outperforming (-7 bps).

The German Finanzagentur held a €3B 10-yr Bund auction (0.25% Feb2027). Total bids amounted to €3.45B, below the €4.89B average at the previous 4 Bund auctions. The Bundesbank retained €0.57B of the amount on offer for secondary market operations, resulting in an official bid cover of 1.4 (real bid cover 1.2). The auction had no tail and the yield nearly halved (0.21%) compared to last month's auction. The Italian Treasury launched a new 3-yr BTP (€4.5B 0.35% Jun2020) and tapped two on the run BTP's (€2.5B 1.85% May2024 & €2B 2.25% Sep2036) and one off the run BTP (€1B 3.5% Mar2030). The total amount sold was the maximum of the high €8-10B target with an auction bid cover (1.32)-in line with Italian average. The Irish debt agency sold the on the run 10-yr IGB (€0.7B 1% May2026) and off the run IGB (€0.55B 3.9% Mar2023) for a combined €1.25B, the higher end of the €1-1.25B target. With the completion of today's auction, the NTMA has issued €7.75B from its stated target range of €9-13B in the bond markets this year. The US Treasury concludes its refinancing tonight with a $12B 30-yr Bond auction. Currently, the WI trades around 2.93%..

Currencies

Dollar stabilizes after disappointing session yesterday

The dollar steadied today as geopolitical tensions moved to the background. There was no economic nor other key headline news that could give the main currency crosses firm direction. So EUR/USD and USD/JPY are currently very close to yesterday's closing levels.

After an uneventful Asian session, EUR/USD tried again to move higher from 1.0610, but the sluggish move ran already into resistance around 1.0625, after which euro selling occurred, pushing the pair to the 1.0605 opening level. It stayed around this level going into the close of our report. Both US and German yields are nearly flat on the day, implying that rate differentials barely changed. European equities eked out small gains, while US equity futures show marginal losses. We think that the upcoming Easter holiday keep investors side-lined. Combined with no strong movers, it leaves EUR/USD paralyzed close to 1.06. Investors are unwilling to reverse last week's dollar gains, but have no appetite either to test the key 1.05 level.

The yen gained substantial ground yesterday on a rise of geopolitical tensions. It pushed USD/JPY through the key 110 level. Risk sentiment turned neutral in the European session. USD/JPY set a new ST low at 1.0935 in Asian trading, but the yen returned its gains. However, also USD/JPY had no appetite to test the broken 110 level. USD/JPY set an intraday high at 1.0976, barely above the 109.62 close yesterday. In the US session, there is a slight negative trading bias, but the pair changes hands at 109.55 at the time of writing, virtually unchanged on the day.

Sterling holds on to yesterday's gains

Similar to our two main crosses, sterling trading was absolutely boring. Traders awaited the labour report, but it was mixed and thus neutral for sterling. As EUR/USD hovered lackluster throughout the session, sterling couldn't get direction from it. The market reacted for a second to the labour market report. Earnings were a tad higher than expected, but it were offset by weaker employment and higher than expected jobless claims. So the initial dip lower in EUR/GBP and the spike higher in cable were immediately undone. Cable traded between 1.2480 and 1.2510 and changes currently hands at 1.2493, virtually unchanged on the day. EUR/GBP trades currently at 0.8490, exactly yesterday's close.

Elliott Wave Analysis: AUDUSD Looking For More Downside

Aussie is not moving much for the last two days, but intraday wave structure and price action from last week suggests that we will see more weakness. The reason is a larger degree pattern which is impulsive to the downside, while hourly chart shows a triangle now in wave four. This is a continuation pattern so we are looking for a break to a new low of the week. Fib. levels shows that there is room for 0.7440.

AUDUSD, 1H

Bank of Canada Interest Rate Announcement: Still Waiting for Sunny Stephen

The Bank of Canada elected to hold its key monetary policy interest rate unchanged at 0.50% despite an upgraded near-term economic outlook.

Today's updated forecasts are for economic growth of 2.6% this year (January forecast: 2.1%). The outlook for 2018 was downgraded slightly, to 1.9% (from 2.1%). The Bank also provided its first forecast of 2019 GDP growth, which sees a 1.8% expansion. Consistent with the revised forecasts (and a downgraded estimate of potential growth), the Bank of Canada now expects the output gap to close in the first half of 2018, slightly earlier than previously thought.

Despite the revisions to the outlook, the statement accompanying the interest rate decision struck a somber tone. Canada is seen has having 'material slack', and while the positive tone in the recent data was acknowledged, the statement pointed to soft hours worked, uneven export growth, and the challenges related to business investment. Perhaps the clearest indication of the Bank's thinking was the statement that "it is too early to conclude that the economy is on a sustainable growth path"

On the inflation front, there were no significant changes in view, with weak core inflation highlighted, but headline inflation forecasted to trend near the 2% target through most of the projection.

The expected drivers of growth this year have been tweaked: housing is now expected to contribute positively to growth, while the government spending profile has been spread out somewhat, reflecting delays in infrastructure projects. Net trade has been upgraded, although seemingly at the expense of later years.

Four main risks to the inflation outlook were provided. Stronger U.S. growth remains a key upside risk for the Canadian economy, alongside stronger, but debt-fueled household spending (which itself creates a longer-term downside risk). Sluggish business investment and the possibility of stronger than estimated potential growth are seen as the main downside risks (to inflation).

Key Implications

The growth outlook may be sunnier, but it seems to be all about the negatives for Governor Poloz. The statement accompanying today's decision attempted to throw cold water on discussions of the recent improvement in Canadian economic indicators. Despite a generally improved forecast, Poloz remains focused on the soft spots in Canadian labour markets and exports, and is not yet ready to declare Canada 'out of the woods' when it comes to unevenness in economic growth.

For the moment, softness in wage and hours worked data, and the current pace of core inflation, appear to support Poloz's cautious approach. That said, there is no denying that the near-term growth outlook has improved, as acknowledged by the Bank of Canada's improved forecast and statement that the output gap will close by early 2018 (previously:"mid-2018"). As economic slack continues to be absorbed, inflationary pressures are likely to mount and make it increasingly difficult to maintain a dovish tone.

That is not to say that a hike is imminent, but rather that the calculus has begun to shift. The Bank of Canada clearly has no intention of following the Federal Reserve's path of interest rate increases (nor should they). Rather, the shifting balance of risks around inflation, particularly as we move into 2018 suggest the potential for a 'pulling forward' of the first rate hike.

Nonfuel Import Price Inflation Rising

Import prices declined 0.2 percent in March on lower prices for imported energy goods. Ex-fuel, however, prices are rising amid strengthening in the industrial sector and an improved capital spending environment.

Petroleum a Drag, but Core Import Prices Rise

Import prices slipped in March for the first time in four months as the recovery in oil prices took a step back. Prices for goods from overseas fell 0.2 percent.

Ex-petroleum prices rose 0.2 percent and are up 1.2 percent year over year. The recovery in nonfuel prices has been in large part driven by strengthening in the business sector as nonfuel industrial supplies and capital goods prices are rebounding.

Consumer Good Price Pressures Still Soft

Prices for imported consumer goods fell last month but, after upward revisions to January and February, suggest some modest easing in the rate of goods deflation in the core CPI.

Exporters have benefited from the improved global backdrop and more stable dollar, allowing further price increases. Export prices ex-food and fuel items rose 0.3 percent in March and, on a 12-month basis, are rising at the strongest pace since 2012.

Canadian Dollar Surges on Upbeat BoC Statement, China Xi Urges Peaceful Handling of North Korea

Canadian Dollar surges sharply on upbeat Bank of Canada statement. BoC left overnight rate target unchanged at 0.50% as widely expected. The central bank noted in the accompany statement that "recent data indicate that economic growth has been faster than was expected in the January MPR". Growth for 2017 through 2019 is expected to "remain above potential". Real GDP growth is projected to 2.5% in 2017, revised up from January projection of 2.1%. Inflation, however, is expected to dip in the months ahead but return to 2% target as the "output gap closes". And BoC concluded by noting that it "acknowledges the strength of recent data, some of which is temporary, and is mindful of the significant uncertainties weighing on the outlook."

China Xi urged Trump to deal with North Korea through peaceful means

It's reported that Chinese President Xi Jinping called US President Donald Trump just four days after the face-to-face summit in Florida. The People's Daily in China noted that Xi advocates resolving the problem in Korean peninsula through "peaceful means". And Xi expressed his willingness to "maintain communication and coordination with the US" on the issue. Xi also stressed that "China insists on realizing the goal of denuclearization of the peninsula." Separately, Chinese Foreign Ministry spokesperson Lu Kang said in a regular news conference that "It is irresponsible and even dangerous to take any actions that may escalate the tension" in Korean Peninsula. And, "all relevant parties should exercise restraint and keep calm, ease the tension instead of provoking each other and adding fuel to the fire."

Russian President Putin said relationship with US worsened under Trump administration

In Russia, President Vladimir Putin complained in a TV interview that level of trust with US has dropped after Trump became President of US. Putin said that "the working level of confidence in Russian-American relations, especially at the military level, under the administration of Donald Trump has not improved, but rather worsened." Putin, who backs Syrian President Bashar al-Assad, said earlier that the chemical weapon attack last week were "provocations" and for accusing the Syrian government. And Putin insisted there should be proper investigation by UN. He also criticized US's missile strike on Syrian air base as "a clear violation of international law". Russian Deputy Foreign Minister Sergei Ryabkov also said today that they have "absolute reliable information" that the chemical attack was done by terrorists.

UK PACAC concerned of foreign intervention in Brexit referendum

In UK, a report by a committee of lawmakers noted that a voter registration website could be attacked by foreign hackers during last year's Brexit referendum. The report was published by the parliament's Public Administration Constitutional Affairs Committee (PACAC). It said the committee did not rule out the possible cause of Distributed Denial of Service attack on the website that cause it to crash before deadline of the vote. And the report noted that "PACAC is deeply concerned about these allegations about foreign interference."

Also, it noted that "the US and UK understanding of 'cyber' is predominantly technical and computer-network based. For example, Russia and China use a cognitive approach based on understanding of mass psychology and of how to exploit individuals." And, "the implications of this different understanding of cyber-attack, as purely technical or as reaching beyond the digital to influence public opinion, for the interference in elections and referendums are clear."

Far-left Melenchon catching up in French presidential race

In France, far-right Marine Le Pen and centrist Emmanuel Macron continued to lead the race for presidential election. However, recent surge in support for far-left Jean-Luc Melenchon into top four trigger some rethink in the possible run-off scenarios. And some investors could be weighing the chance of Melenchon slipping into the run-off in May. A Pollsters Elabe poll showed that both Le Pen and Macron got 23% support, with conservative Francois Fillon at 19% and Melenchon at 17%.

Meanwhile, Elabe also tested a few additional scenarios for the run-off. The result showed that Macron would beat Le Pen, Fillon or Melenchon. Melenchon would beat Le Pen or Fillon but lose to Macron. Fillon would beat Le Pen but lose to the other two.

On the data front...

US import price dropped -0.5% mom in March. UK jobless claims rose 25.5k in March. Unemployment rate was unchanged at 4.7% in February while average weekly earnings rose 2.3% 3moy. Japan machine orders rose 1.5% mom in February. Domestic CGPI rose 1.4% yoy in March. China CPI rose 0.9% yoy in March, PPI rose 7.6% yoy. Australia Westpac consumer confidence dropped -0.7% in April.

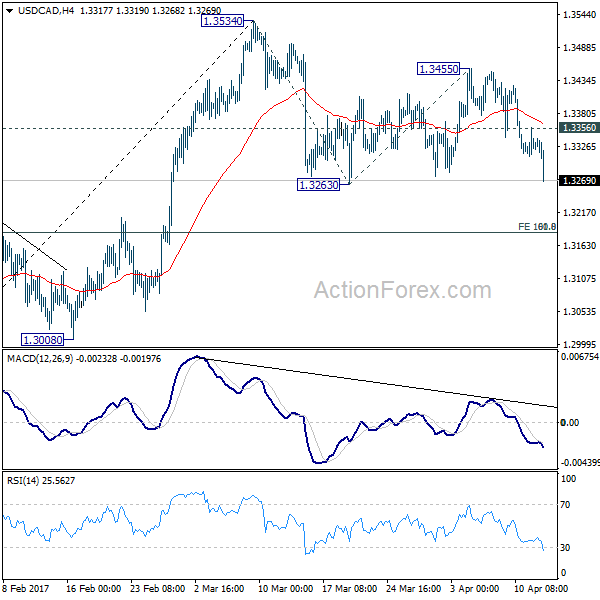

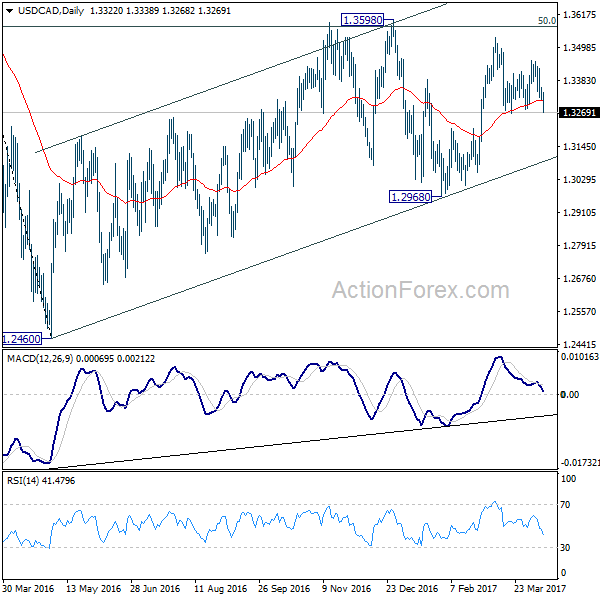

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3305; (P) 1.3331; (R1) 1.3353; More....

USD/CAD's fall accelerates in early US session and reaches as low as 1.3270 so far. Intraday bias remains on the downside for 1.3263 support. Break there will confirm resumption of whole decline from 1.3534 and target 1.3184 cluster level. (61.8% retracement of 1.2968 to 1.3534 at 1.3184, 100% projection of 1.3534 to 1.3263 from 1.3455 at 1.3814 too). As such decline is seen as a correction, we'd expect strong support from 1.3184 to contain downside and bring rebound. On the upside, above 1.3356 minor resistance will turn intraday bias neutral first. But for now, deeper decline is expected as long as 1.3455 resistance holds.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. However, break of 1.2968 will argue that the third leg has already started and should at least bring a retest of 1.2460 low. Meanwhile, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machine Orders M/M Feb | 1.50% | 3.70% | -3.20% | |

| 23:50 | JPY | Domestic CGPI Y/Y Mar | 1.40% | 1.40% | 1.00% | 1.10% |

| 00:30 | AUD | Westpac Consumer Confidence Apr | -0.70% | 0.10% | ||

| 01:30 | CNY | CPI Y/Y Mar | 0.90% | 1.00% | 0.80% | |

| 01:30 | CNY | PPI Y/Y Mar | 7.60% | 7.50% | 7.80% | |

| 08:30 | GBP | Jobless Claims Change Mar | 25.5k | -10.2K | -11.3k | |

| 08:30 | GBP | Claimant Count Rate Mar | 2.20% | 2.10% | ||

| 08:30 | GBP | ILO Unemployment Rate (3M) Feb | 4.70% | 4.70% | 4.70% | |

| 08:30 | GBP | Average Weekly Earnings 3M/Y Feb | 2.30% | 2.20% | 2.20% | 2.30% |

| 12:30 | USD | Import Price Index M/M Mar | -0.20% | -0.30% | 0.20% | 0.40% |

| 14:00 | CAD | BoC Rate Decision | 0.50% | 0.50% | 0.50% | |

| 14:30 | USD | Crude Oil Inventories | -2.2M | -0.7M | 1.M | |

| 18:00 | USD | Monthly Budget Statement Mar | -150.0B | -192.0B |

Trade Idea: EUR/GBP – Sell at 0.8590

EUR/GBP - 0.8485

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Sell at 0.8620, Target: 0.8520, Stop: 0.8660

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.8590, Target: 0.8460, Stop: 0.8630

Position : -

Target : -

Stop : -

The single currency has remained under pressure after recent selloff, suggesting recent decline from 0.8788 is still in progress and bearishness remains for further weakness to 0.8450, break there would add credence to our view that retracement of early upmove is unfolding for subsequent decline to 0.8420-25 but previous support at 0.8403 should hold from here.

In view of this, would not chase this fall here and would be prudent to sell euro on recovery as 0.8580-90 should limit upside. Above 0.8620-25 would abort and suggest low is formed instead, bring a stronger rebound to 0.8660-65 and possibly towards 0.8680 but price should falter below 0.8700.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.