Sample Category Title

BoC Leaves Key Interest Rate Unchanged At 0.50%

For the 24 hours to 23:00 GMT, the USD declined 0.62% against the CAD and closed at 1.3245.

Yesterday, the Bank of Canada (BoC) left the benchmark interest rate unchanged at 0.50%, as widely expected. Further, the BoC Governor, Stephen Poloz, stated that it is too early to conclude that the economy is on a “sustainable growth path” despite a recent rebound that led it to bump up its 2017 outlook.

However, the central bank disclosed that the nation's economic growth in recent quarters has been stronger than it forecasted in January, but also mentioned that it was “uneven expansion”.

In the Asian session, at GMT0300, the pair is trading at 1.3232, with the USD trading 0.1% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.3194, and a fall through could take it to the next support level of 1.3155. The pair is expected to find its first resistance at 1.3305, and a rise through could take it to the next resistance level of 1.3377.

Moving ahead, Canada's new housing price index for February, slated to release later today, will be closely watched by investors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD,AUDUSD, GBPCAD, GOLD, WTI CRUDE, DJIA, FTSE 100, DAX

EUR/USD

The EURUSD pair eventually broke above daily Ichimoku cloud and took out next strong barriers at 1.0622/66 (100 SMA / 55SMA), in late Wednesday's strong bullish acceleration, triggered by comments fron President Trump about too strong dollar that sent the greenback sharply lower across the board.

The Euro enjoyed fresh support and emerged out of two-day congestion, hitting recovery high at 1.0675 near the end of the US session. Strong bullish close on Wednesday would improve pair's near-term sentiment that was firmly bearish and signal stronger recovery.

Today's strong bullish close generated positive signal for fresh acceleration higher for attack at pivotal 1.0700 barrier (Fibonacci 61.8% of 1.0906/1.0570 descend), break of which would confirm reversal.

However, daily studies are still weak and may keep the downside vulnerable if the pair fails to clear 1.0700 pivot. Broken 100 SMA marks key near-term support at 1.0623, loss of which will be bearish.

German, French and Italian inflation data will key releases from the Eurozone on Thursday, with forecasts showing mainly unchanged values in March.

Support: 1.0650, 1.0630, 1.0623, 1.0614

Resistance: 1.0675, 1.0700, 1.0715, 1.0738

USD/JPY

USD JPY slumped in late US session after comments from President Trump about too strong dollar. The pair accelerated strongly lower after consolidating previous day's strong fall. Long bearish candle that was left on Tuesday, maintained strong bearish pressure, as yen remained supported by strong safe-haven buying amid growing geopolitical tensions.

The pair hit fresh nearly five-month low near 109.00 handle on Wednesday's fresh bearish acceleration, on track for the second consecutive strong bearish daily close.Firmly bearish daily technical studies favour further weakness, as fundamentals are already working against the greenback. The pair is eyeing next target at 108.48 (Fibonacci 100% expansion of current wave C from 115.50), to validate wave principles and signal further weakness.

Former strong support at 110.00 that stayed intact on Wednesday, remains as key near-term barrier which should ideallycap corrective upticks, seen on daily RSI / Slow Stochastic entering oversold territory.

Support: 109.00, 108.48, 107.80, 106.73

Resistance: 109.86, 110.10, 110.59, 110.90

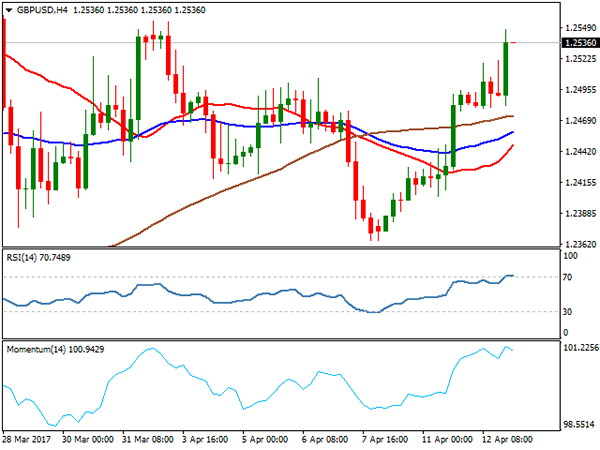

GBP/USD

Cable maintained strong bullish sentiment of past two days on Wednesday and extended strong rally through pivotal barriers at 1.2500/05. Fresh bullish acceleration on comments from US President Trump that the US currency is too strong, smashed the greenback and e fresh support to sterling that also took out next significant barrier at 1.2520 (Fibonacci 61.8% of 1.2615/1.2365 pullback. The pair needs close above the latter for bullish signal for recovery extension. Fresh bullish acceleration is approaching another pivot at 1.2556 (Apr 03 high / Fibonacci 76.4% retracement) break of which will open way towards key near-term barrier at 1.2615 (Mar 27 high).

Cable received support from mixed UK labour data, released earlier today. UK Jobless claims unexpectedly rose to 25.5K vs forecasted -3.0K, but Average earnings beat the forecasts coming at 2.3% in March, vs 2.2% forecast.

Support: 1.2520, 1.2480, 1.2460, 1.2427

Resistance: 1.2543, 1.2555, 1.2613, 1.2631

AUDUSD

The Aussie dollar hasn't changed significantly on Wednesday, remaining within tight consolidation range that is capped by sideways-moving 100SMA at 0.7514 that marks solid barrier and so far prevents stronger corrective action after broader downtrend from 0.7747 found support at 0.7473.

Initial signal of stronger recovery comes from daily slow stochastic that reversed from oversold territory, but initial requirement is firm break above 100SMA. Such scenario could anticipate fresh recovery and expose next pivotal barrier at 0.7550 (200SMA), break of which would confirm reversal and open way for stronger correction of 0.7747/0.7473 downleg.

Otherwise, prolonged consolidation would be likely near-term scenario, with risk shifted lower, as daily studies remain bearishly aligned.

Australian jobs data on Thursday are in focus, with strong forecast for new jobs at 20.0K in Mar, compared to -6.4K in Feb, while Unemployment rate is expected to stay unchanged at 5.9% in March.

Support: 0.7500, 0.7473, 0.7449, 0.7400

Resistance: 0.7514, 0.7550, 0.7576, 0.7611

GBPCAD

The GBPCAD cross showed no significant action on Wednesday and ended trading in Doji that signals indecision after strong rally on Tuesday. Recovery rally from 1.6515 low is struggling to clear 1.6657 barrier (50% of 1.6800/1.6515 downleg, following repeated false break above that was capped just under strong barrier at 1.6692 (200SMA).

Near-term price action is stuck between 100 and 200SMA's and without clear direction.The notion is supported by mixed setup of daily MA's and contradicting daily indicators. MACD is holding in the positive territory, while Momentum studies are negative and daily RSI is holding in neutrality zone.

Break of either congestion boundary, 200SMA at 1.6692 or 100SMA at 1.6493 is needed for firmer direction signal.

Break lower will complete daily Failure Swing pattern for deeper fall, while lift above 200SMA would signal false break below pivotal 1.6535 support (low of Mar 30) and open way for fresh recovery towards key barrier at 1.6800.

Support: 1.6571, 1.6535, 1.6515, 1.6493

Resistance: 1.6680, 1.6692, 1.6736, 1.6800

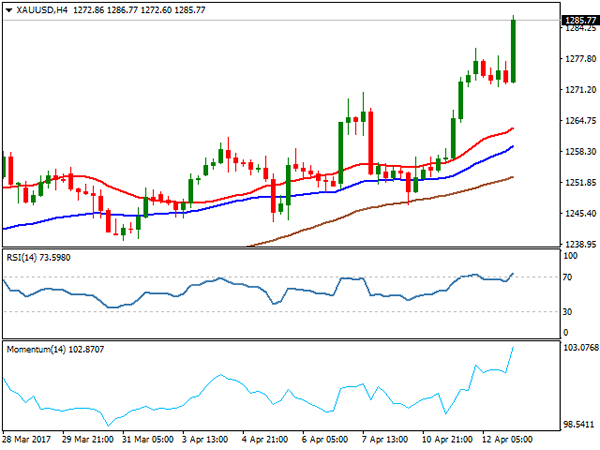

GOLD

Spot Gold surged in late US session extending strong rally for the second day after US dollar slumped on comments from US President Donald Trump, who said that the US currency is getting too strong while geopolitical concerns continue to weigh on sentiment.

The yellow metal hit fresh five-month high at $1283, approaching its next target at $1286 (Fibonacci 76.4$ of $1337/$1122 descend. Gold is driven by rising geopolitical concerns that prompted investors to move from riskier assets into safe-haven gold.After Strong rally on Tuesday left long bullish daily candle that underpinned bullish action, gold price continued to rise and accelerated on the latest comments from President Trump. Strong bullish sentiment was boosted by fresh dollar's weakness and could drive gold price through $1286 barrier towards targets at $1292 and psychological $1300 barrier in extension.

Firmly bullish technical studies remain supportive, however, overbought conditions on daily chart may pause rallies for consolidation.

Former tops at $1270/60 are expected to keep the downside protected.

Support: 1272, 1270, 1263, 1257

Resistance, 1283, 1286, 1292, 1300

WTI CRUDE OIL

WTI oil ended trading in red on Wednesday for the first time after four straight days of gains that hit fresh five-week high at $53.74 per barrel. The oil price eased below $53.00 in late US session, extending pullback despite unexpected fall in US crude inventories. Energy Information Administration released its weekly report, showing fall of crude stocks by 2.2 million barrels in the week ended on Apr 7, compared to forecast for 87.000 barrels build.

Crude oil remains supported by rising tensions in Middle East and North Korea, also being supported by oil producers' decision to extend output reduction for another six months and eyes key short-term barriers at $55.00 zone. Current easing is likely driven by technicals, as studies are overbought, as well as on profit-taking after four-day rally, near the end of holiday-shortened week.

Tuesday's low, left after strong downside rejection at $52.68, marks initial support that stays intact for now, guarding hourly Ichimoku cloud base at $52.41 and broken Fibo 61.8% barrier at 51.97 which also act as significant supports.

Extended dips should find solid supports at $51.65/61 (converged 55/100 SMA), which are expected to contain and keep overall bullish structure intact.

Support: 52.79, 52.68, 51.97, 51.65

Resistance: 53.26, 53.74, 54.50, 55.00

DJIA

U.S. stocks ended lower on Wednesday as investors moved in safe-haven assets amid lingering geopolitical worries, but keeping the upcoming earnings season in sight. Investors remain concerned about the situation over Syria after US military attacked Syrian army base, with growing threats of escalation of conflict and further confrontation with Russia. Traders worry that these developments could distract president Trump from following his campaign promises in pro-business policies, such as tax cuts and higher infrastructure spending that drove Wall Street to its record highs since Trump's election.

Dow Jones ended Wednesday's trading in red and moved deeper into daily Ichimoku cloud, generating bearish signals after triple-Doji that signalled strong indecision during past few sessions.

Daily Tenkan-sen/Kijun-sen lines are in bearish setup and daily indicators entering negative territory, generating negative signal for attack at initial target at 20450 zone and extension towards key support at 20385 (daily Ichimoku cloud base, break of which could trigger further retracement of Jan/Mar 19713/21160 ascend.

Support: 20490,20450, 20385, 20266

Resistance: 20607, 20637, 20682, 20692

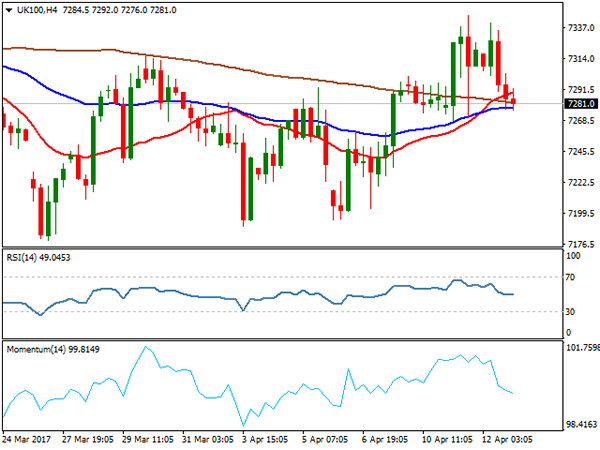

FTSE 100

FTSE index ended in red on Wednesday, after repeated rejection at key 7343 resistance (Fibonacci 61.8% of pullback from record high at 7444 to 7179 (Mar 27 low). Subsequent easing returned below broken Kijun-sen line (7311) and softened near-term structure, as hourly indicators moved into negative territory. Weakness from 7343 managed to find footstep at daily 20SMA 7285 that guards lower trigger at 7268 (daily Tenkan-sen), break below which would further weaken near-term picture and risk return to key near-term support at 7240 (top of rising daily Ichimoku cloud.

Daily technical indicators are holding in neutral zone and lacking clearer signals for now, however, bullish bias would remain in play while the price holds above rising daily cloud.

UK stocks ended lower on Wednesday after gains from financial and industrial sector were offset by losses in Tesco shares that dropped 4.6% on Wednesday, making blue-chip FTSE 100 index to close the day 0.45% down.

Support: 7268, 7240, 7222, 7195

Resistance: 7311, 7343, 7381, 7400

DAX

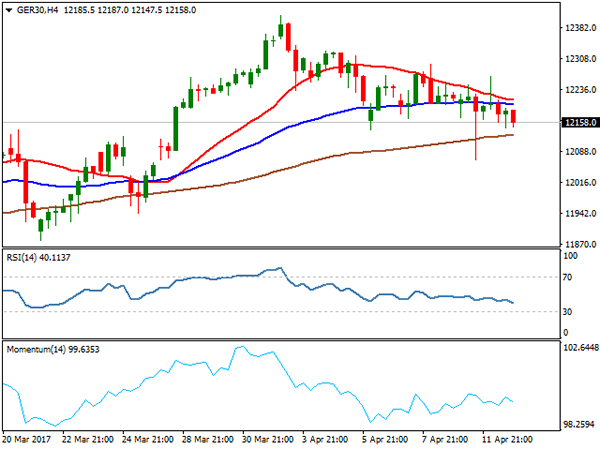

DAX ticked slightly above Tuesday's high today, but remained in red at the end of the day and stayed directionless for the second consecutive day. The price held between daily Tenkan-sen and Kijun-sen line (12240/12141 respectively, after repeated attack at key support at 12141, also Apr 06 low. Mixed signals from daily technical studies are lacking clearer direction signals, after Tuesday's long-legged daily Doji candle.The top performers of DAX index on Wednesday were Henkel (up 1.32%), Adidas (up 0.94%) and BMW which ended session up 0.90%.

On the other side, the worst performers were Thyssenkrupp (down 1.89%), Deutsche Boerse (down 1.08%) and Heidelbergcement (down 1.03%).

Rising stocks were 412 while 306 declined and 25 remained unchanged, with overall result keeping the index without stronger moves on Wednesday.

Rising daily 20SMA contained today's dips and continues to underpin, with key support at 12144, clear break of which would generate stronger bearish signal.

The upper pivot is at 12240 (Tenkan-sen) with lift above 12300 zone (Apr 10 high) needed to trigger stronger recovery.

Support: 12141, 12069, 12000, 11943

Resistance: 12199, 12240, 12267, 12296

Elliott Wave View: Gold Ending Impulse

Short term Elliott Wave view in Gold (XAUUSD) suggests that cycle from 4/10 low (1246.92) is unfolding as an impulse Elliott wave structure where Minutte wave ((i)) ended at 1257.2, Minutte wave (ii) ended at 1250.8, Minute wave (iii) ended at 1279.75, Minute wave (iv) ended at 1271.69 and Minute wave (v) of (a) is in progress towards 1291.99 – 1296.84 area before cycle from 4/10 ends and the yellow metal see a correction in Minutte wave (b). We don’t like selling the proposed pullback and expect buyers to appear again once Minutte wave (b) is over in 3, 7, or 11 swings provided that pivot at 4/10 low (1246.92) remains intact.

Gold 1 hour Elliott Wave Chart

Market Morning Briefing: The US President Sees The Dollar As Too Strong And China Is No Longer A Currency...

STOCKS

Fresh 4-month lows seen in Nikkei, while Shanghai could see a short dip in the coming sessions. Dow may remain sideways while Dax looks bullish.

Dow (20591.86, -0.29%) came down slightly yesterday. 20500-20410 region is an important near term support zone. Some sideways consolidation is expected in the broad 20780-20410 region for the coming sessions.

Dax (12154.70, +0.13%) is holding above the 12049 support and could move higher towards 12400 in the coming sessions before seeing a sharp corrective fall.

Shanghai (3272.94, -0.03%) is trading along the upper end of the daily channel resistance. A fall towards 3250 is expected in the next few sessions.

Nikkei (18342.22, -1.13%) has been coming down in line with our expectations. A fall towards 18200-18000 is on the cards for the near term. This could also pull down Dollar-Yen in the coming sessions.

Nifty (9203.45, -0.36%) tested 9162 yesterday before losing above 9200. As mentioned yesterday the 9120/30 level is an important support and while that holds, near term looks bullish.

COMMODITIES

Our interim target of 1290-1301 is almost achieved with an intraday high of 1289 in Gold so far. A correction towards 1260-65 can be expected due to near-term overbought condition. We have been expecting 1260 for gold to hold as buyers are taking every dip as a further opportunity for buying. 1301 could be a level where the price action has to be checked to assess the chances of further bounce to 1328 to 1350 levels.

Silver (18.53) is hovering around its crucial resistance of 18.50-55 levels. Immediate trading range could be 18.30-19 but a close below 18.30 could open up 17.70 as well. We need to wait for confirmation for immediate directional clarity.

Copper (2.55) has been stuck in the range of 2.55-2.70, which may go on for some time. In the medium term 2.55-57 are going to be a strong support now but a close below that could open up 2.50 and 2.45 levels respectively. Gradual buying at 2.55 levels can’t be ruled out due to near term oversold condition.

Brent (55.83) and WTI (53.08) are trading within the range of 55-57 and 51.70-54.80 respectively. A decrease (-2.2M B) in U.S. weekly crude oil inventory could opened up higher levels of 57 for Brent and 54 for WTI. The trend is bullish in the near term time frame and any corrective fall due to overbought condition may add fresh longs at the lower levels.

FOREX

The US President sees the Dollar as too strong and China is no longer a currency manipulator, a 180 degree turnaround from the elections rhetoric heard just a few months back. These comments have triggered a massive selling in Dollar and have strengthened all the majors against Dollar across the board.

The grinding decline in Dollar Index (100.04) gathered downside momentum after Trump comments of Dollar being too strong. To keep the chances of any recovery open, the immediate support of 99.80 must hold and a rise above 100.40 has to materialize. Otherwise, the decline may extend to 99.00, a very important support.

Contrary to expectations, Euro (1.0674) bounced strongly instead of retesting the support of 1.0550. If it manages to rally above the resistance of 1.0700, then further rise to 1.0780 levels can be seen in the next few days.

Dollar Yen (108.83) keeps falling in line with expectations and now it is approaching the long term support area of 108.40-25 which may hold and trigger a bounce. In case, the support of 108.40-25 fails to hold, lower supports of 107.85-50 may be tested.

Pound (1.2563) has rallied strongly like the other majors on the back of Dollar weakness but the major resistance 1.2600 is expected to hold and keep it in the broader range of 1.2350-1.2600.

Aussie (0.7576), contrary to expectations, has bounced back in a very sharp manner as the Feb’17 employment data beat the expectations by a huge margin. If it sustains above the resistance at the current levels, may rise higher to 0.7640-75.

Dollar-Rupee (64.68) is trading at 64.52 in the NDF this morning. Despite repeated attempts yesterday, it failed to close above the resistance of 64.70 which increased the chances of sideways consolidation in 64.20-70 for the rest of the week as expected. As discussed previously, a breakout of this near term range might take place next week.

INTEREST RATES

The US yields have broken below the immediate support levels and are oversold at current levels. We may expect a bounce back in the next couple of sessions. The 10yr (2.23%) may be expected to recover from levels near 2.20%.

The US-Japan 10Yr (2.22%) has broken below the horizontal support levels after a initiation of a bearish signal in Nikkei. Together the yield spread and Nikkei looks bearish for the near term and could push down Dollar-Yen to lower levels. (Refer to currencies section)

The German-US 2Yr (-2.05%) and 10Yr (-2.03%) continues to move up and could test immediate resistance levels near -2% on both the yield spreads. A rejection is expected from -2% which could again bring in some weakness in the Euro.

The UK-US 10YR (-1.19%) is headed towards -1.13% in the near term from where a fall is expected. Pound could witness some sideways consolidation in the coming sessions followed by another down leg.

BOC Upgraded Growth Outlook, Remains Cautious Over Trade Relations With US

BOC appeared more confident over the economic growth outlook, although it maintained the policy rate unchanged at 0.5% in April. Policymakers upgraded the GDP growth forecast for this year amidst strong housing market activities in the first quarter, but revised lower the figure for 2018. It also revised mildly higher the inflation outlook, though. The central bank cautioned over the uncertainty of trade relations with the US and stressed that material slack remained in Canada. On the monetary policy, Governor Stephen Poloz described the stance as 'decidedly neutral' as the members weighed the improved economic developments against the uncertain trade policy. We expect the policy rate to stay unchanged at 0.5% for the rest of the year. The loonie strengthened around than +0.5% Wednesday as Canadian economic outlook improved. Yet, the magnitude of the gain was mainly due to USD's weakness as US President Donald Trump complained that the greenback is too strong and reiterated his preference of low interest rate policy.

The post-meeting statement noted that global economic growth is 'strengthening and becoming more broadly-based than' the projections made in January. Domestically, incoming macroeconomic data suggested that 'economic growth has been faster than was expected in January' with growth 'temporarily boosted by a resumption of spending in the oil and gas sector and the effects of the Canada Child Benefit on consumer spending'. BOC now forecasts Canada's GDP to expand +2.6% this year, up from +2.1% in January's projection, before decelerating to +1.9% in 2018 (January: +2.1%) and +1.8% in 2019. BOE now expects the output gap to close in 1Q18. Meanwhile, BOC has revised down the 'projection of potential growth, reflecting persistently weak investment'. BOC remained cautious, suggesting that 'it is too early to conclude that the economy is on a sustainable growth path'..

Inflation has been hovering around the +2% target. BOC judged it was largely driven by 'the transitory effects of higher oil prices and carbon pricing measures in two provinces, as well as other temporary factors'. It acknowledged that its three measures of core inflation have been 'drifting down in recent quarters and wage growth remains subdued, consistent with material excess capacity in the economy'. The central bank revised the inflation forecast a tick higher to +1.9% and +2% in 2017 and 2018, respectively. Inflation would then further improve to +2.1% in 2019.

In the concluding paragraph, BOC noted that despite 'the strength of recent data, some of which is temporary, and is mindful of the significant uncertainties weighing on the outlook'. We expect the policy rte would stay unchanged at 0.5% for the remainder of the year.

Trump Confirms Dollar Breakdown

The range breaks in USD/JPY and 10-year Treasuries were tenuous on Wednesday until late in the day when Trump jawboned the dollar lower. The euro was the top performer on the day while USD lagged. The Australian jobs report is next. Range breaks can break your heart. Well defined ranges in USD/JPY and 10-year yields gave way on Tuesday in a strong move but the lack of fear in stocks and the lack of a compelling new catalyst was a concern. On Wednesday, the lack of follow and a quiet market through added to the worries about a false break. Both gold and silver longs in our Premium service have deepened in the green at +77 and 110 pts respectively.

That changed late in the day as the dollar and yields sank after Donald Trump jawboned the currency lower. The initial headline reported him saying the dollar was getting too strong but buried in the WSJ interview was a comment that may have more long-lasting implications than some minor jawboning. He said that he likes low interest rate policy.

Trump will soon fill one of the Fed governor roles. He has two more vacancies to fill after that and could also replace Yellen. But in perhaps another sign that he's a dove, he reversed campaign comments that she was 'toast' and said he was thinking about extending her but undecided.

His comments were part of handful of policy reversals. He also confirmed suspicions that he won't name China a currency manipulator, that he won't close the Import-Export Bank, that NATO isn't obsolete along with his seeming reversal on taking action in Syria.

The market latched onto the dollar comments and EUR/USD climbed to 1.0670 from 1.0600. Technically, the bigger story was USD/JPY as it broke through 110.00 on Tuesday then spent most of Wednesday consolidating just below before Trump's comments sent it to 108.90. There is huge downside potential in that trade if it can break the 200-dma at 1.0875.

Looking ahead, the Australian dollar will shift into focus in Asia-Pac trading with the jobs report due at 0130 GMT. The consensus is 20.0K new jobs. AUD/USD touched the lowest since mid-January in early trading but reversed in an outside day to 0.7530. A strong jobs number would help confirm the turn.

USDCAD Hawkish Bank of Canada Boosts Loonie As Trump Talks Down Dollar

The Canadian dollar rose against the US dollar after the Bank of Canada (BoC) published its monetary policy statement keeping interest rates unchanged at 0.5 percent but Governor Stephen Poloz offered a hawkish rhetoric by saying that a rate cut is no longer on the table. He later balanced the view by commenting that the stance of the central bank is neutral. Economic indicators have been strong in Canada with employment reports adding two back to back gains of 15,000 or more jobs. Inflation and retail sales have been steady and the economy are at 0.6 percent month over month in March.

The loonie also got a boost from US President Donald Trump after he once again made comments on the greenback being “too strong” which prompted the currency to depreciate across the board. It is unusual for a head of state to issue those types of comments, which are usually made by the Secretary of Treasury. Donald also made a strange comment regarding Fed Chair Janet Yellen saying she is “not toast” implying he is open to extending her term at the head of the central bank adding that he likes and respects her, but is very early.

Oil fell after data from oil inventories was mixed with a larger drawdown than expected in crude inventories but an increase in operating capacity at refineries. The Organization of the Petroleum Exporting Countries (OPEC) production cut has been effective in keeping prices around the $50 range, but higher production in the US and Canada that are not part of the agreement continues to put downward pressure on prices. The OPEC is yet to announce clear plans on an extension to the agreement, but has said that compliance from members is above 100%.

The USD/CAD lost 0.083 percent in the last 24 hours. The pair is trading at 1.3321 after the Bank of Canada kept the benchmark interest rate unchanged on Wednesday. The move was expected by the market as the central bank has kept to the sidelines last year and the first quarter of 2017 after a proactive 2015 that saw two rate cuts ahead of the free fall of oil prices. In a tough balancing act Governor Poloz delivered a hawkish message by taking off the table a rate cut that was at times almost a given as the Canadian economy struggled last year. Negative rates were whispered if the stimulus from the government were to prove insufficient.

Poloz tried to remain neutral adding some pessimism with comments around the underperformance of exports and investment. Geopolitical risk specially with regards to the United States was mentioned by the central bank Governor as risks to the Canadian economy going forward as divergence between the two economies could continue as the US is near full employment.

Later in the day Stephen Poloz made more comments on the state of Canadian housing after he has said there are clear signs of speculation driving prices higher, but is still unconvinced higher interest rates are the answer.

Oil lost 0.675 percent on Wednesday. West Texas is trading at $52.69 after data from the Energy Information Administration (EIA) released today pointed to supply still outstripping demand for energy. While inventories were down, a drawdown of 2.2 million barrels, US production is climbing rapidly to take advantage of current prices made possible by the OPEC agreement.

US refineries are coming out of maintenance mode and it showed with the largest drawdown this year showcasing the two side of the oil showdown. The OPEC, Russia and other big producers have joined in a historic production cut but on the other side those that are not taking part in the deal have ramped up production. US and Canadian shale operations have thrived ahead of the American driving season will see further demand being met domestically.

Market events to watch this week:

Thursday, April 13

8:30am CAD Manufacturing Sales m/m

8:30am USD PPI m/m

8:30am USD Unemployment Claims

10:00am USD Prelim UoM Consumer Sentiment

Friday, April 14

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Trump Says Dollar Getting Too Strong, USDX Drops Hard

In an interview with the Wall Street Journal, US president Donald Trump overnight made it clear that in his eyes, the USD is too strong.

'I think our dollar is getting too strong, and partially that's my fault because people have confidence in me. But that's hurting—that will hurt ultimately.'

So what did that do to price? Let's take a look at the USDX daily:

USDX Daily:

Yuck… Yes, that's goodbye to USD bulls! The bears are back.

I read some commentary claiming that comments like this were unusual for a leader to make about their country's currency, but for me it's just the US entering back into the race to the bottom. Nobody wants to hurt their exporters and as such everyone tries to outdo each other to negatively effect their currency.

Things aren't going to change anytime soon and this was just in response to the fact that the USDX is up over 2% since Donald Trump was elected as President of the United States.

From a trading point of view, I don't think Trump had his MT4 charts open and noticed the trend line support that EUR/USD was sitting on (heck who knows, maybe he did!), but this jawboning just gave that little extra for price to kick on:

EUR/USD Daily:

If you found a long entry off the higher time frame support level that we highlighted on Monday then you're sitting pretty right now. If not then it's now all about waiting to see what sort of pullback we get and why it comes because this is pretty good confirmation of the level holding and the market staying a buy.

Bank of Canada Assumes a “Decidedly Neutral” Policy Stance

Highlights:

- Material slack exists although the estimate of the output gap was 0.75% at the end of the first quarter, markedly below January's 1.25% estimate for the end of 2016

- The economy's potential growth rate has been lowered to account for weak investment though is expected to gradually recover from 2017's 1.3% estimate

- Underlying inflation and wages remain subdued and the headline rate is projected to hold around the 2% target over forecast horizon

- Economic growth has been stronger than anticipated but the composition uneven. More moderate gains are expected and the drivers of growth will transition and be more broadly based going forward. The key driver of the 2017 forecast upgrade was robust housing market activity in Q1.

- Given the uncertain outlook about shifts in trade policy, the Bank's projections incorporate "at least some of the adverse impact of elevated uncertainty" including a 0.2 ppt cut to export growth and a 0.5 ppt hit to investment in both 2017 and 2018.

The Bank incorporated the string of recent strong reports into its near term forecast however remains reluctant to extrapolate this strengthening. Rather the report highlights that temporary factors underpinned the uptick and concludes that it's "too early" to say the economy will stay on this firmer growth trajectory. That said, the Bank pulled forward the absorption of current slack in the economy to the first half of next year. Today's update shows growth running above potential in 2018 and 2019, implying the economy will shift into excess demand. However given the risk that external uncertainties and the attendant downward impact on growth will play out, there is little focus on this. Should these pressures fail to materialize, however, the current outlook implies policy will need to tighten.

Today's report aimed to balance the recent strengthening in growth and potential headwinds associated with shifting trade policies leading the Governor to characterize the Bank's stance as "decidedly neutral." As a result, we continue to expect the overnight rate will remain at 0.5% in 2017.

Our Take:

Markets were prepared for the Bank to leave the overnight rate at 0.5% today however they were less certain about how they would characterize the outlook. Ever cautious, policymakers highlighted risks to the outlook and the persistence of economic slack although now expect output gap will close sooner than they did in January. The Bank incorporated the string of recent strong reports into its near term forecast however remains reluctant to extrapolate this strengthening. Rather the report highlights that temporary factors underpinned the uptick and concludes that it's "too early" to say the economy will stay on this firmer growth trajectory.

The report aimed to balance the recent strengthening in growth and potential headwinds associated with shifting trade policies leading the Governor to characterize the Bank's stance as "decidedly neutral." As a result, we continue to expect the overnight rate will remain at 0.5% in 2017.

Trade Idea Wrap-up: USD/CHF – Buy at 1.0000

USD/CHF - 1.0052

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0061

Kijun-Sen level : 1.0065

Ichimoku cloud top : 1.0080

Ichimoku cloud bottom : 1.0067

Original strategy :

Buy at 1.0000, Target: 1.0100, Stop: 0.9965

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0000, Target: 1.0100, Stop: 0.9965

Position : -

Target : -

Stop : -

Dollar has slipped again in NY morning, adding credence to our view that temporary top has been formed at 1.0108 on Monday and consolidation below this level would be seen and initial downside bias is for pullback towards support at 1.0026, however, reckon 0.9995 support would contain weakness and bring another rise later, above 1.0085-90 would bring test of indicated resistance at 1.0108-09 but break there is needed to extend recent upmove from 0.9813 towards 1.0140-45 but loss of upward momentum should prevent sharp move beyond another previous resistance at 1.0171.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as support at 0.9995 should limit downside. Below 0.9970 (50% Fibonacci retracement of 0.9831-1.0108) would abort and signal top is formed instead, bring correction to support at 0.9948.