Sample Category Title

Canada’s Housing Starts Jumped To Its Highest Level Since September 2007 In March

For the 24 hours to 23:00 GMT, the USD declined 0.71% against the CAD and closed at 1.3322.

The Canadian Dollar gained ground, after Canada's housing starts climbed more-than-anticipated to a level of 253.7K March, notching its highest level in nearly a decade, suggesting that housing market will remain one of the bright spots in the nation's economy. Housing starts had recorded a revised level of

214.3K in the preceding month, while market participants anticipated for a rise to a level of 214.5K.

In the Asian session, at GMT0300, the pair is trading at 1.3327, with the USD trading marginally higher against the CAD from yesterday's close.

The pair is expected to find support at 1.3283, and a fall through could take it to the next support level of 1.3238. The pair is expected to find its first resistance at 1.3399, and a rise through could take it to the next resistance level of 1.3470.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

USDCHF Momentum Ready To Shift To Bearish

Key Points:

- Long-term wedge ready to slap the USDCHF lower.

- Fundamental bias suggestive of losses moving forward.

- The pair should retreat back to parity.

The Swissy should be gearing up for another reversal in fairly short order as the technical and fundamental biases turn against the pair. Specifically, we continue to see the long-term chart pattern exert its influence and when this is coupled with a number of fundamental developments, downside risks seem to be increasing at a notable rate. As a result, let's take a closer look at the pair to ascertain exactly what may be on offer this week.

As is shown on the daily chart, it is rather plain to see that the USDCHF has been rallying strongly over the past week or so. Additionally, if the EMA bias is anything to go by, this momentum looks to be fairly entrenched which could mean we see even further gains over the impending sessions. However, what is also becoming clear, is that a rather convincing wedge pattern is forming up which would typically indicate precisely the opposite is on the agenda for the Swissy

Indeed, the pair is challenging the upper constraint of this long-term wedge so the question is now, will we see a breakout or will the structure hold firm? From a technical point of view, there is some uncertainty about which of these two outcomes is more likely. On the one hand, the EMA bias and parabolic SAR readings are leaning towards bullish which could mean that a breakout isn't totally impossible. Whilst, on the other hand, stochastics are overbought and the pair has drifted close to the upper Bollinger band which could be indicative of a reversal.

Taking a look at the broader fundamental environment, we have a slightly clearer image of what is likely to be the pair’s next move. Specifically, it appears that the rally was already petering out as it contended with the 100 day moving average and the last two major spikes in buying pressure are simply near-term bursts coming in response to some solid US employment data. As a result, the USDCHF may have much less underlying support than it might at first appear.

Furthermore, there is a strong case suggesting that the Franc should be taking ground back from the greenback based on its safe haven status. In particular, the US’s involvement in Syria and heightened tensions between North Korea and the entire planet dominated headlines last week and this will be bolstering interest in the CHF. Moreover, fears that the stock market is amid a bubble and in danger of correcting will see traders taking a slightly more risk-off approach, likely adding to the Franc’s buoyancy. In fact, we are already seeing the effects of these expectations creeping back into the market as the VIX is at its highest point for 2017 at around the 14.05 mark.

Overall, the forecast for the pair is skewed towards bearish which could result in some decent downside action within the next few sessions. Specifically, if a reversal is seen, the USDCHF should retreat back to parity before the 100 day EMA and the 38.2% Fibonacci level cap losses. As for where the pair moves to from there, it is currently unclear but the aforementioned support zone is by no means unbreakable. As a result, monitor the Swissy closely as these near-term downsides may only be the beginning of a sizable decline.

Euro Likely To Remain Under Pressure As 1.05 Handle Looms

Key Points:

- Euro likely to continue sliding towards the 1.05 handle.

- RSI Still trending lower within neutral territory.

- Watch for a gradual slide to oversold status before we are likely to see a retracement.

The Euro continued to retreat throughout most of last week, as price action was rejected from levels around the 55EMA, despite a stronger than expected EU Retail Sales Result of 0.7% m/m. Much of the move was due to the stronger greenback sentiment in the wake of a sharp fall in the U.S. Unemployment Rate to 4.5%. However, the pair is nearing some key support around the 1.05 handle which could prove to be decisive in the coming week. Subsequently, let’s take a look at last week’s machinations as we attempt to provide some forward guidance.

Last week continued the ongoing depreciation of the Euro as the pair saw the impact of a relatively sharp sentiment swing towards the U.S. Dollar. Subsequently, the market largely ignored the robust EU Retail Sales result of 0.7% m/m and instead focused on the tightening U.S. labour market figures. In particular, a surprise fall in the unemployment rate to 4.5% is indicative of the ongoing tightening within the market as the economy effectively abuts the natural rate of unemployment. Subsequently, this is fuelling rising speculation of near term rate hikes as we view the forward outlook for the Fed. This sentiment swing continued to push the Euro lower and the pair subsequently ended the week around the 1.0589 mark.

Looking ahead, the pair is likely to focus sharply on Fed Chair Yellen’s pending speech as well as the U.S. Core CPI numbers. As the U.S. Labour market continues to firm, so too does the focus upon further rate hikes from the central bank. In particular, the market will be reviewing the CPI figures with a view to second guessing the Fed’s direction in the coming months. In contrast, the EU has little in the way of fundamental data to contribute to the week ahead with the primary event likely to be the ZEW Economic Sentiment result. However, there will be little in the way of volatility from the Eurocentric data and the market’s focus will remains firmly on the greenback side of the pair.

From a technical perspective, the Euro’s ongoing fall has taken it towards a key support level at 1.0494 which breaching would send it sharply lower. This development argues that the corrective phase is not yet over, however, the RSI Oscillator is now nearing oversold levels which suggests that a period of moderation is the likely move in the week ahead. Subsequently, our initial bias for the coming week is neutral but with the caveat to watch for a gradual slide back towards the key 1.05 handle. Support is currently in place for the pair at 1.0572, 1.0495, and 1.0364. Resistance exists on the upside at 1.0677, 1.0783, and 1.0828.

Ultimately, there is little upside momentum to suggest that the Euro is likely to turn around any time soon. The medium term view still suggests a pullback towards the 1.05 handle, before the daily RSI becomes oversold, and we see any chance of a sharp retracement away from further declines. Subsequently, the pair is likely to provide little in the way of respite for the bulls in the short term but keep a close watch on it as markets open on the other side of the Easter holidays.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

EUR/USD

Going into the early hours of yesterday's US segment, the shared currency managed to advance after coming within an inch of connecting with March's opening level at 1.0569. However, despite an earnest attempt, the bulls struggled to surpass the nearby 1.06 handle (bolstered by a H4 resistance area at 1.0607-1.0632).

As highlighted in Monday's report, weekly action shows price extended its pullback from the 2016 yearly opening level at 1.0873. According to this scale, there's little support seen in this market until we reach the 2017 yearly opening level at 1.0515/support area at 1.0333-1.0502. The flipside, of course, is that daily movement recently checked in with demand coming in at 1.0525-1.0576, and indicates that the bulls have space to rally up to a resistance area pegged at 1.0714-1.0683.

Our suggestions: Since we know H4 price is trading beneath 1.06/resistance area at 1.0607-1.0632, and the weekly candles point to further selling, taking a long from the daily demand base at 1.0525-1.0576 is not something our desk is comfortable with. Yet, similarly, taking shorts from the 1.06 neighborhood is also not really a trade we would label high probability, due to March's opening level at 1.0569 sitting only 30 pips away! It doesn't exactly leave a lot of room to play with.

Data points to consider: German ZEW economic statement at 10am. FOMC member Kashkari speaks at 6.45pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

GBP/USD

Strengthened by the daily demand at 1.2323-1.2379, the H4 symmetrical AB=CD (filled arrows) completion point taken from the high 1.2556 managed to hold firm, closing price back above March's opening level at 1.2378 and the 1.24 handle. While we are expecting H4 flow to find some resistance around current price, due to immediate structure seen to the left marked with a green circle at the 1.2423ish range, both the weekly and daily charts show room to advance.

Our suggestions: Given the noted structure, longs from the 1.24 handle could be something to consider. Nevertheless, there is a strong possibility that H4 price could fakeout down to 1.2378, so avoid simply placing a pending buy order and hoping for the best! Instead, wait for price to connect with 1.24 and form a lower-timeframe confirming buy signal (see the top of this report). This will help with stop-loss placement and avoiding the dreaded fakeout. The Initial take-profit target from this region is the H4 mid-way resistance marked at 1.2450.

Data points to consider: UK inflation figures at 9.30am. FOMC member Kashkari speaks at 6.45pm GMT+1.

Levels to watch/live orders:

- Buys: 1.24 region ([waiting for a lower-timeframe confirming signal to form before pulling the trigger is advised] stop loss: dependent on where one confirms this area).

- Sells: Flat (stop loss: N/A).

AUD/USD

Looking at this market from the top/down today, buyers and sellers remain battling for position within the walls of a weekly support area at 0.7524-0.7446. This zone has provided support and resistance since mid-2016, so we do expect to see some buying pressure eventually emerge from here. Along the same vein, daily price found a pocket of bids around the AB=CD (taken from the high 0.7749) 161.8% Fib ext. at 0.7489, which is housed within a daily support area at 0.7449-0.7506 and the noted weekly support area.

Over on the H4 chart, the candles are seen trading above the 0.75 handle after coming within striking distance of demand at 0.7449-0.7475. Should the bulls manage to hold ground beyond 0.75, this would, in our opinion, further confirm bullish strength from the mentioned higher-timeframe support areas.

Our suggestions: Basically, our team is looking for 0.75 to hold. In the event that price retests this number and prints a reasonably sized H4 bullish candle, we would, dependent on the time of day, look to long from here and target 0.7550 as an initial take-profit zone.

Data points to consider: FOMC member Kashkari speaks at 6.45pm GMT+1.

Levels to watch/live orders:

- Buys: 0.75 region ([waiting for a reasonably sized H4 bullish candle to form before pulling the trigger is advised] stop loss: ideally beyond the trigger candle's tail).

- Sells: Flat (stop loss: N/A).

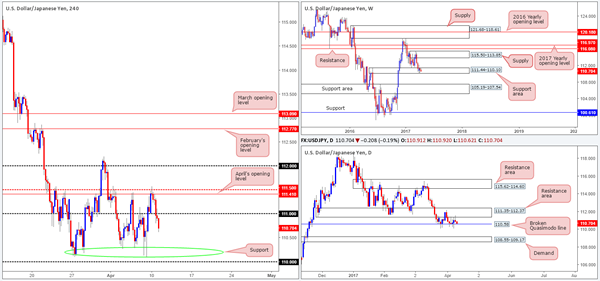

USD/JPY

The USD/JPY spent yesterday's sessions fading from April's opening level at 111.41 which, as you can see, is shadowed closely by the H4 mid-way resistance at 111.50. After running through bids at the 111 handle, the H4 chart shows room for price to attack the support area marked with a green circle at the 110.20ish area, followed closely by the 110 handle.

Although we have to agree the bears do look incredibly enthusiastic at the moment, it might be worth noting that there's a weekly support area in play at 111.44-110.10 and also a daily broken Quasimodo line at 110.58! As such, we wouldn't fancy being a seller in this market right now.

Our suggestions: In view of the unit's close proximity to the noted higher-timeframe structures, our desk is going to be looking for longs around the 110 neighborhood today. An ideal scenario would be for the H4 candles to print a reasonably sized bullish rotation off this number. This would be enough evidence to suggest the buyers are making a play, in our opinion.

Data points to consider: FOMC member Kashkari speaks at 6.45pm GMT+1.

Levels to watch/live orders:

- Buys: 110 region ([waiting for a reasonably sized H4 bullish candle to form before pulling the trigger is advised] stop loss: ideally beyond the trigger candle's tail).

- Sells: Flat (stop loss: N/A).

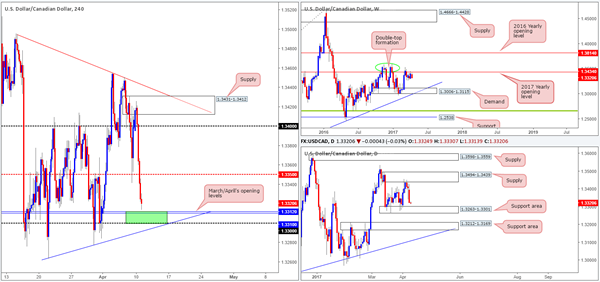

USD/CAD

Weighed on heavily by rising oil prices, the USD/CAD fell sharply yesterday. The 1.34 handle and the H4 mid-way support 1.3350 were both taken out, leaving price free to challenge March/April's opening levels at 1.3310/12.

Technically speaking, this recent downside move should not really come as too much of a surprise since weekly price has spent the best part of a month teasing the underside of the 2017 yearly opening level at 1.3434. While the bears do look to be in a strong position at the moment, one may want to take into account that a daily support area at 1.3263-1.3301 has recently elbowed its way into the spotlight! The zone has offered support to this market since the 16th March and could very well do so again.

Our suggestions: March/April's opening levels at 1.3310/12, coupled with the 1.33 handle and nearby daily support area (green H4 zone), could, in our view, hold this market higher this week despite weekly action suggesting lower prices may be on the horizon. However, before we'd look to commit here, we would require a reasonably sized H4 bullish candle to form out of the zone, showing us that the bulls have interest here.

Data points to consider: FOMC member Kashkari speaks at 6.45pm GMT+1.

Levels to watch/live orders:

- Buys: 1.33/1.3312 ([waiting for a reasonably sized H4 bullish candle to form before pulling the trigger is advised] stop loss: ideally beyond the trigger candle's tail).

- Sells: Flat (stop loss: N/A).

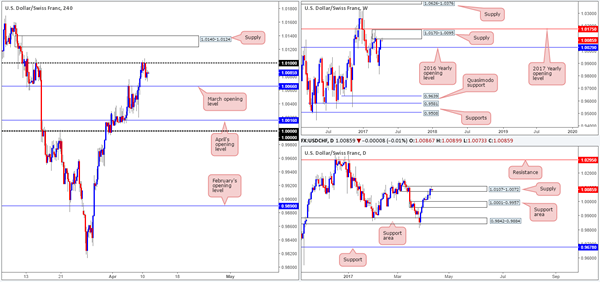

USD/CHF

Try as it might, the Swissy failed to muster enough strength to breach the 1.01 handle yesterday. This might have had something to do with the fact that the daily candles are seen trading within the walls of a supply zone penciled in at 1.0107-1.0072, and also weekly price seen teasing the underside of a supply formed at 1.0170-1.0095.

Before traders look to press the sell button, however, we would strongly recommend waiting for March's opening level at 1.0066 to be consumed. Not only would this confirm downside strength, it would also open the path south to April's opening level at 1.0016 and parity (1.0000), which also represents the top edge of a daily support area (the next downside target on that timeframe).

Our suggestions: A decisive H4 close beyond 1.0066, followed up with a retest as resistance and a reasonably sized H4 bearish candle, would, in our estimation, be enough evidence to warrant a short position. Under these circumstances, stops are usually placed a few pips beyond the candle's wick.

Data points to consider: FOMC member Kashkari speaks at 6.45pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for H4 price to engulf 1.0066 and then look to trade any retest seen thereafter ([waiting for a reasonably sized H4 bearish candle to form following the retest is advised] stop loss: ideally beyond the trigger candle's wick).

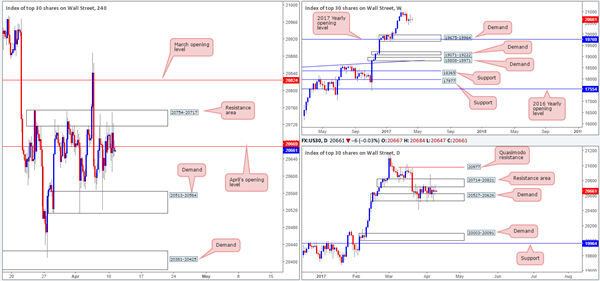

DOW 30

The H4 resistance area at 20754-20717 managed to hold ground yesterday, consequently pushing the index back below April's opening level at 20669. While a short from this number could be something to consider, let's be mindful to the fact that the daily candles have experienced a significant amount of choppy action between demand plugged at 20527-20626 and the resistance area at 20714-20821 since the 22nd March. Although daily action indicates that shorts may be risky, we should remind ourselves that there is little weekly structure seen until the index crosses swords with demand at 19675-19964, which happens to intersect with the 2017 yearly opening level at 19769.

Our suggestions: For those willing to take the risk of selling into a daily demand, a short from 20669 does have the backing of weekly flow at the moment. Waiting for a H4 bearish candle to form off 20669 is advised before pressing the sell button. That way stops can be placed beyond the rejection candle's wick.

Data points to consider: FOMC member Kashkari speaks at 6.45pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 20669 level ([waiting for a reasonably sized H4 bearish candle to form before pulling the trigger is advised] stop loss: ideally beyond the trigger candle's wick).

GOLD

As anticipated, the yellow metal bounced nicely from between April and March's opening lines at 1245.9/1248.0 and rallied to a high of 1257.0 on the day. With H4 price now seen meandering between the noted monthly levels and resistance planted at 1260.0, where does one step from here? Well, with weekly price recently crossing swords with resistance at 1263.7, and daily movement trading within supply lodged at 1265.2-1252.1, the path of least resistance is south.

Our suggestions: Based on the above notes, we see two possible scenarios playing out:

Wait and see if H4 price tests resistance at 1260.0. In the event that it holds ground and forms a reasonably sized H4 bearish candle, a short from here is valid.

Assuming that the monthly levels at 1245.9/1248.0 are taken out, the next area on the hit list is a support zone formed at 1235.7-1238.1. Should price retest the underside of these levels and print a reasonably sized H4 bearish candle, a short from here is also valid.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1260.0 region ([waiting for a reasonably sized H4 bearish candle to form before pulling the trigger is advised] stop loss: ideally beyond the trigger candle's wick). Watch for H4 price to engulf 1245.9/1248.0 and then look to trade any retest seen thereafter ([waiting for a reasonably sized H4 bearish candle to form following the retest is advised] stop loss: ideally beyond the trigger candle's wick).

European Open Briefing: Most Asian Stock Markets Declined Overnight

Global Markets:

- Asian stock markets: Nikkei down 0.65 %, Shanghai Composite fell 0.35 %, Hang Seng declined 0.90 %, ASX 200 gained 0.40 %

- Commodities: Gold at $1258 (+0.30 %), Silver at $17.95 (+0.15 %), WTI Oil at $63.10 (+0.10 %), Brent Oil at $65.08 (+0.15 %)

- Rates: US 10 year yield at 2.34, UK 10 year yield at 1.08, German 10 year yield at 0.21

News & Data:

- Australia NAB Business Conditions Mar: 14 (prev 9)

- Australia NAB Business Confidence Mar: 6 (prev 7)

- Australia ANZ Roy Morgan Consumer Confidence 9-Apr: 114.8 (prev 111.1)

- UK BRC Sales Like-For-Like (YoY) Mar: -1.0% (exp -0.3%; prev -0.4%)

- PBoC Fixes USDCNY Reference Rate At 6.8957 (prev fix 6.9042 prev close 6.9050)

- Global stocks pressured, safe assets up on rising geopolitical risks – RTRS

- Oil hits five-week top on geopolitical tensions, strong demand – RTRS

Markets Update:

Most Asian stock markets declined overnight, while safe havens were once again in demand. The Japanese Yen extended gains as USD/JPY fell from 111.00 to a low of 110.58. Meanwhile, Gold recovered to 1257. Geopolitical tensions are keeping traders nervous, and there is little risk appetite in the market. Gold should therefore remain in demand and retest the recent high at 1270 soon.

The commodity currencies are under pressure as well. The Australian Dollar managed to recover slightly yesterday, but reversed those gains overnight as it fell back to 0.7495. Worse than expected NAB business confidence weighed on the AUD too. Following the break below 0.75 support, a test of 0.74 seems likely in the short-term.

The British Pound recovered a bit against the Dollar. The UK will release its inflation numbers for March today, and the traders are anticipating a higher number. Intraday, resistance is seen at 1.2450 and 1.25, while decent support is noted in the area between 1.2350 and 1.2370.

Upcoming Events:

- 09:30 GMT – UK CPI

- 10:00 GMT – German ZEW Economic Sentiment

- 10:00 GMT – Euro Zone Industrial Production

- 10:00 GMT – Euro Zone ZEW Economic Sentiment

- 15:00 GMT – US JOLTs Job Openings

- 18:45 GMT – FOMC Member Kashkari speaks

Elliott Wave View: Crude Oil (CL_F) Waiting For Pullback

Short term Elliott Wave view in Crude Oil (CL_F) suggests that cycle from 3/22 low (47.01) is unfolding as a double three Elliott wave structure where Minute wave ((w)) ended at 50.85 and Minute wave ((x)) ended at 49.88. Minute wave ((y)) is in progress and the internal is unfolding also as a double three Elliott wave structure where Minutte wave (w) ended at 52.94 and Minutte wave (x) pullback ended at 51.49. Near term, while pullbacks stay above 51.51, focus is on 53.71 – 54.61 area to complete Minor wave 1 and end cycle from 3/22 low, then Crude Oil should pullback in Minor wave 2 to correct cycle from 3/22 low before the rally resumes. We don’t like selling CL_F and expect buyers to appear once Minor wave 2 pullback is complete in 3, 7, or 11 swing for an extension higher.

Market Morning Briefing: Nothing Changed In The Global Scenario

STOCKS

Dow (20658.02, +0.01%) is almost stable and in a sideways consolidation mode as expected. Some steady movement in the 20780-20500 region is possible in the next couple of sessions before breaking on either side.

Dax (12200.52, -0.20%) is testing support near 12200 or could test lower support near 12100 from where an immediate bounce is expected in the coming sessions. But on a medium term some sideways movement could be expected as there is not much scope on the upside beyond 12400 just now. A dip below 12100, could take it towards 12000 or lower before recovering again.

Asia-Pac is weak with the Chinese and Japanese stocks looking weak.

Shanghai (3262.10, -0.22%) came off from daily resistance near 3280 and while that holds, we could see a fall towards 3250 again before bouncing back towards 3300 in the medium term.

Nikkei (18708.49, -0.48%) has not been able to sustain at higher levels and may re-test 18600 or lower in the near term. A sustained movement below 18600, if seen, could eventually lead to a fall in the index for the medium term.

Nifty (9181.45, -0.18%) could fall to 9130 today before possibly bouncing back again from there in the coming sessions.

COMMODITIES

Gold (1251) was almost unchanged and it keep trading in the narrow range of 1237-1263, which may continue for some days. Global cues are in favor of gold as the break below 100.50 for Dollar Index (101) could be resulted in good gains for bullion. We have been expecting 1237 for gold to hold for some time and gradual buying at lower levels can’t be ruled out as buyers are taking every dip as a further opportunity for buying.

Silver (17.95) has tested its support at 17.70 and settled marginally higher. Immediate trading range could be 17.80-18.30 but a close below 17.70 could open up 17.50 as well. Overall silver looks weak but we need to wait for confirmation for immediate directional clarity.

Copper (2.61) has been stuck in the range of 2.55-2.70 with no visible intent for a breakout. Range bound trading may go on for some time. In the medium term 2.55-57 are going to be a strong support now but a close below that could open up 2.50 and 2.45 levels respectively.

Brent (56.01) and WTI (53.07) had closed above their respective resistances, which has opened up higher levels of 57 and 54. Immediate trading range for Brent and WTI could be 54-56.40 and 51-53 and considering the short term overbought state, possibility of a near term correction can’t be ignored.

In case of any surplus in U.S crude inventories, the upside in the near term may be limited to 56.40 and 53. The trend is bullish in the near term time frame and any corrective fall may add fresh longs at the lower levels.

FOREX

Nothing changed in the global scenario as the political tension over Syria and North Korea lingers. Dollar stays strong against the majors and Rupee may conditionally weaken a bit more.

Dollar Index (101.05) is stalling near our resistance of 101.55-75 and only a successful break above the resistance can open up further upside. In case of a failure here, a gradual decline towards 100.00 can be seen. Prefer to watch the price action here for clarity at this point.

Euro (1.0585) is timidly holding above the support of 1.0550 till now but no strength is visible yet. The persistent decline in the German-US yield spreads (check Interest Rates section) keep the currency weak and if 1.0550 breaks, the decline may extend to 1.0450.

Dollar Yen (110.65) has been rejected exactly from our resistance of 111.60. Unless an immediate break above 111.60 is seen, the risk of a break below the support of 111.10-109.90 may be back. No clear bias in the near term though the trend remains down in the medium term.

Pound (1.2419) has bounced back from our support of 1.2350, increasing the chances of further sideways movement in the broader range of 1.2350-1.2600. Immediate resistance comes at 1.2465 which may be tested soon.

Aussie (0.7495) sustains the lower levels with no apparent strength. Our downside target of 0.7450 remains unchanged with even 0.7375 a possibility.

Dollar-Rupee (64.56) has made a high of 64.5750 yesterday, very close to our immediate target of 64.60. As the pair trades at 64.72 in the NDF at this moment, a successful break above 64.60-70 in the onshore market may push it higher towards the major resistance of 65.10-25 in the next few days.

INTEREST RATES

The US yields do not look as if they are willing to move up just now contrary to our expectation of a rise mentioned yesterday. Some consolidation near current levels is possible for a few more sessions before moving up sharply. The yields have again moved down to re-test support levels and may not have much scope on the upside just now.

The 5YR (1.88%), 10Yr (2.35%) and the 30YR (2.98%) are down from 1.91%, 2.38% and 2.98% respectively.

The German-US 2Yr (-2.10%) and 10Yr (-2.14%) have moved up slightly but overall looks bearish over the medium term. A slight rise could be expected over today and tomorrow followed by a dip back toward current levels or even lower.

The 10Yr GOI (7.0569%) could rise towards 7.15-7.20% in the next 4-5 sessions before dipping towards 7%.

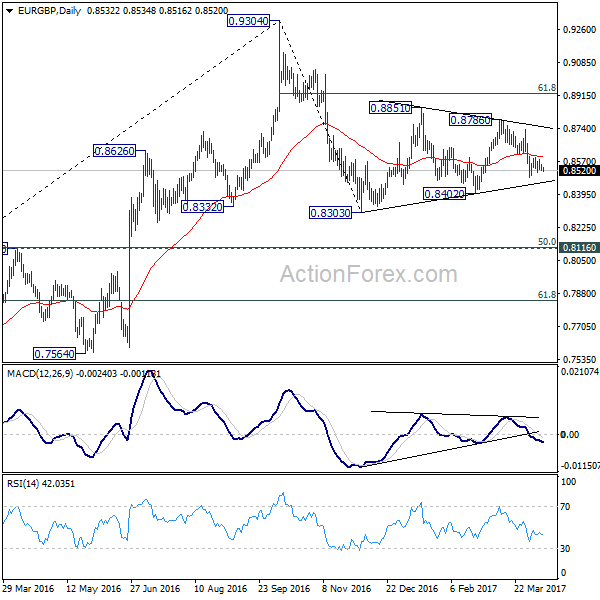

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8520; (P) 0.8536; (R1) 0.8549; More...

EUR/GBP dips mildly today but stays above 0.8483 temporary low. Intraday bias remains neutral at this point. As noted before, decline from 0.8786 could be developing into the third leg of the whole corrective pattern from 0.9304. And hence, deeper fall is expected ahead. On the downside, break of 0.8483 will turn bias to the downside for 0.8402 support first. Decisive break there should confirm our bearish view and target 0.8303 and below. As fall from 0.9304 is viewed as a corrective move, we'd expect strong support at 0.8116/20 cluster support to contain downside and bring rebound. On the upside, above 0.8604 minor resistance will delay the bearish case. That is, one more recovery will be seen to complete a five wave triangle pattern fro 0.8303 before completion.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Such decline is likely ready to resume and should make a new low below 0.8303. At this point, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

Euro Sees Renewed Selling, British Pound Resilience to be Tested by UK CPI

Some selling pressure is seen in Euro in Asian session as the common currency is dipping through Monday's low against Yen and Sterling. French election in April and May is the main focus for the common currency for now. But it should be noted that instead of political uncertainties, Euro's current selloff is more due to adjustments on ECB expectations. That is, there is little chance for ECB to raise interest rate soon in spite of the "hawkish twist" back in March. There are talks that Euro could be given a lift after French election but that would likely be just temporary. The situation of the British Pound is indeed quite different as Sterling has survived news of Brexit and stayed firm. BoE outlook is the main support for the Pound as Kristin Forbes voted for a rate hike back in March. And that was accompanied by stronger than expected February headline inflation reading. UK CPI release today will be importantly to decide whether Sterling can hold on to its resilience.

ECB Draghi: 2016 was a good year

ECB President Mario Draghi said in the central bank's annual report that 2016 "ended with the economy on its firmest footing since the crisis," even though the year began "shrouded in economic uncertainty". The report noted that the scaling back of asset purchase from EUR 80b per month to EUR 60b "reflected the success of our actions earlier in the year: growing confidence in the euro area economy and disappearing deflation risks". However, overall, the Eurozone economy's recovery is still dependent on massive support from the central bank. And the report also reiterated the calls on governments' effort on fiscal reforms.

Fed Yellen: Policy stance closer to neutral

Dollar fails to extend last week's rally while stocks and yields also lost some momentum. Fed chair Janet Yellen said yesterday that the central bank has shifted its focus the economy is closing to the targets of inflation and employment. She said that before, Fed had to "press down on the gas pedal trying to give the economy all of the oomph that we possibly could." But now, Fed is trying to "give it some gas, but not so much that we're pushing down hard on the accelerator." And, the "appropriate stance of policy" is now closer to "neutral". But she also emphasized not be to "ahead" nor "behind" the curve. Or, Fed would be in a position to "have to raise rates rapidly, which could conceivably cause a recession".

Australia business conditions improved, confidence dropped

Australia NAB business confidence rose 5 pts to 14 in March, hitting the highest level since the global financial crisis. But business confidence dropped 1 pt to 6. NAB noted that "the bounce in business conditions this month came as a bit of a surprise, especially the big improvement in Queensland in light of the likely disruptions from Cyclone Debbie in late March." And, "one possibility is that 'Debbie' is having the unexpected effect of overstating conditions in March given that the cyclone coincided with a lower response rate from firms in Northern Queensland.". But overall, "conditions have improved almost across the board to levels that suggest a strong economy in the near term."

On the data front...

UK BRC retail sales monitor dropped -1.0% yoy in March. Australia NAB business confidence dropped to 6 in March. UK inflation data will be a main focus for today as CPI, RPI and PPI will be released. Germany will release ZEW economic sentiment while Eurozone will release industrial production. No important economic release is scheduled for US session.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8520; (P) 0.8536; (R1) 0.8549; More...

EUR/GBP dips mildly today but stays above 0.8483 temporary low. Intraday bias remains neutral at this point. As noted before, decline from 0.8786 could be developing into the third leg of the whole corrective pattern from 0.9304. And hence, deeper fall is expected ahead. On the downside, break of 0.8483 will turn bias to the downside for 0.8402 support first. Decisive break there should confirm our bearish view and target 0.8303 and below. As fall from 0.9304 is viewed as a corrective move, we'd expect strong support at 0.8116/20 cluster support to contain downside and bring rebound. On the upside, above 0.8604 minor resistance will delay the bearish case. That is, one more recovery will be seen to complete a five wave triangle pattern fro 0.8303 before completion.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Such decline is likely ready to resume and should make a new low below 0.8303. At this point, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Mar | -1.00% | -0.50% | -0.40% | |

| 1:30 | AUD | NAB Business Confidence Mar | 6 | 7 | ||

| 6:00 | JPY | Machine Tool Orders Y/Y Mar P | 9.10% | |||

| 8:30 | GBP | CPI M/M Mar | 0.30% | 0.70% | ||

| 8:30 | GBP | CPI Y/Y Mar | 2.30% | 2.30% | ||

| 8:30 | GBP | Core CPI Y/Y Mar | 1.90% | 2.00% | ||

| 8:30 | GBP | RPI M/M Mar | 0.40% | 1.10% | ||

| 8:30 | GBP | RPI Y/Y Mar | 3.20% | 3.20% | ||

| 8:30 | GBP | PPI Input M/M Mar | -0.10% | -0.40% | ||

| 8:30 | GBP | PPI Input Y/Y Mar | 17.00% | 19.10% | ||

| 8:30 | GBP | PPI Output M/M Mar | 0.10% | 0.20% | ||

| 8:30 | GBP | PPI Output Y/Y Mar | 3.40% | 3.70% | ||

| 8:30 | GBP | PPI Output Core M/M Mar | 0.20% | 0.00% | ||

| 8:30 | GBP | PPI Output Core Y/Y Mar | 2.50% | 2.40% | ||

| 8:30 | GBP | House Price Index Y/Y Feb | 6.10% | 6.20% | ||

| 9:00 | EUR | Eurozone Industrial Production M/M Feb | 0.10% | 0.90% | ||

| 9:00 | EUR | German ZEW (Economic Sentiment) Apr | 14.8 | 12.8 | ||

| 9:00 | EUR | German ZEW (Current Situation) Apr | 77.5 | 77.3 | ||

| 9:00 | EUR | Eurozone ZEW (Economic Sentiment) Apr | 25 | 25.6 |

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD was indecisive yesterday. The bias is neutral in nearest term. Overall price is still in a bearish phase since the false break above 1.0873 key resistance two weeks ago but as you can see on my H4 chart below price respecting a trend line support which is a good place to buy with a tight stop loss as a clear break below the trend line support and 1.0570 area would expose 1.0500 region. Immediate resistance is seen around 1.0620. A clear break above that area could trigger further bullish pressure testing 1.0700 region. On the downside, a clear break and daily close below 1.0500 would expose 1.0350 area. Overall I remain neutral.

GBPUSD

The GBPUSD failed to continue its bearish momentum yesterday topped at 1.2428. The bias is neutral in nearest term. The bearish outlook after broke below the triangle (see my H1 chart below) remains valid with 1.2450 as key resistance (H1 EMA 200). A clear break above that area would nullify the bearish scenario testing 1.2500 region. Immediate support is seen around 1.2375. A clear break below that area would expose 1.2300 region. Overall I remain neutral.

USDJPY

The USDJPY attempted to push higher yesterday topped at 111.57 but closed lower back below 111.30 key resistance and hit 110.62 earlier today in Asian session. The bias is neutral in nearest term probably with a little bearish bias testing 110.10 key support which is a good place to buy with a tight stop loss as a clear break and daily close below that area could trigger further bearish pressure testing 108.50 region. On the upside, 111.30 remains a key resistance. Any sustained movement above that level could trigger further bullish pressure testing 112.00 or higher.

USDCHF

The USDCHF was indecisive yesterday. The bias is neutral in nearest term but overall price is still in a bullish phase with 1.0020 – 1.0060 as key support area targeting 1.0170 area. A clear break and daily close above that area would expose 1.0250 or higher. On the downside, a clear break and daily close back below 1.0020 would be a threat to the bullish phase testing 0.9970 region. Overall I remain neutral.