Sample Category Title

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0011; (P) 1.0044; (R1) 1.0081; More.....

Intraday bias in USD/CHF remains on the upside with 1.0007 minor support intact. Rise from 0.9812 should target 1.0169 resistance first. As noted before, corrective decline fall from 1.0342 should have finished with three waves down to 0.9812 already. Break of 1.0169 should confirm this bullish case and target a test on 1.0342 high. On the downside, below 1.0007 minor support will turn bias neutral and bring retreat before staging another rally.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

Price Levels & Exuberance

The final 30 minutes of Wednesday's S&P500 cash session saw the biggest decline in the index since September. The sell-off across US indices (and global futures) was largely attributed to the release of the March FOMC minutes and House Speaker Paul Ryan's comments on the remaining obstacles facing Trump's tax stimulus. The quotes below indicate FOMC officials have grown bolder in expressing their doubts with equity valuations, something similar to Greenspan's irrational exuberance speech 21 years ago.

Technical analysts will tell you the above explanations are fundamental triggers for developments largely apparent in the charts. The 20,800 and 2370 territories in the Dow30 and SP500 acted as previous support, now resistance levels, while the USD index faces rising pressure at 100.80s. We could elaborate further on the relevant pressure points in US 10-year yields and individual USD pairs, but... you get the picture.

As we approach tomorrow's US jobs report, some decisions may have to be made with regards to our existing USD and cross pair Premium trades. Some may say Friday's report is least important of the year as there is no Fed meeting scheduled for this month. The upside surprise in this week's ADP release may suggest the figures could come in above the 180K expected, following the 235K in February. But as we saw in the last report, USD and yields are increasingly to the mercy of the earnings figures. 4 Premium trades remain in FX and 2 in indices. The 2 trades in commodities have not and will not be touched for quite some time.

Trade Idea: EUR/GBP – Sell at 0.8620

EUR/GBP - 0.8545

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Sell at 0.8620, Target: 0.8520, Stop: 0.8660

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.8620, Target: 0.8520, Stop: 0.8660

Position : -

Target : -

Stop : -

Euro found support at 0.8511 and has rebounded again, retaining our view that further consolidation above last week’s low at 0.8485 would be seen and another bounce to 0.8590-00 cannot be ruled out, however, renewed selling interest should emerge around 0.8620-25, bring another decline later, below said support at 0.8485 would add credence to our view that top has been formed at 0.8788 and bearishness remains for this fall from there to bring retracement of early upmove, hence further weakness to 0.8470 would be seen but oversold condition should prevent sharp fall below 0.8450, risk from there has increased for a rebound to take place later.

In view of this, we are looking to sell euro on recovery as 0.8620-25 should limit upside. Only above 0.8660-65 would defer and suggest low is possibly formed, risk rebound to 0.8680, then 0.8700 but price should falter below said resistance at 0.8735, bring further choppy trading later.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Canadian Dollar Shrugs off Soft Building Permits

USD/CAD is almost unchanged in the Thursday session, as the pair trades at 1.3430. On the release front, Canadian Building Permits posted a sharp decline of 2.5%, well short of the estimate of a 1.4% gain. In the US, unemployment claims dropped sharply to 234 thousand, easily beating the forecast of 251 thousand. The week wraps up with a host of employment indicators. Canada will publish Employment Change and the unemployment rate, while the US releases three key events - Nonfarm Employment Change, Average Hourly Earnings and the unemployment rate.

The Canadian dollar continues to struggle, and a major reason is weak oil prices. Despite OPEC cutting production levels, the world remains awash in oil, as increasing US production has offset the OPEC cuts. US Crude Inventories continue to show surpluses, most of which have been higher than the forecast. This was the case again last week, with US crude inventories posting a strong gain of 1.6 million. The indicator has posted 12 surpluses in the last 13 weeks, which has helped keep oil prices close to the $50 level.

The Federal Reserve released the minutes of its March policy meeting on Wednesday. At that meeting, the Fed raised rates a quarter-point to 0.75%, but the dovish rate statement disappointed the markets, triggering broad losses for the US dollar. In the minutes, policymakers noted upside risk to the US economy, but remained divided on whether inflation will rise to the Fed target of 2.0%. Most policymakers were in favor of taking steps to trim the $4.5 trillion balance, which has ballooned since the Fed implemented its aggressive quantitative easing program back in 2008. So what's next for the Fed? According to the CME's Fed Watch, the odds of a rate hike at the May meeting are just 5 percent, while the likelihood of a rate hike in June stand at 63 percent. Last week, FOMC member Eric Rosengren called for three more hikes, saying the Fed should raise rates in June, September and December. Rosengren said that employment and inflation levels were close to the Fed's targets, and that three additional hikes were needed in order to prevent the US economy from overheating. However, a majority of FOMC members are in favor of just two more hikes this year.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.33; (P) 110.89; (R1) 111.25; More....

USD/JPY is still bounded in range of 110.10/112.19 and intraday bias remains neutral at this point. On the downside, break of 110.10 will resume the whole corrective decline from 118.65 and target 50% retracement of 98.97 to 118.65 at 108.81. On the upside, however, break of 112.19 resistance will indicate short term reversal and turn bias back to the upside for 115.49 resistance.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.16) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

Dollar Range Bound as Trump and Xi Meet, ECB Draghi Said Policies Still Appropriate

Dollar trades in rather tight range as the markets await the summit between US President Donald Trump and China President Xi Jinping. They will greet each other at Trump's Mar-a Lago retreat in Florida late in the afternoon and dine together. The summit will conclude with a working lunch tomorrow. Pressure is on Trump's shoulder to deliver something concrete out of the meeting. Those would include bringing jobs "stolen" by the Chinese back to the US, ending China's "currency manipulation", push China to use its "great influence" on North Korea, etc. Some market participants might have high expectation on the outcome of the summit. But other might just prefer Trump to move his focus back to tax reform, which is, in our view, more essential in determining the financial markets' direction.

Released from US, initial jobless claims dropped 25k to 234k in the week ended April 1, below expectation of 250k. Prior week's figure was revised up by 1k to 259k. Initial claims have now stayed below 300k level for the 109 straight week, the second longest streak since 1970s. Four week moving average dropped 4.5k to 250k. Continuing claims dropped 24k to 2.03m in the week ended March 25. Challenger job cuts dropped -2.0% yoy in March. From Canada, building permits dropped -2.5% mom in February.

Fed Williams: Takes around five year to shrink balance sheet

San Francisco Fed President John Williams said that it may take around five years for Fed to wind down the $4.5T balance sheet. And, "towards the end of this year would be a good time to take that next step" of normalization of the balance sheet, "assuming the economy progresses.

The minutes of the March FOMC meeting was overall hawkish. They outlined the steps to shrink the USD 4.5T balance sheet. The minutes noted that the reduction has to be "gradual and predictable", accomplished by "phasing out" or reinvestment and such process could start "later this year". No detail is provided yet but the minutes said Fed will "its deliberations on reinvestment policy during upcoming meetings and would release additional information as it becomes available."

Meanwhile, some officials are concerned that if unemployment falls further, it could pose "significant upside risk" of inflation. The minutes also showed "some participants viewed equity prices as quite high relative to standard valuation measures." More on FOMC Minutes: FOMC Might Begin Shrinking Balance Sheet In Late-2017

ECB Draghi: Reassessment of policy stance not warranted

ECB President Mario Draghi expressed today his confidence that "our policy is working and that the outlook for the economy is gradually improving." However, he emphasized that there was no "sufficient evidence to materially alter our assessment of the inflation outlook". Therefore, "reassessment of the current monetary policy stance is not warranted at this stage." And those include "interest rates, asset purchases and forward guidance."

ECB chief economist Peter Praet said that introducing the idea of a rate hike will undo some of the stimulus because of changed market expectations. He said that "if investors start perceiving that the path of the policy rate is subject to upward uncertainty ... long-term interest rates will be pushed higher and asset purchases will become less effective." On the other hand, separately, Bundesbank head Jens Weidmann said that the time for ECB to scale back stimulus was fast-approaching.

Eurogroup Dijsselbloem urged UK and EU to stay away from the cliff

Eurogroup head Jeroen Dijsselbloem urged UK and EU to keep future trade relationship "as close as possible". He said that "the longer I think about it, the longer we study all the topics that need to be negotiated, the more worried I get. It is hugely complex, it is going to take a lot of effort from both sides to try and manage it." And, he urged to "try to stay away from the cliff of the [World Trade Organization] standards" as they would be very damaging to trade between the different regions."

Yesterday, the European Parliament voted 516-133, with 50 abstentions, for the phased approach of Brexit negotiation, rather than parallel. European Union chief negotiator Michel Barnier said yesterday that "parallel talks" on Brexit terms and future trade relationship is "a very risky approach". And, he emphasized that to succeed, "we need on the contrary to devote the first phase of negotiations exclusively to reaching an agreement on the principles of the exit."

Release from Europe, Eurozone retail PMI dropped to 49.5 in March. Germany factory orders rose 3.4% mom in February. Swiss CPI was unchanged at 0.6% yoy in March.

BoJ Kuroda favorite to get second term

In Japan, it's reported that BoJ Governor Haruhiko Kuroda is Prime Minister Shinzo Abe's favorite for the job. And Kuroda will likely renew for another five year term next year. Reuters quoted unnamed source saying that Abe trusts Kuroda and believed he did a "very good job". Also, the it's believed that Abe's administration is happy with impact of BoJ's QQE program that keep government borrowing costs very low. The selection process for the next BoJ Governor will start in the second half of this year.

Release in Asia, Japan consumer confidence rose to 43.9 in March. China Caixin PMI services dropped to 52.2 in March.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.33; (P) 110.89; (R1) 111.25; More....

USD/JPY is still bounded in range of 110.10/112.19 and intraday bias remains neutral at this point. On the downside, break of 110.10 will resume the whole corrective decline from 118.65 and target 50% retracement of 98.97 to 118.65 at 108.81. On the upside, however, break of 112.19 resistance will indicate short term reversal and turn bias back to the upside for 115.49 resistance.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.16) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:45 | CNY | Caixin PMI Services Mar | 52.2 | 53.2 | 52.6 | |

| 05:00 | JPY | Consumer Confidence Index Mar | 43.9 | 43.4 | 43.1 | |

| 06:00 | EUR | German Factory Orders M/M Feb | 3.40% | 3.50% | -7.40% | -6.80% |

| 07:15 | CHF | CPI M/M Mar | 0.20% | 0.20% | 0.50% | |

| 07:15 | CHF | CPI Y/Y Mar | 0.60% | 0.50% | 0.60% | |

| 08:10 | EUR | Eurozone Retail PMI Mar | 49.5 | 49.9 | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 11:30 | USD | Challenger Job Cuts Y/Y Mar | -2.00% | -40.00% | ||

| 12:30 | CAD | Building Permits M/M Feb | -2.50% | 1.40% | 5.40% | 5.80% |

| 12:30 | USD | Initial Jobless Claims (APR 01) | 234K | 250k | 258k | 259K |

| 14:30 | USD | Natural Gas Storage | 10B | -43B |

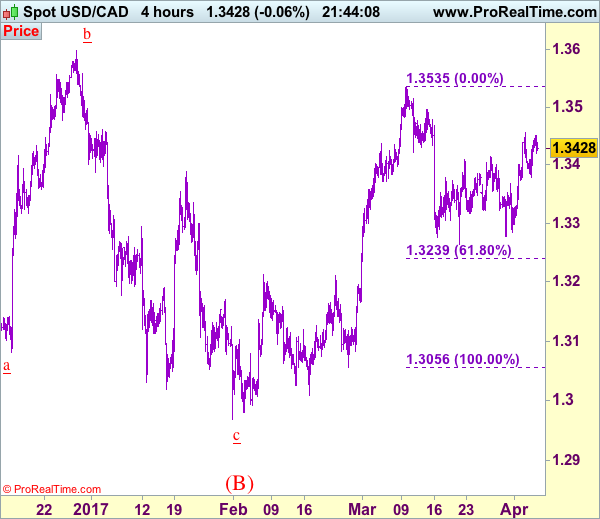

Trade Idea: USD/CAD – Buy at 1.3375

USD/CAD - 1.3434

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Buy at 1.3375, Target: 1.3550, Stop: 1.3315

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.3375, Target: 1.3550, Stop: 1.3315

Position: -

Target: -

Stop:-

As the greenback staged a strong rebound after holding above indicated previous support at 1.3264, consolidation with upside bias is seen and above 1.3456 resistance would add credence to our view that the correction from 1.3535 has ended and bring further gain to 1.3495-00 but break there is needed to signal upmove has resumed for retest of 1.3535, once this level is penetrated, this would extend recent recent upmove from 1.2969 to 1.3575-80 but previous chart resistance at 1.3599 should hold on first testing.

In view of this, we are looking to buy on pullback as 1.3370-75 should limit downside and bring another rise. Below 1.3340 would abort and suggest the rebound from 1.3264 has ended instead, bring further fall to 1.3300-10 but said support at 1.3264 should remain intact. Only a break below this level at 1.3264 would shift risk back to downside for the fall from 1.3535 to extend weakness to 1.3235-40 (61.8% Fibonacci retracement of 1.3056-1.3535) and then 1.3200-10.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

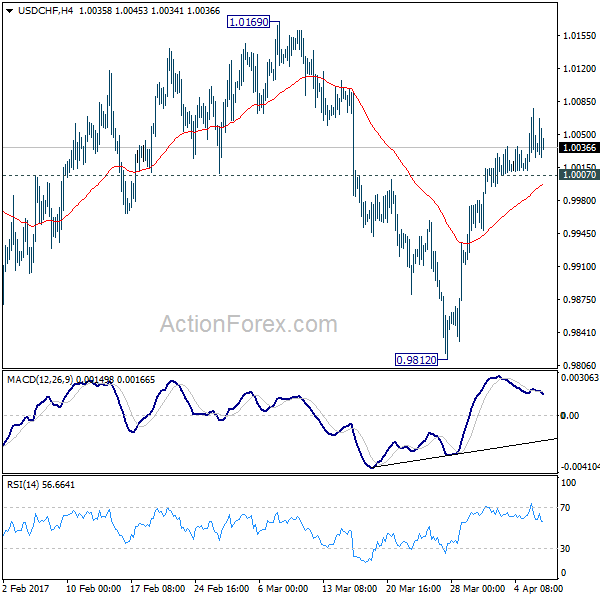

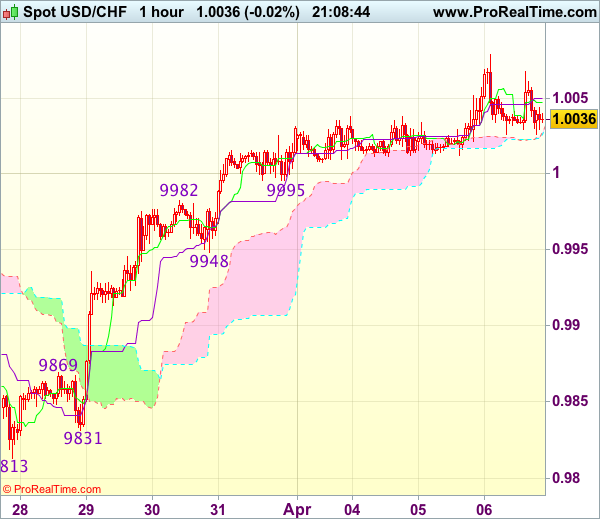

Trade Idea Update: USD/CHF – Buy at 0.9950

USD/CHF - 1.0039

Original strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after last week’s rally above 1.0003 resistance, suggesting recent rise from last week’s low at 0.9813 is still in progress and bullishness remains for this move to 1.0080, then towards previous resistance at 1.0109, however, loss of upward momentum should prevent sharp move beyond latter level and reckon 1.0140-50 would hold, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as support at 0.9948 should limit downside. Below 0.9925-30 would abort and signal top is formed instead, bring correction to 0.9905-10 but reckon previous resistance at 0.9869 would hold from here.

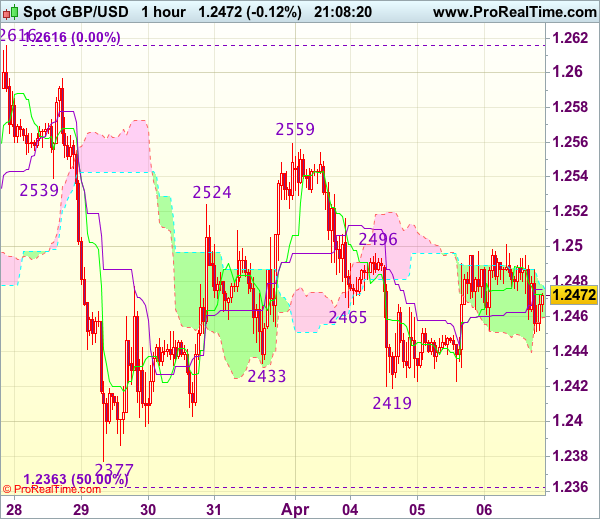

Trade Idea Update: GBP/USD – Hold short entered at 1.2465

GBP/USD - 1.2466

Original strategy :

Sold at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

New strategy :

Hold short entered at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

Cable’s rebound after holding above support at 1.2419 suggests further consolidation above this level would be seen, however, as long as indicated resistance at 1.2500 holds, mild downside bias remains for another fall, below said support at 1.2419 would bring test of 1.2400 but break there is needed to add credence to our view that the rebound from 1.2377 has ended at 1.2559, bring further fall towards support at 1.2377. Looking ahead, only a drop below 1.2377 would confirm the fall from 1.2616 is still in progress for subsequent decline towards key support at 1.2335.

In view of this, we are holding on to our short position entered at 1.2465 but one should exit on such decline. Only break of said resistance at 1.2500 would abort and suggest low has been formed instead, risk a stronger rebound to 1.2525-30, then towards resistance at 1.2559.

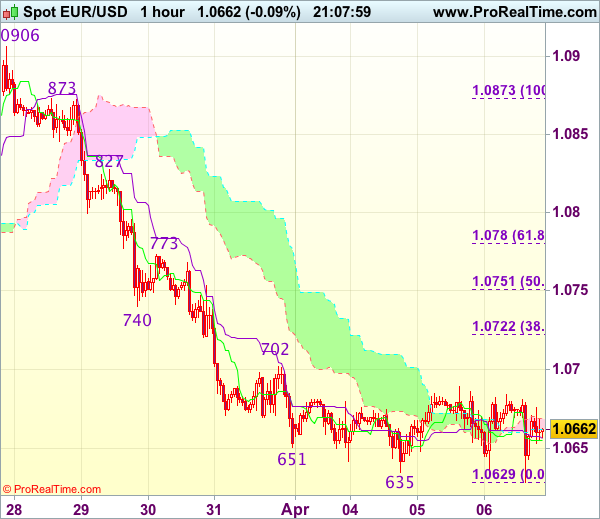

Trade Idea Update: EUR/USD – Sell at 1.0725

EUR/USD - 1.0659

Original strategy :

Sell at 1.0725, Target: 1.0610, Stop: 1.0760

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0725, Target: 1.0610, Stop: 1.0760

Position : -

Target : -

Stop : -

As the single currency has remained under pressure after recent selloff, bearishness remains for the decline from 1.0906 to extend further weakness to 1.0620, then test of previous chart support at 1.0600, however, a sustained breach below the latter level is needed to retain downside bias for subsequent selloff to 1.0570-75 first.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0720-30 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.